Bespoke’s Weekly Sector Snapshot — 3/19/26

Powell Performance – Winners and Losers Since Fed Chair Began

The S&P 500 fell 1.36% on Fed Chair Powell’s penultimate FOMC day on Wednesday (3/18/26). While a hallmark of Powell’s tenure as Chair has been the stock market’s tendency to trade sharply lower in afternoon trading on Fed Days, the market has also done very well over the entirety of his 8+ year term.

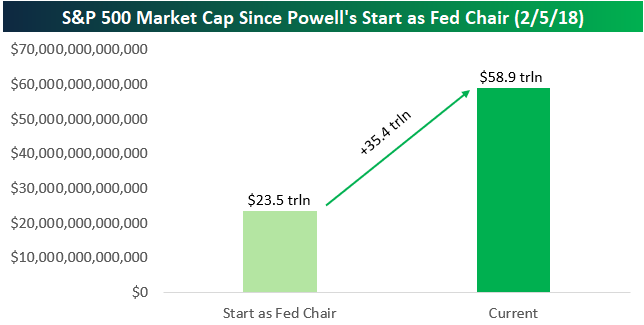

When Powell became Fed Chair in February 2018, the combined market cap of stocks in the S&P 500 was $23.5 trillion. That number has ballooned by $35.4 trillion up to $58.9 trillion today.

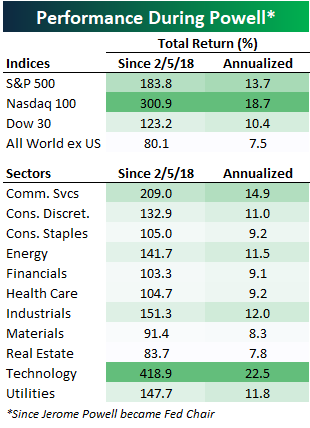

The S&P 500 has gained more than 180% since 2/5/18 when Powell became Chair, representing an annualized total return of 13.7%. The tech-heavy Nasdaq 100 has gained much more at 300.9% (18.7% ann.), while the Dow 30 is up 123%.

Compared to the rest of the world, Powell has kept US markets in a dominant position. The S&P has beaten the rest of the world by more than 100 percentage points since his time as Chair began.

Looking at sector performance, Technology has more than doubled the next-best sector (Communication Services) during Powell’s tenure. As shown above, Tech has returned 418% since Powell took over, while Materials and Real Estate are the only two sectors that haven’t at least doubled.

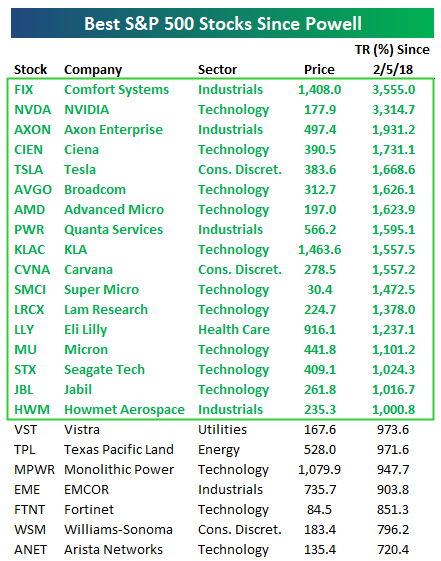

Of the current S&P 500 members that were trading back in early 2018 when Powell became Chair, 59% have gained at least 100% since then. There are nearly just as many S&P 500 stocks up 500%+ (39) since Powell’s tenure began as there are stocks that are down (45).

Below is a table showing the best-performing S&P 500 stocks since Powell became Chair, with the seventeen “10-baggers” highlighted in green.

You may have thought NVIDIA (NVDA) would be at the top of this list given its place as the largest company in the world right now, but a company that’s just over a tenth of NVDA’s size actually has it beat. Comfort Systems (FIX) — which builds out the mechanical, electrical, and plumbing systems for AI data centers and other infrastructure projects — is actually #1 when it comes to share-price performance under Powell. As shown, FIX is up 3,555% compared to a gain of 3,314% for NVDA.

Most of the names on the list of big winners since Powell became Chair are directly related to the AI Boom, but some that are not include Axon Enterprises (AXON) — which sells Tasers and police bodycam hardware and software, Carvana (CVNA) — which sells used cars, and Eli Lilly (LLY) — which sells weight-loss drugs and other pharmaceuticals.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

While there are seventeen “10-baggers” since Powell became Chair, not all of those stocks are in uptrends right now. Below are price charts for the six best performers in our table above. While Ciena (CIEN) and Comfort Systems (FIX) remain in strong uptrends, the other four have either traded sideways or lower over the last six months.

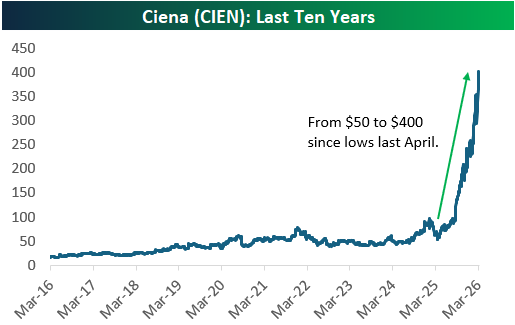

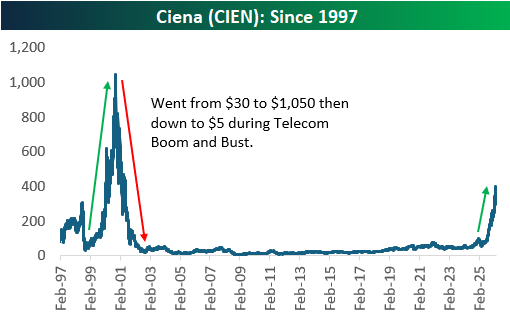

Of the six biggest winners under Powell, Ciena (CIEN) is the only one trading at record highs today. Its price action lately has been a sight to behold.

Last year at the tariff-tantrum lows, the stock was trading in the low-$50s. It’s currently trading above $400.

Ciena (CIEN) somewhat slid under the radar in the early years of the AI Boom, but over the last year or so, investors haven’t been able to get enough of it.

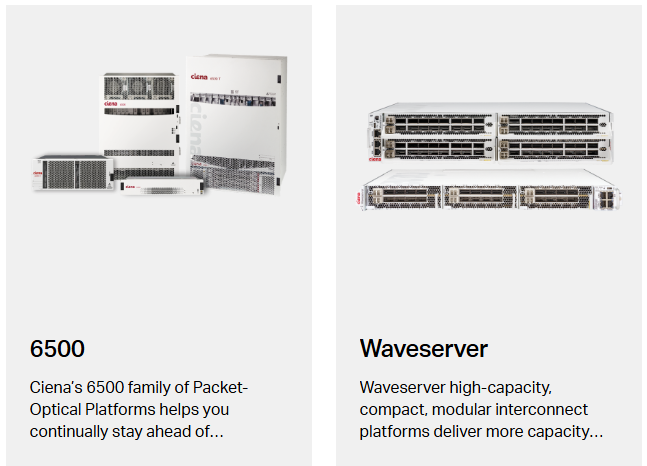

That’s because Ciena makes some of the most important networking gear for AI data centers (shown below). Every time a company makes a bigger, smarter LLM for consumption, they need more of Ciena’s gear to make that data work and move faster.

What’s even crazier about Ciena (CIEN) is that even though the stock is up nearly 1,000% in the last few years and 1,700% since Powell became Fed Chair, it still hasn’t gotten back to half of what it peaked at during the Dot Com Bubble of the late 1990s.

Just as Ciena is a key player in the AI infrastructure build-out right now, it was also a key player in the Internet/Telecom buildout of the late 1990s. After rallying from $30 to north of $1,000/share at its peak, shares plummeted to as low as $5 after the bubble burst in the early 2000s.

This should be a key reminder of how carried away investors can get during market manias, but it also shows that while the AI Boom indeed has a lot of hype, things were even crazier back in the late 90s.

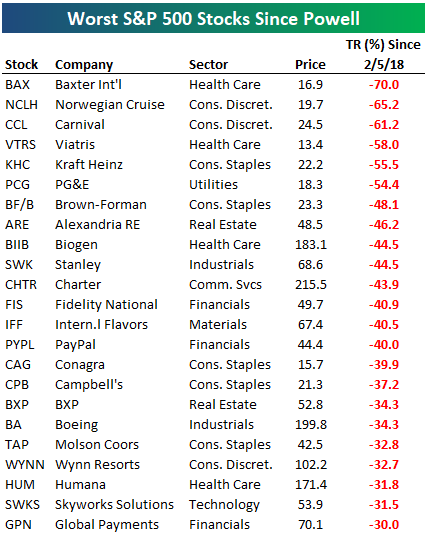

So far we’ve only discussed winners since Powell became Fed Chair, but below is a list of the S&P 500 stocks that have done the worst over his tenure. The names shown are the 23 stocks down at least 30% since 2/5/18, led by Baxter International (BAX) with a 70% drop.

Two cruise-lines rank 2nd and 3rd worst (Norwegian and Carnival) with declines of more than 60%, and another three stocks have been more than cut in half: Viatris (VTRS), Kraft Heinz (KHC), and PG&E (PCG). Other well-known names on this list of losers include Biogen (BIIB), PayPal (PYPL), Campbell’s (CPB), Boeing (BA), Molson Coors (TAP), and Wynn Resorts (WYNN).

Like this analysis? Become a Bespoke Premium member today using our March Madness special! Click below for details on how to sign up:

Chart of the Day: Bears Roar

Bears Cross 50%

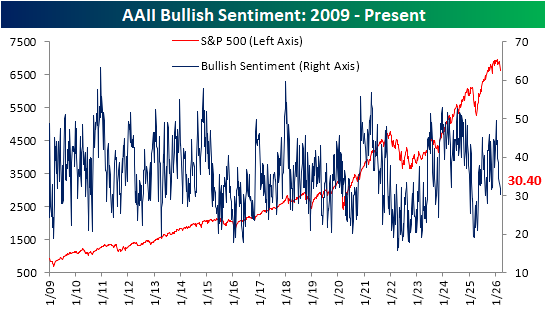

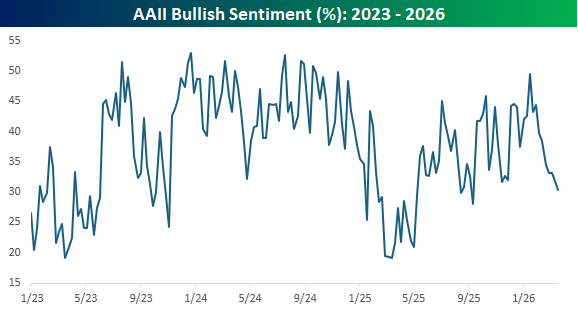

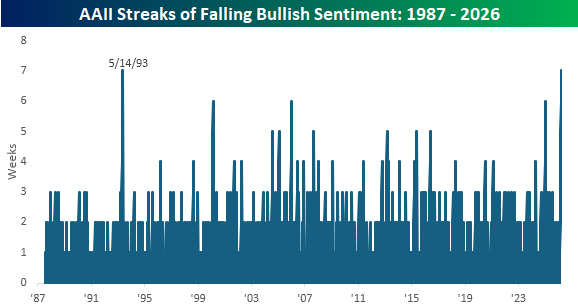

As if news headlines and price action haven’t been signals enough, investor sentiment readings are also pointing toward negative outlooks in the wake of the conflict in the Middle East. The American Association of Individual Investors (AAII) weekly sentiment survey saw only 30.4% of respondents report bullish sentiment this week. That is the lowest level since the week of 9/11/25, when it registered 28%. Additionally, as we first highlighted in today’s Morning Lineup, the 1.5 percentage point drop this week marked the seventh consecutive weekly decline in bullish sentiment, which ties another 7-week-long streak from May 1993.

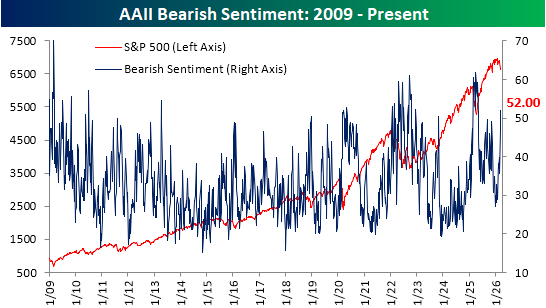

Given the drop in bulls, bearish sentiment has continued to surge. This week, the reading rose another 5.6 percentage points to 52%. That is the highest reading since last May, when it was at 59.3%. Throughout the survey’s history since 1987, less than 5% of weekly readings have seen more than half of respondents report as bearish.

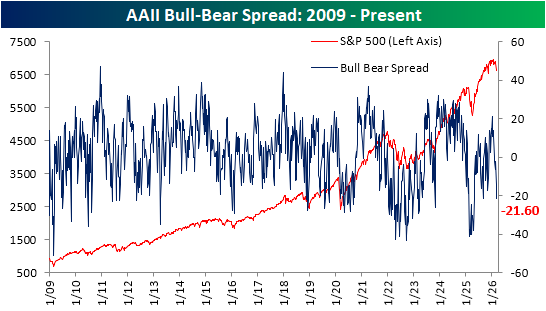

With inverse moves in bulls and bears, the bull-bear spread fell to -21.6. That narrowly surpasses the previous local low of -21.5 from the week of 9/11/25, registering the worst reading since last May.

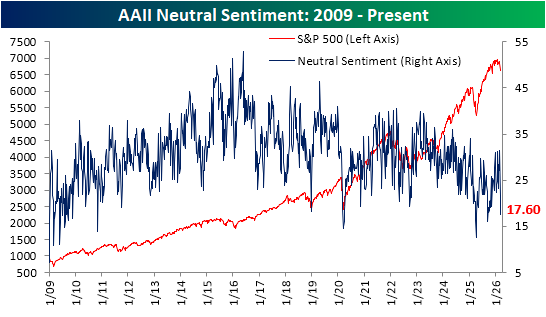

We would also note that not only has there been a big move toward bearish sentiment due to lost bullishness, but a big drop in those reporting neutral sentiment has also been a factor. Only two weeks ago, 31.4% of respondents reported neutral sentiment for the highest reading since January 2025. In the two weeks since then, it has fallen to 17.%, which ranks in the 4th percentile of all periods on record, and is the lowest since a reading of 16% last September.

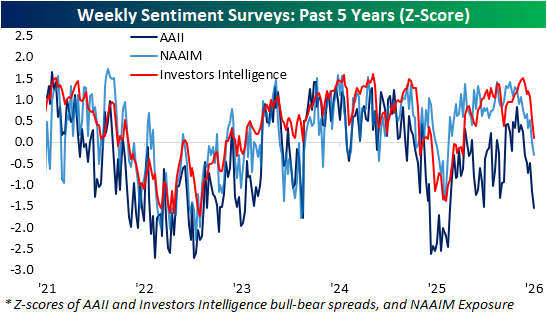

In other words, sentiment has turned overwhelmingly bearish. That is also reflected in other surveys like the Investors’ Intelligence and NAAIM Exposure index readings. The latter now indicates the lowest level of long exposure to equities since last spring, and that reading is now also below the historical average. The Investors’ Intelligence survey is still marginally bullish relative to historical norms, although it too is quickly approaching bearish readings.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Bespoke’s Morning Lineup – 3/19/26 – Unlucky Seven

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you don’t understand what the professor is saying, don’t dismiss the possibility that he might be wrong.” – Paul Volcker

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

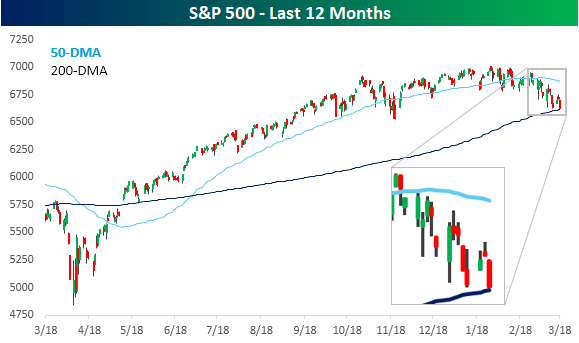

After a relatively strong start to the week, where it looked like the market would be able to look past the spike higher in energy prices, continued tensions in the Middle East and the stubbornly high level of crude oil prices have pushed the S&P 500 back into the red for the week, with further downside in store for today. S&P 500 futures are trading down 0.4%, which would put the S&P 500 below its 200-day moving average (DMA). The Nasdaq, which already closed below its 200-DMA yesterday, is expected to add to that breakdown with a decline of 0.5%.

International markets had a terrible night, with most major averages in the region down at least 2% and in most cases much more. That’s the same trend in Europe as well, with the STOXX 600 down over 2%, as is the case with most indices in the region.

As we’ve been pointing out all along, the declines are all about energy prices, and this morning, they’re not helping out as WTI trades up 2% to more than $98 per barrel, while Brent trades up by nearly 7% to $115 per barrel. The spread between Brent and WTI is now a monstrously high $16+ per barrel.

Treasury yields are moving higher as investors fear the inflationary impacts of rising energy prices, and the 10-year yield is now testing 4.3%. Gold prices are plunging more than 5% to under $4,700 per ounce, and Bitcoin is back below $70K.

The economic calendar is relatively busy this morning with jobless claims and Philly Fed at 8:30, while New Home Sales and Wholesale Inventories will hit the tape at 10 AM. Jobless claims came in lower than expected on an initial basis but slightly higher than expected on a continuing basis, while the Philly Fed was actually better than expected. With everything going on in the Middle East, though, the data is basically meaningless.

As the quote of the day notes, in many aspects of life, change has a way of happening slowly and then all at once. For months, the S&P 500 has been trading in a sideways range, consolidating the gains from the April lows. Then, all of the sudden we have a day like yesterday where the S&P 500 sells off a not necessarily dramatic 1.4%, but then all of the sudden, we’re looking at an S&P 500 whose 50-day moving average (DMA) has just started to slope downward just as the index is on the verge of trading below its 200-DMA for the first time since last spring. Steady uptrend to sideways range and now a potential downtrend? Change happens slowly until it doesn’t.

With the S&P 500 slowly (and now more suddenly) trending lower, investor sentiment has also been on the decline. In the latest survey from the American Association of Individual Investors (AAII), bullish sentiment declined from an already low level of 31.9% to 30.4%, which is the lowest level since last September, as the uptrend in sentiment since the lows early last year has been firmly broken.

With this week’s decline, bullish sentiment has now declined for a record seven straight weeks. That’s now tied with the seven-week streak from May 1993 for the longest weekly losing streak in the survey’s history. Behind these two streaks, there were three others (Feb 2000, Jan 06, and Jan 2025) that lasted six weeks. Based on how the market traded yesterday, if we don’t see an improvement in the next couple of days, we would expect that this current streak could move into first place all on its own.

The Closer – FOMC, TICS, PPI – 3/18/26

Log-in here if you’re a member with access to the Closer.

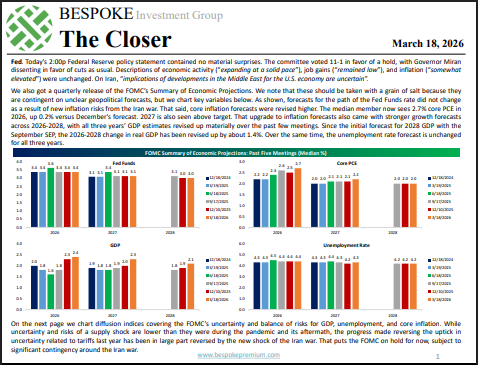

- Today’s Federal Reserve policy statement contained no material surprises and Fed Chair Powell’s presser was also mostly unremarkable.

- DRAM/NAND memory producer Micron (MU) blew the doors off earnings with revenues 21% above estimates and triple what they were a year ago.

- The latest PPI release showed that costs were broadly accelerating even before the recent leap in gasoline and diesel prices.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/18/26

Bespoke Baskets Update – March 2026

Q4 2025 Earnings Conference Call Recaps: Williams-Sonoma (WSM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Williams-Sonoma’s (WSM) Q4 2025 earnings call.

![]()

Williams-Sonoma (WSM) is a premium home furnishings retailer operating a multi-brand portfolio including Pottery Barn, West Elm, and Williams-Sonoma, selling furniture, décor, kitchenware, and design services through a digital-first, omnichannel model. WSM delivered a 3.2% Q4 comp and 20.3% operating margin despite tariff headwinds and weak housing turnover, gaining share while maintaining full-price selling. Management emphasized resilience to tariffs through sourcing and pricing actions, with margin pressure expected to be front-half weighted in 2026. Growth is being driven by product newness, collaborations, and emerging brands, while B2B (+10% FY growth) and Rejuvenation remain key white-space opportunities. The company is pivoting back to retail expansion (20 new stores, 19 repositions) after years of optimization. Pottery Barn lagged in Q4 due to weak décor assortment, but is being reset with stronger product and brand positioning. WSM reported weaker revenue on better-than-expected EPS, resulting in shares up as much as 6% on 3/18…

Continue reading our Conference Call Recap for WSM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: