August 2025 Headlines

Chart of the Day: Internals + After Hours vs. Intraday

7,8,9…

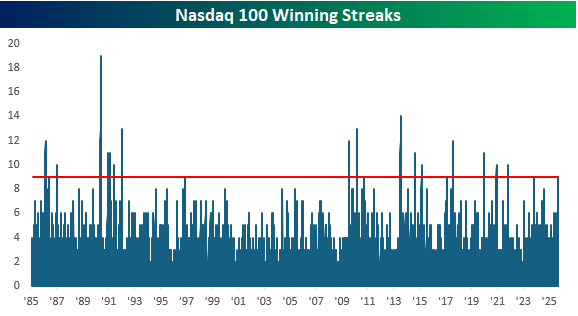

There are still a couple of hours left in the trading day, but with the Nasdaq 100 rallying more than 0.5%, it is on pace for its ninth straight day of gains. After gapping lower to start the month, it looked, on 9/2, like this September would show the weakness that typically accompanies the last month of the third quarter. After successfully testing the 50-day moving average (DMA) that day, though, the Nasdaq 100 has done nothing but trade higher, hitting new highs in the process.

If the Nasdaq 100 does finish the session higher today, it will be its longest winning streak in nearly two years (November 2023) and tied for the longest since November 2021, or nearly four years! The longest daily winning streak in the index’s history was 19 back in May 1990, just two months before a July peak that led to a 33% decline in the subsequent weeks. We also found it notable that while extended winning streaks were relatively uncommon before 2009, they have become far more frequent in the last 15 years. For example, in the 23+ years from 1985 through 2008, there were just nine winning streaks of nine or more days, but in the last 16 years, there have been 13.

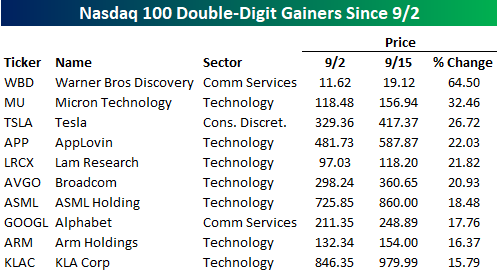

Over the course of the Nasdaq 100’s winning streak, the index’s 4.4% gain has been weaker than its average gain of 7.2% in the first nine trading days of prior streaks lasting nine or more days. As a result, there haven’t been a lot of big winners, and nearly half of the index’s components are lower since the streak began. Of the index’s 100 components, just ten are up 10% or more during the streak, with Warner Bros. Discovery (WBD) leading the way as merger speculation has pushed that stock up 64.5% since the close on 9/2. Besides WBD, seven of the ten stocks listed are from the Technology sector, and while not many stocks are up by double-digit percentages, an unlikely trio of mega-caps made the list with Tesla (TSLA), Broadcom (AVGO), and Alphabet (GOOGL) rallying 26.7%, 20.9%, and 17.8%, respectively.

Bespoke’s Consumer Pulse Report – September 2025

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Morning Lineup – 9/15/25 – Halfway Through September

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best way to make your dreams come true is to wake up.” – Muhammad Ali

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong week, markets are getting off to a positive start this week ahead of this week’s Fed meeting. The S&P 500 is indicated to open with a gain of 0.25%. Overnight, Asia was mixed, but Europe has been higher across the board. The economic calendar is light to kick off the week, as the Empire Manufacturing report came in weaker than expected. Later on this week, things will pick up with Retail Sales highlighting Tuesday’s schedule and Housing Starts and Building Permits coming on Wednesday, along with the Fed.

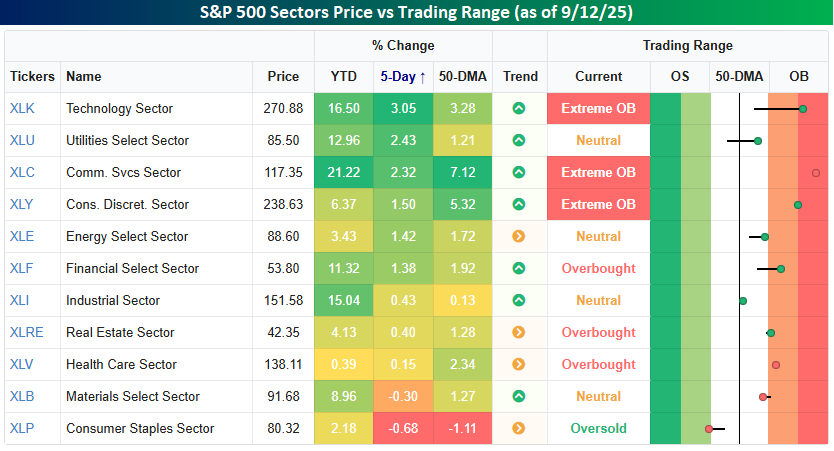

Markets are always forward-looking, and last week they looked forward to this week’s FOMC meeting, where Powell & Co will announce a cut of at least 25 basis points (bps) on Wednesday. Last week, six sectors rallied by at least 1%, including Technology, Utilities, and Communication Services, which rallied more than 2% each. We’ve grown accustomed to seeing Tech and Communication Services rally in unison. However, it’s still hard to get used to seeing the traditionally defensive-oriented Utilities sector rallying alongside those two sectors, but markets are always evolving. On the downside, the only sectors to finish lower last week were Consumer Staples and Materials. They’re also the only two sectors to finish last week below their 50-day moving averages. Consumer Staples is even oversold as well!

Six sectors finished last week at short-term overbought levels heading into this week’s Fed meeting, including three at ‘extreme’ overbought levels. While there is nothing prohibiting overbought sectors from becoming more overbought in the short term, it also sets up the possibility of a sell-the-news reaction to this week’s rate cuts. Just something to be on the lookout for.

Brunch Reads – 9/14/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Pop-Tarts Pop Off: On September 14, 1964, Kellogg’s officially launched Pop-Tarts, forever changing the American breakfast. The idea came after Post had announced a similar product called “Country Squares,” but Kellogg’s rushed its own version to market first and captured the spotlight. The initial release featured just four flavors (strawberry, blueberry, brown sugar cinnamon, and apple currant), each sealed in foil so they could be stored without refrigeration, which was groundbreaking for the time.

When they hit shelves, demand was so overwhelming that stores couldn’t keep them in stock. Parents loved the convenience, kids loved the sweetness, and the “toaster pastry” became a cultural phenomenon almost overnight. Kellogg’s marketing leaned heavily into modern convenience, pitching Pop-Tarts as a quick, tidy breakfast for busy mornings. From frosted toppings introduced in the late 1960s to wild flavors and viral pop culture tie-ins today, the debut of Pop-Tarts was more than just a new product launch; it was a snapshot of 1960s America, where speed, convenience, and a sweet tooth collided.

Crime

How Bitcoin ATMs Are Helping Scammers Steal Millions (Inc)

Gas station clerks in Idaho have become unlikely front-line defenders against a wave of Bitcoin ATM scams that target seniors with fake government bills and doctored arrest warrants. Machines from companies like Bitcoin Depot and CoinFlip convert cash into untraceable crypto, and police say scammers have stolen at least $65 million through them in the first half of 2024 alone. With state rules patchy and federal action limited, regulators are suing operators while store employees are left unplugging ATMs to keep victims from handing over tens of thousands in cash to overseas fraud rings. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

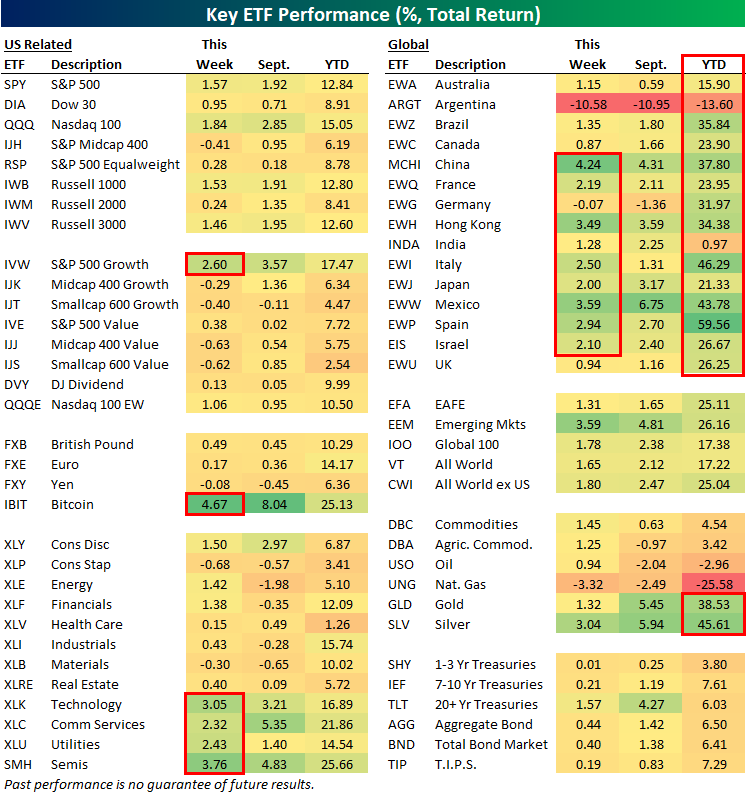

Another Strong Week for Stocks

With the week now complete, below is a helpful look at the recent performance of various asset classes using key ETFs traded in the US.

Large-cap growth (IVW) was up 2.6% on the week, while mid-caps and small-caps actually fell. Technology (XLK) was the best performing sector due to Oracle’s (ORCL) massive gain, while Consumer Staples (XLP) and Materials (XLB) were the worst.

Outside of the US, there are a dozen country ETFs now up 20%+ on the year, which easily beats out SPY’s year-to-date gain of 12.8%. Spain (EWP) is up the most in 2025 with a huge gain of 59.6%.

Argentina (ARGT) and natural gas (UNG) were the two worst performing ETFs in our matrix this week.

Sticking with commodities, agriculture (DBA), gold (GLD), and silver (SLV) all rallied more than 1%, with GLD and SLV extending huge year-to-date gains.

Finally, Treasury ETFs were also up across the board this week as rates fell, especially at the long-end.

If you like this snapshot, we update it daily for Bespoke subscribers. Sign up now with our September Special to gain access.

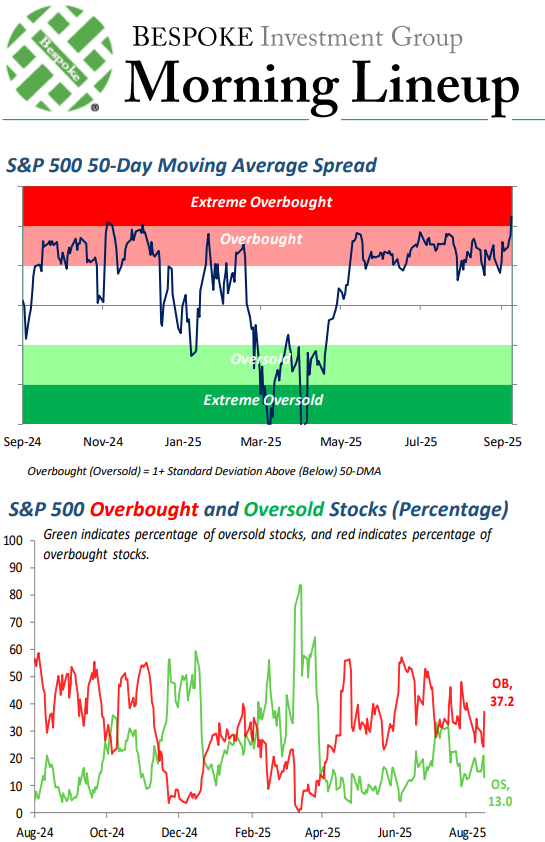

Extreme Overbought

The S&P 500 has had a great run over the last few weeks, but just yesterday it closed in “extreme overbought” territory for the first time since December. You can see the “extreme overbought” reading in our 50-DMA spread chart below (which gets published in our Morning Lineup each day).

Overbought levels are indicative of a market that’s extended. Price can’t stay overbought forever, and eventually mean reversion takes place.

But it’s worth knowing how the market has historically performed when it has gotten to “extreme overbought” levels for the first time in a long time. While there may be some weakness in the near-term, what about the next 3, 6, or 12 months?

If you’re interested in finding out, we’ve got the stats in this week’s Bespoke Report newsletter, which just got posted for subscribers.

The entire report is worth the read, so start a Bespoke Premium trial today! With a new membership, you’ll gain access to a lot more than just our weekly Bespoke Report.

The Bespoke Report – 9/12/25 – Objects In Motion

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week, we review the ongoing enthusiasm across asset markets including a bullish signal delivered by the equity market this week, tight spreads, falling long-term rates, and strong price action in a range of global equity markets. We also got a lot of interesting data this week with implications for labor markets, inflation, and the overall health of the economy. From AI to option-adjusted spreads, this week’s Bespoke Report will get you caught up on markets and economic data for the week. Give it a read!

Bespoke’s Morning Lineup – 9/12/25 – Highs Keep Adding Up

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A cynic is a man who, when he smells flowers, looks around for a coffin.” – H.L. Mencken

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Well, the market can’t go up every day. Equity futures are on pace to close out the week on a modestly weaker note as the Dow and S&P 500 are indicated to open the session modestly lower. For its part, the Nasdaq is looking at modest gains following strong earnings from Adobe (ADBE), which has that stock trading up 3%. The 10-year yield is two bps higher, but at less than 4.04%, it’s been a good week for longer-term treasuries. Crude oil is up fractionally, along with most precious metals, but silver is up closer to 2%. In crypto, Bitcoin is looking at modest gain as it flirts with $115K, but Ethereum is back above $4,500 with a gain of over 2%, while Solana, the newest flavor of the month in the space, has surged over 5% to $239 and its highest levels since January.

The uneventful tone in the US follows what was mostly a positive session in Asia as Japan and South Korea rallied to new all-time highs. Outside of Australia, all the major averages in the region finished the week with gains of at least 1%, and in most cases more.

In Europe, the tone has been more subdued as the STOXX is trading slightly lower along with most major country benchmarks. For the week, though, returns have also been positive with gains of roughly 1%. One negative item has been growth in the UK, where GDP was unchanged in July, versus forecasts for an increase of 0.4%. Meanwhile, Industrial Production, which was forecast to be unchanged versus June, dropped by 0.9%.

Yesterday’s weaker-than-expected jobless claims report and mostly in-line CPI solidified the case for multiple FOMC rate cuts in the months ahead. The market responded with a very broad-based rally as over 85% of S&P 500 stocks traded higher on the session, and small caps outperformed large caps. The S&P 500’s 0.85% rally took it to another record closing high as the index now pushes up against a trendline that has been in place for the last year. As shown in the chart below, while stocks sold off sharply after the index bumped up against this rising ceiling early in the year, most times it has encountered this trendline, the pullbacks were modest.

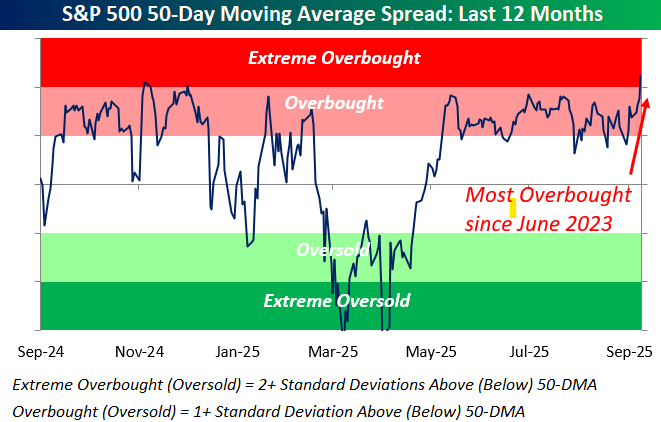

Following yesterday’s rally, the S&P 500 has now moved into ‘extreme’ overbought territory on a short-term basis, which we define as more than two standard deviations above its 50-day moving average (DMA). The last time it traded at more overbought levels was back in June 2023. We’ll have more on these ‘extreme’ overbought readings in tonight’s Bespoke Report.

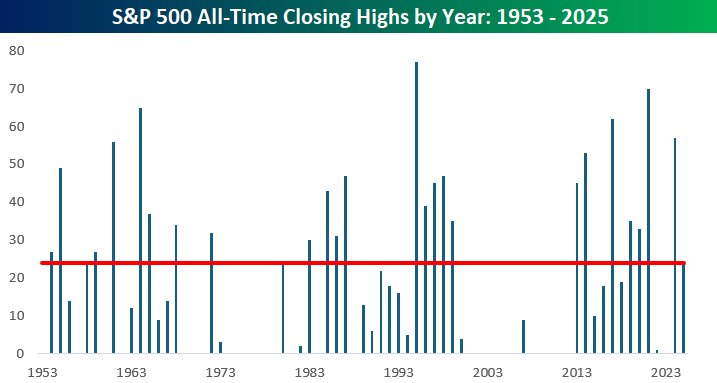

With yesterday’s new high, the S&P 500 has now had 24 record closing highs this year. While it’s above the historical average of 18 per year, 24 is hardly extreme by any stretch of the imagination, and it’s less than half of last year’s total of 57. On the other hand, back in early April, was anyone thinking we’d be anywhere close to new highs later this year, let alone hitting them multiple times? Be honest!

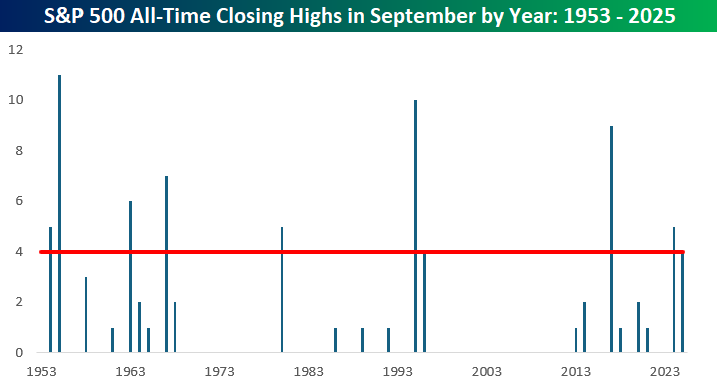

While September is historically known for its weakness, the S&P 500 has already had four record closing highs in eight trading days this month. That may be short of last year’s total of five, but there’s still another 13 trading days left in the month! The record for closing highs in September was 11 in 1955, followed by 10 in 1995, and 9 in 2017. If your memory is good (and long), you’ll remember that those were all good years, and some people reading this may have even been around for all of them!