Q2 2025 Earnings Conference Call Recaps: AeroVironment (AVAV)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers AeroVironment’s (AVAV) Q1 2026 earnings call.

AeroVironment (AVAV) is a defense technology company that develops unmanned systems and advanced defense solutions across air, land, sea, space, and cyber domains. Its portfolio includes tactical drones like the Raven (hand-launched small UAS for reconnaissance and surveillance), Puma (small, portable UAS for long-endurance tactical missions), Switchblade (loitering munition drones designed for precision strike), and the P550 (Group 2 drone for long-range reconnaissance and intelligence gathering). Through its recent acquisition of BlueHalo, the company has expanded into space-based communications (e.g., laser terminals), directed-energy weapons (LOCUST laser system for counter-drone and missile defense), and RF/electronic warfare solutions (Titan jamming systems, BADGER phased-array satellite ground stations). AeroVironment posted record Q1 revenue of $454.7M, up 140% YoY, with bookings near $400M and a $1.1B funded backlog plus $3.1B unfunded. Growth was driven by a $240M Space Force laser communications contract, a $95M Army award for the FE-1 long-range interceptor, and surging sales of Switchblade 600 (+200%), JUMP 20 (6x), and LOCUST laser defense (5x). Management highlighted that conflicts such as Ukraine show vulnerabilities in traditional RF systems, boosting demand for laser and RF solutions like Titan, while NATO allies are showing increased interest in UAS and missile defense. AVAV missed EPS estimates on stronger revenue. The stock was up roughly 3% on 9/10…

Continue reading our Conference Call Recap for AVAV by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q3 2025 Earnings Conference Call Recaps: Oracle (ORCL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Oracle’s (ORCL) Q1 2026 earnings call.

![]()

Oracle (ORCL) is a global leader in enterprise software, cloud infrastructure, and database technology. Best known for its flagship Oracle Database, the company also provides cloud services, enterprise applications, and advanced infrastructure such as the Oracle Cloud Infrastructure (OCI). Oracle’s offerings support a broad range of customers, including large enterprises, governments, healthcare providers, and emerging AI companies. The firm plays a pivotal role in enabling digital transformation, data management, and artificial intelligence adoption across industries, making it a bellwether for both enterprise IT spending and cloud infrastructure demand. Oracle reported 7% revenue growth YoY, with cloud revenue up 14% to $6.2B and OCI revenue jumping 51%. Management emphasized that growth is constrained not by demand but by supply. Limited availability of NVIDIA GPUs and data center capacity reduced revenue by roughly $235M in Q1. To meet soaring AI demand, Oracle is building over 100 new data centers globally, including six exascale-scale regions and sovereign regions in Europe, Japan, and the Middle East. Larry Ellison highlighted the “Butterfly” system, a compact $6M three-rack OCI region, designed to let enterprises run large AI models securely on their own data. Oracle sees AI-driven cloud workloads, especially in healthcare, government, and ERP, as the biggest growth engine of this technology cycle. The stock rose as much as 42% on 9/10 despite EPS and revenue misses, making Larry Ellison the richest person in the world (for now), surpassing Elon Musk…

Continue reading our Conference Call Recap for Oracle by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Historic Earnings Surges

Oracle (ORCL) and the Best and Worst Performers Since April 8th

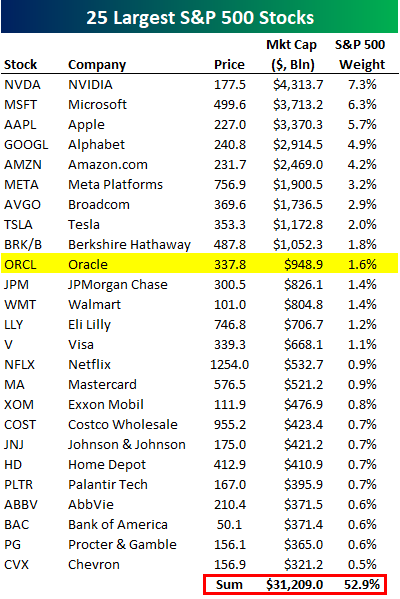

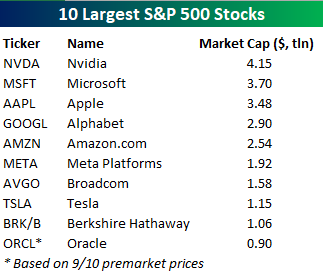

As of mid-day, Oracle (ORCL) is trading up 38% in reaction to its quarterly earnings release after the close yesterday. Since the start of 2020, there have been more than 47,000 individual earnings reports across US stocks, and only 126 of those reports resulted in a one-day share price jump of 38% or more. Oracle is set to make it 127 today. While most stocks that jump 38% in a day have smaller market caps, Oracle is doing it with a market cap that’s now nearing $1 trillion.

As shown below, Oracle’s gain today has propelled it up to the 10th largest stock in the S&P 500 with a market cap of $949 billion. It needs to gain another 5% or so to reach the $1+ trillion market cap club.

The 25 largest stocks in the S&P now comprise roughly 53% of the S&P 500 with a combined market cap of just over $31 trillion.

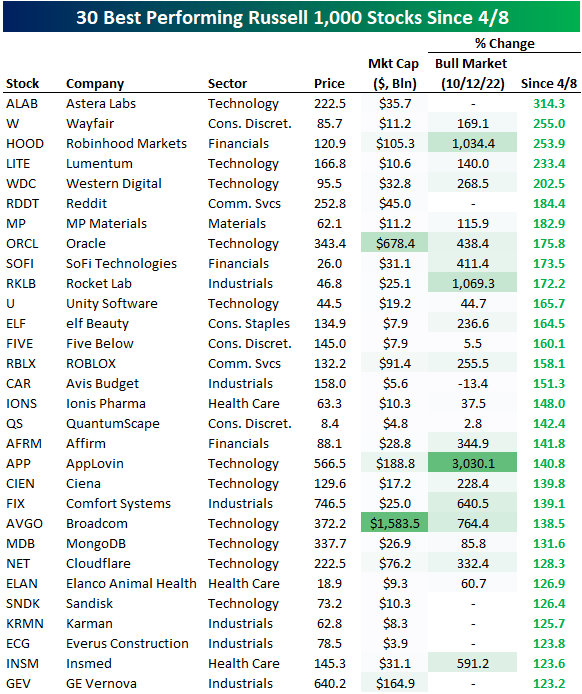

The average Russell 1,000 stock is now up 29% since the index’s low on April 8th following the Tariff-Crash of early April. There are 47 stocks in the index that have more than doubled since then, and below are the 30 that are up the most. Five stocks are up more than 200%: Astera Labs (ALAB), Wayfair (W), Robinhood (HOOD), Lumentum (LITE), and Western Digital (WDC). As shown below, Oracle (ORCL) is up the 8th most of any stock in the Russell 1,000 since 4/8 with a gain of 175.8%.

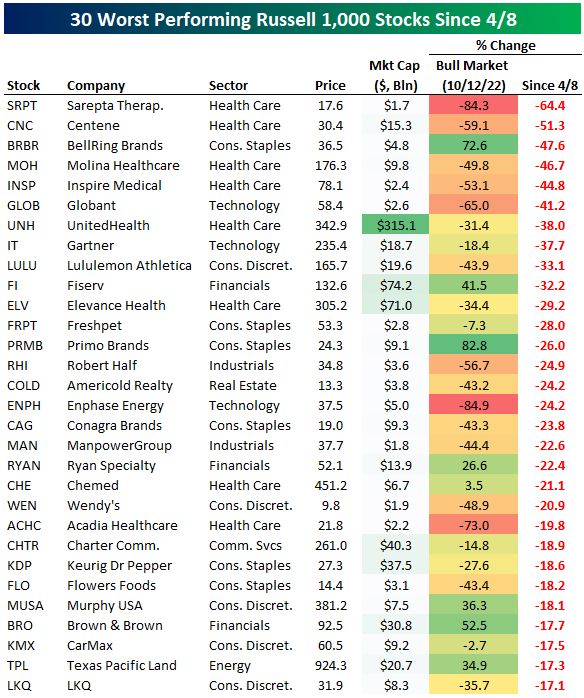

There are 155 stocks in the Russell 1,000 that are down since 4/8 (roughly 15% of the index). Below are the 30 worst performers over this time frame. The three worst performers have been Sarepta Therapeutics (SRPT), Centene (CNC), and BellRing Brands (BRBR).

B.I.G. Tips – Earnings Triple Plays Recap: Q2 2025

During the just-completed Q2 2025 earnings reporting period, there were a total of 202 earnings triple plays out of just under 2,000 individual quarterly earnings reports from US-listed stocks. That’s 124 more than the 78 triple plays we saw during the prior earnings reporting period.

What is a triple play? When a stock reports quarterly earnings, it registers a “triple play” when it beats analyst EPS estimates, beats analyst revenue estimates, and raises forward guidance. We coined the term back in the mid-2000s, and you can read more about it at Investopedia.com. We consider triple plays to be the cream of the crop of earnings season, and we’re constantly finding new long-term opportunities from this basket of names each quarter. You can track the newest earnings triple plays on a daily basis at our Triple Plays page if you’re a Bespoke Premium or Bespoke Institutional member. To read our newest report and see some of the triple plays with intriguing charts at the moment, start a two-week trial to Bespoke Premium!

Bespoke’s Morning Lineup – 9/10/25 – A New Entrant On the Top 10 List

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I believe people have to follow their dreams – I did.” – Larry Ellison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Between Oracle’s (ORCL) 30%+ surge this morning and a weaker-than-expected PPI report, you would expect futures to be higher, but maybe the biggest surprise is that they aren’t up more. Both the S&P 500 and Nasdaq are indicated to open up 0.5%, and given it’s still September, bulls will take all they can get. Treasury yields are little changed, commodities are fractionally higher, and crypto is seeing the largest gains as Bitcoin and Ethereum are both up over 1.5%.

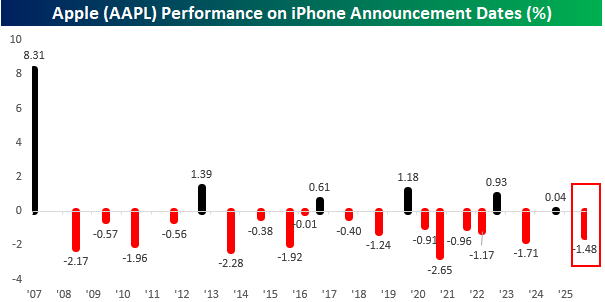

The market’s focus has now shifted to the upcoming inflation data, but yesterday, Apple (AAPL) was a focus with the launch of the latest iPhone models. As noted in our Chart of the Day from Monday, AAPL’s performance on the day of iPhone announcements has been weak, and yesterday was no exception as the stock fell 1.48%. As shown in the chart, for all the gains AAPL has had in the iPhone era, one of the worst days to own the stock has been on these announcement days.

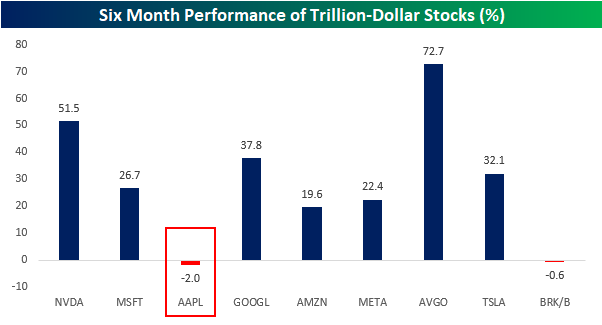

Normally, AAPL’s stock performs well in the lead-up to iPhone announcements, but that hasn’t been the case this year. Over the last six months, the stock has declined 2%, which is weaker than any of the other nine trillion-dollar S&P 500 stocks. The only other one that is down during this stretch is Berkshire Hathaway (BRK/b), which also happens to be one of the company’s largest shareholders.

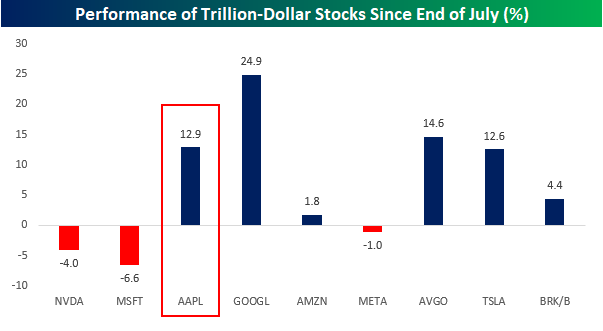

More recently, though, AAPL has started to turn the corner. Since the start of August, the stock has rallied 12.9% which ranks as the fourth-best among the trillion-dollar stocks, trailing Alphabet (GOOGL), Broadcom (AVGO), and Tesla (TSLA).

Speaking of the largest stocks, the trillion-dollar club may be on the verge of getting a new member. As of yesterday’s close, shares of Oracle (ORCL) had a market cap of $680 billion. After reporting a blowout earnings report, though, the stock is trading nearly 32% higher in the pre-market, which would take its market cap up just shy of $900 billion, catapulting it from the 13th largest stock in the S&P 500 and into the top ten list. It’s hard to comprehend just how large a move ORCL is having in reaction to its earnings. Only 42 companies in the S&P 500 have a larger market cap than ORCL’s market cap increase since the close yesterday, and it’s also larger than the entire market cap of Disney (DIS). Less than 0.35% of all earnings reports since 2001 have seen a stock rally more than 31% in reaction to earnings, and in those rare instances, the gains have been typically in small and micro-cap stocks.

The Closer – Risk Appetite, Revisions, Housing – 9/9/25

Log-in here if you’re a member with access to the Closer.

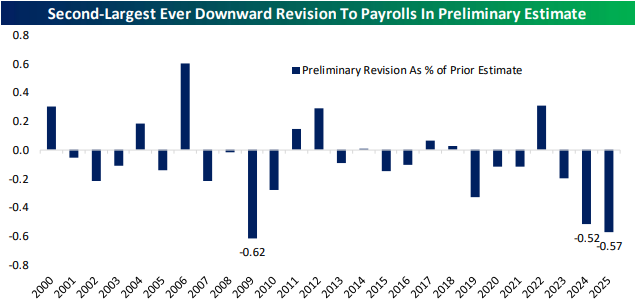

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look into IPO performance and the outstanding guidance from Oracle (ORCL) (page 1). Next, we review today’s revisions to payrolls (page 2) followed by a dive into the latest housing data that includes ICE’s Mortgage Monitor Report (page 3) and inventories data from Realtor.com (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/9/25

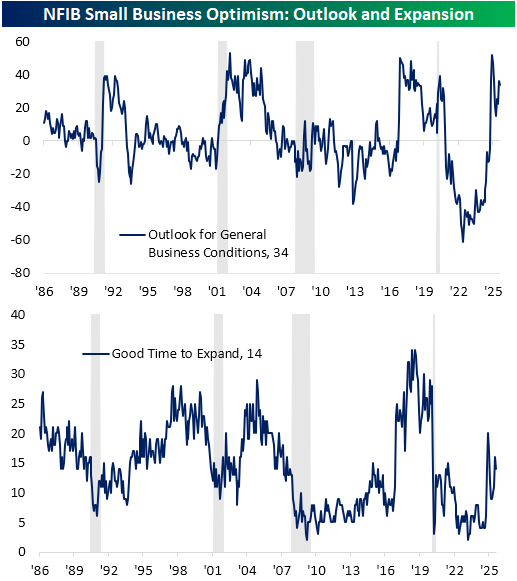

Small Businesses Shy From Expansion

This morning’s release of the NFIB’s gauge on small business optimism saw the headline index climb to 100.8, the strongest level since January. While there was an increase in the Optimism Index, under the hood, breadth was more mixed. For example, the outlook for the economy and the share of respondents viewing now as a good time to expand were both lower month over month. With regards to the former, the two-point decline still leaves the index in the 88th percentile of readings historically, whereas the latter is now below the historical median.

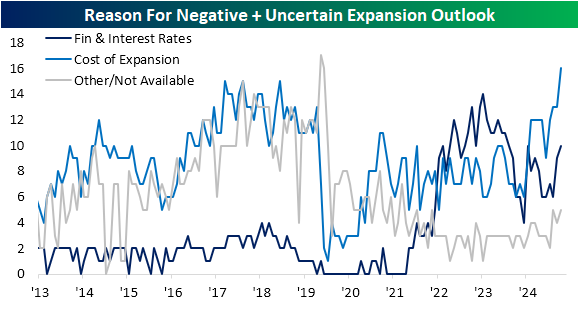

In addition to the index on expansion outlook, the report also details the reasons respondents give for various outlooks. Of those who view now as a good time to expand, only 1% pointed to sales prospects as the reason, while another 5% pointed to the political climate, and another 6% credited economic conditions. As for negative or uncertain responses, the bulk of responses (21% and 13% respectively) blamed economic conditions. While that reason accounted for the bulk of responses, costs are also appearing to be prohibitive. As shown below, for negative and uncertain expansion outlooks combined, 16% of responses blamed the cost of expansion, which is a record high for the series going back to at least 2013. While not at a new high, financials and interest rates have also risen recently, albeit with rate cuts on the horizon, so that reading could pivot lower in the near future. While any further details on what exactly the reasons may be are unfortunately unavailable, we would also note that “other” responses have likewise risen and came in at the high end of the past few years’ range.

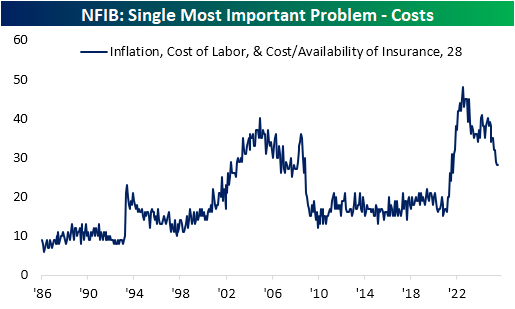

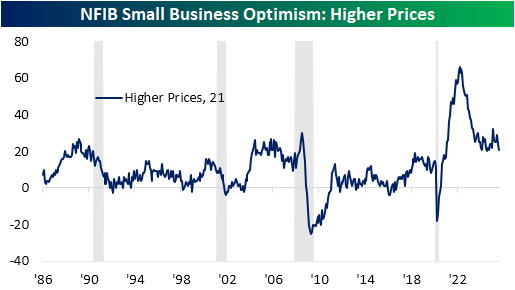

While high costs may appear to be the reason firms are not viewing now as a good time to expand, other data in the report counters this argument. For example, the combined share of respondents who view their most important problems as either inflation, cost of labor, or cost/availability of insurance has continued to fall. Likewise, the share of respondents reporting higher prices is also at the low end of the post-pandemic range.

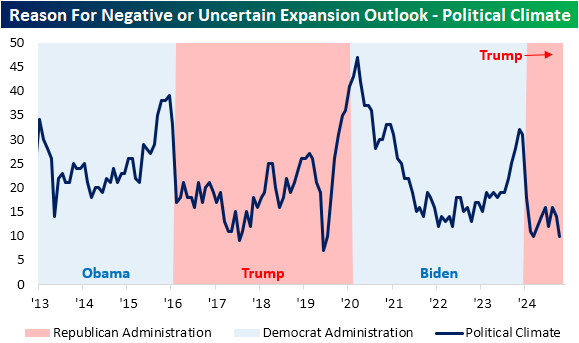

As noted previously, the NFIB survey tends to show political bias with favoritism toward Republican administrations. In other words, small business sentiment has historically tended to be better when a Republican is in office. For example, during Democratic administrations, an average of 13.9% of responses from respondents with a negative expansion outlook have blamed politics, but during Republican administrations, the average declines to 6.4%. Below we show the combined responses for negative and uncertain outlooks that have blamed politics. While Trump’s election resulted in a sharp decline earlier this year, there had been a rebound as policies like tariffs began to roll out. In the past few months, though, those politics-based negative outlooks have once again reverted lower and are nearing record lows. This dynamic of possibly temporary policy shocks to sentiment is something that we discussed related to the report’s labor data in today’s Morning Lineup.

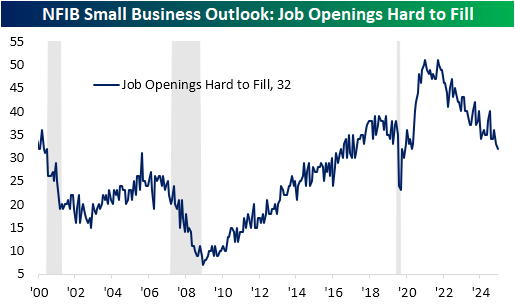

Finally, we would note that while overall labor market indicators have shown modest improvement, or at the very least stability, one exception is the share of respondents reporting that job openings are hard to fill. As shown below, that category is now showing its weakest levels since December 2020.