Q2 2025 Earnings Conference Call Recaps: Home Depot (HD)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Home Depot’s (HD) Q2 2025 earnings call.

![]()

Home Depot (HD) is the world’s largest home improvement retailer, operating more than 2,300 stores across the US, Canada, and Mexico. It serves both do-it-yourself (DIY) customers and professional contractors (“Pros”) with an assortment of building materials, home improvement products, appliances, and tools. Beyond retail, the company has built a powerful logistics and digital platform, offering same-day and next-day delivery, and is expanding deeper into wholesale distribution with acquisitions like SRS (roofing, landscaping, pool) and pending GMS (drywall, ceilings, steel framing). HD reported Q2 sales of $45.3B, up 4.9% YoY, with US comps +1.4%. Smaller projects and seasonal categories drove momentum, while large renovations remain weak amid high rates and economic uncertainty. Management stressed that consumers remain healthy, with $11T in tappable home equity, but are deferring (not canceling) big projects. Technology and AI-powered delivery improvements produced record speed, boosting digital sales by 12% and lifting spend among repeat users. Pro initiatives are accelerating, with SRS exceeding expectations and GMS adding 400 distribution nodes. Trade credit accounts are already driving double-digit lifts in Pro spend. Merchandising strength was broad-based, with 12 of 16 departments comping positive, a sales record in battery-powered tools, and strong appliance gains. Despite misses on the top and bottom lines, HD shares rose as much as 3.2% on 8/19…

Continue reading our Conference Call Recap for HD by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Daily Sector Snapshot — 8/19/25

Chart of the Day – Earnings Season Send-Off

Q2 2025 Earnings Conference Call Recaps: Viking (VIK)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Viking’s (VIK) Q2 2025 earnings call.

![]()

Viking (VIK) is a leading operator of river, ocean, and expedition cruises, built around culturally immersive, destination-focused travel. Its fleet spans 85 river vessels and 12 ocean ships, all designed with a uniform, understated luxury (no casinos, no children, and no nickel-and-diming) that appeals to affluent, “culturally curious” travelers, particularly older demographics seeking comfort and enrichment. Viking controls or has priority access to over 100 docking sites worldwide, giving it a competitive moat in river cruising. The company provides insight into global travel demand trends, discretionary spending patterns among wealthier consumers, and how tourism is shifting toward experiential, high-end travel. Viking reported an 18.5% revenue increase in Q2 2025, fueled by 8.8% capacity growth and an 8% rise in net yields. Bookings remain robust: 96% of 2025 capacity is already sold, and 2026 is 55% booked at higher rates. Egypt and India itineraries sold out quickly, showing strong demand for new cultural destinations. The company highlighted river versus ocean dynamics, river pricing accelerated while ocean moderated slightly, but both segments maintain high occupancy above 95%. Management stressed that marketing, not discounting, is their lever when demand softens. VIK posted better-than-expected revenue on in-line EPS, though the stock fell 5.5% at the open on 8/19…

Continue reading our Conference Call Recap for VIK by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Palo Alto Networks (PANW)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Palo Alto Networks’ (PANW) Q4 2025 earnings call.

![]()

Palo Alto Networks (PANW) is the world’s largest pure-play cybersecurity firm, serving enterprises, governments, and critical infrastructure across the globe. Best known for pioneering the next-generation firewall, the company now offers an integrated portfolio spanning network security, cloud security, and AI-driven security operations. Its platform-based model helps organizations consolidate fragmented security tools into unified systems, improving both outcomes and cost efficiency. Fiscal Q4 2025 marked a milestone as PANW became the first dedicated cybersecurity company to surpass a $10B revenue run rate. Management leaned heavily into AI security, highlighting Prisma AIRS and AI Access as demand surges (GenAI traffic up 890% YoY). Platformization dominated deal flow, including a $100M+ consulting firm win, driving net retention to 120%. Network Security momentum came from SASE (ARR +35% YoY) and Prisma Access Browser (3M licenses sold in Q4). Cortex/XSIAM continued to scale, cutting response times to under 10 minutes for many clients. The proposed CyberArk acquisition would make identity a new platform pillar. Despite global tariff uncertainty, US-based manufacturing insulated margins. The company’s triple play is its first since 2022, and the stock popped 6.4% at the open on 8/19 as a result…

Continue reading our Conference Call Recap for PANW by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 8/19/25 – Paint Dry Yet?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A lot of people are scared to ask questions because they don’t want people to know how dumb they are. I’ve never had that problem.” – Ken Langone

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Home Depot (HD) kicked off retailer earnings week this morning and reported weaker-than-expected EPS on slightly weaker-than-expected revenues. That’s the bad news. On a positive note, the company reaffirmed its guidance for the full year, and while most companies missing results this earnings season have been pummeled on their earnings reaction days, shares of HD are trading more than 1% higher in the pre-market. HD earnings have had little impact on futures, which are mixed on either side of the flatline. That follows what was a fractionally negative overnight session in Asia, and a fractionally positive session so far in Europe.

Here in the US this morning, besides the HD earnings report, there hasn’t been much in the way of stock-specific news. On the economic calendar, July Building Permits and Housing Starts will hit the tape at 8:30. Heading into those reports, bonds are trading slightly higher, crude oil is down 1%, gold and other precious metals are modestly high, while Bitcoin and Ether continue their recent weakness with declines of roughly 1%.

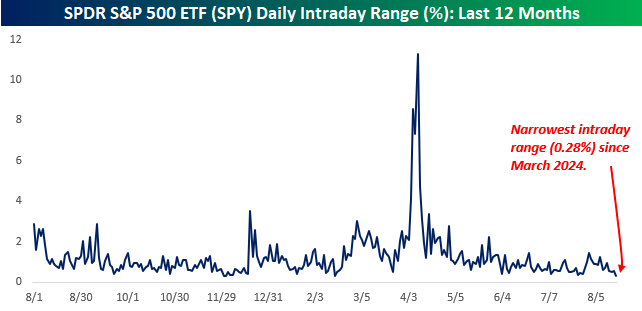

Yesterday was a tough day in the market – to stay awake. From the opening to closing bell, the SPDR S&P 500 ETF (SPY) traded in a range of 0.28% which was the narrowest intraday range since March 2024. To put yesterday’s range in perspective, the intraday range of the market on April 9th at the height of the tariff drama was more than 40 times larger.

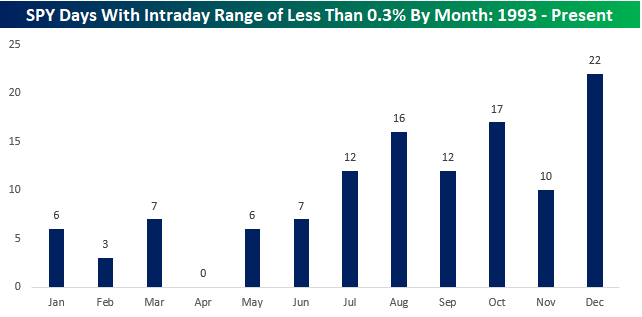

Given that we’re in August, it shouldn’t come as too much of a surprise that the market has been quiet. Since the launch of SPY back in 1993, August has seen the third-highest frequency of days when the ETF’s intraday range was narrower than 0.3%. The only two months with a higher frequency were October (17) and December (22). December makes sense given the holidays, but the fact that October has had the second-highest frequency of days with an intraday range of less than 0.3% was surprising. Digging a little deeper, we found that more than half of them (9) occurred in October 2017. That could have been the most docile month of trading in SPY’s history!

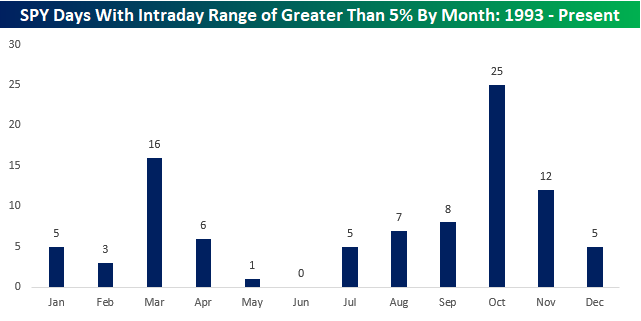

On the flip side, just for fun, we also looked at which months most frequently have seen 5% intraday ranges in SPY. Unsurprisingly, October has been the clear leader with 25, followed by March with 16. Here again, the high frequency of occurrences in March is primarily due to 2020, when there were 12, and the only four other occurrences were in 2009, around the lows of the Financial Crisis.

The Closer – Spreads, Sentiment, Rates Vol – 8/18/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a look into credit spreads (pages 1 and 2) and how rates volatility has shaped up (page 3). We finish with an update on positioning (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 8/18/25

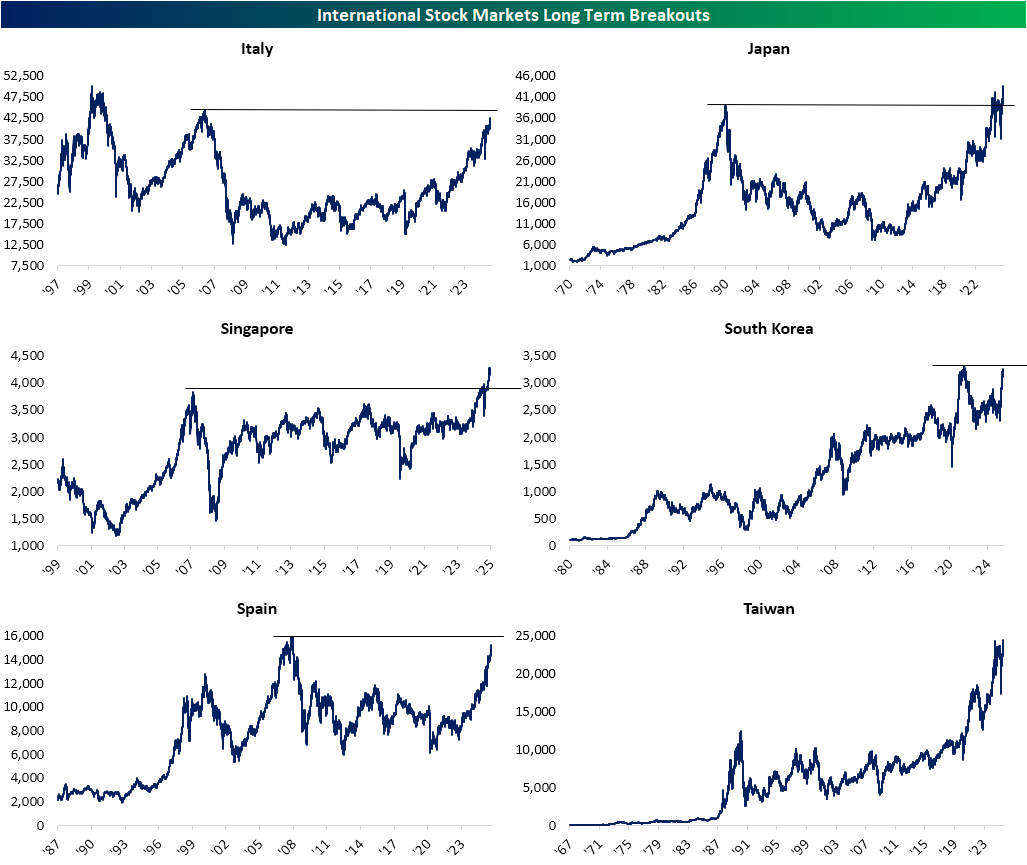

International Breakouts to Watch

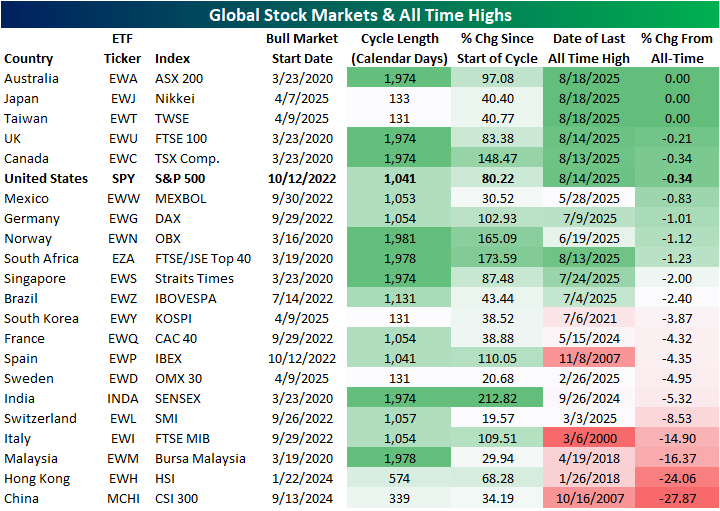

The S&P 500 has seen a slight dip off of record highs in the past few days with many other equity markets around the globe seeing similar price action. As shown below, of 22 major global markets we track, there are currently seven that are within 1% of record highs (priced in local currencies). That includes the S&P 500 which is 0.34% away and three countries trading at record highs as of mid-day Monday: Australia, Japan, and Taiwan. Of those, Japan and Taiwan are actually some of the fresher bull markets (all 22 of these countries are currently in bull markets) whereas Australia is still in the same bull market that has been in place since the COVID Crash lows. The four others within 1% of a high include the UK, Canada, United States, and Mexico. Mexico is the only country within 1% of a fresh high that has yet to have a record close in August. As for the other countries that are further below prior highs, Italy, Malaysia, Hong Kong, and China are the only ones that are still more than 10% away.

As discussed above, Japan is one of three countries trading at fresh all time highs. While notable on its own, Japan’s rally is even more impressive when put in the context of the past several decades. After peaking on December 29, 1989, Japan didn’t move into the black from those levels until February of last year. While the past 18 months since that initial breakout have seen some fluctuations around those prior highs, this latest rally more clearly defines the breakout. Elsewhere in the APAC region, Taiwan is also at a fresh highs after recently breaking out above more short term resistance of its highs from July 2024. Those are not the only two long term breakouts though. In the first week of this year, Singapore finally reclaimed its peak from October 2007. Outside of the spring dip as trade became front and center, Singaporean equities have left those prior highs in the dust.

While those breakouts have been confirmed, a few other areas are setting up to breakout. Italy and Spain have rallied solidly so far into the 2020s, and as a result of those gains are pressing up towards highs not seen since 2007. For Italian equities, a breakout above those levels would still leave resistance at its early 2000 all time high in play whereas a Spanish breakout would result in all time highs. Over in South Korea, a post-pandemic stock surge sent the KOSPI up to records in the first half of 2021. However, it has now been a few years below those highs. That is until this year. The KOSPI has rallied over 30% since this April’s lows and now it is within 4% of that 2021 peak.