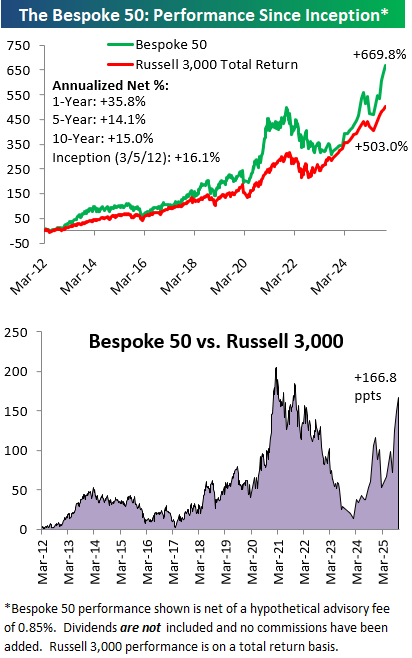

The Bespoke 50 Growth Stocks – 10/23/25

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 11 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Q3 2025 Earnings Conference Call Recaps: CBRE (CBRE)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers CBRE’s (CBRE) Q3 2025 earnings call.

![]()

CBRE (CBRE) is the world’s largest commercial real estate services and investment firm. The company manages billions of square feet of client space and roughly $156 billion in assets under management. CBRE’s scale and global reach spanning over 100 countries give it unique insight into property market cycles, corporate occupier trends, and the intersection of real estate with technology, sustainability, and infrastructure development. Its work increasingly overlaps with megatrends like data-center growth, automation, and AI-driven building operations. CBRE delivered another strong quarter, with core EPS up 34%, prompting management to raise full-year guidance. Data centers were a standout, generating $700 million in quarterly revenue, up 40% year-over-year. Advisory Services leasing grew 17%, led by industrial (+27%) and office (+double digits), while sales jumped 28%. Japan and India posted 30%+ revenue growth. Project Management rose 19%, aided by government and hyperscaler demand. Executives expect a steady recovery in CRE transactions as interest rates stabilize and cited expanding facility-management pipelines. Management reaffirmed its M&A focus on resilient, high-growth sectors like data centers, life sciences, and healthcare. Shares were up as much as 1.5% on 10/23 in reaction to the triple play…

Continue reading our Conference Call Recap for CBRE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q3 2025 Earnings Conference Call Recaps: Tesla (TSLA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Tesla’s (TSLA) Q3 2025 earnings call.

![]()

Tesla (TSLA) designs and manufactures electric vehicles, battery energy storage systems, and AI technologies that extend beyond the auto industry. The company serves consumers, businesses, and utilities through products like its Model Y, Powerwall, and Megapack, while advancing autonomous driving and humanoid robotics through its AI and hardware. Tesla’s deep vertical integration, custom chip design, and manufacturing scale make it a bellwether for the intersection of mobility, energy, and artificial intelligence. Elon Musk called this quarter a turning point as Tesla accelerates real-world AI deployment. The company confirmed plans to remove safety drivers in parts of Austin by year-end and expand Robotaxi service to 8–10 metro areas. Tesla unveiled its AI5 chip (40× more powerful than AI4), manufactured by both TSMC (in Arizona) and Samsung (in Texas). Energy storage reached record deployments, with strong hyperscaler demand offsetting $400M in tariff impacts. The Optimus humanoid robot remains a central focus, with a production-intent prototype coming in Q1 2026. Musk reaffirmed a path to 3M vehicle capacity within two years, driven by Cybercab and AI integration across products. TSLA missed EPS estimates on stronger revenue as the stock opened 4.4% lower on 10/23, though shares rallied back into positive territory intraday…

Continue reading our Conference Call Recap for TSLA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Revenue Record

Bespoke’s Morning Lineup – 10/23/25 – Stuck in the Middle

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want to increase your success rate, double your failure rate.” – Thomas J. Watson, Sr

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We may be starting to sound like a broken record, but once again this morning, futures are little changed with a downside bias, and the government is still closed. With the Fed in blackout ahead of next week’s rate decision, the only data the market has to focus on domestically is earnings. Overall, the pace of reports continues to come in positively with EPS and sales beat rates in excess of 70%. Also on the subject of broken records, it’s now been eight trading days where the S&P 500 has been stuck within the range it traded in on 10/10.

While the government may be closed, Washington is far from quiet, with the latest news being reports that the Trump Administration is in talks to acquire stakes of up to $10 million in various quantum computing stocks, including IonQ, Rigetti Computing, and D-Wave Quantum. Obviously, these stocks are surging in reaction to the news, and as a result have mostly erased yesterday’s declines. It’s worth pointing out, however, that after the gains these stocks have seen in the last couple of years, their market caps are all at or above $10 billion; a $10 million investment works out to less than 0.1%.

Outside of equities, crude oil is surging 5% and back above $60 per barrel after yesterday’s latest round of sanctions against Russian oil companies. Gold is also trying to regroup after the sell-off from the last couple of days, rallying 1.5% and back above $4,100 per ounce, while silver and platinum are both up at least 2.5%. Even Bitcoin and Ethereum have managed to rally more than 1%.

In international markets, Asian stocks were mixed overnight, with the Nikkei falling 1.4% and the Kospi dropping a percent. Hong Kong (0.7%), China (0.2%), India (0.2%), and Australia (0.1%) all managed to finish higher. The tone in Europe this morning is skewed more positive, with the STOXX 600 rallying 0.3% with little in the way of catalysts besides earnings driving the action.

The 10-year yield remains below 4% this morning after trading yesterday at its lowest level since the tariff-tantrum in April. While it wasn’t enough for a 52-week low on an intraday basis, on a closing basis, it was the lowest level since early October of last year. Since peaking at just under 4.6% in May, the 10-year yield has been stuck in a very consistent downtrend channel, and has been moving towards the lower end of that range all month.

The Closer – Rotation, Earnings, Treasury Allotment – 10/22/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look at the market’s rotation (page 1) followed by a rundown of all the latest earnings including results from Tesla (TSLA), IBM (IBM), and more (pages 2 and 3). We cap off with a look into the latest Treasury auctions (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 10/22/25

Chart of the Day – Decent Breadth, No New Highs

B.I.G. Tips – Speculative Stocks Pop

Q3 2025 Earnings Conference Call Recaps: PulteGroup (PHM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers PulteGroup’s (PHM) Q3 2025 earnings call.

![]()

PulteGroup (PHM) is a leading US homebuilder that operates under well-known brands like Pulte Homes, Centex, and Del Webb, delivering thousands of single-family homes annually across 45+ markets. They serve first-time buyers, move-up buyers, and active-adult (55+) communities, offering insight into how large homebuilders navigate affordability, macroeconomic strain, and regional migration. In Q3, the company closed roughly 7,500 homes with home-sale revenue of about $4.2 billion and delivered a 16.8% home-building margin while managing an ROE of about 21%. They noted that buyer demand remains “good, albeit competitive,” but is challenged by weak consumer confidence and stretched affordability, even as interest rates decline. Their active-adult segment grew about 7% in orders, while first-time buyers fell about 14%. They started roughly 6,557 homes and reduced their build cycle to 106 days to manage inventory; spec homes remain near 50% of production, above their 40-45% target, but they’re comfortable with that in the near term. Regionally, Florida and the Southeast showed relative strength, while Texas and the West lagged. On the policy front, they reiterated the US housing shortage (about 3-4 million homes) and flagged a potential $1,500 build-cost headwind per home from tariffs in 2026. They moderated 2025 land spend ($5 billion) but maintain control of about 240,000 lots and noted that easing horizontal development costs (earth-moving/underground) should benefit future lot inflation. On better-than-expected results, PHM shares opened more than 6% lower on 10/21, but recovered the declines by around mid-day…

Continue reading our Conference Call Recap for PHM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: