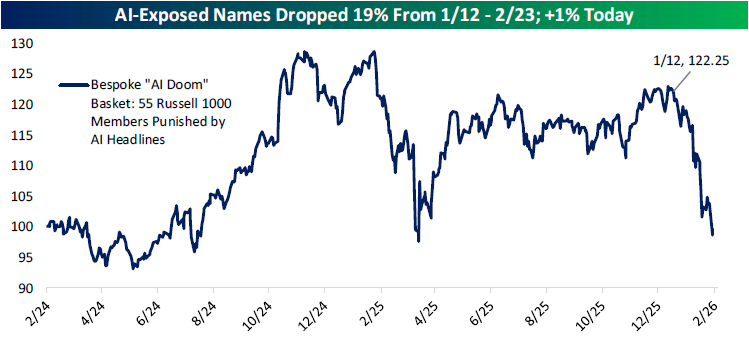

Chart of the Day: AI Data Doom

Q4 2025 Earnings Conference Call Recaps: Lowe’s (LOW)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Lowe’s (LOW) Q4 2025 earnings call.

![]()

Lowe’s (LOW) is the second-largest home improvement retailer in the world, operating approximately 1,700 stores across the United States. The company serves both do-it-yourself homeowners and professional contractors, offering everything from appliances and building materials to installation services. Lowe’s delivered Q4 comparable sales growth of 1.3% and full-year sales of $86.3 billion, but management struck a cautious tone for 2026, guiding comparable sales of flat to up 2% against a home improvement market they expect to be roughly flat. The central headwind remains elevated mortgage rates and the lock-in effect, suppressing housing turnover, though rates briefly dipped below 6% this week. Big-ticket discretionary DIY spending continues to be deferred. Pro customer growth was a standout, with the Pro extended aisle exceeding expectations and new AI-powered tools improving sales interactions. LOW shares fell as much as 5.7% on 1/25 despite beating EPS and revenue estimates…

Continue reading our Conference Call Recap for LOW by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Daily Sector Snapshot — 2/25/26

Q4 2025 Earnings Conference Call Recaps: CAVA (CAVA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers CAVA’s (CAVA) Q4 2025 earnings call.

![]()

CAVA (CAVA) is a fast-casual Mediterranean restaurant chain that has become a category leader, serving customizable bowls, salads, and pitas. With 439 locations across 28 states at year-end 2025, the company crossed $1 billion in annual revenue for the first time and is targeting at least 1,000 restaurants by 2032. CAVA delivered 22.5% full-year revenue growth and 4% same-restaurant sales growth in 2025, though Q4 comps slowed to 0.5%. Management guided 2026 same-restaurant sales of 3%–5%, noting Q1 is tracking above that range but embedding macro caution for the balance of the year. CAVA raised menu prices just 1.4% in January, kept its base bowl price unchanged, and has consistently taken far less pricing than competitors, underpricing inflation by over 10% in recent years. The company is launching pomegranate-glazed salmon, its first seafood protein, which tested better than chicken shawarma but carries a roughly 100bp margin headwind. Tariffs contributed to a 50bps food cost increase in Q4. After posting better-than-expected results, CAVA shares were up 24% on 2/25…

Continue reading our Conference Call Recap for CAVA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Triple Play Report: 2/24/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

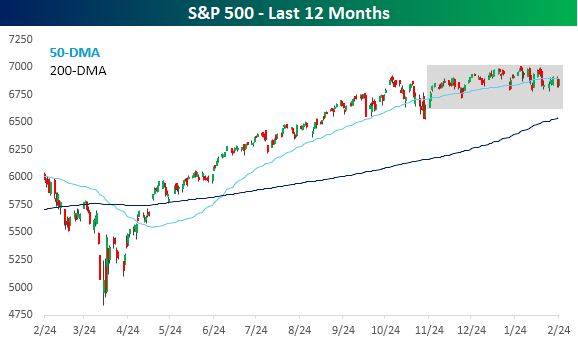

Bespoke’s Morning Lineup – 2/25/26 – Stuck to the 50-DMA

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To devastate is easier and more spectacular than to create.” – Anthony Burgess

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets are looking to build on yesterday’s turnaround Tuesday gains and are on pace to erase much of Monday’s losses, but whether these gains stick through the end of the week could depend on Nvidia’s (NVDA) report after the close. It’s widely assumed that the results will be strong, but will they be strong enough? And ff they’re too strong, will that also be interpreted as further future disruption in the software space?

Crude oil is higher this morning, trading just above $66 per barrel, even as Reuters reports that OPEC+ is considering a 137K barrel increase to daily production. Gold is also fractionally higher, back above $5,200 per ounce as silver surges 4% and platinum spikes 8%. Even bitcoin, yes bitcoin, is higher by more than 2%.

Asian stocks finished the day higher across the board, with the Nikkei up over 2% and South Korea up just under 2%. Chinese stocks also traded higher even as the Ministry of Commerce threatened to impose countertrade measures in response to the new tariff policies of the Trump Administration.

In Europe, stocks are also broadly higher but at a more restrained pace. The STOXX 600 is up 0.5%, led higher by 1% gains in Italy and the UK. Eurozone GDP fell more than expected (-0.6% vs -0.5% forecast) and German GDP was in line with expectations, growing 0.3% q/q.

Besides some important earnings reports after the close from NVDA and Salesforce (CRM), it’s a quiet day for data, but we will hear from many Fed speakers, including Barkin, Schmid, and Musalem.

Given the ongoing weakness we have seen in certain areas of the market, which investors now think will be devastated by AI, it’s still hard to believe how range-bound the S&P 500 has been. Yesterday, the S&P 500 closed less than 0.1% below its 50-day moving average. You can’t get much closer than that! And it wasn’t just yesterday. The rangebound morass has been going on for months now, as there hasn’t been a day in the last three months where the S&P 500 closed more than 2.5% above or below its 50-day moving average.

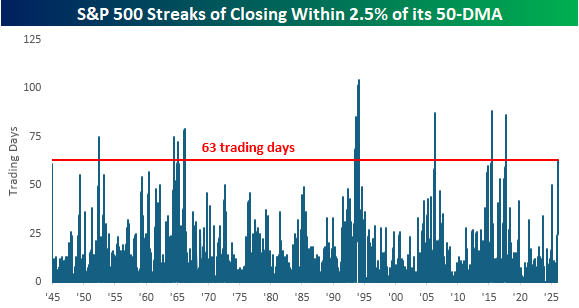

Periods where the S&P 500 has been so closely anchored to its 50-DMA haven’t been all that common throughout history. The chart below shows streaks when the S&P 500 closed within 2.5% of its 50-DMA (above or below), and the current streak, which reached three months (63 trading days) yesterday, is the longest since the first Trump administration in August 2017. Since WWII, there haven’t been many other extended periods where price was consistently so close to its 50-DMA.

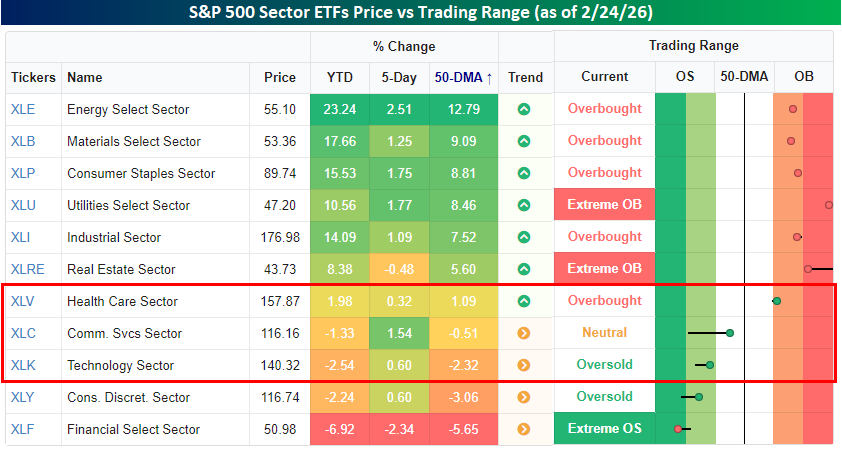

What makes the current streak even more incredible is that most sectors haven’t been showing the same pattern. As of yesterday’s close, just three of eleven S&P 500 sector ETFs – Health Care (XLV), Communication Services (XLC), and Technology (XLK) – closed within 2.5% of their 50-DMAs, and most sectors aren’t even close. Six are more than 5% above their 50-DMAs, and another is more than 5% below its 50-DMA. Like a sleeping volcano, the S&P 500 looks placid from above, but underground, the molten lava bubbles.

The Closer – AI Doom, ADP, Earnings – 2/24/26

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a review of the latest Fedspeak in addition to all the further pain in software names (pages 1 – 3). Next up, we show where some outperformers were today in addition to an update on regional Fed indices (page 4). After that, we provide a review of the latest positioning data (pages 5 & 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

The Triple Play Report: 2/23/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Daily Sector Snapshot — 2/24/26

Q4 2025 Earnings Conference Call Recaps: Domino’s Pizza (DPZ)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Domino’s Pizza’s (DPZ) Q4 2025 earnings call.

![]()

Domino’s Pizza (DPZ) is the world’s largest pizza company by retail sales, operating over 21,000 stores globally through a franchise-heavy model with roughly 7,186 US locations. As the dominant player in quick-serve (QSR) pizza with approximately 25% US market share, the company offers insight into consumer spending patterns across income cohorts, the evolving economics of delivery versus carryout, and the competitive dynamics of value-driven restaurant businesses. Management guided to 3% US same-store sales growth in 2026 against what they expect will remain a pressured macro backdrop. CEO Weiner introduced the ambition of doubling US retail sales from roughly $10 billion over time, benchmarking against QSR category leaders with 40-50% share. Pricing was flat in Q4, yet estimated franchisee store profitability grew to approximately $166,000, management’s “profit power” thesis in action. The company grew all income cohorts in 2025, pushing back on the lower-income consumer weakness narrative prevalent across QSR. On aggregators, management stressed they haven’t reached fair share on Uber or DoorDash and are growing those platforms carefully to ensure new orders are genuinely additional rather than cannibalizing their own direct channels. DPZ reported better-than-expected revenue on weaker EPS, as the stock climbed 4.1% on 2/23…

Continue reading our Conference Call Recap for DPZ by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: