Daily Sector Snapshot — 3/28/25

B.I.G. Tips – Nasdaq’s Month From Hell

Q4 2024 Earnings Conference Call Recaps: Lululemon Athletica (LULU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Lululemon’s (LULU) Q4 2024 earnings call.

![]()

Lululemon Athletica (LULU) is an athletic apparel retailer specializing in technical athletic wear for activities such as yoga, running, and training. The company offers a range of products, including pants, shorts, tops, jackets, and accessories designed for both men and women. Known for its innovative, high-quality fabrics like Luon and Luxtreme, LULU has positioned itself as a premium brand in the athleisure market. Beyond apparel, Lululemon provides insights into the growing intersection of fitness and fashion, catering to consumers seeking both performance and style. To end its year, LULU reported a 13% YoY increase in revenue, reaching $3.61 billion. Despite this growth, the company experienced a slowdown in traffic at its 374 US stores, attributed to cautious consumer behavior amid economic uncertainties and high inflation. International markets, particularly China, showed strength, with a 21% increase in same-store sales. CEO Calvin McDonald highlighted ongoing challenges such as tariffs and increased competition from emerging brands like Alo Yoga and Vuori. Despite better-than-expected results, downbeat guidance spooked investors, dragging the stock down more than 15% in trading on 3/28…

Continue reading our Conference Call Recap for LULU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 3/28/25 – Breakout Fake Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s simply no polite way to tell people they’ve dedicated their lives to an illusion.” – Daniel Dennett

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As the S&P 500 and Nasdaq look to extend their weekly winning streaks to two, they will need some help. Overnight, Asian markets were lower across the board with the Nikkei down 0.3% while China was down 0.7% as tariff concerns continue to weigh on sentiment. In Europe, things aren’t much better as the fallout from this week’s tariff announcements and others planned for next week on April 2nd, shake investor confidence. The STOXX 600 is down about 0.5% which would put it down by about 1% for the week.

US futures are down across the board with the S&P 500 trading nearly 0.2% lower while the Nasdaq faces a decline of 0.31%. Treasury yields had been rising in recent days even as stocks struggled, but this morning, the 10-year yield is 4 basis points lower to 4.33%. Oil prices are basically unchanged at just under $70 per barrel, while gold and silver are both up about 1%. After hitting a record high two days ago and selling off by over 4% since then, copper prices are marginally lower again this morning.

This morning’s economic calendar is busy with Personal Income and Spending at 8:30, as well as the Michigan Sentiment report at 10 AM. The key report of the day, however, will be the PCE report at 8:30. How this report comes in relative to expectations will likely determine whether the week finishes with a plus sign or minus sign next to it.

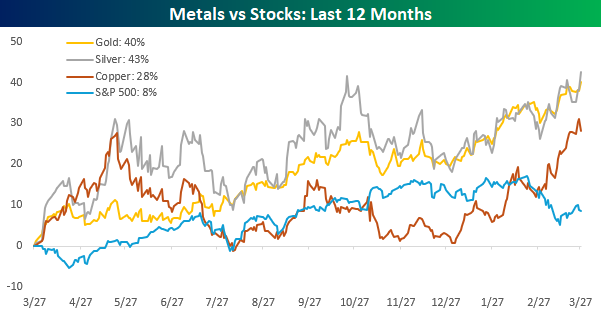

Stocks have had difficulties seeing gains lately, but hard assets like gold, silver, and copper have been ripping higher. Over the last year, gold and silver have rallied 40% or more while copper prices have risen 28%. The S&P 500 is also up on a y/y basis, but it’s up by less than a third of copper’s gain and less than a quarter of gold and silver. While gold and silver have been outperforming the S&P 500, up until just recently copper had been underperforming. Since the S&P 500’s peak in mid-February, though, all three commodities have seen their rallies pick up steam, and this week they all traded at 52-week and/or all-time highs.

This week’s move in copper was particularly interesting. After trading at an all-time high on Wednesday, copper finished the day down more than 2% from its intraday high and fell another 2%+ in Thursday’s session. As you can see in the chart, the commodity had a similar move higher and subsequent reversal early last May when it hit record highs after an even more impressive rally. While it’s tempting to look at the rally in copper as a sign of economic strength, it’s worth pointing out that the price in New York has rallied more than the price in London, and that’s because traders have been stockpiling inventories ahead of anticipated tariffs from the Trump administration.

The Closer – NIPA Revisions, Autos, Internationals – 3/27/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with some commentary regarding the North American tariff situation (page 1). We then look at the latest update of GDP data (page 2). Next, we look at the tariffs ramifications for used cars (page 3) and the advanced trade balance (page 4). We finish with a look at the historic spread between QTD performance of the US versus the rest of the world (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 3/27/25

Q1 2025 Earnings Conference Call Recaps: Cintas (CTAS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cintas’ (CTAS) Q3 2025 earnings call.

![]()

Cintas (CTAS) provides uniform rental services, facility services, first aid and safety products, and fire protection solutions primarily to businesses across North America. The company reported total revenue growth of 8.4% to $2.61 billion, driven by strong customer retention and operational efficiency. Despite macroeconomic uncertainty, customer purchasing remained steady, reflecting continued demand for outsourcing solutions that stabilize cash flows. The company achieved record-high gross margins of 50.6%, benefiting from investments in technology-driven operational improvements, including SAP (enterprise software standardizing business processes) and Smart Truck (route optimization software improving logistics efficiency). Management emphasized their preparedness for potential new tariffs, citing geographic diversity and dual-sourcing strategies. Additionally, CTAS ended efforts to acquire rival uniform services provider UniFirst, citing unsuccessful negotiations. With the triple play earnings, its third such report in the last five quarters, shares rose as much as 8.5% on 3/26, bringing the stock roughly 9% from its all-time high last November…

Continue reading our Conference Call Recap for CTAS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2025 Earnings Conference Call Recaps: Winnebago (WGO)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Winnebago’s (WGO) Q2 2025 earnings call.

![]()

Winnebago (WGO) is a leading manufacturer of recreational vehicles (RVs), boats, and specialty vehicles. Known for its iconic motorhomes, travel trailers, and premium brands like Newmar and Grand Design, the company serves outdoor enthusiasts, providing products that enhance the RV experience. WGO’s results were impacted by weak retail demand and rising consumer uncertainty, leading to a reduction in guidance. The company is navigating a cautious market, with consumer sentiment and inflationary pressures dampening RV and marine sales. Notable highlights include product innovation across motorhomes (Grand Design’s Lineage Series) and marine segments (Barletta’s market share gains). The company’s tri-brand strategy in motorhomes is showing promise, while WGO Towables is undergoing a pricing reset to boost competitiveness. Tariffs remain a concern, especially for motorized RV chassis, but WGO is working on mitigating costs. The stock opened 9.1% higher on 3/27 on better-than-expected results…

Continue reading our Conference Call Recap for WGO by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Country ETF Dividends

It’s been two weeks since the S&P 500 (SPY) put in its March 13 low. Since then, SPY has risen 3.2% which is slightly above the 2.6% average gain of the ETFs tracking the stock markets of 22 major global economies. As shown below, topping the list and outperforming in that span have been emerging market countries like Brazil (EWZ) and India (INDA) which are both up well over 6.5%. Meanwhile, only two stocks are meaningfully lower in that time: Taiwan (EWT) and Hong Kong (EWH). Of those, EWT is much more closely resembling the US over a longer time frame. Since the S&P 500’s February 19 peak, it is down 7.2% which is essentially tied with Taiwan for the worst performance since then. While those are the two biggest losers, most other country ETFs have moved higher to build upon what has been impressive strength year to date. Whereas the US is down low single digits this year, most other countries have in that time risen well into the double digits.

International ETFs don’t only have momentum on their side, but they also offer higher yields than the US at the current moment. On a twelve trailing month basis, SPY’s 1.26% yield ranks as the second lowest among these ETFs. The only one that has offered a smaller, and less than 1%, yield is India (INDA). On the whole, across all 22 ETFs, the average yield stands at 3.25%. Relative to each one’s respective history, whether or not those are elevated yields vary. For example, for the S&P 500, the current yield only ranks in the 5th percentile of that 20 year range. Meanwhile, Japan’s (EWJ) 2.22% yield ranks at the low-middle end of these ETFs, but is in the top decile versus EWJ’s own history.

Like this post? Join our complimentary Dividend Discovery email newsletter to receive a dividend-centric post in your inbox a couple of times per week. If you’re interested in dividend stocks and ETFs, this newsletter is for you! CLICK HERE to sign up with just your email or click on the image below.