Chart of the Day – Conflicting Signals

Bespoke’s Morning Lineup – 12/16/25 – Honey, I Shrunk the Range

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The more wonderful the means of communication, the more trivial, tawdry, or depressing its contents seemed to be.” – Arthur C. Clarke

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Ahead of a busy morning for economic data, US futures are lower but well off their lows of the overnight session. S&P 500 futures are down just 10 basis points, while the Nasdaq is down 16. Treasury yields are down nearly 2 bps to 4.165%, and crude oil is down over 1.6% and on pace for another closing low. Gold prices are fractionally lower but still trading over $4,300 per ounce. In the crypto space, Bitcoin is up 1.5% but still only trading at $87,100.

As mentioned above, it’s a busy morning for economic data with Non-Farm Payrolls and Retail Sales hitting the tape at 8:30. It’s good to get some economic data again, but be forewarned that these reports could be noisy.

Most Asian markets were down at least 1% overnight, with South Korea leading the losses and falling over 2% as memory stocks were weak. European stocks are also weak this morning, but the losses are much more contained than what Asia saw overnight.

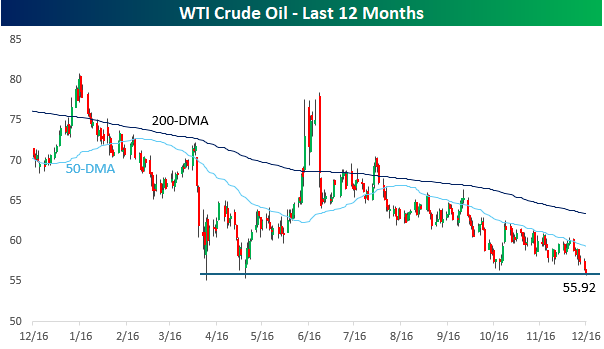

As mentioned above, crude oil prices are down over 1% this morning, and while not quite at 52-week lows on an intraday basis, if these losses hold, it will mark a new 52-week closing low. After briefly trading over $80 per barrel in January, prices have been in a steady decline almost all year. The only exception was back in June when prices briefly spiked after Israel launched airstrikes on Iranian nuclear facilities.

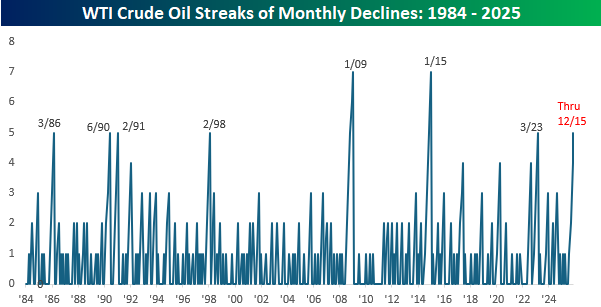

With this morning’s declines, crude oil prices are down close to 5% for the month, and if these losses hold throughout the next two weeks, it will be the fifth straight month of declines for crude oil. That would be tied for the longest streak since January 2015 (7 months). Since 1984, there have only been two longer streaks (7 months each) and five others that lasted five months. What would also make this current streak noteworthy if the losses hold is that it would also be the fifth month in a row that crude oil declines 2% or more. Since 1984, there have only been two streaks that lasted longer and one that lasted as long.

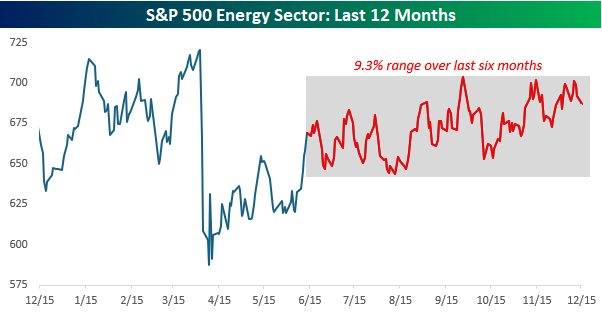

Even though crude oil is sinking towards new 52-week lows, the S&P 500 Energy sector has been holding up relatively well. While it’s underperforming the S&P 500 on a YTD basis, it’s still much closer to 52-week highs than 52-week lows. That may be partly due to the strength of natural gas, although even that commodity has weakened in the last few days, falling from $5.25 MMBtu on 12/5, down to $3.94 this morning.

The Closer – Cuts vs. Rates, Fedspeak, Energy Prices – 12/15/25

Log-in here if you’re a member with access to the Closer.

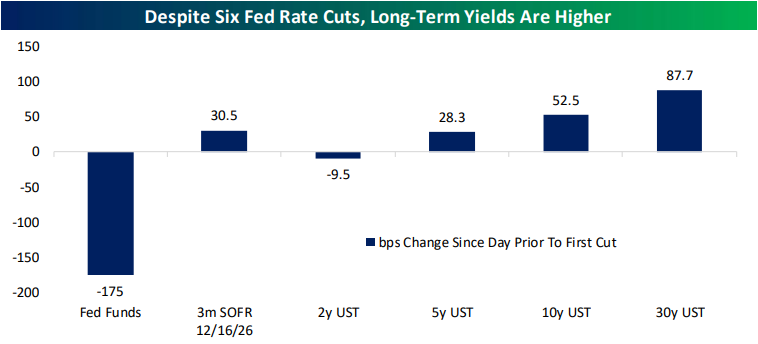

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight’s report with a dive into how markets have responded to rate cuts (pages 1 and 2). We then review the latest Fedspeak and corporate news (page 3) before finishing with a checkup on energy prices (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: RH (RH)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers RH’s (RH) Q3 2025 earnings call.

![]()

RH (RH) is a luxury lifestyle brand curating high-end home furnishings, lighting, and textiles through immersive physical “Galleries” rather than traditional stores. Serving affluent consumers and interior designers, it integrates hospitality venues like its restaurants to drive traffic and offset rent, offering insights into the luxury housing market and the “experience economy.” In Q3, RH delivered 9% revenue growth despite battling the “worst housing market in 50 years” and chaotic tariff fluctuations that pressured operating margins to 11.6%. CEO Gary Friedman emphasized the brand’s “long game,” highlighting the strong initial performance of RH Paris and a massive upcoming “Classic” product launch expected to drive multi-billion dollar growth. While navigating supply chain volatility, including 16 tariff announcements in 10 months, management continues to aggressively invest in international expansion (Milan, London) and RH’s own design ecosystem, viewing current macro headwinds as a rare opportunity to gain market share while competitors retreat. RH beat revenue estimates but missed the mark on EPS, sending shares 8% higher on 12/12…

Continue reading our Conference Call Recap for RH by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Daily Sector Snapshot — 12/15/25

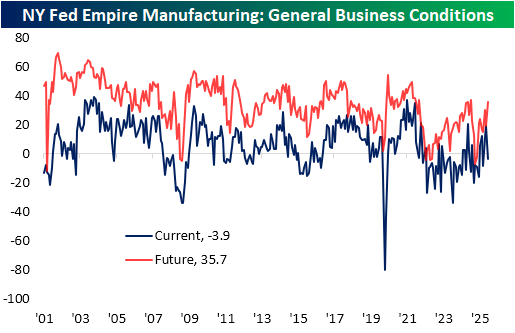

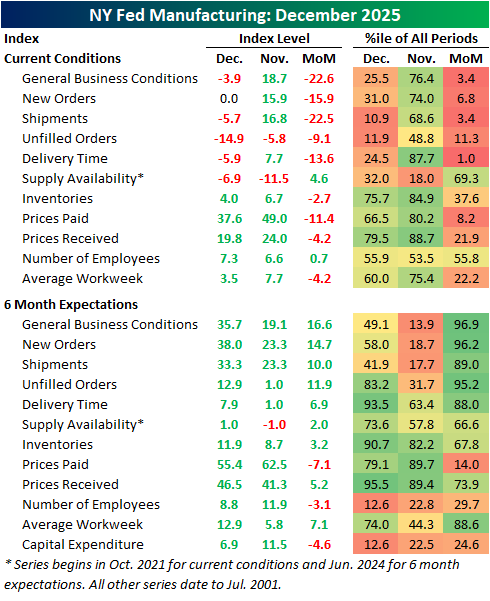

Weak NY Manufacturing

It was a light morning for economic data to start the week. One of the two releases was the New York Fed’s monthly Empire Manufacturing Survey. After coming in at 18.7 in November, the second highest reading since April 2022, the index pulled back sharply to contractionary territory in December. Albeit back into contraction, there was a lower reading as recently as September. Countering that negative outlook for the region’s manufacturers was solid six month expectations. As shown below (red line), expectations continued to climb in December with the 16.6 point month-over-month jump, ranking in the 96th percentile of all monthly moves on record. Additionally, that is at the high end of the past few years’ range and nearly back to the historical median.

Looking under the hood, the weakness in the headline index comes on broad declines across most categories for current conditions. In fact, of the eleven indices including general business conditions, only two rose month over month. Further, eight of the eleven experienced bottom quartile monthly declines, which has resulted in roughly half of categories sitting in contraction.

Again, expectations were much better. Not a single category fell into contraction in December. In fact, the lone category formerly in contraction, Supply Availability, moved back into expansion. As all expectation readings are now expansion, six of the eleven saw top quintile monthly gains. That includes big moves higher from ever-important categories like new orders, shipments, and unfilled orders. In other words, the December survey indicates that the region’s businesses observed weakness, but don’t see that weakness to be lasting.

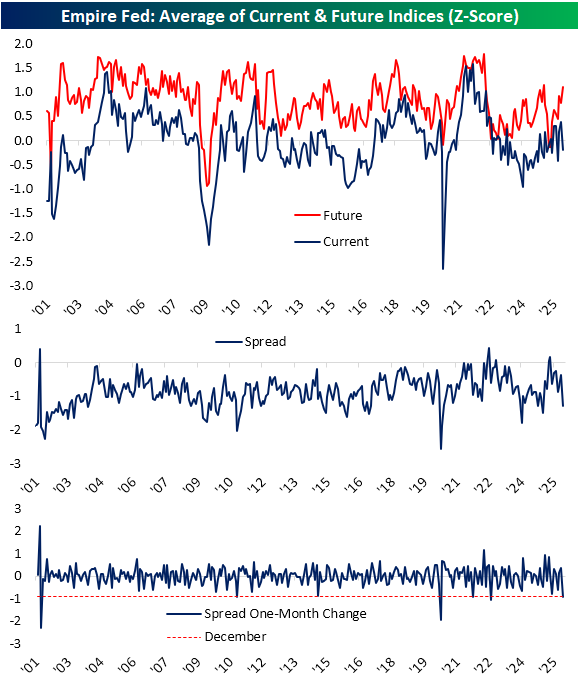

To help quantify just how large of a disconnect there has been between current and future indices, below we show averages of those categories going back through the history of the survey. As shown, expectations generally hold a positive bias and it has been rare for current condition indices in aggregate to come in stronger than future expectations. That most recently happened this past May, and in 2022 before that, but as of December, things have shifted the opposite direction. The spread between current and future categories is now at the widest level since January. Compared to one month ago, that spread fell 0.93 standard deviations, which ranks in the first percentile of all monthly moves over the survey’s history. That means it was a historic month for shifts of positive expectations and negative current conditions.

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

Q4 2025 Earnings Conference Call Recaps: Costco (COST)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Costco’s (COST) Q4 2025 earnings call.

![]()

Costco (COST) operates a global chain of membership-only warehouses, serving over 81 million households with high-quality, low-priced items ranging from fresh food to clothing to fuel. Costco delivered strong Q1 results for the quarter that ended November 23, with $65.98 billion in net sales (+8.2%) and a 20.5% surge in digital sales, led by app enhancements and AI integration in pharmacy and logistics. Management addressed macro concerns by detailing strategies to mitigate potential tariffs, including sourcing adjustments and inventory optimization. While overall inflation remained stable, specific commodity costs like beef rose. Interestingly, a slight dip in global renewal rates to 89.7% was attributed to an influx of younger, digital-first members. The company reaffirmed plans for 30+ annual openings, including creative mixed-use sites, and highlighted record-breaking holiday demand, selling 4.5 million pies in the days leading up to Thanksgiving. Shares were flat on Friday, 12/12, despite better-than-expected results…

Continue reading our Conference Call Recap for COST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: AI Inning + More Intraday Blues

Bespoke’s Morning Lineup – 12/15/25 – Midpoint

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life’s under no obligation to give us what we expect.”- Margaret Mitchell, Gone With the Wind

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a rough end to last week, bulls are shaking the dirt off their shoulders and looking to make a stand as we head into the final half of the month. Both the S&P 500 and Nasdaq are down fractionally so far this month, but with the seasonally strong second half of the month now here, will the bulls show up?

So far, they’re coming out on the offensive. Futures on all three of the major averages are higher by roughly 0.5%. The 10-year yield is moving lower and picking up in pace to the downside following a weaker-than-expected Empire Manufacturing report. Crude oil is fractionally higher, while gold and Bitcoin move higher.

Asian stocks started the week with broad-based losses. The South Korean Kospi led the losses with a decline of 1.8%, but both the Nikkei and Hang Seng finished down 1.3%. China also finished lower, but the losses were more contained at 0.6%. Besides follow-through from Friday’s losses in the US, the declines in the region also followed weak economic data out of China, where Industrial Production (4.8% y/y) and Retail Sales (1.3% y/y) both missed expectations.

Unlike Asia, European stocks are higher across the board with the STOXX 600 trading up 0.8%, with the UK, France, Italy, and Spain all up over 1% while Germany lags as peace talks in Ukraine continue to drag on.

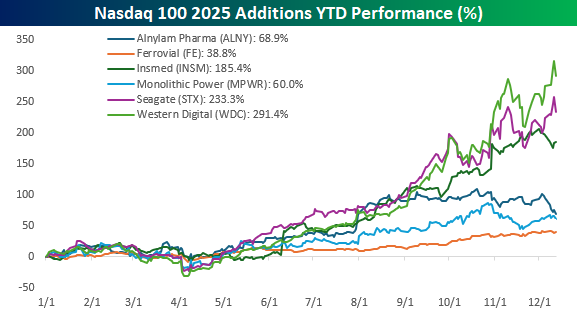

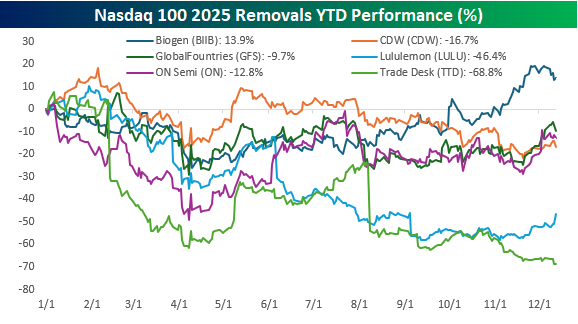

On Friday, Nasdaq announced the annual changes to the Nasdaq 100, and for this year’s shakeup, six stocks will be added and six removed. The new class of 2025 includes Alnylam Pharmaceuticals (ALNY), Ferrovial (FER), Insmed (INSM), Monolithic Power Systems (MPWR), Seagate Technology (STX), and Western Digital (WDC). The six stocks being removed to make room are Biogen (BIIB), CDW (CDW), GlobalFoundries (GFS), Lululemon Athletica (LULU), ON Semiconductor (ON), and The Trade Desk (TTD).

The two charts below show the performance of the six stocks being added and removed from the Nasdaq 100 on a YTD basis, and judging by their performance, one factor that appears to be part of the criteria is popularity. All six of the stocks being added this year have positive returns since the start of the year, and the median gain is 127.2%. Leading the way higher, Western Digital (WDC) and Seagate Technology (STX) have both rallied more than 200%. Even the worst performer of those stocks being added – Ferrovial (FE) – was 38.8%.

Turning to the six stocks being removed, they haven’t exactly shone this year. Five out of six of the stocks are down on the year, and the only winner – Biogen (BIIB) – is up only 13.9%. All totaled, the median performance of the six stocks is a decline of 14.8%.

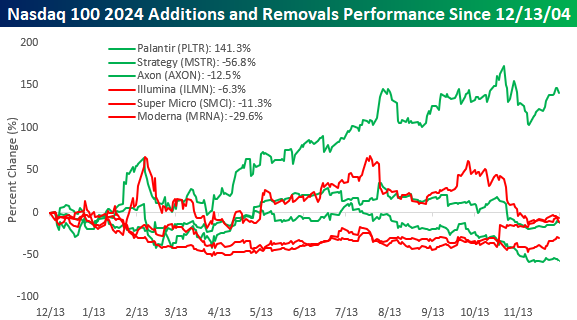

While six stocks are being added and removed this year, last year, there were only three. With one exception, the performance of both the stocks being added and removed from the Nasdaq 100 wasn’t particularly good. As shown in the chart below, shares of Palantir (PLTR) have rallied 141.3% since last year’s announcement that it was being added to the Nasdaq 100, but shares of Strategy (MSTR) and Axon (AXON) are both lower. Likewise, all three of the stocks removed last year are also lower, with declines in the range of 6.3% for Illumina (ILMN) to 29.6% for Moderna (MRNA).

Finally, since we’re talking about the Nasdaq 100, it’s worth pointing out that the index closed below its 50-day moving average again to close out last week as the latest rally off the November lows failed to make a higher high. With megacaps like Nvidia (NVDA), Microsoft (MSFT), and Oracle (ORCL) faltering recently, it’s showing up in the performance of indices they dominate, like the Nasdaq 100.

Brunch Reads – 12/14/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

The Quantum Question: On December 14, 1900, German physicist Max Planck presented a paper to the German Physical Society in Berlin that solved how energy is emitted by a “blackbody,” an idealized object that absorbs and radiates energy perfectly. Physicists had been studying how hot objects glow, like a piece of metal heated in a fire or the filament inside a light bulb. According to the physics of the day, the math predicted that as objects got hotter, they should release infinite energy at certain wavelengths. That clearly didn’t happen in the real world, so something in the theory was broken.

Planck’s solution suggested that energy doesn’t flow out smoothly, like water from a faucet. Instead, it comes out in tiny, fixed-size packets. He called these packets “quanta.” The key idea was simple: energy could only be released in certain amounts, not just any amount continuously.

This small change made the math work and matched what experiments actually showed. Planck even introduced a new number to describe how big these energy packets are, now known as Planck’s constant. At the time, it didn’t seem especially important. Even Planck himself thought of it as a mathematical workaround, not a deep truth about nature. But that idea turned out to be a big deal. If energy comes in packets, then the universe isn’t perfectly smooth at its smallest levels. That insight became the foundation of quantum physics. Over the next few decades, other scientists built on Planck’s work to explain atoms, light, electricity, and eventually technologies like semiconductors, lasers, and computers.

Markets & Investing

401(k)s Are Minting a Generation of ‘Moderate Millionaires’ (WSJ)

Three straight years of market gains have pushed a record number of retirement accounts past the million-dollar mark. While these savers hit a massive financial goal, many find that seven figures no longer buys the lavish lifestyle they once imagined. It seems the new face of being a millionaire looks less like owning a yacht and more like hunting for grocery deals. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.