Daily Sector Snapshot — 12/2/25

Historic Health Care Relative Strength

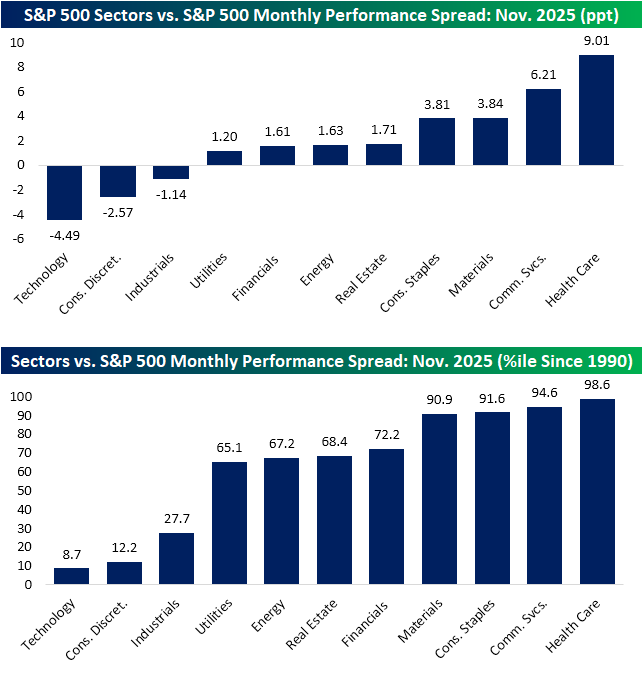

While stocks are getting off to a quiet start to December, the S&P 500 staged a solid recovery in the final week of November to manage a modest 13 bps gain on the month. Below, we show the performance spread of each S&P 500 sector versus the overall index in November. As shown, a majority of sectors actually outdid the index during the month with only Technology, Consumer Discretionary, and Industrials having underperformed. Tech in particular was a significant underperformer given it’s oversized weight; the monthly performance spread ranked in the bottom decile of all months since 1990. Conversely, Materials, Consumer Staples, Communication Services, and Health Care’s performance relative to the S&P 500 ranked in the top decile for all months since 1990. Health Care beat the S&P by nine percentage points in November, which was in the 98th decile for all months since 1990.

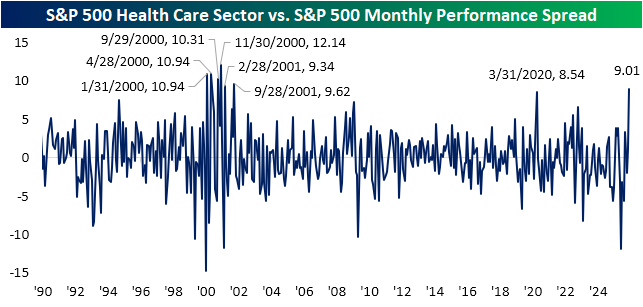

As shown below, it has been exceptionally uncommon for Health Care to outperform the broader market by such a wide degree. The last time the sector’s one-month outperformance was nearly as strong was in March 2020 when it outpaced the S&P 500 by a slightly smaller 8.54 percentage points. Prior to that, the only period with 9 percentage points or more like this November was a string of months in 2000 and 2001. Additionally, we would note that this latest big month for Health Care came only six months after one of its worst months on record versus the broad market; in May the sector fell 5.7% versus the S&P 500’s gain of 6.2%.

Health Care fell almost 1.5% yesterday to start off December and is again weak today. That was the sector’s first decline on the first trading day of a month since May. As shown below, that ends the longest streak of daily gains on the first day of a month since a seven month long streak ending in July 2017.

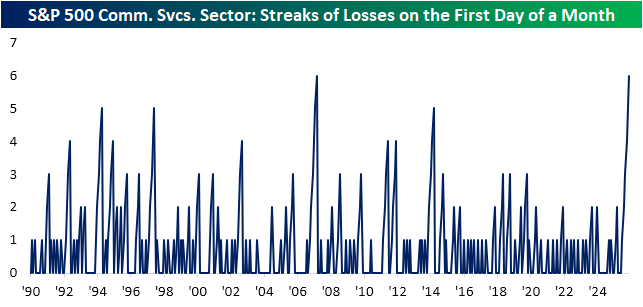

Switching over to a different sector, Communication Services also fell yesterday with an over 1% decline. That extends a losing streak of declines on the first day of a month to six months. Given the sector reshuffling in 2018, Communication Services has a different makeup today than it did in the years prior to the reshuffling. With that caveat in mind, there has only been one other period in which it fell on the first day of a month each month for half a year: October 2006 through March 2007.

Chart of the Day – Back End Loaded December

Bespoke’s Morning Lineup – 12/2/25 – Code Red

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Colonel Jessup! Did you order the Code Red?!” – Lieutenant Daniel Kaffee, A Few Good Men

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Silicon Valley is abuzz this morning following reports that OpenAI CEO Sam Altman declared a ‘code red’ on Monday as competition from Google and Anthropic intensifies. To fight the threats, initiatives like an advertising model, AI agents, and a personalized “Pulse” service for individual users have been temporarily put on hold. This latest story is just another example of how quickly the currents can change in the AI space, and that no one’s lead is safe.

Going back to the internet era, remember the ‘browser wars’? Google Chrome now dominates the browser space with about 70% market share, but you may find it hard to believe that it wasn’t released until 2008, more than eight years after the Internet bubble burst! There’s still a lot of runway left in the battle for AI supremacy.

US stocks started off December with broad-based declines as the S&P 500 fell 0.5%, but the Dow fared worse, falling nearly 1% as the Nasdaq outperformed, falling just 0.38 as Nvidia’s 2% gain propped that index up. The real area of weakness, though, was in the small-cap Russell 2000, which fell 1.25%. So much for the broadening trade.

Bulls started off the overnight session looking to put up a fight as S&P 500 futures rally 0.25% while the Nasdaq looks to open 0.38% higher. Crude oil is down fractionally as it wasn’t able to trade back above $60 in yesterday’s rally, while gold falls 1%, silver plunges 2%, and platinum falls even more (-2.38%). Crypto had a rough start to December, but has bounced back over 2% this morning, trading back above $87K.

Asian stocks saw mostly muted moves overnight. The one exception was South Korea, as the Kospi rallied nearly 2% following confirmation from US officials that tariffs on exports to the US would be cut to 15%. In Europe, the tone is also positive as the STOXX 600 bounces 0.3% with Germany rallying 0.60%.

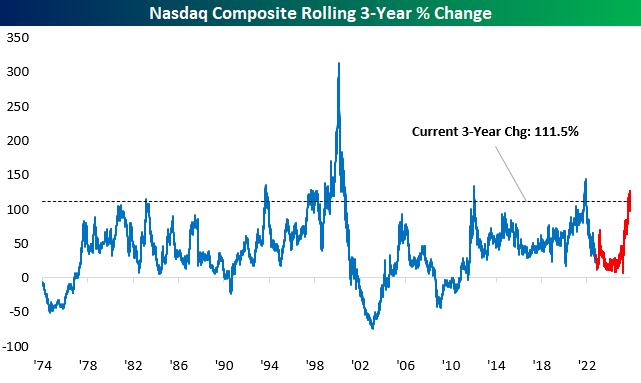

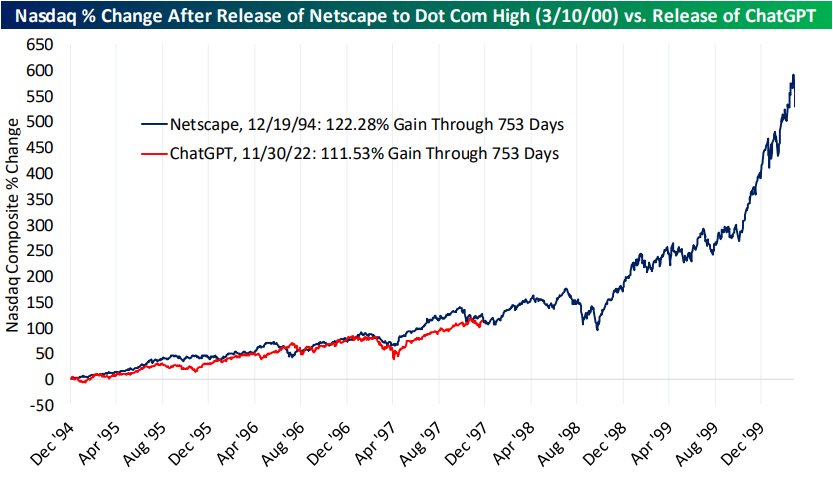

In last night’s Closer, we looked at the performance of the Nasdaq over the three years since the release of ChatGPT and compared that performance to other major tech releases of the last 50 years. Since the launch of ChatGPT in late 2022, the Nasdaq has rallied more than 100% ranking as the strongest three-year return since the period coming out of Covid and the massive tech investment to facilitate the work-from-home era. Outside of that period, the only other three-year period that was stronger was the one coming out of the Financial Crisis.

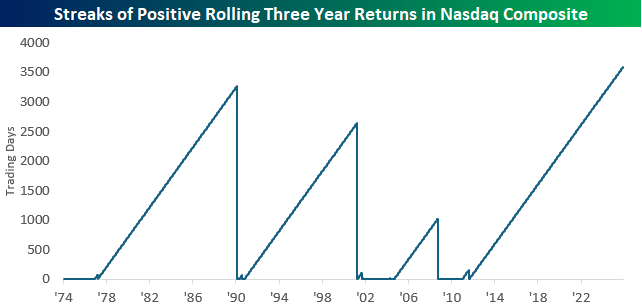

In addition to the massive rally of the last three years, what stood out in the chart was how long it has been since the Nasdaq had a negative rolling three-year return. The last time it was negative was in August 2011, just after S&P downgraded the AAA sovereign US credit rating more than 14 years ago! The chart below shows streaks of positive readings in the Nasdaq’s rolling three-year return, and at a length of 3,590 trading days, the current streak easily ranks as the longest. Besides that, three years ago the Nasdaq was under 11,500, or more than 50% below current levels. In other words, barring a large decline, the current streak of positive three-year returns isn’t going away soon.

The Closer – Year 3 of ChatGPT, KISS, PMIs – 12/1/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look into the first three years of ChatGPT (pages 1 and 2) followed by an update of our KISS basket (page 3). Next, dive into economic data in the form of PMIs and Mexico remittances (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 12/1/25

Q3 2025 Earnings Conference Call Recaps: Deere (DE)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Deere’s (DE) Q4 2025 earnings call.

![]()

Deere (DE) is the world’s leading maker of agricultural, construction, and forestry machinery, serving farmers, contractors, and governments with everything from high-horsepower tractors and combines to precision sprayers, excavators, skid steers, and forestry harvesters. While farming equipment may not be traditionally associated with complex digital systems, DE is standing out with new products that incorporate automation, computer vision, satellite connectivity, and autonomy, giving investors a view into the digitization of global agriculture and infrastructure. The company’s platform, the John Deere Operations Center, now covers more than 500 million engaged acres. This quarter highlighted a tough Large Ag market, but better results elsewhere as tariffs surged to a $1.2B pretax headwind for FY26 and farm fundamentals stayed soft due to high global crop stocks and elevated input costs. Demand for biofuels was a bright spot, with US corn exports projected to hit all-time highs, and soybean crush volume set for a record year. Technology adoption grew nicely: See & Spray (Deere’s computer-vision spraying system that uses cameras and AI to detect weeds in real time and apply herbicide only where needed) covered 5M+ acres with ~50% herbicide savings, and autonomous tillage expanded toward commercial rollout. Construction markets improved with data center builds, infrastructure spending, and a 25% increase in earthmoving order books. As a result of a weaker Large Ag market, DE shares declined 5.8% on 11/26…

Continue reading our Conference Call Recap for DE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Market Calendar — December 2025

Please click the image below to view our December 2025 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.

Note: Due to the government shutdown, scheduled release dates are subject to change. Click here to view Bespoke’s premium membership options.

Chart of the Day: Welcome December

Bespoke’s Morning Lineup – 12/1/25 – Back to Gravity

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Many people are busy trying to find better ways of doing things that should not have to be done at all. There is no progress in merely finding a better way to do a useless thing.” – Henry Ford

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a zero-gravity rally on Friday that pushed the S&P 500 into positive territory for the month and extended the S&P 500’s monthly winning streak to seven, equities are rediscovering gravity to start December as futures on the major averages all trade lower. The Nasdaq is poised to open down nearly 1% while the S&P 500 faces a 0.7% decline. Even with equities falling, treasury yields are also higher as the 10-year ticks up 3 bps to 4.05%. Crude oil is up just over 1% as OPEC+ announced plans to maintain output levels rather than raise them, and gold is back near $4,300, gaining about 0.8%. The big loser on the day, though, is Bitcoin. With a decline of over 6%, the largest crypto is on pace for its worst day since March, and part of the weakness could be related to reports that Strategy (MSTR) could potentially be forced to sell some of its holdings to fund its dividend.

The weakness started in Asia as the Nikkei fell close to 2% as JGB yields continue hitting levels not seen since before the Financial Crisis, as expectations for a rate hike later this month solidify. In China, stocks went the other way with the Shanghai Composite rallying 0.7%, even as November Manufacturing and Non-Manufacturing PMIs remained in contraction territory.

In Europe, the losses have been more uniform as the STOXX 600 falls 0.5% as Manufacturing PMIs for the economic bloc and individual countries missed expectations. The biggest loser on a country basis is Germany, as the DAX declines more than 1.5% as defense contractors have been especially weak on reports of progress in the Russia-Ukraine war talks.

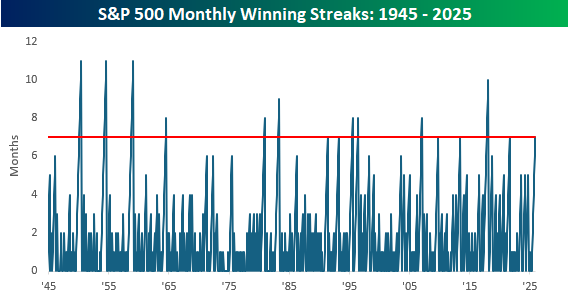

As mentioned above, the S&P 500’s winning streak extended to seven in November, and that’s the longest streak of gains for the index in more than four years (August 2021). Since the end of WWII, there have been 15 other seven-month winning streaks, with the longest being eleven. Believe it or not, that happened three times, all of which were all in the 1950s. So, while history always talks about the roaring twenties, don’t forget about the fantastic fifties.

Outside of those three eleven-month winning streaks in the 1950s, the only other streak that extended into the double-digits was the 10-month streak that kicked off President Trump’s first term in office, ending in January 2018 (seventh month was October 2017). Getting back to the most recent streak, the seven months ending in August 2021 were followed by a sharp decline of 4.8% the following month, and weak returns thereafter.

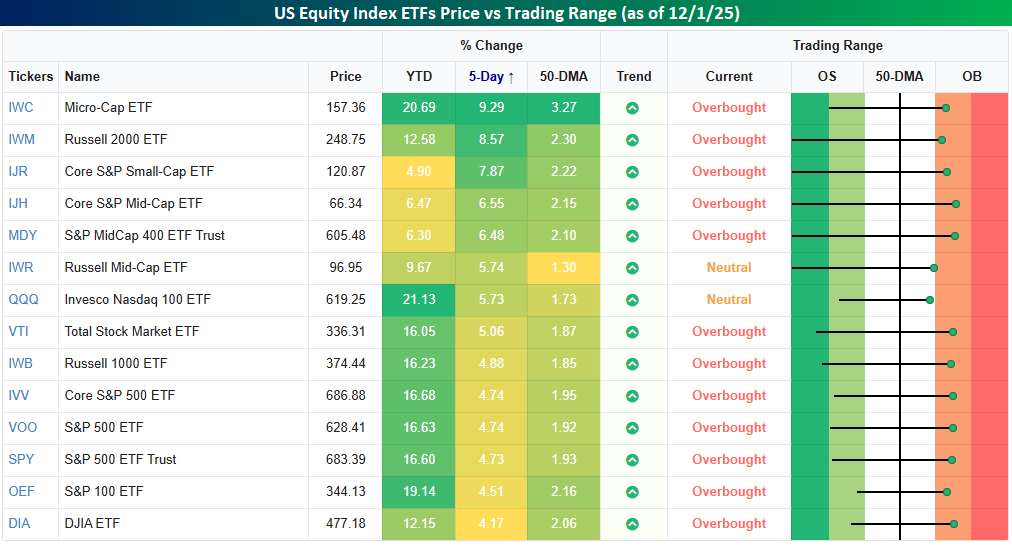

Last week, right before Thanksgiving, we pointed out that the S&P 500 and other major US equity indices had quickly gone from oversold to neutral. In the two trading days since then, the rally kicked into another gear with little selling resistance (as evidenced by Friday’s rally), and all but two of the major equity index ETFs in our Trend Analyzer snapshot have moved into overbought territory. The only exceptions are the Russell Mic-Cap ETF (IWR) and the Nasdaq 100 (QQQ), and while they may not be overbought, they still rallied over 5% in the five trading days through last Friday’s close (from close on 11/20).

Of all the ETFs shown, every one of them was up at least 4% in the trailing five trading days. While large-cap ETFs lagged with gains of less than 5%, small caps had a day in the sun with the Russell Micro Cap ETF (IWC) surging 9% while the Russell 2000 ETF rallied over 8.5%. While usually not the case in recent months, this rally has been one where big gains came in small packages.