The Closer – Earnings, Revisions, Data Center ABS – 4/22/26

Log-in here if you’re a member with access to the Closer.

- Tesla (TSLA) reported earnings after the bell with weaker profitability in part because of a litany of massive projects such as Optimus robots, Robotaxi rollout, and more.

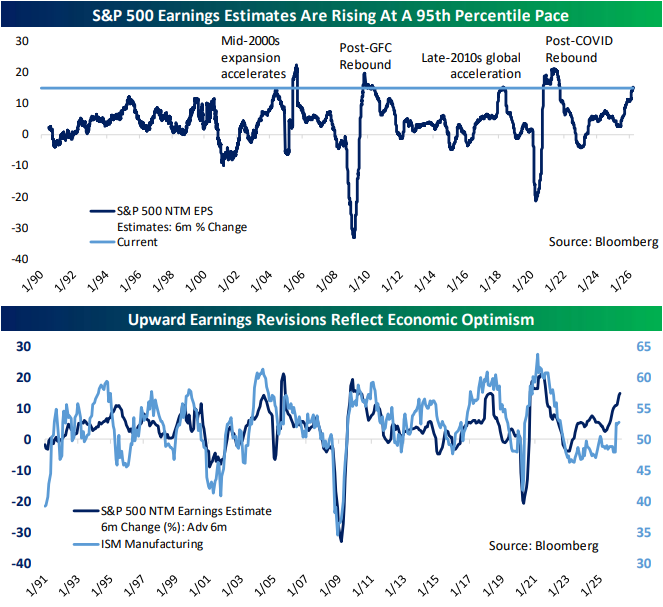

- Since the end of 2024, earnings estimates have risen 25.3% and have accelerated more recently with the 6 month change in the 95th percentile of all periods.

- After a strong Q1 last year, data center ABS issuance has moderated over the past year.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 4/22/26

Q1 2026 Earnings Conference Call Recaps: Masco (MAS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Masco’s (MAS) Q1 2026 earnings call.

![]()

Masco (MAS) is a global leader in home improvement and building products, best known for brands like Delta Faucet, Behr paint, and Hansgrohe. The company primarily serves repair and remodel markets across plumbing, coatings, and wellness products, giving it a strong read on housing activity, consumer spending, and contractor demand. Masco delivered a strong Q1 with sales up 6% and EPS up 20%, driven by pricing and better-than-expected plumbing volumes, especially in North America, where share gains and resilient demand stood out. The company is navigating a volatile macro backdrop, with tariff changes potentially helping but largely offset by rising commodity costs like copper, oil, and resins. PRO paint demand remained solid while DIY continues to lag due to weak existing home sales. Management highlighted restructuring and cost actions as key margin drivers, with benefits already showing. Despite geopolitical uncertainty, including oil-related inflation pressures, Masco remains optimistic about long-term demand for repair and remodel, supported by aging housing stock and high home equity. On better-than-expected results, shares rose 10% on 4/22…

Continue reading our Conference Call Recap for MAS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Leaders Leap

B.I.G. Tips – New Highs Without the Mag 7

Q1 2026 Earnings Conference Call Recaps: Boeing (BA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Boeing’s (BA) Q1 2026 earnings call.

![]()

Boeing (BA) is one of the world’s largest aerospace and defense companies, building commercial aircraft like the 737 and 787, military platforms, satellites, and aviation services for airlines, governments, and defense agencies. With a nearly $700 billion backlog and exposure to both global travel demand and defense spending, Boeing offers a real-time lens into airline health, geopolitical tensions, and large-scale industrial production. The quarter showed continued stabilization with revenue up 14% to $22.2 billion and improved losses, driven by stronger deliveries and performance across all segments. Commercial momentum is building, with 737 production stable at 42/month and plans to ramp higher, while certification of the 737-7/10 and 777X remains the key for future deliveries and cash flow. Defense demand is accelerating alongside heightened global tensions, helping offset potential risks from the Middle East conflict, which has not yet impacted deliveries but could affect airline economics via fuel prices. The main bottleneck is supply chain friction, like engine delays and seat certifications that are holding back deliveries despite improved factory execution. Free cash flow was negative $1.5 billion in Q1 but is expected to turn positive in the second half as production ramps and deliveries increase. On better-than-expected results, BA gained 5.75% on 4/22…

Continue reading our Conference Call Recap for BA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Signs of Life for Bitcoin

It was a rough six months for Bitcoin longs, as the price of BTC fell by more than half from an all-time high of $126,251 last October 6th, down to the low $60,000s in Q1.

Things have turned more positive this month, though, as Bitcoin has risen from $68k at the end of March up to $79k today.

As shown below, the rally over the last week or two has pushed Bitcoin’s price above the top of the downtrend channel that had formed off the highs made late last year. We’ve also seen a series of higher lows since the intraday low was made on February 24th.

If Bitcoin continues higher, its next test will be right around $85k, which acted as support from last November through January before ultimately giving way.

That prior support will now act as resistance that could be difficult to break through on a first or second test.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market thought like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

Bespoke’s Morning Lineup – 4/22/26 – Semis on the Brink of History

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When you sell your great companies and add to the losers, it’s like watering the weeds and cutting the flowers.” – Peter Lynch

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to check out Paul Hickey on CNBC’s Squawk on the Street today at 10:30 Eastern.

It looks like a two-day losing streak was all the Nasdaq needed to recharge from the impressive 13-day streak the index ripped off from the March lows. Following news that President Trump extended the ceasefire with Iran, Nasdaq futures point 0.75% higher while the S&P 500 looks to gap up 0.60% at the open. Treasury yields are lower, with the 10-year hovering near 4.27%, while crude oil and gold rally by 0.50% to 1.0%. The star of the show this morning is Bitcoin, which is up over 4% and trading back above $78K, the highest level since early February.

In Asia, it was a mixed session overnight with the Nikkei up 0.4% and the Kospi adding 0.5%. Hong Kong and India, however, both finished down over 1%. European stocks aren’t looking as positive. The STOXX 600 is slightly lower, with Spain leading the losses, declining 0.5%. In both regions, the key driver of the moves has been Iran and its impact on energy prices.

Here in the US, it will be a quiet session for economic data, but the pace of earnings continues to pick up steam. Some of the more notable reports since the close yesterday include Boeing (BA), Capital One (COF), GE (GE), and United (UAL), and after the close, IBM, Tesla (TSLA), Texas Instruments (TXN), and United Rentals (URI) will be the headliners.

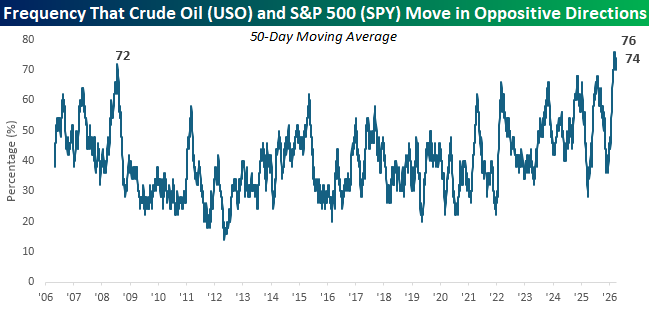

The fact that equity futures and crude oil are trading higher this morning is uncommon relative to recent history, especially since the war started. Over the last 50 trading days, the crude oil ETF (USO) and the S&P 500 ETF (SPY) have traded in the opposite direction (up or down) 37 times (74%). Since the ETF launched in 2006, this is right near the record high of 76%, reached less than two weeks ago on April 9th. Before this current period, the last time the correlation between the two ETFs was at comparable levels was in the summer of 2008, during the early stages of the financial crisis.

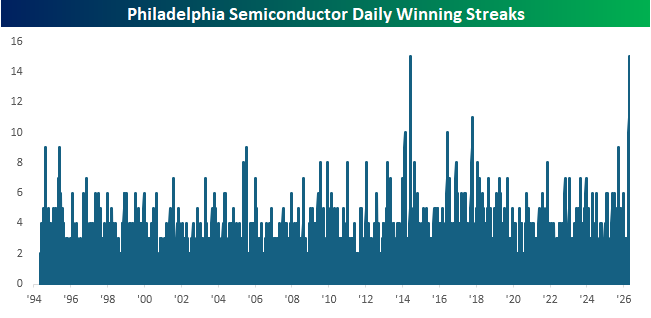

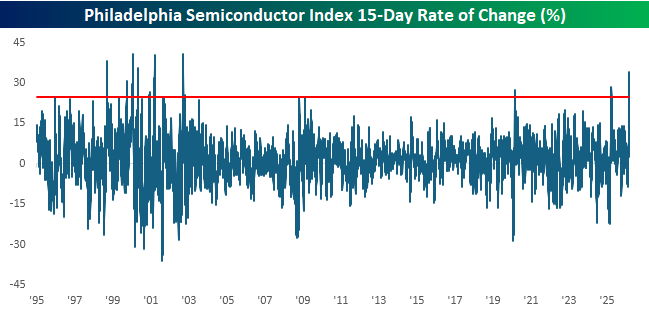

Shifting from crude oil, the fuel of the physical economy, to the fuel of the digital economy, semiconductors continued to roll yesterday as the Philadelphia Semiconductor Index (SOX) traded higher for the 15th straight day, tying the record from June 2014. Besides these two periods, there have only been three other periods where the SOX even had a ten-day winning streak.

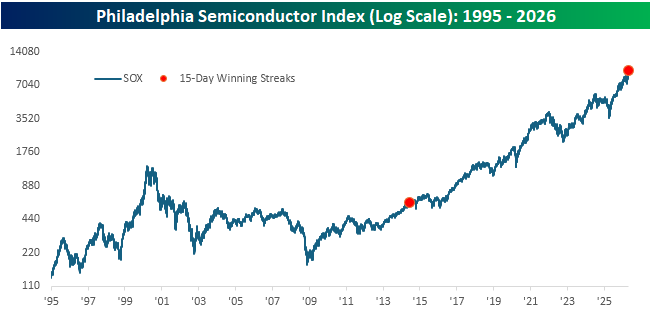

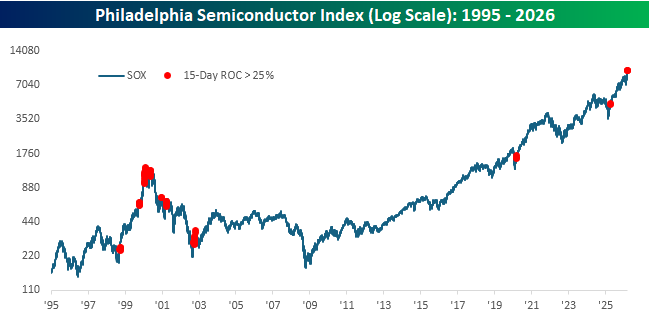

Below we show a long-term chart of the SOX showing when the prior 15-day winning streak occurred with a red dot. That streak capped off a longer run of gains for the index, and while it continued to rally, the pace of the ascent started to slow. From a longer-term perspective, though, it’s amazing to think that in the 12 years since that streak, the SOX has doubled and then doubled again and then doubled again and doubled once more for a total gain of 1,500%. Not bad for 12 years!

What’s just as impressive as the SOX’s 15-day winning streak is the 34% rally it has experienced during that span. That’s the largest 15-day gain for the index since October 2002, coming out of the dot-com lows. As shown in the chart, these types of moves were somewhat more common during the late 1990s and early 2000s, but have been very uncommon since.

Again, looking at these occurrences on a long-term chart of the SOX shows that most were exclusive to the period after the 1998 Russian Debt Crisis through the lows of the dot-com crash. Since then, the only two others were coming out of Covid and the tariff-tantrum. What has also been uncommon is for these moves to cap off rallies to all-time highs. That only occurred in late 1999 and early 2000. Gulp.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Warsh, Tech Finally Falls, Credit Cards – 4/21/26

Log-in here if you’re a member with access to the Closer.

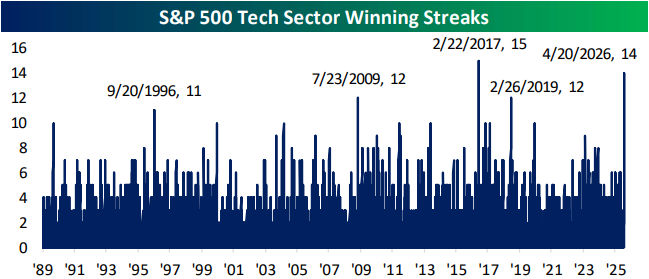

- The Tech sector ended a 14-day long winning streak; the sector’s second longest winning streak on record.

- Weekly estimates of private sector jobs growth from ADP continue to impress and are running above 200K for March.

- Credit card issuer delinquency rates have generally remained stable as related stocks have rebounded solidly.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!