My Oh My, What a Month of May

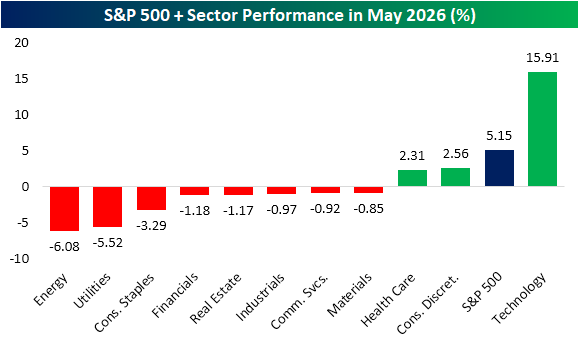

The calendar has turned the page, and May is now in the rearview. Looking back on sector performance during the month, it was certainly one for the history books. In the chart below, we show May performance for the S&P 500 and each of its eleven sectors during the month.

Impressively, the technology sector climbed almost 16% from the end of April to the end of May. Considering it is the most heavily-weighted sector, representing a record 38% of the S&P 500’s market cap, tech’s strength helped to overcome weakness across most other sectors and boost the S&P 500 to a 5.15% gain during the month. Tech was also the only sector to outperform the S&P 500 in May, and just two other sectors were even in the green: Consumer Discretionary and Health Care. Meanwhile, on the other end of the spectrum, Energy and Utilities both fell by over 5%.

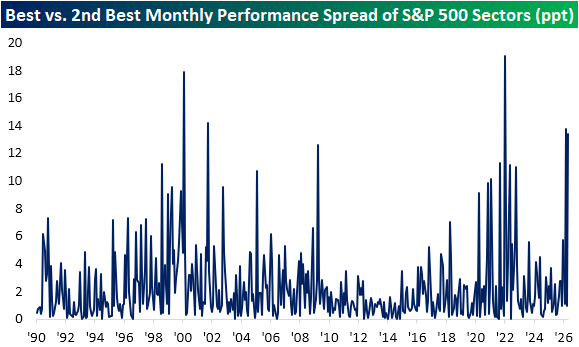

While Consumer Discretionary was higher, it made for a pretty lackluster runner-up. The sector only gained 2.56% in May, which was about half of the S&P 500’s return and a fraction of the huge run in Tech. In fact, it made for one of the largest gaps between the best and second-best performing sectors of any month since at least 1990.

As shown below, only four other months on record saw larger gaps in performance between the best and second-best performing sectors. One was very recently with a 13.73 percentage point spread between Energy (+10.3%) and Utilities (-3.4%) in March, but before that, January 2022 was the most recent with a record-setting 19 percentage point gap between Energy’s 19% gain and Financials’ modest 8 bps decline. Other than that, February 2000 and October 2001 were the only wider divergences.

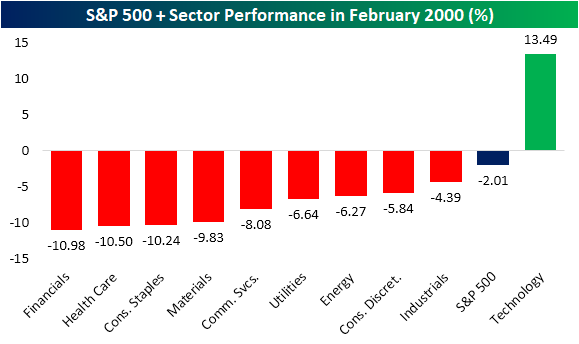

Focusing on the February 2000 instance, we would note that there is one other (maybe concerning) parallel with this past May. February 2000 and this past May are the only months on record in which just a single sector outperformed the S&P 500. In both cases, that outperforming sector – Technology – was the most heavily weighted. Obviously, that 2000 instance was also right before the Dot Com Bubble high the following month.

While that similarity between now and the Dot Com peak may cause concern, we would note that there was also a major difference between February 2000 and last month. In February 2000, as Tech sprinted ahead of the rest of the market, performance from the other sectors was far worse than last month. As shown, multiple sectors fell by over 10% in February 2000 without even one other sector outside of Tech rallying. That compares to last month, when the worst decline was a 6% drop in the recently high-flying Energy sector. Meanwhile, most other sectors were down in the low single digits. In other words, sector bifurcation was far worse 26 years ago.

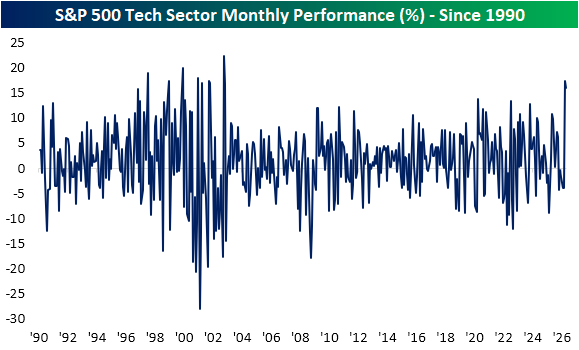

Zooming in on Tech, May was again a historic month. The sector’s nearly 16% gain was actually a bit smaller than the 17.4% jump it experienced in April. As we highlighted in Friday’s Sector Snapshot, since our data begins in 1990, it was the strongest May on record, and for all months of the year, there have only been 10 others with larger gains (again one of those was this April). Combining the April and May rally, the 36.1% run in that span is the sector’s third strongest two-month rally on record behind November 2001 and November 2002.

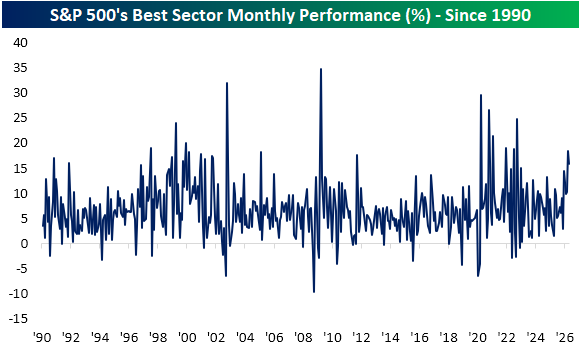

Compared to all sectors across all months, in the chart below, we show the monthly performance of the top-performing sector for all months since 1990. Tech’s rally in May was impressive for another reason as it ranked as the 26th best monthly gain of any sector since 1990. As noted above, Tech also rose 17.4% in April, but that wasn’t the best performer that month. That title belonged to Communication Services, which rallied 18.4% in April. That was the single best monthly performance for any sector since October 2022 when Energy rallied 24.8%. Turning back the calendar just one more month, Energy was this March’s biggest gainer as it rose 10.3% at the onset of the US-Iran war.

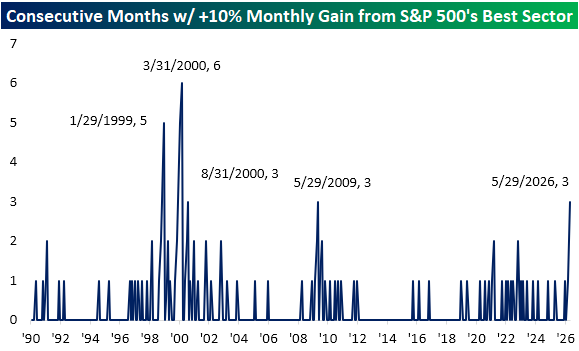

Altogether, that means the S&P 500’s best-performing sector has posted double-digit monthly gains for three months in a row which is the first time that has happened since May 2009. Before that, the only other times this happened were in January 1999 and a couple of times in 2000.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

May 2026 Headlines

Chart of the Day: Back-to-Back 5%+ Monthly Gains

Bespoke’s Morning Lineup – 6/1/26 – The Year of Semis

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“People talk about AI reducing jobs – complete nonsense. It’s causing more software engineers to be hired.” – Jensen Huang

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a new month, but the market rally continues to roll on. S&P 500 futures are priced to open 0.2% higher, while the Nasdaq is fractionally higher. Treasury yields are unchanged right around 4.45% while crude oil trades back above $90, as there don’t seem to be any signs of an imminent peace deal or ceasefire. Gold prices are down 1.4% but still above $4,500 per ounce, while weakness in Bitcoin persists as prices fall to their lowest level since April.

Asian and European markets have been mixed to kick off the month, as manufacturing PMI indices have started to hit the tape. Here in the US, we’ll get the S&P 500 and ISM reads on the manufacturing sector at 9:45 and 10:00 AM, respectively.

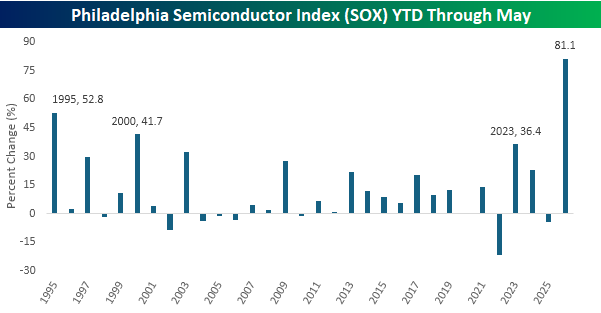

In a speech from Taiwan overnight, Nvidia (NVDA) CEO Jensen Huang called 2026 “the year of agents”. In the evolution of AI, that’s definitely been the case, and the side-effect of that trend in AI is that in the stock market, 2026 has been the year of semiconductors. With a year-to-date gain of 81.1% through the end of May, the Philadelphia Semiconductor Index (SOX) has easily had its best start to a year in its history.

Before 2026, the best start to a year for the SOX was its first full year in 1995, when it rallied 52.8%, or nearly 30 percentage points less than this year’s gain. An 81% gain to start the year is impressive under any circumstances, but when you consider the size of the sector, 81% is almost unbelievable.

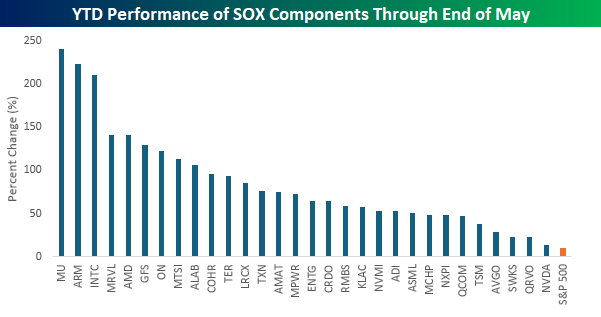

Besides having a monster gain at the index level, the rally in semis has been broad. Of the index’s 30 components, eight have more than doubled, including three that are up over 200%. The average gain of all 30 components has been modestly better than the index itself (+87%), indicating that, unlike the S&P 500, it hasn’t been just the biggest stocks in the index driving the gains. Participation has been so broad, in fact, that every stock in the SOX has outperformed the S&P 500 so far this year.

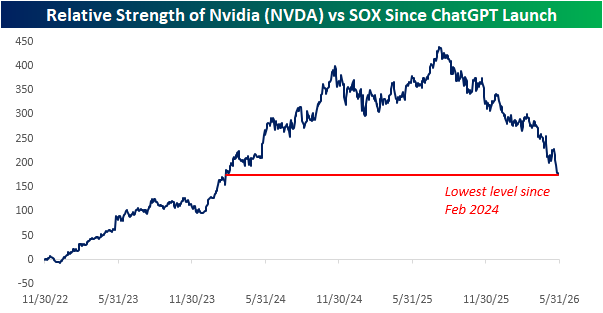

What really stands out about the chart below, though, is NVDA’s performance relative to all the other members of the SOX. With a gain of 13.2% YTD, it’s easily the worst performer in the index and outperforming the S&P 500 by less than three percentage points. So, while all of the major financial outlets are focusing endlessly on last night’s announcements from NVDA out of Taiwan, investors have been looking elsewhere.

Relative to the rest of the semis space, NVDA has been giving up ground for nearly a year now. The chart below shows the stock’s relative strength versus the SOX since the launch of ChatGPT in late 2022. While the stock saw blistering outperformance in the first two years after ChatGPT’s launch, it moved sideways relative to the SOX for nearly a year, and since last August, it has been steadily giving up ground to the index’s other 29 components.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Brunch Reads – 5/31/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Greatness in the Garden:

On May 31st, 1879, the first Madison Square Garden officially opened its doors in New York City, marking the humble beginnings of what would become one of the most famous arenas for sports and entertainment globally. The original arena was built on the site of an old railroad station near Madison Square in Manhattan, which is where the venue got its name. Over time, Madison Square Garden evolved through four different versions, with the current arena opening in 1968 above Pennsylvania Station in Midtown Manhattan.

Throughout its history, Madison Square Garden became known as “The World’s Most Famous Arena,” hosting countless historic moments in sports, music, and politics. Athletes such as Muhammad Ali, Michael Jordan, Wayne Gretzky, and artists like Billy Joel, Elton John, The Grateful Dead, and the Rolling Stones have all been on the biggest stage inside MSG.

MSG is also home to the New York Knicks, who have played there since the latest opening in 1968. For decades, Knicks fans have endured long stretches of disappointment and playoff struggles, despite the iconic arena in which they’ve played every home game. However, the New York Knicks are heading to the NBA finals for the first time since 1999 this year. Led by stars Jalen Brunson and Karl-Anthony Towns, the Knicks have their sights set on bringing a title back to New York, a first since 1973.

More than 140 years after its original opening, Madison Square Garden continues to serve as both a symbol of New York City and a centerpiece of American sports and culture.

Labor

Samsung workers set for $400,000 bonus after deal to share AI profits (Financial Times)

Samsung workers approved a profit-sharing agreement that could pay employees in its memory chip division nearly $400,000 each this year as AI-related chip demand drives record profits. The size of the payouts is already creating tension inside the company, with workers in Samsung’s smartphone and consumer electronics businesses receiving far smaller bonuses despite working for the same employer. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – 5/29/26 – Tech’s Ten Percent Two-Fer

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, choose one of our three member plans today!

This week’s report covers a market that keeps making history, a big earnings week for retailers, and a fascinating look at how private credit is financing the AI buildout. Give it a read!

Daily Sector Snapshot — 5/29/26

Q1 2026 Earnings Conference Call Recaps: Costco (COST)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Costco (COST) Q3 2026 earnings call.

![]()

Costco (COST) is a membership-based warehouse retailer with 928 locations worldwide, selling everything from groceries and electronics to tires and prescription drugs at competitive prices. Rising oil prices due to the conflict in the Middle East sent gas volumes through the roof, with all three fiscal periods setting successive all-time sales records and the final five weeks becoming the five biggest volume weeks in company history. Net sales hit $69.2 billion, up 11.6%, with comps up 9.8%. Excluding gas entirely, comps still grew 6.6%, showing the core business is healthy. Membership fee income rose 10.7% to $1.37 billion, executive memberships grew 9.6%, and more online customers renewed their memberships. On the digital side, AI-driven traffic to Costco’s site tripled in the quarter and posted the highest conversion rate of any traffic source. Kirkland Signature continues to innovate through premium private-label expansion in categories like protein products, apparel, and health supplements, while Costco’s pharmacy business is surging due in part to strong demand for GLP-1 medications such as Wegovy and Ozempic. Inflation is modest but building in nonfoods due to higher resin and memory chip costs. Costco opened down almost 1% after beating revenue expectations but missing on the bottom line…

Continue reading our Conference Call Recap for COST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Encore Performance

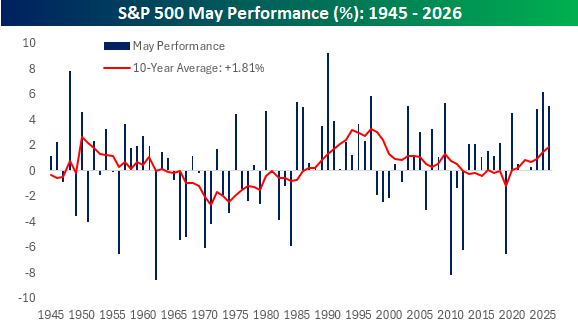

May marks the onset of the “go away” six-month period for US stocks, when they have historically had weaker-than-average returns. In more recent history, though, it has been the encore performance for the October—April period where market returns have historically shined.

With a 5% gain this month, the S&P 500 is on pace for its first-ever “three-peat” of 4%+ gains in May. Not only that, but over the last 14 years, May has only finished in the red once (2019’s -6.58%), driving the 10-year rolling average May return to 1.81%, which is the strongest rolling performance for the month since 1999. Your parents may have once told you that it’s never smart to hang around the bars after last call, but in recent years, staying late has paid off. Now about that hangover the next morning…

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Q1 2026 Earnings Conference Call Recaps: Dell (DELL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dell (DELL) Q1 2027 earnings call.

![]()

Dell (DELL) designs and sells servers, storage, PCs, and networking equipment to businesses of all sizes worldwide. It has become one of the most important picks-and-shovels plays on AI infrastructure, assembling and delivering the physical hardware that hyperscalers, governments, and enterprises need to run the technology. Revenue hit $43.8 billion, up 88%, and EPS grew 214% to $4.86. AI server orders alone were $24.4 billion in a single quarter, and Dell exited with a record $51.3 billion backlog with a pipeline that is multiples larger still. The company raised its full-year revenue guide by $27 billion to a midpoint of $167 billion, with $60 billion expected from AI servers alone. The main constraint is not demand but supply, particularly DRAM, NAND, and CPUs, with lead times stretching to a year on some components. Management also highlighted an emerging trend: new AI systems are increasing demand not only for advanced AI servers but also for traditional CPU-based servers that handle tasks like data processing, storage, and workflow management, creating a market opportunity the company did not expect to see just a few months ago. Storage is recovering strongly with five straight quarters of market outperformance, and the PC business is navigating memory-driven price increases while taking share. Shares of DELL were up over 30% in reaction to its triple play…

Continue reading our Conference Call Recap for DELL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: