Chart of the Day: New High For the DJIA Cumulative A/D Line

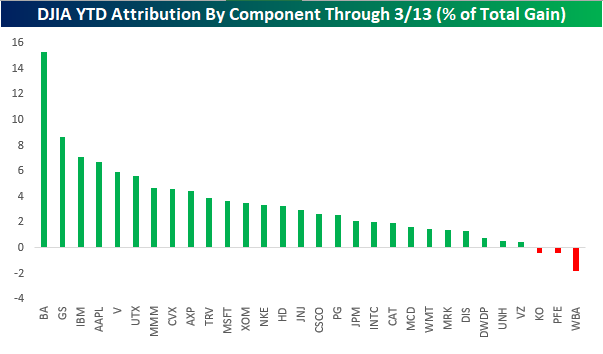

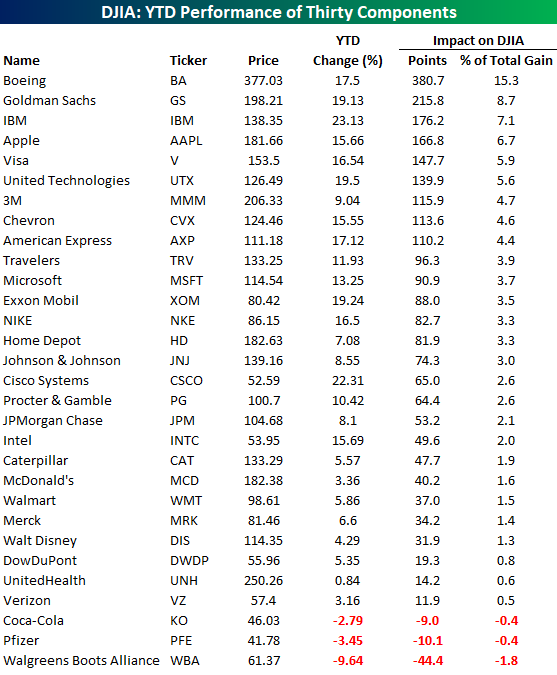

Boeing Still on Top of the DJIA

To say it has been a tough couple of days for anyone connected to Boeing (BA) would be an understatement. In terms of the company’s stock, the last two days have seen the first back to back declines of 5%+ in close to a decade (June 2009). As a result of this week’s decline, BA has lost its perch at the top of the DJIA in terms of best performers YTD, now coming in at number six. That being said, the stock is still up over 17% on the year, and because of the DJIA’s unique way of weighting components by their share price rather than market cap, BA has still been the largest contributor to the DJIA’s YTD gains. Even more amazing? It’s still not even close.

The chart below shows the YTD attribution of each of the DJIA’s 30 components to the index’s total gain YTD. Accounting for still more than 15% of the DJIA’s YTD gain, BA has had nearly twice the YTD impact on the DJIA so far this year as the next closest stock (Goldman Sachs – +8.7%). The fact that BA still has had such an outsized impact on the DJIA even after its big decline this week shows not only how extreme its move higher to kick off the year was, but also how odd it is to weight a stock index by an arbitrary measure like each component’s share price. One final note — it was somewhat ironic to see that the one stock that has had the most negative impact on the DJIA YTD is also the index’s newest component: Walgreen’s Boots Alliance (WBA) added last June.

![]()

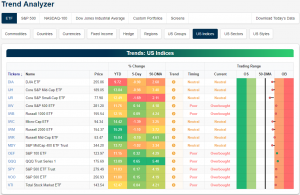

Trend Analyzer – 3/13/19 – Half and Half

Coming off of declines last week, equities have performed much better in the first half of this week. Currently, half of the major index ETFs have erased last week’s losses and moved back into overbought territory. Meanwhile, the other half which is predominantly small and mid-caps, in addition to the Dow thanks to Boeing, are still in the red. This half remains in neutral territory whereas most had been overbought this time last week. Despite some of these ETFs having managed to recoup losses from the past week, small and mid-caps still have a little ways to go until they do the same. Each of these are still down over 1% with the Core S&P Small Cap (IJR) down the most at 1.69%. Even with this recent pullback, small and mid-caps remain some of the best performing indices so far in 2019.

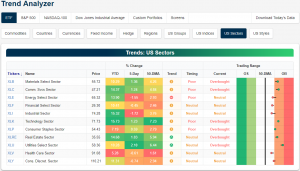

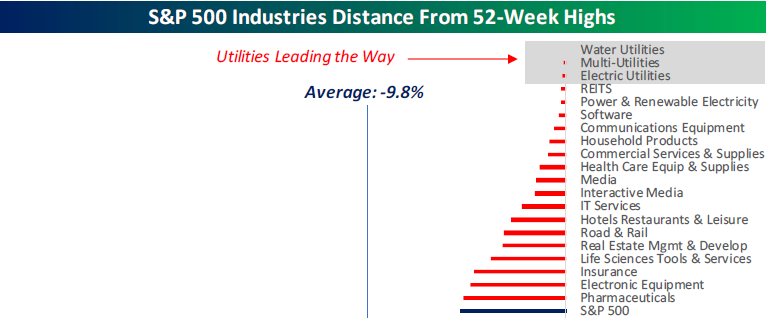

Taking a look by sector, it is just about the same story. Of the eleven sectors, six are now overbought while the remaining five are neutral. In the same way that those with a loss over the past week are still neutral, the others that have edged out gains have pushed deeper into overbought territory. As we mentioned in last night’s Closer, the Utilities sector is of particular interest. The sector’s Water, Multi, and Electric industries are the closest to their respective 52-week highs. Utilities is currently the most overbought approaching extreme levels (2 standard deviations or more above the 50-DMA). Over the past week it has gained the most at 2.1%, while on a YTD basis, the sector’s gains have been more middling. Conversely, the weakness in the Health Care sector ETF should be addressed as it is up only 5.28%; far worse than its peers.

Morning Lineup – Positive Bias in a Quiet Tape

Besides Brexit and Boeing again today, there really isn’t a lot going on in markets this morning. US futures are indicated modestly higher, and Boeing is trading down again. The stock is off its lows, though, as it attempts to bounce back from its first back to back declines of 5%+ in nearly a decade.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/13/19

After bouncing back nicely from its early lows on Friday, the S&P 500 is currently less than 5% from its September all-time high, while the 60+ industries in the index are down an average of close to 10%. What’s most surprising about where individual groups stand relative to their highs, though, is that the groups at the top are all Utilities. As shown below, Water, Multi, and Electric Utilities all hit 52-week highs yesterday and closed out the session less than 1% from those highs.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Boeing in the Penalty Box, Utilities Lead, Miners Bounce, Labor Bites — 3/12/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we provide a recap of today’s rejection of the Brexit deal and the continued turbulence in Boeing (BA). Next, we break down the S&P 500 industries distance from their 52-week highs. We note that the three industries closest to their 52-week highs are all Utilities. On the other hand, we look at Metals and Mining which currently sits the furthest from its highs, though, we show why the industry is not necessarily unattractive. We finish with a look at today’s release of NFIB Small Business Optimism and CPI.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Uptrends Galore

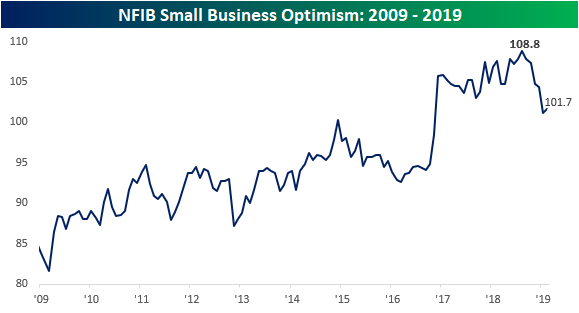

Small Business Rebounds Less Than Expected

After the steepest five month decline since the Financial Crisis and the longest monthly losing streak since 1998, NFIB Small Business Confidence rebounded in February, although by a less than anticipated degree. While economists were expecting the headline index to bounce from 101.2 up to 102.5, the actual increase was much smaller at just 101.7. As shown in the chart below, while the index was higher this month, it hasn’t put anything more than a small dent into the decline we saw from the high back in August of last year.

From a longer term perspective, the recent decline from the August 2018 high is definitely severe relative to prior declines. What we noted following last month’s report and is worth reiterating again is that prior periods where we have seen a quick and fast drop in small business sentiment haven’t been particularly good at timing downturns in the business cycle. While recessions typically are accompanied by a sharp downturn in business sentiment, there have also been plenty of other periods (1984, 1993, and 2005) where we saw sharp declines in small business sentiment but were nowhere near the onset of a recession.

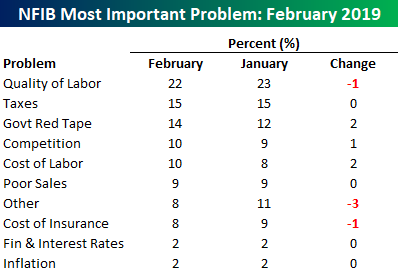

Finally, when it comes to issues facing small businesses, finding qualified employees continues to be the biggest problem they face, and there are some signs that they are starting to pay up in order to find those with the right qualifications. In this month’s survey, the percentage of businesses citing Labor Costs as the biggest problem increased from 8% to 10%.

Bespoke Stock Scores — 3/12/19

Morning Lineup – Brexit and Boeing

Today’s Morning Lineup is brought to you by the letter “B” as Brexit and Boeing are the major drivers of headlines this morning. Regarding Brexit, while things looked promising ahead of today’s vote after last night’s deal between PM May and EU President Juncker, reality has set in overnight, and the prospects of the deal passing a vote in Parliament aren’t looking entirely promising at this point. Meanwhile, Australia and Singapore joined the growing list of countries grounding flights of the 737 Max, and just now Malaysia announced the same. While the FAA deemed the 737 Max airworthy overnight, it also sent a mixed message mandating Boeing to push certain changes to the 737’s flight control system by ‘no later’ than April.

In economic news, the NFIB Small Business Optimism Survey increased versus January but came in lighter than expected, while CPI was right in line with forecasts at both the headline and core levels.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/12/19

Software has been a key group for the market over the last year, and yesterday’s rally took the S&P 500 Software group back within 1% of an all-time high. On Friday, the index bounced right at what was former resistance levels which was an encouraging sign. This group is dominated by Microsoft (MSFT) but is also comprised of Oracle (ORCL) Adobe (ADBE), and salesforce.com (CRM). Watch this group in the coming days to see if it can lead the broader market higher.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Technicals, Big Mondays, and Analyst Sentiment — 3/11/19

Log-in here if you’re a member with access to the Closer.

The S&P 500 managed to re-take its 200-day moving average today after just one day below it, and this sets the stage for a fourth test of resistance at 2,818 in the coming days/weeks. In tonight’s Closer sent to Bespoke Institutional clients, we take a look at Monday gains of 1%+ for the S&P 500 over the last ten years and whether the upside momentum to start the week typically continues for the remainder of the week. We also provide a big update on analyst Buy, Sell, and Hold ratings and how analyst sentiment has changed since the S&P peaked nearly six months ago on September 21st.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!