Chart of the Day – Rate-Cut Fed Days and Beyond

Bespoke’s Morning Lineup – 9/17/25 – Everybody Rallies

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To hell with facts! We need stories!” – Ken Kesey

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The long-awaited Fed decision day has arrived, and despite an Atlanta Fed GDPNow forecast for growth of 3.4% in Q3, stronger-than-expected retail sales in August, still relatively low (but admittedly rising jobless claims), and higher-than-normal inflation, the Fed will likely cut rates this afternoon. That’s not to say there is no justification for a rate cut. Continuing jobless claims remain elevated, job growth has practically evaporated, and both the manufacturing sector of the economy and housing remain weak. Additionally, other secondary indicators, such as heavy truck sales, have been particularly weak. There are very few people who would say that the Fed should not be cutting rates today, but given how fast sentiment towards rate cuts has shifted, it’s hard to argue that the President using the bully pulpit of the White House hasn’t at least played in role in shifting the conversation.

Heading into today’s session, equity futures are modestly negative along with treasury yields, crude oil, gold, and crypto. Housing Starts and Building Permits were also just released, and both reports missed expectations by a relatively wide margin, providing more justification for a cut today.

Overnight in Asia and this morning in Europe, equity markets had mixed returns. CPI in the Eurozone came in lower than expected, while it was hotter than expected in the UK. On a y/y basis, CPI for the Eurozone came in slightly lower than expected at 2.0% compared to forecasts for 2.1%.

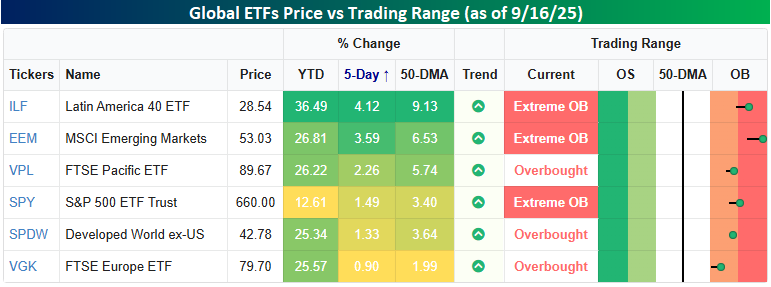

As we head into this afternoon’s expected rate cut from the Federal Reserve, US stocks have been in rally mode, but they’re not alone, at least from the perspective of a US investor. The snapshot below from our Trend Analyzer shows where various global ETFs closed yesterday relative to their short-term trading ranges. The S&P 500, as measured by the SPDR S&P 500 ETF (SPY) is up 1.5% over the last five trading days and closed yesterday in ‘extreme’ overbought territory (more than 2 standard deviations above its 50-DMA), but it’s not the only one and certainly not the best performer. Of the ETFs shown in the spotlight, three have outperformed the US over the last week, and SPY is the worst performer on a YTD basis.

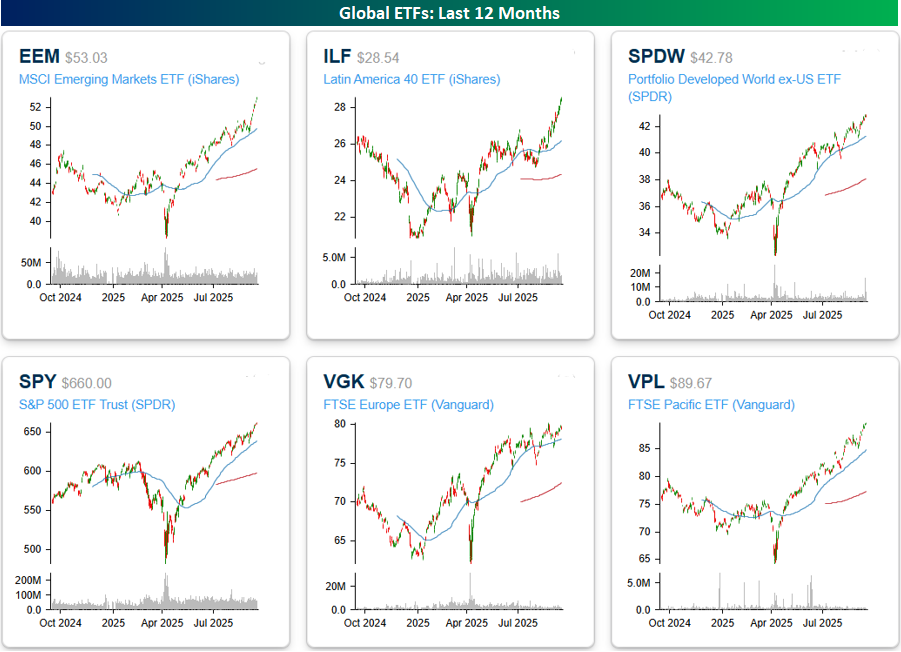

A look at one-year price charts of all six ETFs shows that they’re all either at or right near 52-week highs heading into today’s session. The only difference is the slope of their advances heading into those highs. The MSCI Emerging Markets ETF (EEM) and the Latin America 40 ETF (ILF) have been moving almost vertically over the last couple of weeks, while the FTSE Europe ETF (VGK) has been moving in more of a sideways range.

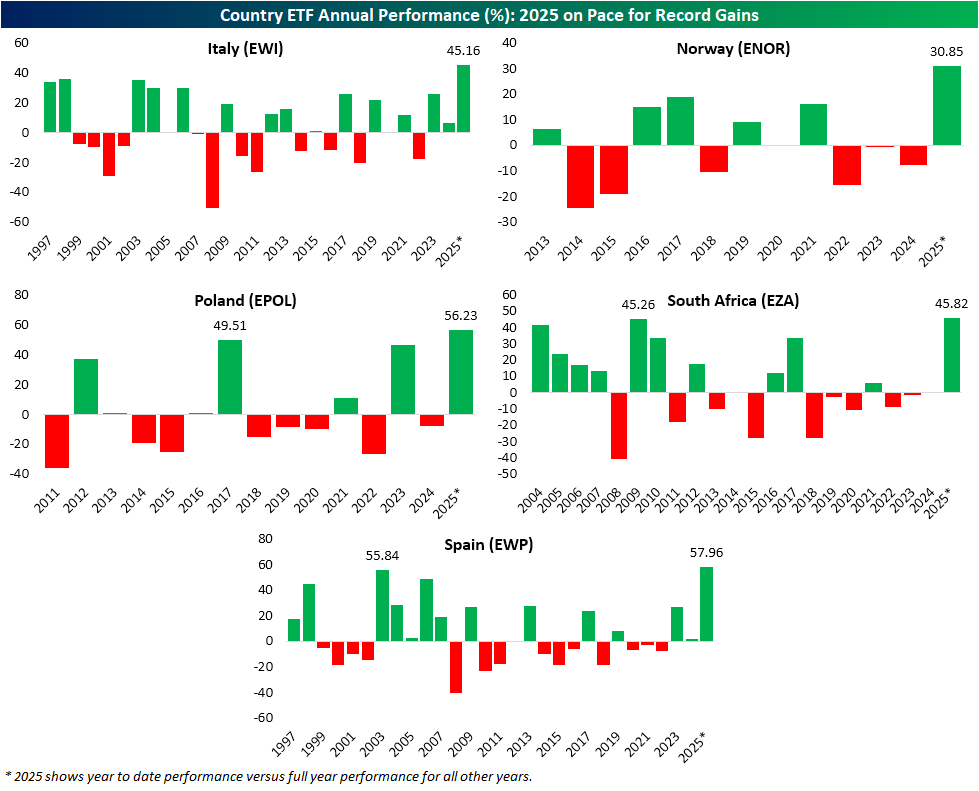

Country ETFs Looking for Record Years

Now in the home stretch of Q3, international stocks have had a banner year in 2025. Whereas the United States’ S&P 500 (SPY) is currently up 12.7% year to date, the MSCI All World Ex. US ETFs (ACWX) have gained well over 24% in that same span. Looking at individual country ETFs in the iShares MSCI family, there have been some monumental winners. For example, Italy (EWI) is up over 45% on a year to date basis. That puts it on pace for the ETF’s largest annual gain on record (it began trading in March 1996) if it holds. The ETF tracking Spain (EWP) has similarly been around since the late 1990s, and its 58% gain this year narrowly beats the 55.8% gain observed in 2003 for its best year on record. Elsewhere in Europe, Norway (ENOR) and Poland (EPOL) are likewise sitting on what would be record gains, although those ETFs have much less extensive histories of a little more than a decade. Finally, we would note that outside of Europe, there is one other country whose tracking ETF is looking for a record. That is South Africa (EZA) which is currently up 45.8%. While that is in fact looking to be a record annual gain, it’s by a much more narrow margin than the others. In 2009, EZA rose 45.3% which is only 50 bps of underperformance relative to this year.

The Closer – Retail Strength, The Dollar, Internationals – 9/16/25

Log-in here if you’re a member with access to the Closer.

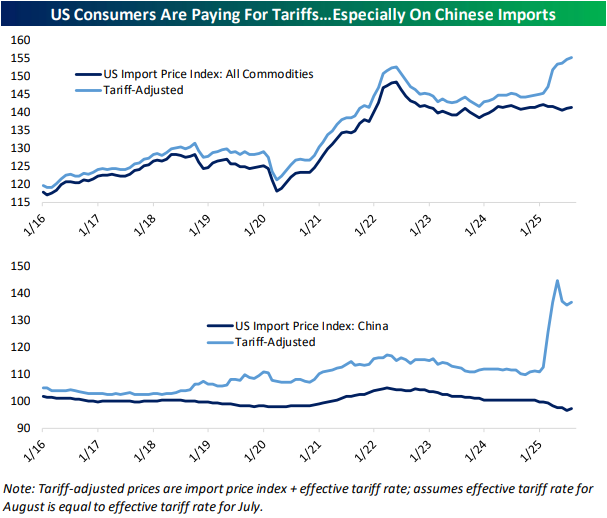

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look at how retail sales have outpaced inflation (page 1) before checking in on various other releases of the day including GDP tracking, homebuilder sentiment, heavy truck sales (page 2), and NY Fed service data (pages 2 and 3). We then dive into tariff effects on trade prices and the dollar (page 4). We also include a look at the dollar versus a handful of currencies (page 5) before finishing with a check up on international market performance (pages 6 and 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/16/25

Chart of the Day – New Highs and Apple Crosses

B.I.G. Tips – Strong Retail Sales

Bespoke’s Morning Lineup – 9/16/25 – Streaky Semis

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The beautiful thing about learning is nobody can take it away from you.” – B.B. King

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We’re looking at another positive start to the market this morning, with futures modestly higher and the Nasdaq leading the way as mega-caps continue to lead the way. This morning’s economic calendar includes Retail Sales and Import Prices at 8:30, Industrial Production and Capacity Utilization at 9:15, and then Business Inventories and Homebuilder Sentiment at 10. After that, pretty much all of the focus will shift to tomorrow’s announcement from the FOMC, where rates are widely expected to be cut 25 bps.

This morning’s gains follow what was mostly a positive session in Asia. The highlight of the region was South Korea, where the Kospi rallied more than 1% for its 11th straight daily gain. In Europe, the tone isn’t as positive as the STOXX 600 trades down 0.2% even as the ZEW survey of economic sentiment unexpectedly increased, although Industrial Production for the Eurozone rose less than expected (0.3% vs 0.4%).

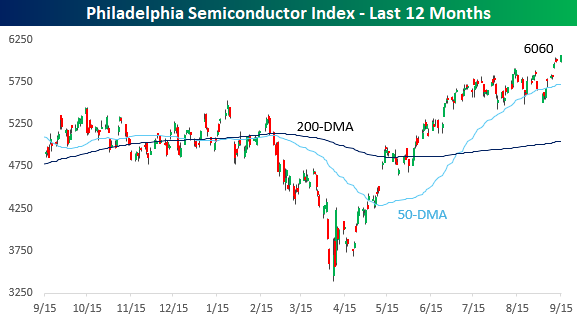

Like the major indices, semiconductor stocks have been lurching to new all-time highs, and when the semis are rallying with the overall market, it’s usually a good sign. After several successful tests of the 50-day moving average (DMA) in the summer, the Philadelphia Semiconductor Index (SOX) finally broke out above resistance last Wednesday.

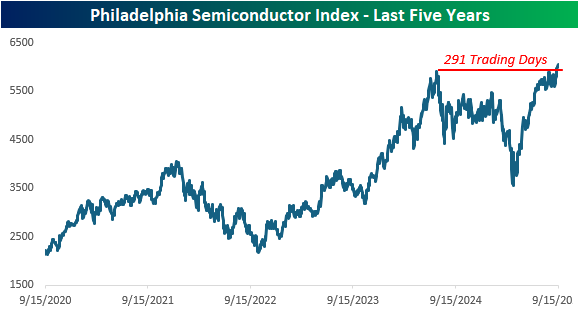

The breakout to new highs also ended a streak of more than a year during which the index had not traded at an all-time high. At 291 trading days, it was the fifth-longest drought without a new high in the SOX’s history, dating back to 199,4, and the sixth-longest that lasted longer than a year. The longest streak was nearly 4,500 trading days ending in January 2018, and the second-longest ended less than two years ago in December 2023 at 488 trading days.

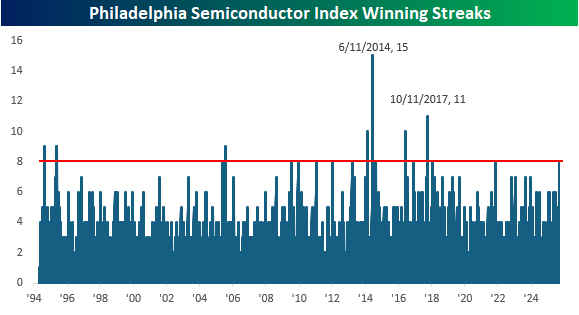

In the process of breaking out to new highs, the SOX has also traded higher for eight straight trading days, trailing the Nasdaq 100’s streak by a day. That eight-day streak is tied for the longest streak since October 2017, when it went more than two weeks in a row without trading lower. The longest streak was three weeks long, ending in early June 2014.

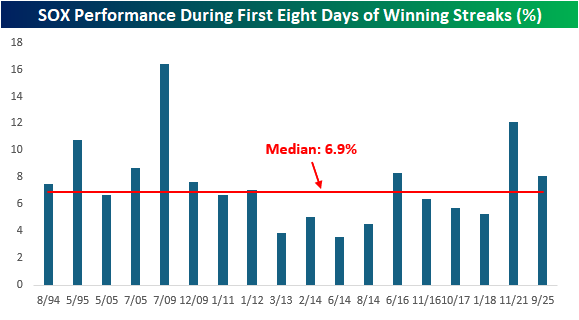

Over the course of the SOX’s eight-day streak, the index has rallied 8.1%, which comes in modestly ahead of the median gain of 6.9% during the first eight days of all 18 streaks and the sixth best overall.

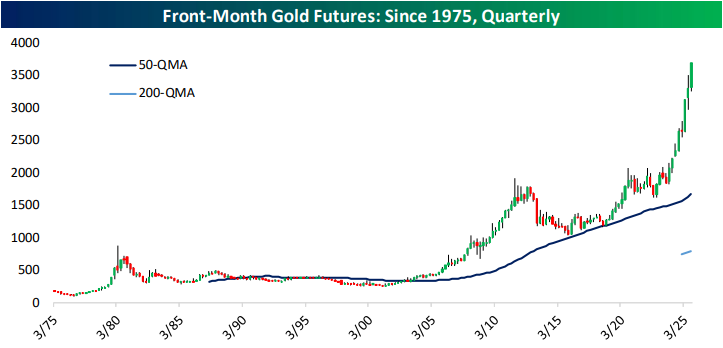

The Closer – Price vs. Breadth, Farming, Gold – 9/15/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look into the rare disconnect of extreme overbought stock prices on weak breadth (page 1). We follow up with a rundown on the rough go for farming (page 2) including farm employment and ag prices (page 3). We then provide a technical checkup on gold (pages 4 and 5) before pivoting over to the latest positioning data (pages 6 and 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!