Chart of the Day: Cue the “Truth”

Bespoke’s Morning Lineup – 3/23/26 – Early Morning Reversal

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Appear weak when you are strong, and strong when you are weak.” – Sun Tzu

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Asian stocks plunged overnight, Europe was lower, and US futures were in the red about an hour ago, but all it took was one Truth Social Post to erase those losses and push stock futures firmly into the green. The S&P 500 and Nasdaq are both on pace to gap up more than 1.5% at the open, and European stocks are up by about 1%. Treasury yields are modestly lower, but the 10-year yield is still at an uncomfortably high 4.39%. After trading higher earlier, crude oil is down 7% to just under $92 per barrel. Gold is still trading down by close to 4%, sitting at $4,400 per ounce. At the end of January, it was more than $1,000 higher!

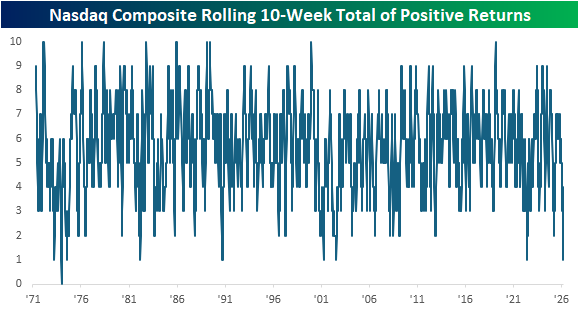

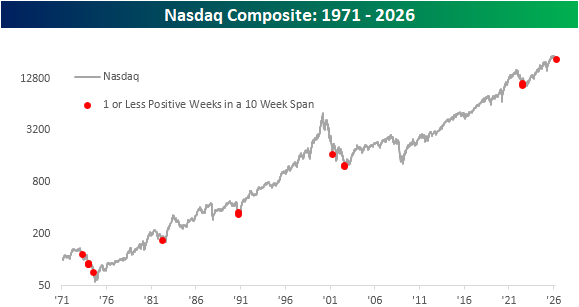

After last week’s declines, the Nasdaq finished lower for the fourth week in a row and the ninth week in the last ten. For ten weeks, that’s the fewest positive weeks since June 2022 and before that, July 2002. In the Nasdaq’s entire history, there have only been eight other periods when the Nasdaq declined for nine or more weeks in ten weeks, and only one of those periods saw the Nasdaq go ten straight weeks with declines.

Below, we show when each of these prior periods occurred on a long-term chart of the Nasdaq. Outside of the period in the mid-1970s, these other occurrences all came in the later stages of market declines. That sounds like good news, but a counter to that is that the only other time the Nasdaq declined for nine weeks in a ten-week span and was still so close to 52-week highs was in that early 1970s period.

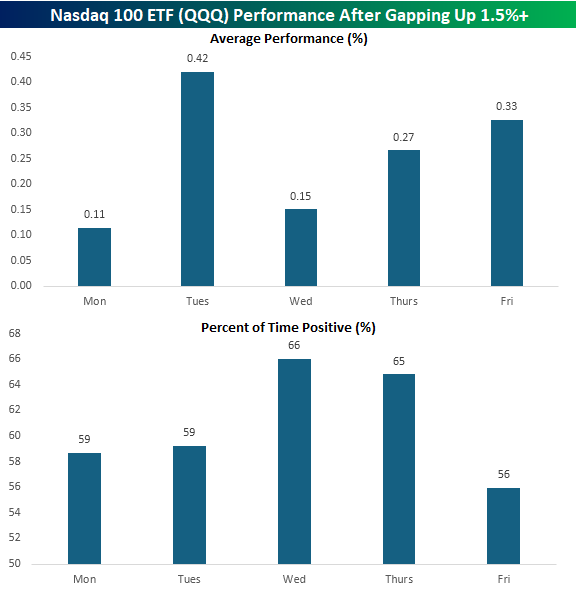

While it was looking like another negative start to the week earlier, futures took a sharply positive turn after the President’s Truth Social post saying that the US and Iran had engaged in conversations “regarding a complete and total resolution” of hostilities. As a result, the Nasdaq 100 ETF (QQQ) is on pace to gap up 1.5% at the open. If those gains hold through the open, it would be the first 1.5%+ upside gap for QQQ this year and the 266th since the ETF’s inception in 1999.

The chart below shows QQQ’s average performance from the open to close after gapping up 1.5%+ at the open based on the day of the week it occurred. Of the 46 that occurred on a Monday, QQQ’s average performance from the open to close was a gain of 0.11% with positive returns 59% of the time. While positive, that ranks as the worst performance from the open to close following a 1.5%+ upside gap of any other weekday.

Brunch Reads – 3/22/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

A Tradition Unlike Any Other: The first Masters Tournament began on March 22, 1934, at Augusta National Golf Club, though, at the time, it was known as the Augusta National Invitation Tournament. Founded by Bobby Jones and Clifford Roberts, the event was conceived as a gathering of top players on a course designed to reflect Jones’ ideal vision of golf. Augusta National was still in its infancy, lacking many of the defining features and traditions that now make it iconic.

A field of 72 players teed it up in that inaugural event, both professionals and amateurs, in a relatively understated competition compared to today’s tournament. Horton Smith became the first champion, finishing at four under par and earning $1,500. There were no green jackets, no ceremonial traditions, and even the course was different. Back then, players started their round on what is now the back nine and finished on what we now know as the front nine. This meant that Amen Corner (holes 11–13), arguably the most pressure-filled stretch in golf, was played at the beginning of the round rather than near the finish. In 1935, Bobby Jones decided to reverse the nines to create a more exciting finish, which is the layout still used today.

Despite its modest beginnings, the foundation was set for something great. Within a few years, the tournament adopted the name “The Masters,” traditions began to take shape, and Augusta National evolved into one of the most revered stages in sports.

Markets & Investing

SEC Prepares Proposal to Eliminate Quarterly Reporting Requirement (WSJ)

The SEC is considering a rule that would let companies report earnings twice a year instead of quarterly, with a proposal expected soon and a final decision coming after public feedback. Supporters say it could ease the burden of being public, while critics worry it would reduce transparency for investors who rely on frequent updates. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – 3/20/26 – Closure Continues

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we are closely focused on the three week war in Iran and its consequences for energy markets and the economy. The conflict has driven a massive surge in energy stocks around the world with US refiners especially benefitting. But broad indices have plunged into deep oversold territory as stocks reel from a sudden and extreme shift in central bank pricing. We recap a long list of central bank decisions across emerging and developed markets as well as the chaos in bonds markets that spent the week waking up to the risks for interest rates of significant global petroleum shortages. We also review economic data, which this week showed an economy with surprisingly solid labor markets, healthy balance sheets, and accelerating inflation…even before the impacts of oil price surges.

Daily Sector Snapshot — 3/20/26

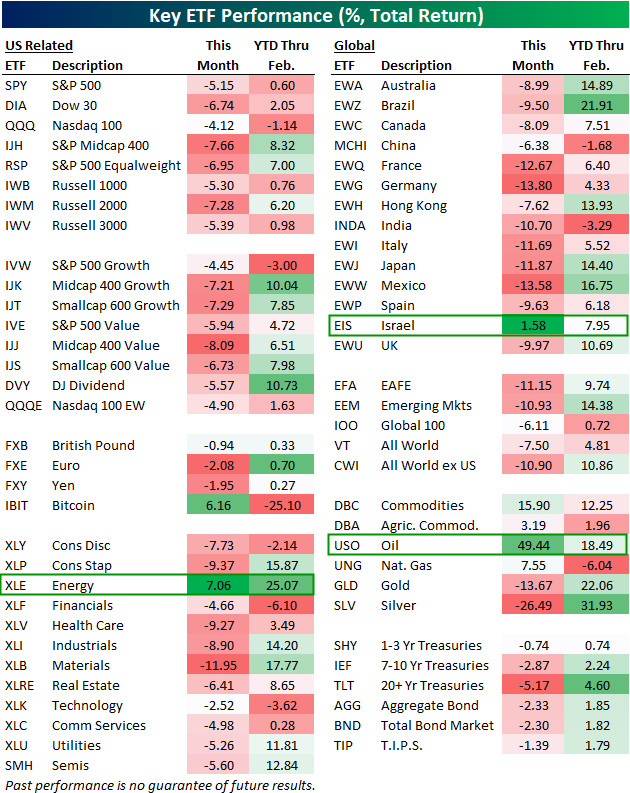

Post-Iran Winners: Oil, Energy, and Israel

Equities around the world continue to take it on the chin this March, with month-to-date performance coinciding with the beginning of the start of the war in Iran over the last weekend of February.

Below is a look at our asset class performance matrix featuring total returns for dozens of ETFs across domestic and international equities, sectors, currencies, commodities, and fixed income.

For each ETF, we show year-to-date performance through February along with performance so far in March.

ETFs across asset classes are bleeding red this month with the exception of a few: Bitcoin (IBIT), the Energy sector (XLE), oil (USO) and other energy/ag commodities, and Israel (EIS). Of these month-to-date winners, oil (USO), the agriculture commodities ETF (DBA), the Energy sector (XLE), and Israel (EIS) are the only ones that were also up year-to-date before the Iran war began.

On the downside, mid-caps and small-caps have been some of the hardest hit domestic index ETFs, with mid-cap value (IJJ) down the most at -8.1%.

Every sector ETF is down this month except Energy (XLE), with Materials (XLB) down the most at -12%.

Outside the US, country ETFs like France (EWQ), Germany (EWG), India (INDA), Italy (EWI), Japan (EWJ), and Mexico (EWW) are all down 10%+ since the war, while gold (GLD) and silver (SLV) have also gotten pummeled. Additionally, fixed income has not offered any safety due to inflation concerns brought about by the war. The 20+ Year Treasury ETF (TLT) is already down 5.2% since the bombings began.

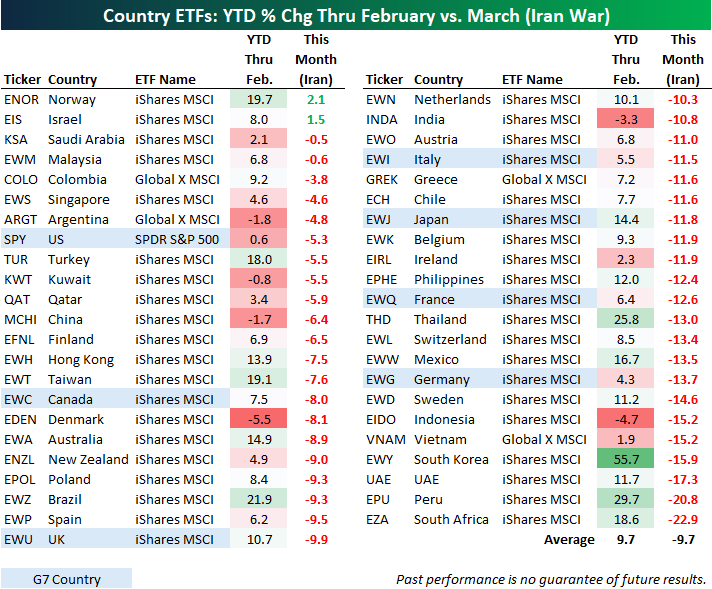

Below is a look at the recent performance of more than 40 country stock market ETFs traded on US exchanges.

On average, these country ETFs were up 9.7% through the first two months of 2026. Since the end of February, though, they’re down an average of 9.7%. Just a few weeks ago, it looked like 2026 was likely to be another year of outperformance for international markets. Now that there’s war in the Middle East and the Strait of Hormuz is unofficially closed for business, countries that heavily rely on energy imports are getting hit (with the exception of Israel). Along with Israel (EIS), Norway (ENOR) is the only other country ETF that’s positive this month. As a reminder, Norway is one of the few non-Middle Eastern countries that’s a net exporter of oil.

Six country ETFs are down 15%+ since the war began: Indonesia (EIDO), Vietnam (VNAM), South Korea (EWY), UAE (UAE), Peru (EPU), and South Africa (EZA).

Of the G7 countries, the US (SPY) is down the least with a decline of 5.3%, followed by Canada (EWC) — down 8%, and the UK (EWU) — down 9.9%.

Like this analysis? Become a Bespoke Premium member today using our March Madness special! Click below for details on how to sign up:

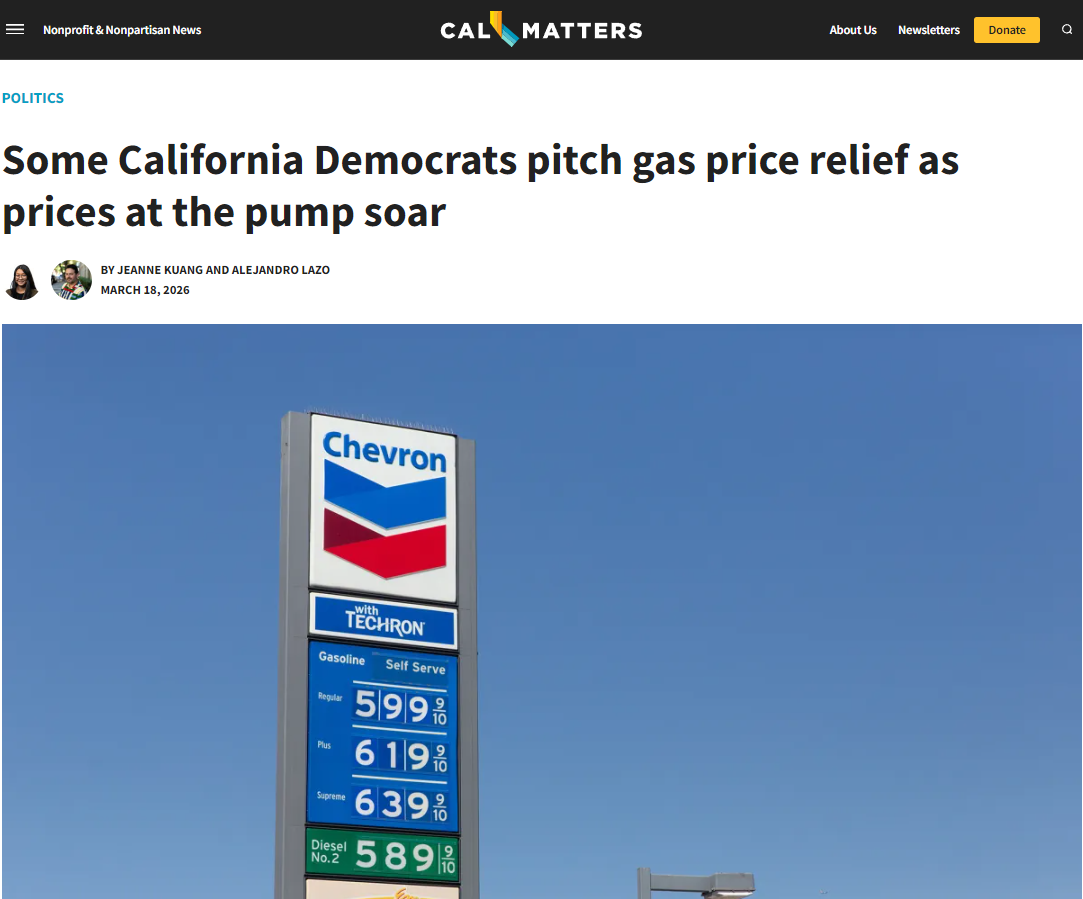

“Sir, We’re Going to Need a Bigger Rabbit”

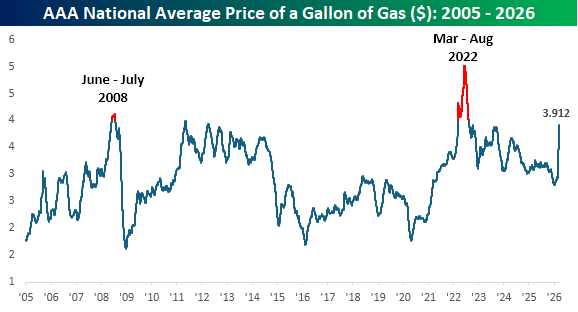

Memorial Day weekend and the beginning of the summer driving season is barely more than two months away. Were you planning a road trip? Well, maybe you’re starting to have second thoughts. Gas prices around the country have surged, and at times like this, the pictures from California always get the most attention. While we’ve seen pictures of even higher prices, the one below pretty much encapsulates what you’ll pay in the high gas price capital of the continental US. With prices reaching $6/gallon for the “cheap stuff”, shelling out $100 each time you go to get gas is now the norm. That’s before snacks, drinks, and the obligatory scratch-offs!

Obviously, California is not the norm. On a national basis, the average price of a gallon of gas, according to AAA, is still at $3.91 and will likely tip above $4 by early next week. Since the start of 2005, only two other periods have seen prices top $4. The first was from June to July of 2008, just as the Financial Crisis was accelerating. Then, in April 2022, after Russia invaded Ukraine, prices shot up to near $5 and stayed above $4 through early August.

The US consumer isn’t nearly as exposed to energy in terms of their total spending as they have been in decades past, but $4 still hurts. In 2008, the US economy experienced one of the deepest recessions in its history, and while the economy didn’t tip into a recession in 2022, GDP did turn negative, and stocks were in a bear market.

Besides filling up the tank, rising energy prices are showing up in other areas, notably airfares. So, if you thought the TSA security lines, which are growing longer by the day due to the shutdown, were a slap in the face, now you get to pay much more for the privilege of flying.

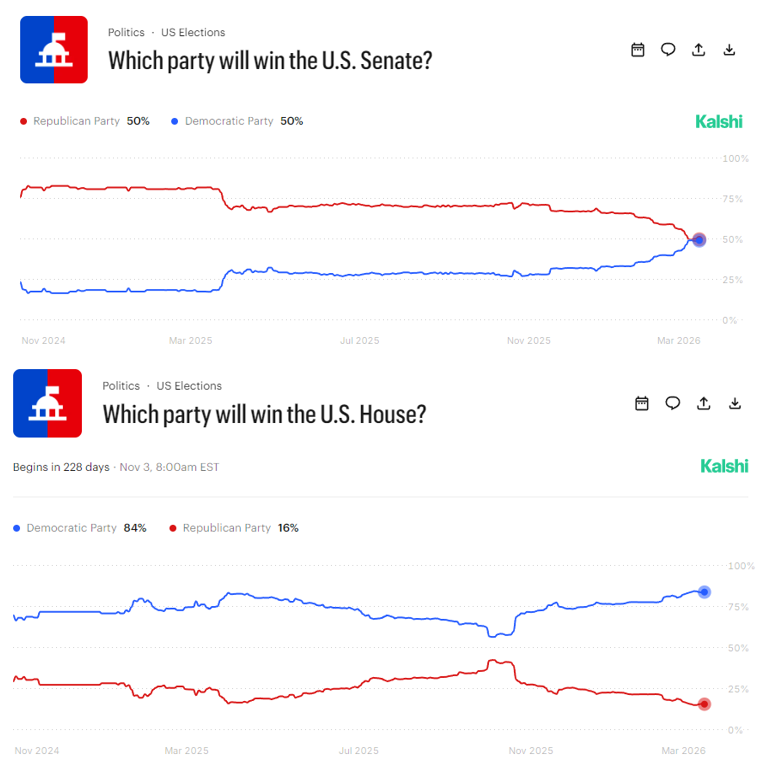

Between rising energy prices and a government shutdown that politicians have little urgency to end, if you’re up for re-election this year, good luck. This year, that spells trouble for Republicans. While it’s been widely assumed that Democrats would regain control of the House for some time now, in recent weeks, prediction markets have seen those odds increase to the highest levels since the last Presidential election (lower chart).

The picture in the Senate (top chart) is more interesting. While Republicans have largely been expected to maintain control after the midterms, in the last several days, prediction markets are now a toss-up for the Senate and moving in the wrong direction for the GOP. Whatever your political leanings, if you think that DC has been dysfunctional in terms of getting things done for the last year, just wait until next year if Democrats take control of both chambers of Congress. President Trump has shown an ability to pull rabbits out of his hat in the past, but as the midterms inch closer and gas prices sprint higher, the longer this trend persists, the bigger the bunny he’s going to need to pull out of his hat.

Like this analysis? Become a Bespoke Premium member today using our March Madness special! Click below for details on how to sign up:

The Triple Play Report: 3/17/26 – 3/19/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 3/20/26 – Stocks, A Port in the Storm

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The longest way must have its close – the gloomiest night will wear on to a morning.” ― Harriet Beecher Stowe

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A negative week is on pace to finish with a negative session as the S&P 500 looks to finish lower for the fourth week in a row and the sixth down week in the last seven. S&P 500 and Nasdaq futures are both down about 0.5% but off their overnight lows. Where we close, though, will depend almost entirely on the price of oil, which is down 1% to $95.15 per barrel. Treasury yields are modestly higher, with the 10-year yield just under 4.3%, while gold is up 1.3% and Bitcoin is holding above $70K.

In Asia overnight, most major equity indices in the region were lower, although the KOSPI rallied 0.3% to finish up 5.4% for the week. In Europe, we’re seeing more muted performance to close out the week. The STOXX 600 is down 0.1%, which would put it down more than 2% for the week, but Spain has bucked the negative trend, rallying 1% today and putting it into positive territory for the week.

There’s no economic or major earnings data on the calendar today, so geopolitical headlines will dictate the market’s performance.

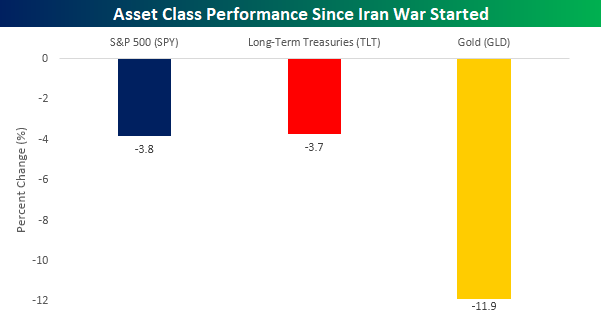

Heading into today’s session, the S&P 500 is down nearly 4% this month, which is unsurprising given the war in the Middle East. It’s only natural in times of geopolitical uncertainty for investors to move out of riskier assets into the safety of treasuries or even gold, the ultimate port in geopolitical storms. So, how are those two asset classes doing this month? Long-term treasuries, as proxied by the iShares 20+ Year Treasury ETF (TLT), are down 3.7%, which is basically in line with the S&P 500, while gold (GLD) is down more than triple either of the other two, with a decline of 11.9%. Just when you think you have it all figured out.

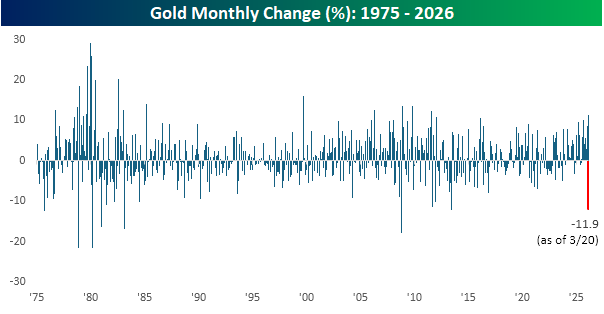

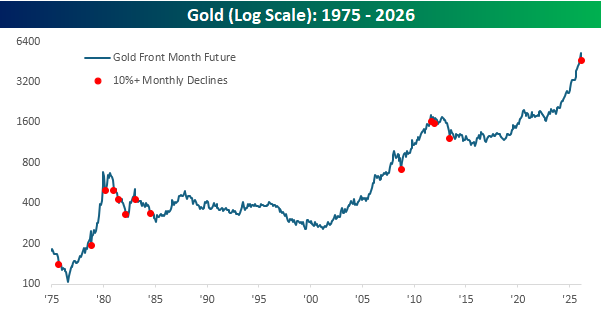

Gold’s double-digit percentage decline this month is on pace for the largest monthly decline in the commodity since June 2013 and, if it holds, would rank as the eighth largest one-month decline in gold since at least 1975. What’s even more interesting is that this month’s decline follows a double-digit percentage gain in February.

The chart below shows gold’s performance since 1975, and each red dot shows months when it declined 10% or more. Most of these declines occurred either early on or well into longer-term downtrends. There were some exceptions, though. The decline in October 2008 occurred right near the low for that period, and after the decline in November 1978, gold more than tripled over the next year.

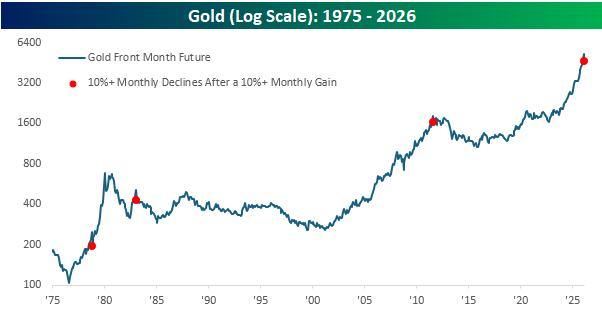

Looking at just the periods when gold declined by at least 10% following a double-digit percentage gain. Here, the sample size is much smaller, with just three other occurrences. The two most recent, in 2011 and 1983, were followed by years of weakness, while the one other occurrence in 1978 was the one period where gold quickly tripled.

The Closer – Mystery Charts, Sector Streaks, Flow of Funds – 3/19/26

Log-in here if you’re a member with access to the Closer.

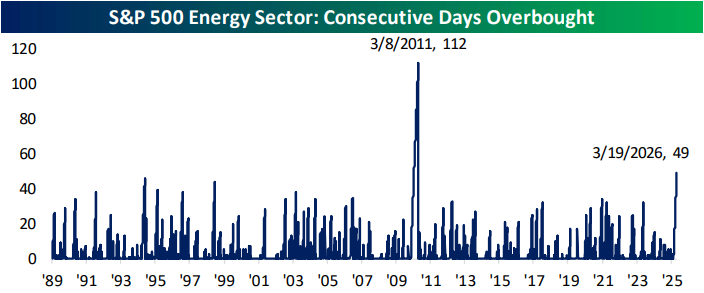

- The Energy sector has now traded in overbought territory for 49 consecutive trading days; the second longest streak of overbought readings on record.

- Intraday, crude oil futures continue to be driven by extreme lurches in positioning and weak liquidity.

- Data from the Federal Reserve’s Flow of Funds report showed that the corporate financing gap remains negative despite the boom in AI investment.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!