The Bespoke Report – 9/19/25 – “It’s About Time”

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week, we review the consistently overbought nature of the market, demand for equities, the FOMC’s resumption of rate cuts, the state of the economy, where breadth stands, and finally, a review of one and five-year charts of the major indices, sectors, and asset classes. Give it a read!

The Closer – Russell’s New High, Courts, Valuations – 9/18/25

Log-in here if you’re a member with access to the Closer.

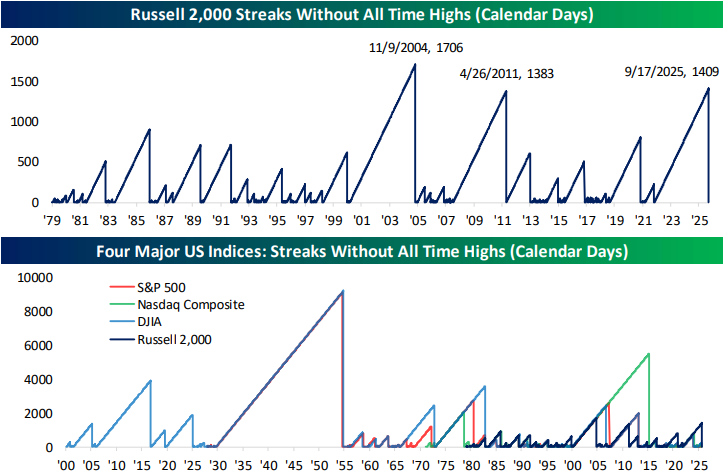

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the Russell 2,000’s breakout to fresh all time highs, comparing its streak without a high to similar streaks of the past (page 1). Next, we review today’s news surrounding the Supreme Court, Fed Governor Cook, and tariffs (page 2). We then delve into equity market valuations (pages 2 and 3) before shifting into macro data that includes claims (page 4), TICS (page 5), regional Fed Manufacturing gauges (page 6), and freight volumes and prices (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 9/18/25

Chart of the Day: NVIDIA (NVDA) Falls Behind

Bespoke’s Morning Lineup – 9/18/25 – Slow Moving Rally

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“He who waits to do a great deal of good at once will never do anything.” – Samuel Johnson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Investors apparently slept on the Fed’s announcement yesterday and woke up in a good mood. The S&P 500 is on pace to open up by 0.75% this morning, while the Nasdaq is on track to open up by more than 1%, and small caps are leading the way with a gain of 1.25%. The US strength follows what was a mostly positive night in Asia, where China was the only country to trade lower, while Japan and Korea both shot higher by over 1%. The strength in Japan came even as Machinery Orders fell 4.6% m/m compared to forecasts for a drop of just 1.8%. In Europe, stocks are also higher across the board as the STOXX 600 rallies 0.8%.

This morning in the US, there’s little in the way of earnings data, and the only reports on the economic calendar are jobless claims at 8:30 and the Philly Fed and Leading Indicators at 10 AM.

Like the quote above, the market’s grind higher for the last several months has been more gradual than a move concentrated into a handful of days. There are several ways to illustrate this, and we’ll start with the VIX. At 14.8 this morning, the VIX is on pace for its lowest close since late August, not exactly a level you would expect for what historically has been one of the most volatile months of the year. As shown in the chart below, if the VIX was an EKG, we’d be putting a sheet over the patient as it has flatlined since first falling back below its 200-DMA in June.

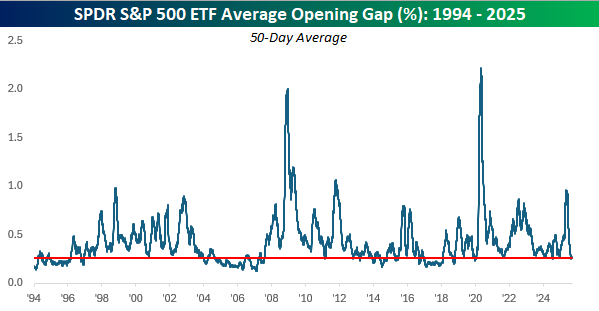

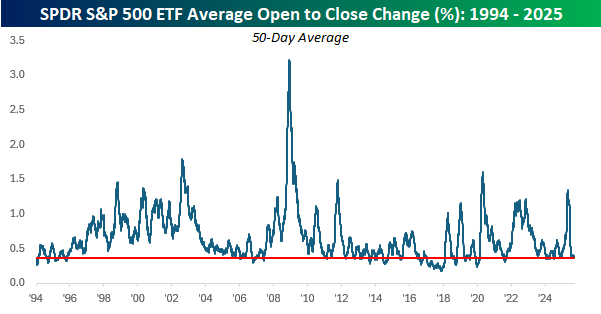

In addition to the low VIX, another example of the gradual moves is by looking at the S&P 500’s average opening gap. Using SPY as a proxy, the S&P 500’s average change at the open relative to the prior days’ close over the last 50 trading days has been 0.25%, and there has only been one day when the S&P 500 gapped up or down more than 1% (9/2/25: -1.17%). After volatility at the open rocketed to the highest levels since COVID back in April, the average daily change has sunk like a stone to some of the lowest levels of the last five years.

Just as volatility has been subdued at the opening bell, it has also been tamed during regular trading hours. Just like the average opening gap, intraday volatility shot higher in April only to come crashing down in the summer to around the lowest levels of the last five years. The old cliché says to never short a dull market, and that’s the only piece of advice an investor has needed over the last few months.

The Closer – FOMC Reactions, Residential Construction – 9/17/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap the Fed decision beginning with a review of the update of the Summary of Economic Projections (page 1) followed by a dive into the market’s reaction to the rate cut (pages 2 and 3). We wrap up the report with a review of the latest residential construction figures (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 9/17/25

Bespoke Baskets Update – September 2025

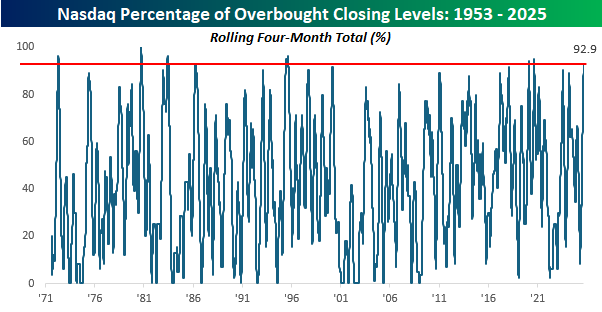

Overbought Becomes the Norm For the Nasdaq

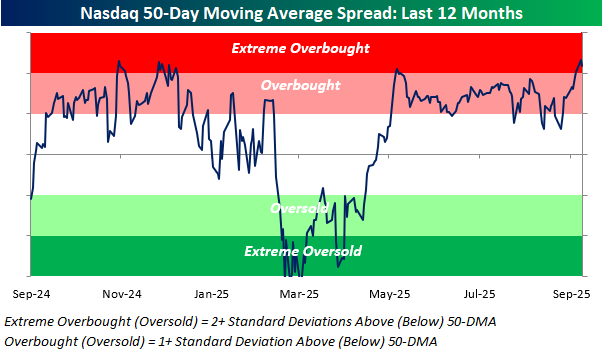

The chart below shows the Nasdaq’s daily close relative to its trading range expressed in terms of standard deviations relative to its 50-day moving average (DMA). We also update a similar chart for the S&P 500 every day in our Morning Lineup. When the line is in the white zone, it indicates that the Nasdaq is trading within its normal trading range (less than one standard deviation above or below the 50-DMA). When it rises into the red zones, it indicates various levels of overbought, while readings in the green zones represent short-term oversold levels. Heading into this morning, the Nasdaq was firmly into ‘extreme’ overbought territory (2+ standard deviations above its 50-DMA) after trading almost exclusively at overbought levels for the last four months.

Normally, overbought or oversold levels revert to the mean over time, so situations like the present are very unusual. Over the last four months, the Nasdaq has closed at overbought levels on just under 93% of trading days. While readings this high aren’t unprecedented, they are rare. In fact, there hasn’t been a higher frequency of overbought daily closes for the Nasdaq in a four-month window since August 2020, and the reading has only been above 85% on 0.04% of all trading days in the Nasdaq’s history. Overbought markets can’t stay overbought forever, so eventually we’ll see the market pull back from these levels, but for now, it’s been an unbelievable run.

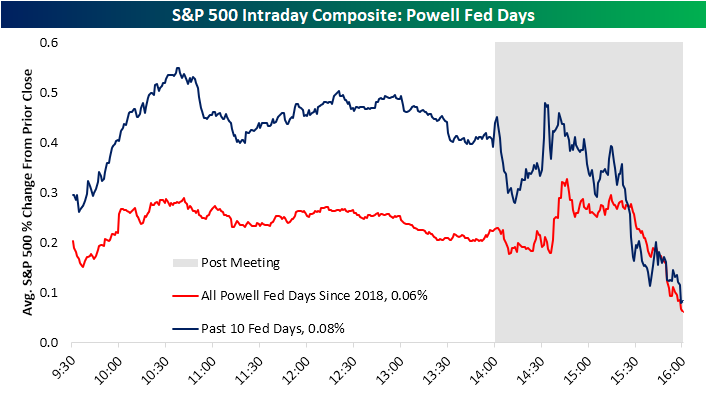

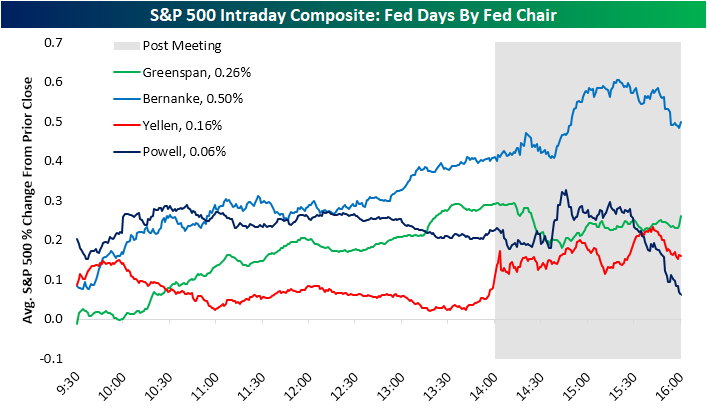

Another Powell Fed Day

Fed Day is here! The FOMC concludes its meeting this afternoon and in all likelihood Powell and company will cut rates by 25 bps. As we have highlighted in the past, when it comes to how stocks respond to the FOMC, Powell Fed Days have on average been the worst of any Fed Chair. By the close of trading, the S&P 500 has only averaged a 6 bps gain on Fed days since Powell has been at the helm. That compares to 16 bps for his predecessor, a 50 bps gain for Bernanke and a 26 bps gain for Greenspan. While that may be the case for full-day changes, it’s worth nothing that earlier in the day would be an entirely different story. In fact, between 2:30 PM EST and up until the final half hour of trading, Powell Fed days have actually been on pace for the second strongest stock price reactions of any Fed chair. That means sharp declines at the end of the day can largely be credited for the Fed day weakness during Powell’s tenure. It almost wouldn’t be a Powell Fed day without a post-presser sell-off!

Below is a closer look at the S&P 500’s average intraday path on Powell Fed days. The red line shows the S&P’s average path across all 61 Powell Fed days since his tenure began in 2018, while the blue line shows just the last ten Powell Fed days. Under both scenarios, the market has been sitting on solid gains heading into the 2 PM ET rate decision, but the final hour of trading has averaged a pretty steep drop.