Daily Sector Snapshot — 1/20/26

Q4 2025 Earnings Conference Call Recaps: Fastenal (FAST)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Fastenal’s (FAST) Q4 2025 earnings call.

![]()

Fastenal (FAST) is a maker of industrial and construction supplies, specializing in fasteners, safety gear, and MRO (Maintenance, Repair, and Operations) products. Beyond simple retail, the company is a supply chain powerhouse that embeds itself into customer workflows through Onsite locations (miniature warehouses inside client facilities) and FMI (Fastenal Managed Inventory) technology, an automated network of industrial vending machines and smart bins. FAST serves heavy manufacturing and construction clients, governments, and data centers. Fastenal capped a recovery year with a strong Q4, posting $2.03 billion in sales (up 11%) and record annual revenue of $8.2 billion. Despite a “sideways” industrial economy and mixed signals from the PMI, the company achieved market share gains by pivoting toward large-account “ultra-high spend” sites ($50K+ monthly), which now account for over half of revenue. A key highlight was the acceleration of FAST’s digital moat: FMI and eBusiness now represent 62.1% of sales, creating sticky relationships that outperformed the broader market. Looking toward 2026, FAST anticipates continued double-digit growth, supported by a fresh leadership transition with Jeff Watts named as the next CEO. FAST reported a revenue beat on in-line EPS, resulting in a loss as much as 5% for the stock on 1/20…

Continue reading our Conference Call Recap for FAST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

First Year of Trump’s Second Term in the Books

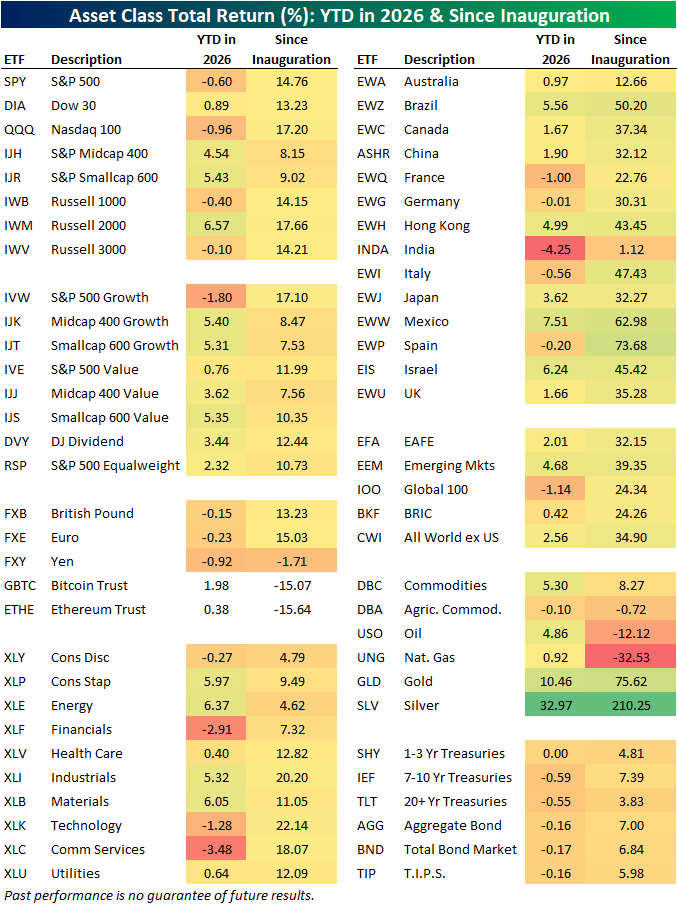

It has been one year since President Trump was sworn in for a second time. Looking back on the past year using our ETF asset class matrix below, the single best performing assets were precious metals with gold (GLD) up 75.6% and silver (SLV) providing an astounding 210.6% total return.

While their gains didn’t quite stack up to gold and silver, equities also had a respectable year. The major US indices all provided a total return ranging from high-single digits to the mid-teens with oversized gains from the small-cap Russell 2,000, large cap growth (IVW), and the Nasdaq 100 (QQQ).

On a sector level, traditionally cyclical areas were mixed as the likes of Energy (XLE), Consumer Discretionary (XLY), and Financials (XLF) underperformed with mid-single digit gains whereas Tech (XLK) and Industrials (XLI) both provided total returns surpassing 20%. Closing in on one month into the new year, there has been some rotation as XLE has rebounded while XLK is in the red.

While US equities did well in Trump’s first year, it was internationals that were the stars in the equity space. Of the fourteen country ETFs shown in the matrix below, only two underperformed the S&P 500 (SPY). Those were Australia (EWA) with a marginal 2 percentage points of underperformance and more meaningful lagging performance from India (INDA).

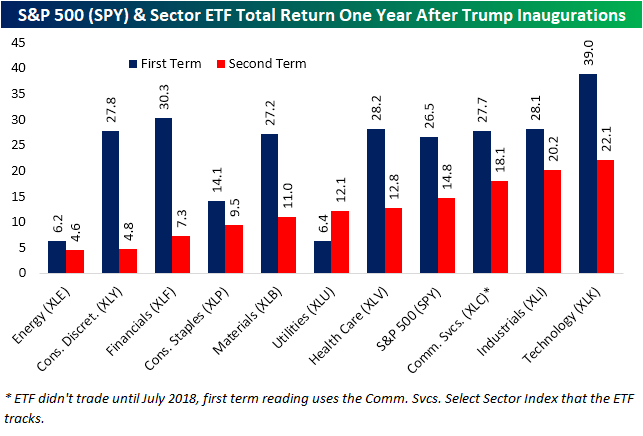

Looking back to the first time Trump was sworn in back in 2017, the year following saw an even larger gain for the S&P 500 ETF (SPY) as it offered a 26.5% return in Trump’s first year in the Presidency. For this second term, SPY is again higher but by about ten percentage points less. Taking it a step down, the only sector outperforming during this second term versus the first is Utilities (XLU), which is up 12.1% since last January; that compares to a 6.4% gain after the 2017 inauguration. Finally, we would note that whereas in 2017 there was a significant cluster (seven of the eleven sectors) with similarly-sized gains between 25% and 30%, this time there is a more gradual increase across sectors. With that said, Tech was the top performing sector in both periods, and the margin was much larger during the first term.

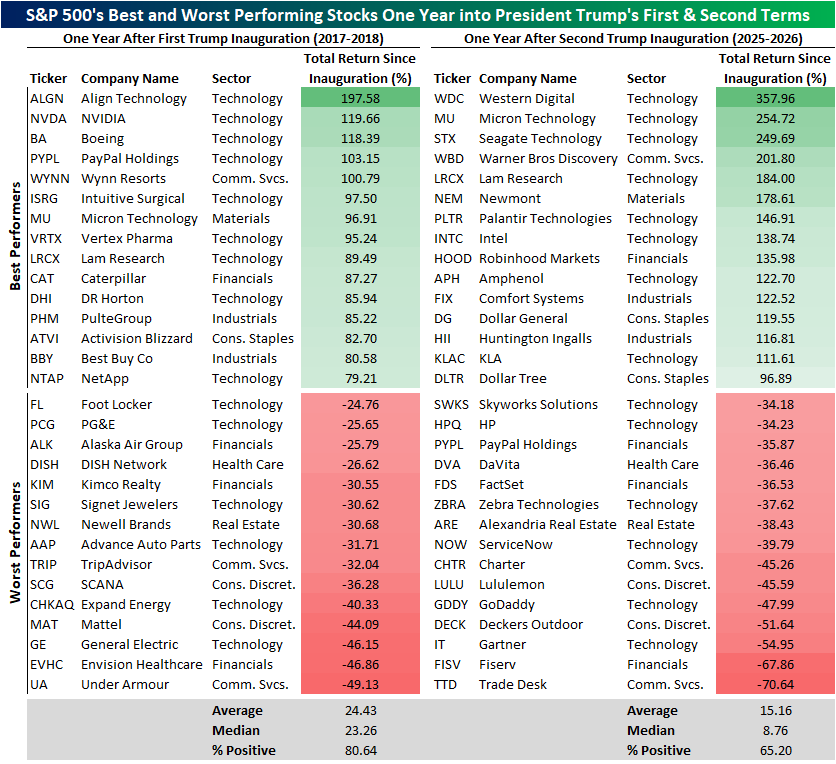

Below we include a look at the S&P 500’s individual best and worst stocks of the first year of Trump’s first and second terms. As shown, this second term has seen larger losses and larger gains for the best and worst stocks. In fact, of the 15 best performers of the past year, 14 more than doubled compared to only five from 2017 to 2018. Additionally, four stocks were more than cut in half this time around. Only Under Armor (UA) came close to that with a 49% loss after Trump’s first inauguration. Despite these big moves at the tail ends of the distribution, on the whole of S&P 500 members, average gains are smaller in the past year than they were from January 2017 to January 2018. Additionally, fewer stocks have risen (80% versus 65%).

Q4 2025 Earnings Conference Call Recaps: D.R. Horton (DHI)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers D.R. Horton’s (DHI) Q1 2026 earnings call.

![]()

D.R. Horton (DHI) is the largest homebuilder in the United States by volume. The company designs and constructs high-quality, attainable homes primarily for entry-level and first-time buyers, who represent over 60% of its business. Its scale spans 126 markets across 36 states, providing insight into the health of the American consumer and the broader housing market. Management reported a disciplined start to 2026, beating revenue expectations with $6.9 billion despite “cautious consumer sentiment.” To combat affordability headwinds, DHI aggressively utilized mortgage rate buy-downs, maintaining a floor as low as 3.99% for some buyers. This strategy successfully drove a 3% increase in net sales orders. A key focus this quarter was “rightsizing” product; the builder is transitioning to smaller floor plans and higher-density communities to lower monthly payments. Despite broader economic uncertainty, the company reiterated its guidance to close up to 88,000 homes this year. On better-than-expected results, DHI shares opened 2.9% lower on 1/20, though erased most of the losses intraday…

Continue reading our Conference Call Recap for DHI by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

B.I.G. Tips – A Break From the Banks

Chart of the Day: Lower Opens After Long Weekends

Bespoke’s Morning Lineup – 1/20/26 – One Year

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember, your mind is like a parachute: If it isn’t open, it doesn’t work. So keep an open mind!” – Buzz Aldrin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

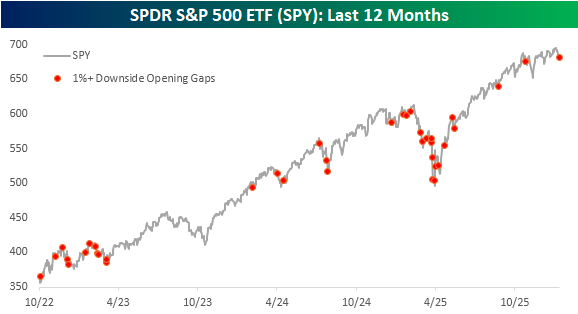

If this is the price we pay for a three-day weekend, maybe we should have kept the market open. It’s looking like a terrible Tuesday for US equities as the S&P 500 is poised to open down 1.4% while the Nasdaq is indicated 1.7% lower. Over the weekend, President Trump escalated his rhetoric towards Greenland and threatened tariffs on European allies if a deal isn’t reached. Today also marks the first anniversary of Trump’s second inauguration, and it’s been eventful to say the least.

Equity indices in Asia were weak, given the declines in US equity futures and the global trade tensions. The Nikkei was down over 1%, but India was the only other country down more than 1%. South Korea’s KOSPI declined 0.4%. Yes, you read that correctly- South Korean stocks had a daily decline for the first time in 2026. The more concerning aspect of the weakness in Asia, though, is in the bond markets where JGB yields are surging to multi-decade highs in their biggest one-day moves since the Liberation Day turmoil last April.

European stocks are much weaker this morning, and in early trading, the STOXX 600 is down 1.3%. Spain is leading the declines with a drop of 1.7%, followed by Germany (-1.6%), and Italy (-1.5%). The weakness this morning stems from President Trump’s announcement over the weekend that he would put tariffs of 10% on the imports of eight European countries beginning on 2/1, which will increase to 25% on 6/1, if no deal is reached on Greenland. Making matters worse are reports that the President will put 200% tariffs on imports of French wine if French President Macron refuses to join the Gaza Board of Peace.

Whenever we see large declines like the market is poised for this morning, it always helps to put the move in perspective. The chart below shows SPY’s performance during the current bull market, and the red dots indicate every other time that SPY gapped down at least 1%. While today’s occurrence is only the third in the last eight months, since October 2022, there have been 37 other occurrences, which works out to an average of once per month.

Today’s gap down in SPY comes as the market has been stuck in a holding pattern for the last several weeks. Based on pre-market trading, SPY is trading right now at the same levels it traded in back in late October.

Brunch Reads – 1/18/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Oh, Bother: Every year on January 18, we celebrate Winnie-the-Pooh Day, which marks the birthday of A. A. Milne, the writer who created Pooh and the rest of the Hundred Acre Wood crew. Written nearly a century ago, Winnie-the-Pooh follows a honey-loving bear and his friends in a countryside inspired by the real Ashdown Forest in England.

Each character plays a distinct role that helps explain why these stories have endured. Pooh himself isn’t especially clever, but thoughtful in his own slow, roundabout way. He’s certainly forgetful and is intensely motivated by his love for honey. Piglet embodies anxiety, often afraid but willing to try anyway. Eeyore is connected to melancholy and pessimism, but he’s still always included and valued. Tigger has over-the-moon enthusiasm and confidence, while Owl is wise, despite his tendency to misspell words. Rabbit needs control, Kanga is overprotective, and Roo is very dependent. Christopher Robin, the only human, anchors the group.

The stories are filled with instantly recognizable symbols and lines that have become cultural shorthand. Pooh’s love of “a little something” to eat, his confusion over long words, and his tendency to pause mid-thought all reinforce the idea that not everything needs to be rushed or optimized. Lines like “You’re braver than you believe, stronger than you seem, and smarter than you think” and “Sometimes the smallest things take up the most room in your heart” are still iconic almost a century later.

Markets & Investing

Even Warren Buffett couldn’t keep beating the market without fail. Here’s why. (MarketWatch)

Even Warren Buffett’s edge has faded some, not because his skill spontaneously disappeared, but because extraordinary success attracts so much capital that beating the market becomes structurally harder. Berkshire Hathaway’s once-massive long-term outperformance steadily shrank as the portfolio grew, with returns converging toward the S&P 500 benchmark over the past couple decades. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – 1/16/26 – Looming Return To Normalcy

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we muse about a return to normalcy across markets, the economy, and society that is rapidly progressing but not quite complete. A review of equity markets from across the globe shows that normal might mean lower given valuations and price action that investors have gotten used to. We also dive into early earnings reports, US economic data, and some notable releases from the rest of the global economy this week.