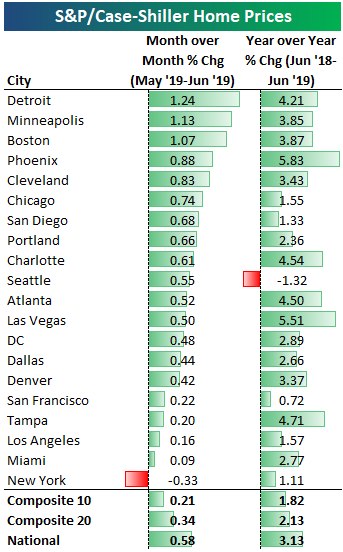

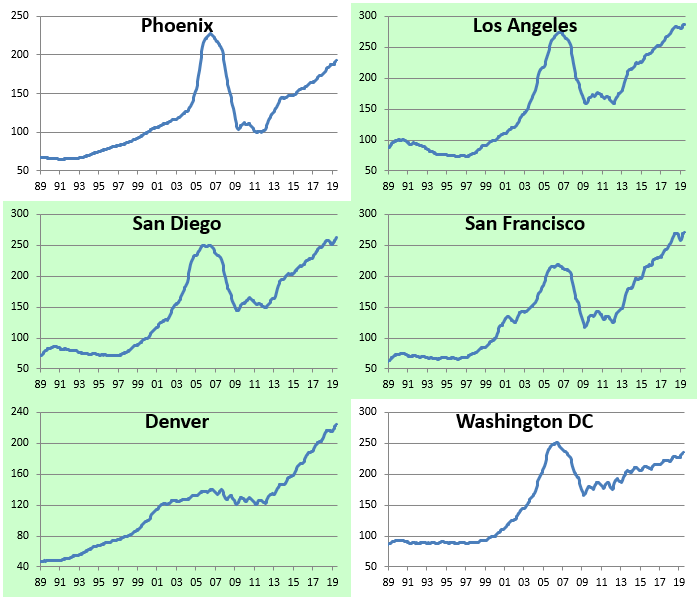

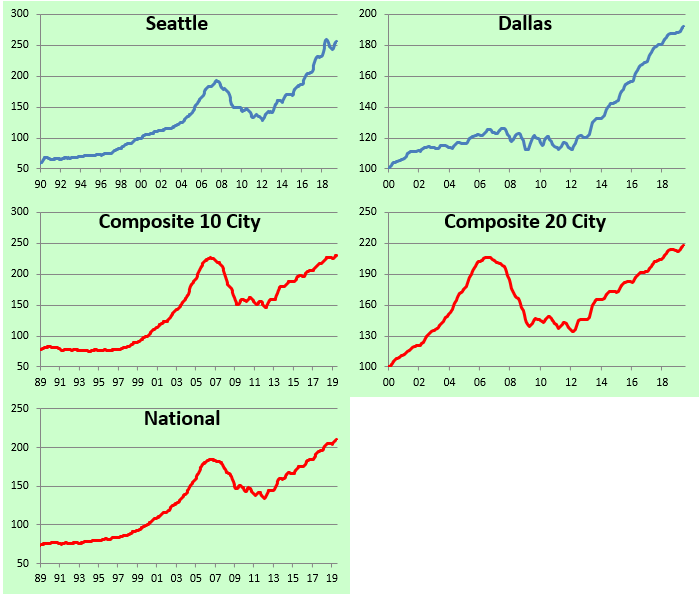

City-by-City Home Price Update — S&P Case Shiller

Below is an updated look at home price changes across the 20 cities tracked by S&P/CoreLogic’s Case Shiller indices. Detroit, Minneapolis, and Boston were the hottest areas for home prices on a month-over-month basis in June. All three areas saw prices increase by more than 1% MoM. The only area that saw MoM home price declines was New York at -0.33%.

On a year-over-year basis, the 10-city composite index was up just 1.82%, while the National index was up 3.13%. Seattle is the one area that is down year-over-year at -1.32%. Phoenix and Las Vegas are up the most YoY at 5%+.

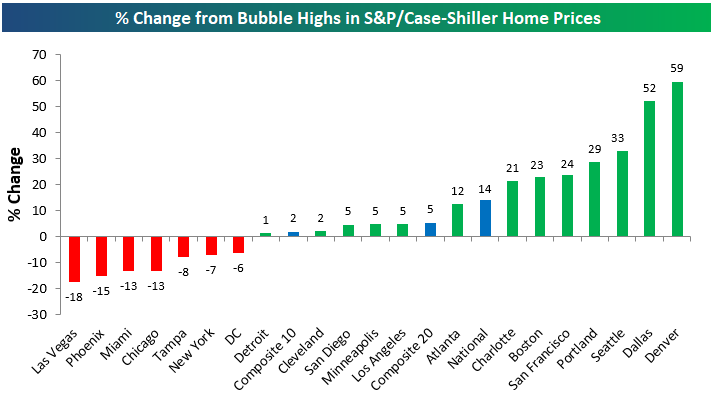

Below is a look at where home prices in each city stand versus their peak prices during the housing bubble of the mid-2000s. At this point, roughly two-thirds of cities have managed to take out their prior housing bubble highs. The only cities where prices are still below their prior highs are Las Vegas, Phoenix, Miami, Chicago, Tampa, New York, and DC. Detroit is the most recent city to take out its prior highs.

Denver and Dallas are both up the most above their prior highs at 50%+.

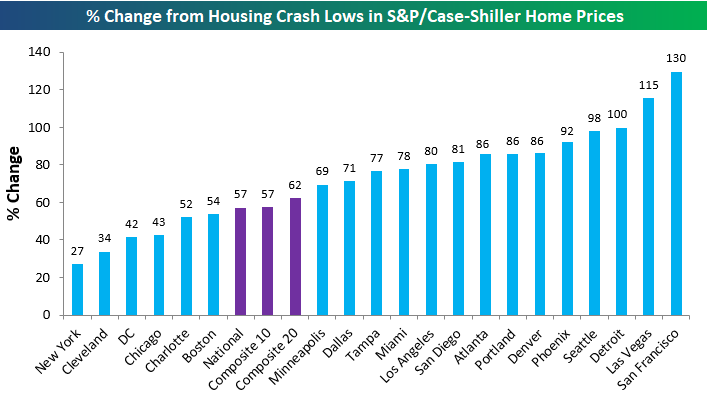

Below we show where home prices currently stand versus their housing crash lows. The composite indices are up 57-62% from their financial crisis lows, while San Francisco, Las Vegas, and Detroit are all up triple digit percentages. New York is up the least at just 27%.

Below are charts of home prices for each city going back to 1989 (Dallas only goes back to 2000). Charts highlighted in green highlight cities where home prices have taken out their prior bubble highs. Start a two-week free trial to Bespoke Premium for more in-depth equity market and economic research.

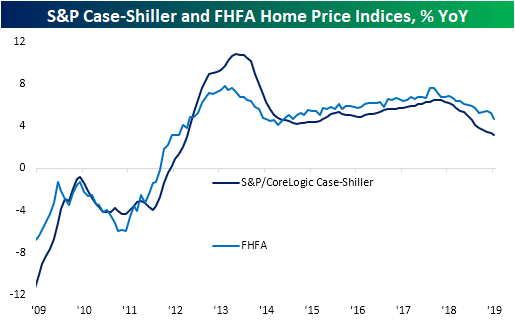

Slowing Home Price Growth

It was a busy morning for data on home prices with the releases of the June readings for S&P/CoreLogic Case-Shiller and the FHFA’s home price indices. Both indices essentially told the same story for home prices: still growing, but at the slowest rate in years. The S&P/CoreLogic reading was expected to show home prices grew by +3.30% YoY compared to +3.43% last month. Results were even weaker with home prices slowing to +3.13% for June while the May release was revised down to +3.35%. This marks the slowest growth since September of 2012 when home prices grew +3.0% YoY. For this index, June marked the 15th consecutive month of declines in the YoY growth rate. That has surpassed a 14-month long streak ending February 2015 and is now the longest since a 41-month long streak that came to a close in February of 2009 when prices were falling over 12% YoY.

The monthly FHFA Home Price index came in at 4.7% YoY which was lower than the prior reading for May of 5.2%. While it is not part of any dramatic streak like the S&P/CoreLogic index, this was the lowest growth rate since early 2015. One important thing to note, though, is that these two home price readings did not take into account all of the effects of the most recent plunge in rates or the Fed’s July rate cut because they’re on a two-month lag. Start a two-week free trial to Bespoke Premium for more in-depth equity market and economic research.

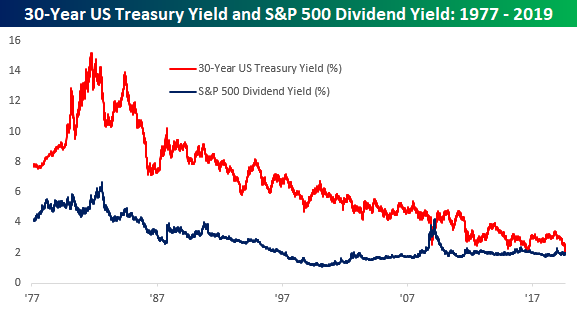

S&P 500 Yield Tops the Thirty Year

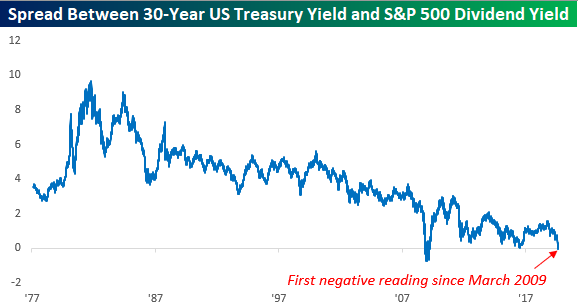

The yield on the 10-year US Treasury dropping below the dividend yield on the S&P 500? That’s so last month. Today, it’s the 30-year yield that’s falling below the S&P 500’s dividend yield. At 1.966%, the 30-year Treasury yield just dropped below the dividend yield of the S&P 500 for the first time since March 2009. Who knows if we’ll finish the day with a 30-year/S&P 500 inversion, but the way things have been moving, it’s probably just a matter of time if it doesn’t happen today.

The chart below shows the spread between the 30-year and the dividend yield of the S&P 500 going back to 1977. The only other time in the last 40+ years where we have seen a similar inversion was for a few months in late 2008 through March 2009 (the low point of the Financial Crisis). In July 2016 right after the Brexit vote, the S&P 500 dividend yield came within 0.01% of the 30-year’s yield, but it couldn’t quite make it higher.

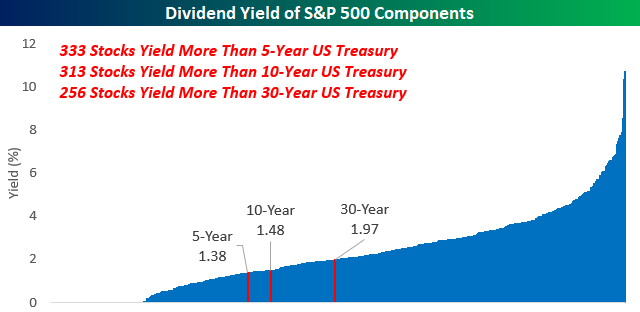

Looking at individual stocks, it’s pretty amazing how many stocks now yield more than the 5,10, and 30 year US treasuries. As of this morning, two-thirds of the stocks in the S&P 500 yield more than the 5-year, more than 62% yield more than the 10-year, and slightly more than half yield more than the 30-year. Start a two-week free trial to Bespoke Premium for more of Bespoke’s actionable equity market research.

Chart of the Day – Massive Bond Outperformance

Bespoke’s Morning Lineup — Drifting Higher

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Copper, Curve, Mortgage Rates, Sector Valuation, Manufacturing – 8/26/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at copper’s 52-week low as the 2s10s curve made new flats for the cycle. We also show the lag in the drop in mortgage rates compared to bond yields. Next, we show just how much investors have flocked to defensive sectors this year before finishing with a review of today’s manufacturing data including durable goods and our Five Fed Manufacturing Composite.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Fed Still Much Less Dovish Than The Market

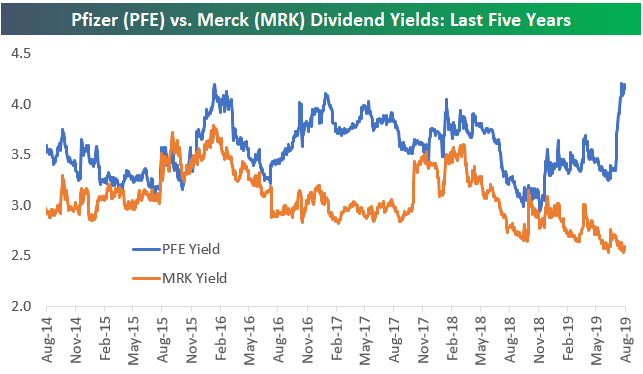

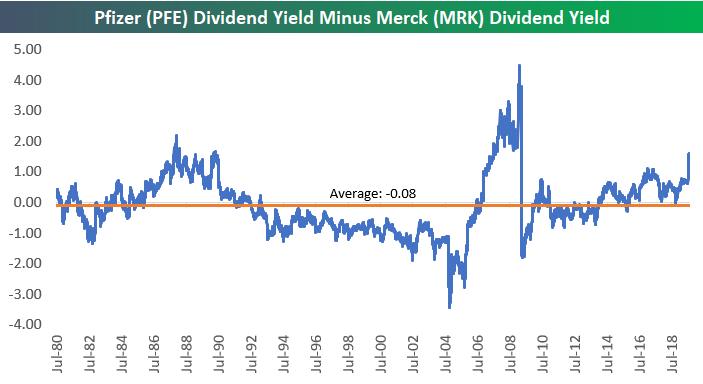

Battle of the Dow 30 Pharmas — PFE vs. MRK

Pfizer (PFE) and Merck (MRK) have been the two pure pharmaceutical plays in the Dow Jones Industrial Average since PFE was added to the index in April 2004 (MRK was added in 1979). Over the years, these two Health Care behemoths have trended mostly inline with each other, as the correlation between their daily prices going back to 1980 is 0.96. Every now and then, however, the two diverge as has been the case recently.

Below is a price chart of Pfizer (PFE) since 1980 with special focus on the last five years. As you can see, the stock trended higher from 2014 through late 2018, but this year it has struggled, especially recently as the company lowered guidance at the end of July and announced a deal to combine its Upjohn business with Mylan (MYL). To many analysts in the sector, the terms of the deal with MYL seemed to be expensive for PFE. As of today, PFE is down 20% year-to-date.

Merck (MRK), on the other hand, has had a great 2019 (up 12% YTD) and is finally approaching its all-time closing high of $89.80 reached on November 29th, 2000.

Below is a chart showing the ratio between PFE’s share price and MRK’s share price since 2000. (Both of these stocks last split in 1999.) When the line is rising, PFE’s share price is outperforming MRK’s share price and vice versa. You can see that since 2008, the ratio has traded back and forth between 0.4 and 0.7. PFE’s recent underperformance has left the ratio at the very bottom of the range over the last 10+ years.

Both of these blue-chip pharmas are big dividend stocks, but along with price their dividend yields have started moving in opposite directions. PFE last upped its dividend in December 2018 right as its stock price was peaking. With its share price down 20% YTD, PFE’s dividend yield has shot up to 4.16%. Merck (MRK) last hiked its dividend in July 2018, and while that caused its yield to move above 3% for a short period of time, the rise in its share price has left it with a yield of just 2.57% at the moment.

Since 1980, the average spread between PFE’s dividend yield and MRK’s dividend yield has been extremely close at just -0.08 percentage points. As shown below, the current spread of 1.59 ppts is as high as it has been in more than ten years. Start a two-week free trial to Bespoke Premium for more of Bespoke’s actionable equity market research.

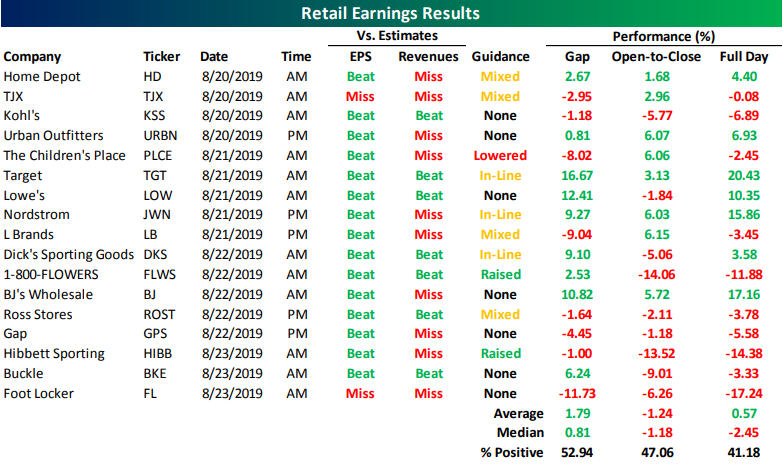

Retail Earnings Still in Focus

As we made note of in Friday’s Bespoke Report, retailers were one of the highlights last week as stocks like Target (TGT) and BJ’s Wholesale (BJ) saw some of their best reaction to earnings in their histories. Despite large gains for some retailers, Friday declines weighed heavy on the average performance of these stocks. Not a single one that reported Thursday night or Friday morning was positive in response to earnings.

Bottom line beat rates were solid as 88% of retailers that reported last week surpassed estimates. Only TJX (TJX) and Foot Locker (FL) missed on EPS. Revenues, on the other hand, were a bit weaker as less than half beat. For comparison, the rolling 3-month revenue beat rate for all stocks from our Earnings Explorer is 57.49%. Guidance also left something to be desired as only two of the ten companies giving any guidance raised forecasts. Ironically, those two that raised guidance—1-800-FLOWERS (FLWS) and Hibbett Sporting (HIBB)—both fell more than 10% on their reaction days!

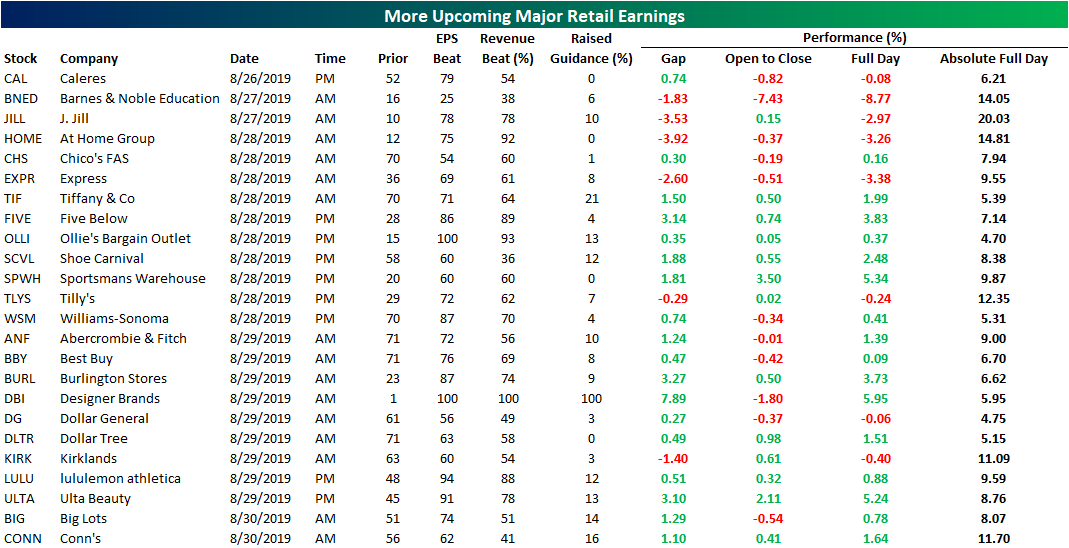

This week, retail continues to dominate the earnings calendar with 24 retail stocks reporting second-quarter results. Some notables include luxury retailer Tiffany & Co (TIF) and, on the other end of the spectrum, dollar stores like Dollar General (DG) and Dollar Tree (DLTR). Two-thirds of the stocks reporting this week have averaged a full day gain in response to earnings. Some of the most volatile of these in either direction are Barnes & Noble Education (BNED), J. Jill (JILL), and At Home (HOME) which have averaged absolute moves of over 14%. Bespoke Institutional members can view these stocks’ earnings history and stock reaction in response using our Earnings Explorer tool.

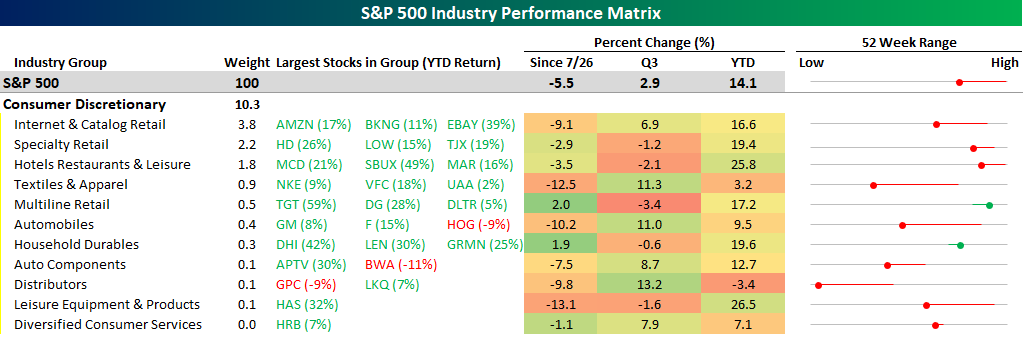

Mixed Fortunes in Consumer Discretionary

Since the S&P 500’s closing high in late July, most industries in the index have seen declines. Of the 60+ active industries, just ten are up since the close on 7/26, and only one (Construction Materials) is up over 5%. On the downside, eleven industries are down over 10%, including Energy Equipment and Services which is down 19%!

Among the 11 major sectors, one where there has been disparate performance among the individual industries within it is Consumer Discretionary. The graphic below shows each of the industries within the Consumer Discretionary sector, their overall weight in the S&P 500, the performance of the largest stocks in each industry, a performance summary, and then a snapshot of where each industry is trading with respect to its 52-week range (red or green circle) and where it was trading on the day of the S&P 500’s peak.

While the Consumer Discretionary sector remains in the upper end of its one-year range after trading near 52-week highs back in late July, individual industries are all over the map with respect to their 52-week ranges. For starters, Distributors, which is a very small industry, is trading right near 52-week lows. Similarly, another three industries (Textiles, Auto Components, and Autos) are in the lower half of their one-year ranges. Outside of these four industries, the remaining seven are all in the upper half of their 52-week range, and two are even up since the S&P 500 peaked in late July. As shown in the graphic, Multiline Retail has rallied 2% since late July and is trading closer to the high end of its 52-week range than any other industry in the sector. Who would have thought a couple of months ago that Multiline Retail would be a leading industry in the sector? But that’s what happens when a stock like Target (TGT), which is the largest stock in the industry, rallies 20% on earnings.

Behind Multiline Retail, the only other industry in the sector that is up since 7/26 is Household Durables, and that group’s strength has been driven by homebuilding stocks which have benefited from extremely low-interest rates and better affordability. Start a two-week free trial to Bespoke Institutional to access our interactive Security Analysis tool and much more.