The “Kingda Ka” of Stocks

When it comes to whatever area of the technology sector is popular, it’s usually safe to assume that Japanese billionaire Masayoshi Son’s investment holding company SoftBank is active in it. The company always rides the wave when certain tech sectors get hot, but it’s usually along for the ride as the wave crests and starts to roll over. The last several weeks provide an excellent example.

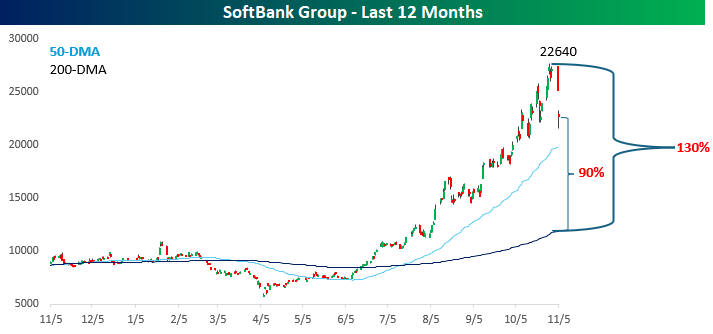

From the April low through its recent intraday high a week ago today, shares of SoftBank rallied more than 380% in the span of just over six months! However, as investors start to question the valuations of AI-related stocks and cryptocurrencies, the stock has quickly corrected. Shares kicked off the week on Tuesday (Monday was a holiday in Japan) by declining 7% and followed that up with an even larger encore overnight, falling more than 10% today. On both a one-day and two-day basis, the declines rank as the steepest since the April lows.

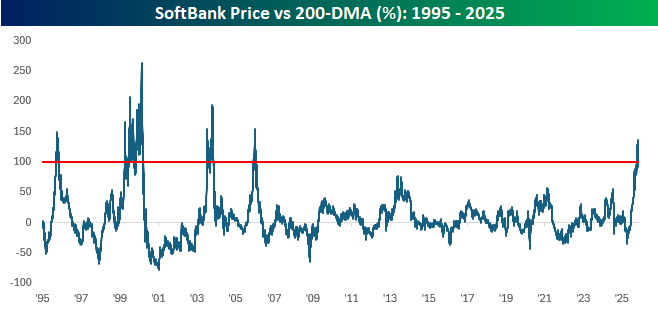

What’s bananas about SoftBank, though, is that even after the declines in the last two days, the stock is still 90% above its 200-day moving average (DMA)! Robinhood (HOOD), the best performing stock in the S&P 500 this year, is ‘only’ 65% above its 200-DMA, so 90%, let alone the 130% that SoftBank was trading above its 200-DMA last week, is incredible.

Relative to its own history, SoftBank’s recent peak of trading 130% above its 200-DMA was the widest spread since December 2005, when its 200-DMA spread reached 154%. Believe it or not, that wasn’t even the stock’s peak. In 2003, the spread reached 190%, and at the height of the dot-com bubble, the spread surged to 262%, or double what the spread just recently peaked at. Double! When it comes to investing, most advisors suggest that slow and steady wins the race, but Masayoshi Son has shown that there are other ways to get from here to there.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

Bespoke’s Morning Lineup – 11/5/25

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When it is darkest there is always light ahead.” – Roald Amundsen

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

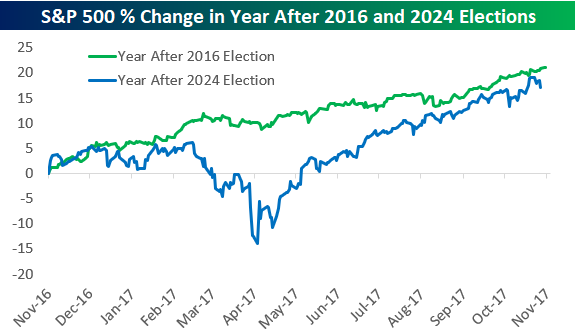

While New York City elected a democratic socialist to be its next mayor last night, today is the first anniversary of the 2024 Presidential Election. Below is a look at the S&P 500’s percentage change over the last year compared to its change in the year after President Trump’s first election victory in 2016. While the two paths diverge in the middle part of the chart because of the “tariff tantrum” seen earlier this year, the full-year performance for the S&P following the 2016 and 2024 Elections is now very similar. We’ll be looking at stock market performance during the Presidential Election Cycle in more detail in today’s Chart of the Day, so keep an eye out for that if you have an interest.

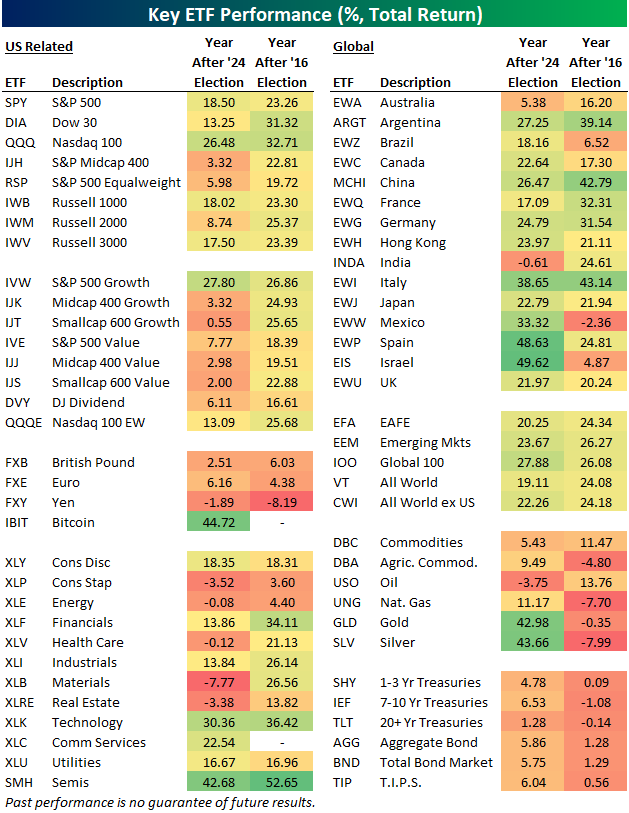

Below is our asset class performance matrix showing total returns across a range of ETFs in the year after the 2024 Election versus the year after the 2016 Election.

While large-cap domestic equity ETFs posted strong gains in the first year after Trump’s 2016 and 2024 wins, there are a lot of areas that have done a lot worse this time around.

The biggest disparities show up in small and mid-cap ETFs. In the year after the 2016 Election, we saw similar 20%+ gains across the market-cap spectrum. This time around, small-caps and mid-caps have been left in the dust, while large-caps have surged.

As an example, the S&P 500 Growth ETF (IVW) is up 27.8% since last year’s Election, while the Smallcap 600 Growth ETF (IJT) is up just 0.55%.

Looking at sector ETFs, Technology (XLK) and Consumer Discretionary (XLY) were up similar amounts, but Health Care (XLV), Materials (XLB), and Real Estate (XLRE) have been much weaker in the last year compared to the year after the 2016 Election.

Outside of the US, we’ve seen most country ETFs post huge gains since the 2024 Election, while their returns were much more muted in the year after the 2016 Election.

Finally, gold (GLD) and silver (SLV) have been two of the best performing ETFs in the entire matrix since Trump’s 2024 victory, but they were down in the year after his first victory.

The Closer – Outside Day, Baskets Check-In, Jobs – 11/4/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with some negative reactions to AI triple plays in addition to the Nasdaq’s downside outside day (page 1). We then review a handful of our various baskets (pages 2 and 3). Next up, we review Indeed job postings both in the US and abroad (pages 4-6) before closing out with a look at the health of supply chain businesses (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 11/4/25

Chart of the Day – S&P 500 (But Not a Lot of Stocks) Up Six Months in a Row

Bespoke’s Morning Lineup – 11/4/25 – It Must Be Tuesday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“America’s health care system is neither healthy, caring, nor a system.” – Walter Cronkite

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strangely subdued reaction to its earnings report after the close yesterday, shares of Palantir (PLTR) are down nearly 8% in the pre-market as investors had some time to sleep on it overnight. An 8% decline is nothing to dismiss, but it’s also important to remember that PLTR is a volatile stock. In its history as a public company, the average one-day reaction to earnings has been a gain or loss of over 15%, and based on where it’s trading now, shares of PLTR are back to where they were just last Tuesday.

The decline in PLTR comes as a cloud of concern envelops the market over how fast stocks have rallied and where valuations have gone. Right on cue, a Bloomberg article says as much with the headline below. While the headline sounds scary enough, the details read a lot less scary. Essentially, it quotes various Wall Street CEOs, among them Morgan Stanley CEO Ted Pick and Goldman Sachs CEO David Solomon, suggesting that the market could see a pullback of 10% to 20% at some point in the next 12 to 24 months. Solomon was quoted as saying, “Of course, it’s likely there will be a 10% to 20% drawdown in equity markets over the next 12 months,” but even he admitted that pullbacks like that can come at any time and from any level.

Concerns are concerns, though, and when investors worry, they sell. With that, futures on the S&P 500 and Nasdaq are both indicated to open down by more than 1%, following a down session in Asia and Europe, where stocks are also broadly lower by around 1% or more.

Even with the sharp decline in equities, bond yields are only modestly lower as the 10-year yield still hangs around 4.1%. Crude oil prices are also down more than 1%, which suggests that investors are also concerned about the health of the economy, given the ongoing shutdown. We’ll be watching the level of airport delays; the more they rise, the more likely it is that policymakers in DC reach an agreement to open the government back up. Thanksgiving is just three weeks away, and no one on either side of the aisle wants to face the wrath of Americans who can’t get home for the holiday.

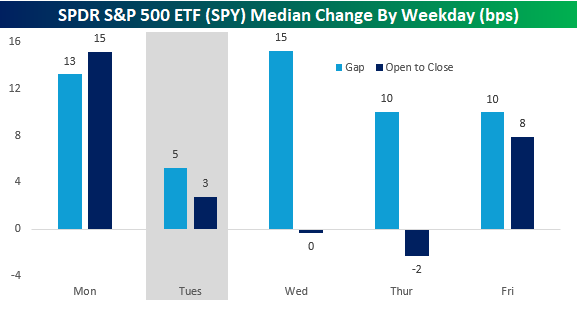

Given the scope of the pre-market declines, it must be Tuesday. As shown in the chart below, the S&P 500’s median opening gap on Tuesdays this year has been just five basis points (bps), which is less than half the next closest weekdays (Thursdays and Fridays), so the day has had a knack for weakness. From the open to close, Tuesday isn’t the weakest day of the week, but it’s still much weaker than the median gains of 15 bps on Monday and 8 bps on Friday.

The Closer – More Breadth Disconnect, Fedspeak, Issuance – 11/3/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a rundown of the latest earnings (page 1) followed by a check up on the disconnects between price and breadth including how mega-caps have impacted the S&P 500 (page 2). Next, we review the latest slug of Fedspeak and give an update on repo markets (page 3). Turning over to macro data, we close out with updates on ISM (page 4), Remittances (page 5), and election day (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Consumer Pulse Report – November 2025

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Daily Sector Snapshot — 11/3/25

Q3 2025 Earnings Conference Call Recaps: Chipotle (CMG)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Chipotle’s (CMG) Q3 2025 earnings call.

![]()

Chipotle (CMG) operates more than 3,500 fast-casual restaurants specializing in customizable burritos, bowls, tacos, and salads. Serving a broad customer base that skews younger and urban, Chipotle offers insight into US consumer behavior and spending trends, especially among millennials and middle-income households. Chipotle’s Q3 call centered on macro pressure from lower- and middle-income consumers, who’ve reduced dining frequency as inflation, unemployment, and student loans weigh on budgets. Management noted that households under $100K account for roughly 40% of sales and are dining out less, but stressed that Chipotle isn’t losing share to competitors, only to food-at-home options. The company plans to limit 2026 price increases and absorb some cost inflation to preserve value, even as tariffs and beef costs rise mid-single digits. Digital engagement and loyalty activations like “Summer of Extras” lifted frequency, while new equipment upgrades improved throughput. Unit expansion and catering pilots remain key growth drivers heading into 2026. CMG missed on the top-line with in-line EPS as shares plummeted 18.3% on 10/30…

Continue reading our Conference Call Recap for CMG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: