Daily Sector Snapshot — 5/16/23

Bespoke Stock Scores — 5/16/23

Homebuilders Sentiment and Stocks Still On the Rise

As we noted last week on the release of the latest mortgage purchase data, housing activity appears to have finally stabilized after plummeting earlier in the tightening cycle. That improvement in housing markets is flowing through to builders as this morning’s release of homebuilder sentiment from the NAHB rose to 50 versus the expectation of it remaining unchanged at 45. While the index still has a long way to go to get back to pre-pandemic levels, let alone the record highs from the first two years of the pandemic, in May it hit the highest level since last July.

The higher reading in the headline index was a result of improvements across the board, including increases in present and future sales and traffic. As for regional sentiment, homebuilders have gotten more optimistic across most of the country. Everywhere save for the Northeast have seen steady improvements to homebuilder sentiment over the past several months. As for the Northeast, that is not to say sentiment has not improved. The reading has rebounded off of the worst levels but remains below the recent highs of 46 from February and March.

Homebuilder stocks continue to be even more impressive. Proxied by the iShares Home Construction ETF (ITB), homebuilders have been trading in a steady and uninterrupted uptrend. In fact, the ETF has been overbought every day for a month now.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.

Chart of the Day: No Love for Dividend Stocks

Fixed Income Weekly: 5/16/23

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit each week. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report, we break down the differences in short-term pricing of interest rates in the Fed Funds and US Treasury markets.

Our Fixed Income Weekly helps investors stay on top of fixed-income markets and gain new perspectives on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

B.I.G. Tips – Retail Sales – Bad Breadth

Bespoke’s Morning Lineup – 5/16/23 – Weak Retail Sales

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Try to decide how good your hand is at a given moment. Nothing else matters. Nothing.” – Doyle Brunson

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

There’s a modest amount of risk-off mentality in the markets this morning, and it started last night with weaker-than-expected economic data in China followed by a weaker-than-expected report on economic sentiment in Germany from ZEW. This morning in the US, Home Depot (HD) is trading more than 2% lower after reporting a sales miss and lowering guidance. That weak report didn’t bode well for April Retail Sales at 8:30 where economists are forecasting a m/m increase of 0.4%. Looking ahead, we’ll get Industrial Production and Capacity Utilization at 9:15 followed by Business Inventories and Homebuilder sentiment at 10 AM.

The release of April Retail Sales was mixed. At the headline level, sales increased just 0.4% compared to forecasts for an increase of 0.8%. Stripping out autos, though, the report was right in line with forecasts (0.4%), and ex-autos and gas, sales actually increased at triple the rate of expectations (0.6% vs 0.2%). In addition, last month’s report was revised to a worse than initially reported number, so there was something for everyone in this report.

After slicing right through the psychologically critical threshold back in September, the yield on the 2-year US Treasury found support multiple times at the 4% level. After the last bounce in early February, the yield looked as though it was going to launch into a new higher range above 5%, and being short bonds looked like a winning hand.

Within a month, though, the failures of SVB Financial, Signature Bank, and later, First Republic caused a rush to safety, and yields quickly erased all of the February spike. Since then, the 4% level has been acting more like resistance (or a magnet) as the yield hasn’t been able to convincingly get back above the 4% level and is trading right around there this morning. With the 50-day moving average (DMA) continuing to roll over and the 200-DMA starting to follow suit, the 2-year yield runs the risk of breaking down below 4% turning what was the nuts into a bad beat.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Dow Down for Five, Fedspeak, Household Debt & Credit, Positioning – 5/15/23

Log-in here if you’re a member with access to the Closer.

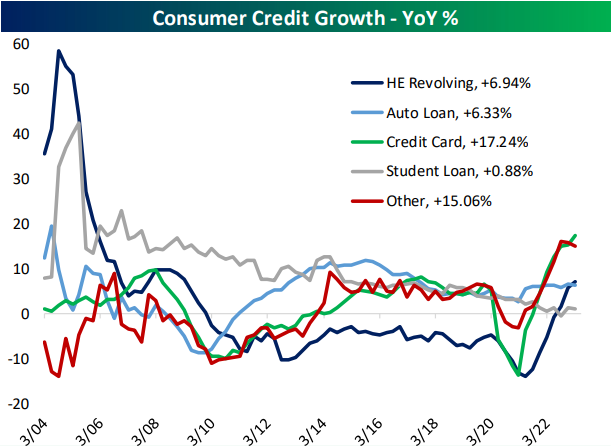

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the Dow snapping its losing streak (page 1) followed by an update on today’s Fedspeak (page 2). We then dive into today’s consumer credit numbers (pages 3 -5) before finishing with updates of this week’s Treasury auctions (page 6) and the latest positioning data (pages 7-9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 5/15/23

NY Fed Plummets

The economic calendar was light this morning with the Empire Fed Manufacturing survey the only release of note. Whereas last month saw a solid reading of 10.8 implying expansionary activity in the NY Fed’s region, expectations were set low as the index was forecasted to fall down to a contractionary reading of -3.9. Instead, the index plummeted all the way down to -31.8, the lowest since January when the index reached a slightly worse -32.9. Additionally, the monthly decline in the headline number ranks as the second largest drop on record behind April 2020. Overall, the index has been quite volatile in recent months bouncing from historically contractionary readings to modest contraction or even growth.

As shown below, the month-over-month declines across many categories were nothing short of historic in May. For example, New Orders saw an astounding 53.1 point decline (just short of a record decline similar to the headline index). Shipments wasn’t much better with a 40-point decline. However, expectations for both of those categories rebounded with New Orders being a particularly big uptick, ranking in the upper decile of all month-over-month increases. That being said, the indices remain in the bottom deciles of their historical ranges while all other categories (like unfilled orders and inventories) saw declines in expectations alongside declines in current condition indices. Again, while recent months have seen some volatility in these survey results, the findings would imply responding firms have observed a significant slowdown in their businesses.

One silver lining relative to post-pandemic trends is that the report has shown a complete reversal in readings on prices and delivery times. As shown in the first chart below, the average of the two current conditions indices has been rolling over and is now basically right in line with the historical median. Balancing out the more normalized level in supply chain readings, firms also appear to be reporting massive pullbacks in hiring capital expenditures, and plans for tech spending. During the past two recessions, this average has turned negative, and at the moment, it is only barely positive at 3.43.

Have you tried Bespoke All Access yet?

Bespoke’s All Access research package is quick-hitting, actionable, and easily digestible. Bespoke’s unique data points and analysis help investors better visualize underlying market trends to ultimately make more informed investment decisions.

Our daily research consists of a pre-market note, a post-market note, and our Chart of the Day. These three daily reports are supplemented with additional research pieces covering ETFs and asset allocation trends, global macro analysis, earnings and conference call analysis, market breadth and internals, economic indicator databases, growth and dividend income stock baskets, and unique interactive trading tools.

Click here to sign up for a one-month trial to Bespoke All Access, or you can read even more about Bespoke All Access here.