The Closer – Energy Rough Run, Beige Book, JOLTS – 9/3/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look over the troubles in the Energy sector (page 1) before switching over to our quantified look at the Beige Book (pages 2 and 3). Next, We close out with a rundown of the latest JOLTS data (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/3/25

Chart of the Day – Antitrust Precedent

Bespoke’s Morning Lineup – 9/3/25 – Good News Google

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Not only strike while the iron is hot, but make it hot by striking.” – Oliver Cromwell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

September may have started on a poor footing. Still, after a bounce yesterday afternoon, the positive tone carried over overnight and into this morning, following positive news for Alphabet (GOOGL) and, by extension, Apple (AAPL). Asian stocks were mostly lower overnight, with the Nikkei falling nearly 1% and China falling more than a percent. In Europe, though, there has been broad-based strength with the STOXX 600 trading up over 0.6%. On the economic calendar today, the only reports on the calendar are JOLTS and Factory Orders.

Yesterday was an unsurprising start to September, and the silver lining was that the ‘buy the dip’ mentality of investors that we discussed in Friday’s Bespoke Report remained intact. The S&P 500 sold off sharply early in the session, tested those lows right around midday, and then rallied throughout the session to finish right at the highs for the day. From a short-term perspective, the S&P 500 has now made two higher highs and two higher lows, reinforcing the overall upward trend.

Both the S&P 500 and Nasdaq are priced to continue yesterday afternoon’s bounce this morning, and the key driver is Alphabet (GOOGL) following last night’s ruling that it would not be required to sell its Chrome browser. In response, the stock is on pace to gap up nearly 6%. If these levels hold through the opening bell, it would be the largest upside non-earnings related gap higher since 2008.

With today’s gain, we also wanted to provide an update on the comparison between GOOGL and Microsoft (MSFT) since the launch of ChatGPT. The overall consensus has been that MSFT’s quick action and investments into OpenAI helped it to win the AI race among the hyperscalers, but the market has a different opinion. While MSFT has nearly doubled since the launch of ChatGPT in November 2022, at the open today, GOOGL will be up over 121%. While MSFT has won in the court of public opinion, GOOGL has won in the wallet.

The Closer – September Starts, Construction, Baskets – 9/2/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the weak start to September in a historical context (page 1). We then dive into the latest construction spending data (page 2) followed by a review of the performance of relevant names in our Picks and Shovels basket (page 3).Next up, we check in on the performance of some other baskets (Page 4) before finishing with a look at today’s PMI readings (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/2/25

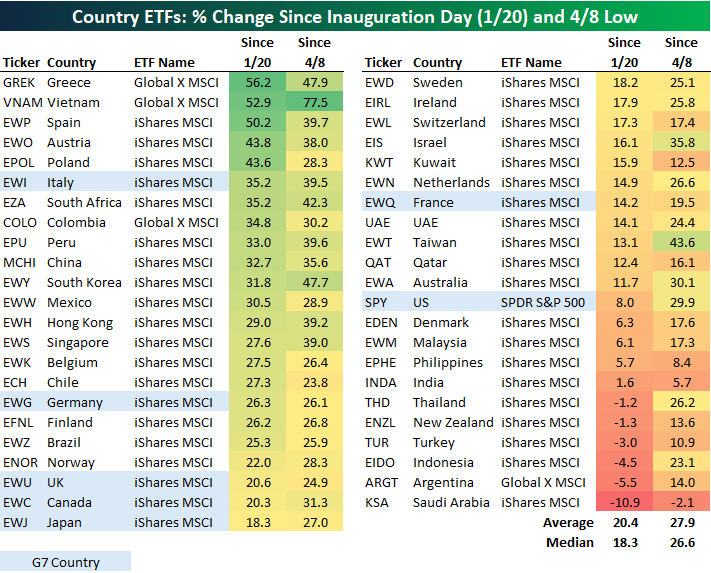

Best and Worst Country ETFs Since Trump 2.0

If you missed Bespoke’s Paul Hickey on CNBC this morning, click here to watch the clip.

It has been 225 days since President Trump’s Inauguration on January 20th, and the S&P 500 (SPY) entered today up 8% since the last close before the Inauguration. That ranks 35th out of 45 country stock market ETFs we track closely. With a gain of 20.4%, the average country ETF shown in the table below is up much more than the US (SPY) since Trump 2.0 began. Greece (GREK), Vietnam (VNAM), and Spain (EWP) are up the most at 50%+, while Italy (EWI) has been the best performing G7 country at +35.2%. Speaking of the G7, the US has been the worst market among these seven developed nations since Inauguration Day in January.

In addition to post-Inauguration Day performance, we also show how each country ETF performed since global equity markets made their post-tariff crash lows on April 8th. The US (SPY) has posted much more respectable returns relative to the rest of the world; up 29.9% versus the average of 27.9%. Of the G7, only Italy (EWI) and Canada (EWC) are up more than the US (SPY) since April 8th, while France (EWQ) has lagged the most of this group with a gain of 19.5%.

Along with being the second-best-performing country ETF since Inauguration Day, Vietnam (VNAM) has easily been the best performer since April 8th with a gain of 77.5%. On the flip side, Saudi Arabia (KSA) is the only country ETF that is down over both periods (-10.9% since 1/20, -2.1% since 4/8). Argentina (ARGT) and Indonesia (EIDO) are two others that are now solidly red since 1/20, while India (INDA) is up just 1.6% since 1/20 and 5.7% since 4/8 (second worst).

Chart of the Day – 100 Days

Bespoke’s Morning Lineup – 9/2/25 – Back to Reality

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I was never part of the crowd.” – Jimmy Connors

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After four summer months when the S&P 500 gained at least 1.9%, September is starting on a characteristically weak note as futures are pointing to a decline of 0.7% to kick off the month. As detailed in this morning’s commentary, there’s nothing in the way of a major catalyst to speak of besides an uptick in treasury yields around the world. Gold and oil prices are also higher. The only economic reports on the calendar are the ISM Manufacturing for August and July Construction Spending. The ISM report is expected to come in below 50 again but show an uptick from last month’s weaker-than-expected reading of 48.0 to 48.9 this month. Construction spending is expected to show a modest uptick of 0.1% after declining 0.4% in June.

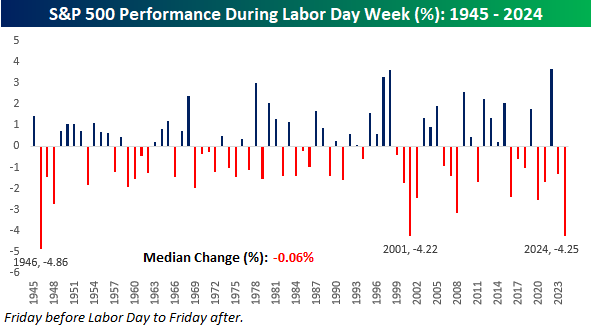

Historically, Labor Day week has been somewhat weak. Since 1945, the S&P 500’s median performance during Labor Day week has been a decline of 0.06% with gains just half of the time. Ironically, last year’s 4.25% decline was the weakest since 1946 and just the third time since 1945 that the index declined 4% or more during the week.

In terms of what that weakness means for the rest of the year, it doesn’t really mean anything. Last year, the S&P 500 rallied 4.13% through year-end after the 4.25% decline. In 2001, it rallied 1.28% for the rest of the year, and in 1946, it fell 8.11%. For all years since 1945, the S&P 500’s median performance from the end of Labor Day week through year-end has been a gain of 3.78% with gains 73% of the time.

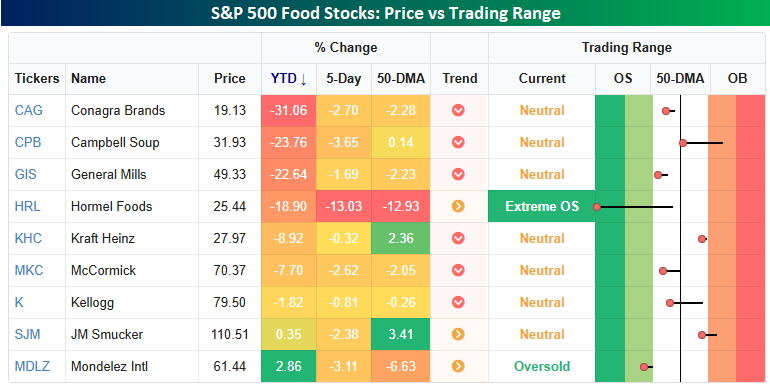

One of the bigger individual stock stories this morning is the announcement that Kraft Heinz (KHC) will split itself into two companies in an effort to boost growth. As the graphic below shows, KHC and its peers could use all the help they can get. The snapshot below from our Trend Analyzer shows where KHC and its peer stocks are trading relative to their trading ranges. On a YTD basis, just two of the nine stocks listed are up on the year, and four of them are down by double-digit percentages. KHC isn’t quite down 10%, but it was before Friday’s news of the breakup originally broke. Last week was particularly poor for the group as well, with all nine trading down anywhere between 13% for Hormel (HRL) to a fractional decline for KHC.

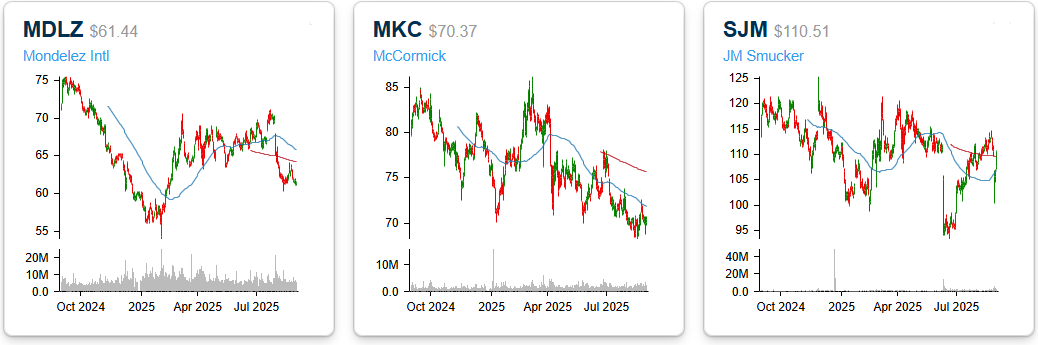

If you have a weak stomach, you may want to skip the section below, which shows one-year price charts of the nine stocks listed above. Practically every single one of them has the same pattern – top left to bottom right. These are the types of charts you would expect to see during a bear market rather than after one of the strongest 100-day market rallies in history!

Brunch Reads – 8/31/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

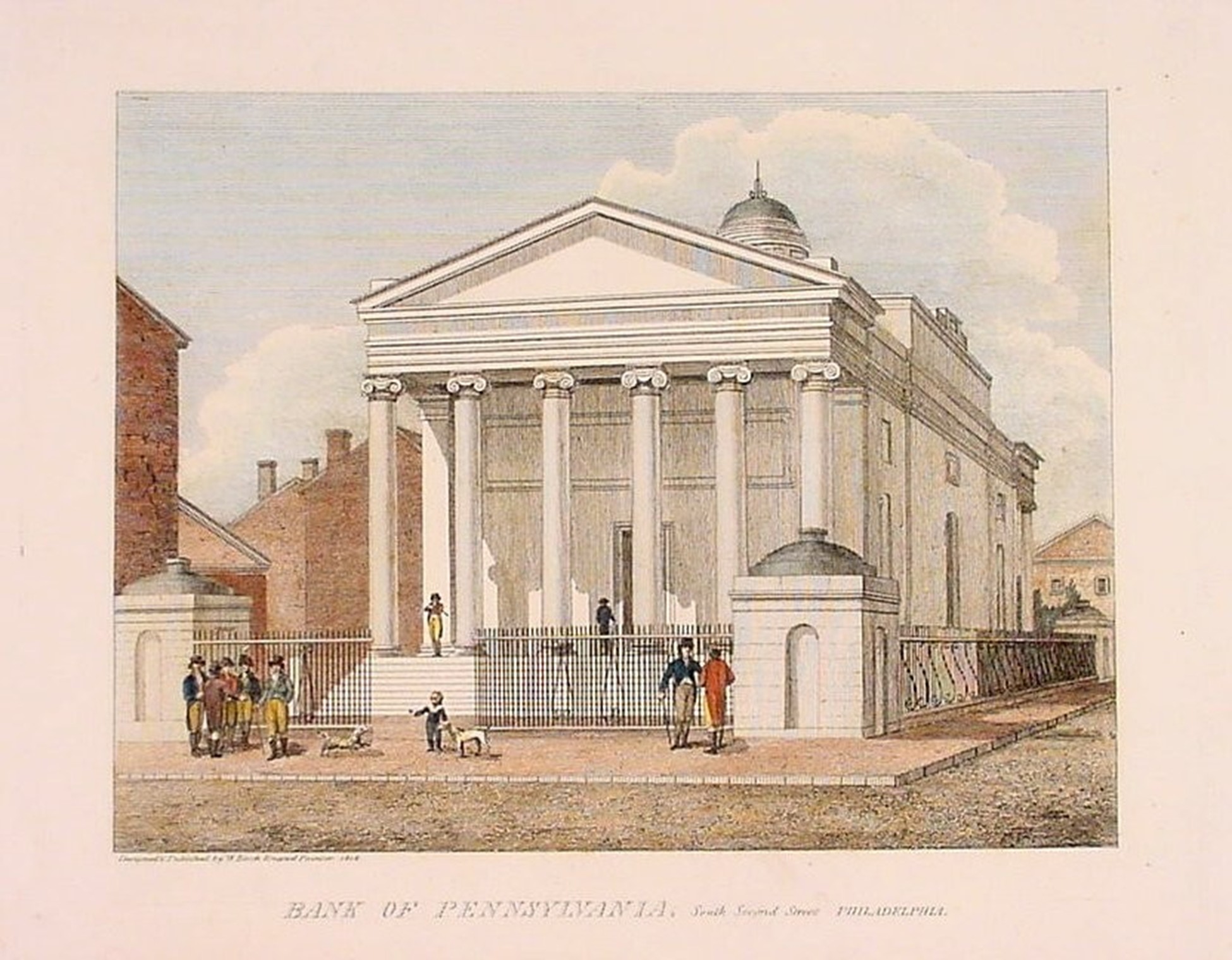

Founding Felons: America’s first bank robbery unfolded in Philadelphia on the night of August 31, 1798, when thieves targeted the Bank of Pennsylvania inside Carpenters’ Hall. By morning, more than $160,000 in cash and notes had vanished, a fortune worth several million dollars today. At first, suspicion fell on the bank’s own directors, since there was no sign of forced entry. The locks themselves had been newly installed, and blame quickly and wrongly landed on the blacksmith who forged them, Patrick Lyon.

Lyon, who had fled the city during a yellow fever outbreak, was arrested upon his return and jailed for months. The truth eventually came out: Isaac Davis, a carpenter who had worked on the building, and Thomas Cunningham, the night watchman, had carried out the crime using stolen keys. Much of the money was later recovered, and Lyon was exonerated, though only after a humiliating ordeal that he later chronicled in a memoir.

Markets & Investing

There Are Now More ETFs in US Than There Are Individual Stocks (Bloomberg)

The number of ETFs in the US has exploded past 4,300, now outnumbering listed stocks for the first time and leaving investors overwhelmed by choice. Issuers are churning out new products at a record clip, often niche or risky strategies like single-stock and leveraged funds, while many near-duplicate strategies fizzle out. The glut has made it harder for individuals to navigate the market on their own, pushing more investors toward professional advice as they struggle to sort the few lasting funds from the many fleeting ones. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.