Daily Sector Snapshot — 3/10/26

Q4 2025 Earnings Conference Call Recaps: Kohl’s (KSS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Kohl’s (KSS) Q4 2025 earnings call.

![]()

Kohl’s (KSS) is a US department store chain with roughly 1,150 locations that sells apparel, footwear, home goods, beauty, and accessories, targeting primarily low- to middle-income households. The retailer blends national brands with a large portfolio of proprietary labels (Sonoma, LC Lauren Conrad, Tek Gear, Jumping Beans) and has leaned heavily on its Sephora at Kohl’s shop-in-shop partnership to attract younger shoppers and drive traffic. Kohl’s is a useful barometer for value-oriented discretionary spending in the US. The company reported a difficult but stabilizing quarter as comparable sales fell 2.8% and net sales declined 3.9%, though EPS of $1.07 benefited from tight inventory control and expense cuts. Management attributed weak traffic largely to financially strained value consumers and admitted missteps in fall seasonal inventory allocation and insufficient promotional intensity during key holiday periods like Black Friday and Cyber Monday. The turnaround strategy centers on restoring proprietary brands, sharpening price points (including more $10-and-under items), improving “trip assurance” by increasing inventory depth, and driving traffic through Sephora, impulse merchandising, and digital improvements. Digital sales rose low single digits, but conversion remains an issue. Guidance for 2026 calls for comps between down 2% and flat with EPS of $1.00–$1.60, reflecting cautious expectations as lower-income shoppers remain pressured by macro conditions. KSS reported a revenue miss on stronger EPS, as the stock rose as much as 11% on 3/10, but completely erased those gains intraday…

Continue reading our Conference Call Recap for KSS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2025 Earnings Conference Call Recaps: Vail Resorts (MTN)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Vail Resorts’ (MTN) Q2 2026 earnings call.

![]()

Vail Resorts (MTN) operates some of the world’s largest ski destinations, including Vail, Breckenridge, Park City, and Whistler, while also running lodging, ski schools, rentals, and retail tied to mountain tourism. Its Epic Pass subscription model has changed the ski industry by locking in demand months before the winter season, with passholders now representing roughly 75% of visits. The company provides insight into premium leisure travel, weather sensitivity in outdoor recreation, and consumer willingness to prepay for experiences. Management described the season as the worst Rockies weather environment in company history, with snowfall down 43% YoY and February temperatures 9°F above average, limiting terrain openings to 70–80% of acreage at some resorts. As a result, visitation was down 13%, revenue was down 5%, and resort EBITDA was down 8%. Despite the disruption, the Epic Pass model helped stabilize results. Pass sales were up 3% entering the season, softening the revenue decline even as skier visits fell 12% season-to-date. Vail is responding with more targeted pricing and marketing, including a 20% pass discount for ages 13–30 and new lift-ticket products like Epic Friends and advance-purchase tickets. MTN shares fell 5.4% at the open on 3/10 after posting EPS and revenue misses, but the stock erased the loss intraday and was in positive territory an hour into the trading session…

Continue reading our Conference Call Recap for MTN by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

A Range Like Few Others

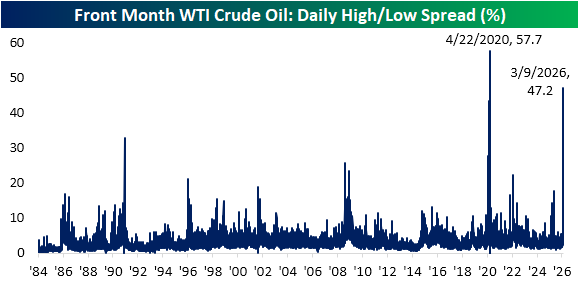

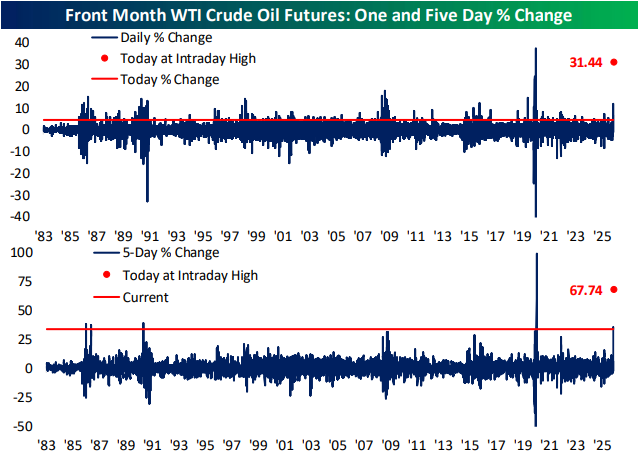

The situation in Iran, among other catalysts, has understandably raised volatility. As we discussed in today’s Chart of the Day, the S&P 500 (SPY) has been experiencing historic intraday moves so far this year, and of course, yesterday’s massive swings in crude oil prices are perhaps the prime example of heightened volatility. We highlighted in the Closer last night how front-month WTI went from trading just shy of $120 at its overnight highs Sunday, which would have been one of its largest daily gains on record. However, the steep drop in afternoon trading erased much of those gains. Today, the pullback has continued with another roughly 10% decline in both WTI and Brent futures. As shown below, the well over 40% intraday high and low range for crude prices yesterday made for WTI’s second largest intraday range in percentage terms. The only time with a wider intraday range was in the spring of 2020, around the time that prices briefly went negative. Even today, as the intraday high/low range has “moderated” to 10.5% for WTI as of this writing, that reading would rank in the 98th percentile of all periods since 1984.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

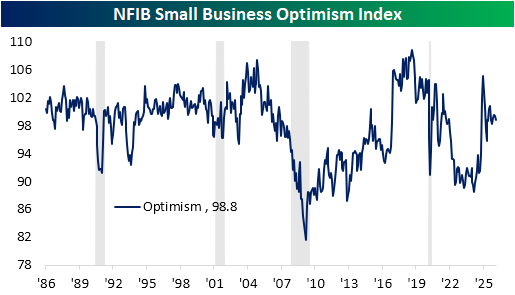

Small Business Sales Surge

This morning, the NFIB published its latest update on small business sentiment. At 98.8, the headline Optimism Index came in below expectations of 99.6 and last month’s reading of 99.3. As shown below, current readings are now middling versus the recent range following the 2024 Election surge and all readings throughout the survey’s history. In fact, the current reading is just below the historical median ranking in the 45th percentile.

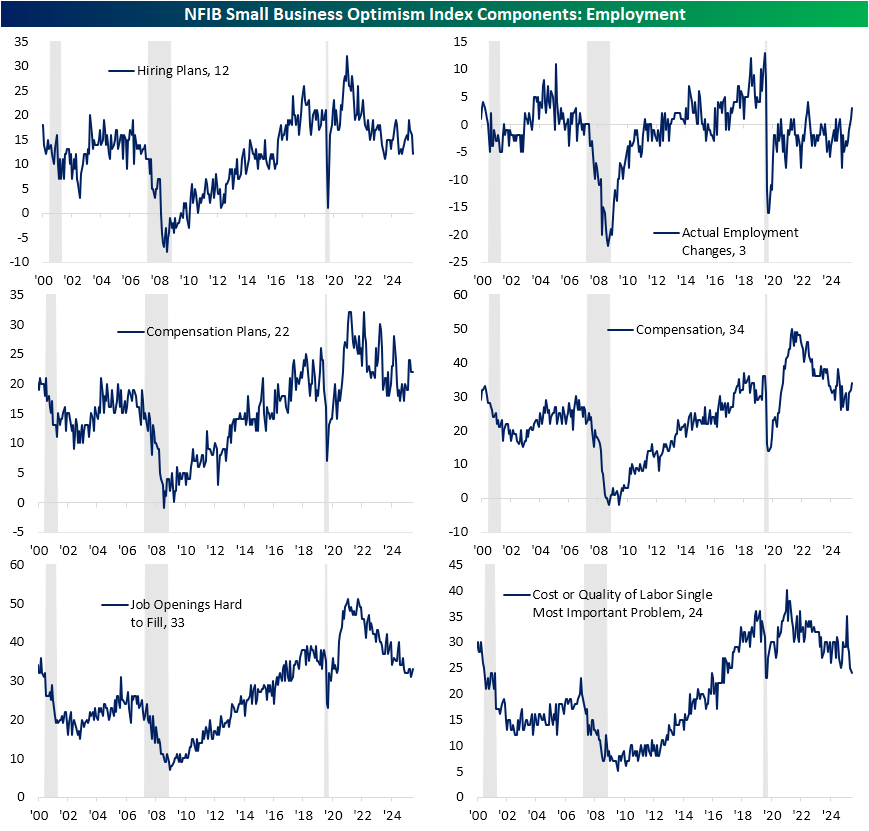

As we discussed in today’s Morning Lineup, labor-centric indices included in the NFIB report have suggested improvement over the past year, with another modest month-over-month increase most recently in February. Looking more closely, there are some interesting readings. For starters, hiring and compensation plans appear to be where there has been deterioration. While the latter was unchanged from recent highs in February, the former ranked as one of the larger declines across categories. Hiring plans dropped 4 points to the lowest level since May. Versus the reading of 16 last month, this index went from the 70th percentile down to below the historical median.

Despite those weaker readings in labor-related plans, actual labor changes were much more positive in February. For starters, actual employment changes came in net positive, which has been rare in the post-pandemic period. Further, that was the highest reading since February 2023. Compensation plans rebounded in tow to an eleven-month high. Finally, we would note that among the most important problem section of the report, the combined reading of the two labor-related problems was the lowest since May 2020.

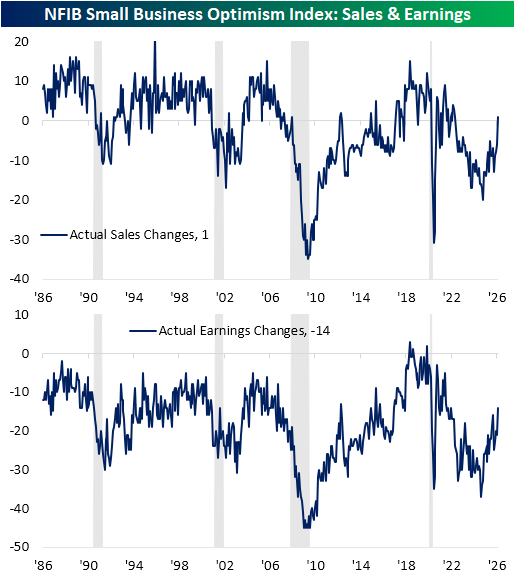

Similar to how “actual” indices were stronger than “expectation” indices regarding labor, the same dynamic was apparent for sales and earnings. Actual sales and earnings both surged in February. Top-line changes were reported as net positive for the first time since May 2022. Actual earnings changes have rarely come in net positive over the history of the survey, but this index rose to the most elevated reading since December 2021.

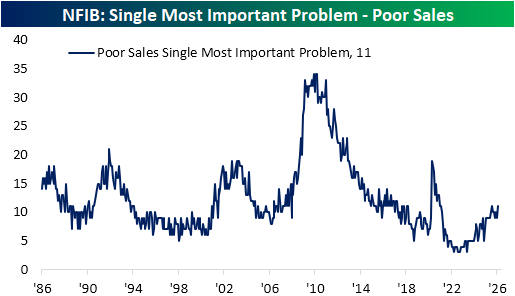

Ironically, the most important problem section again had an idiosyncratic reading versus the aforementioned actual sales change index. 11% of firms reported poor sales as their biggest issue, matching last July for the highest reading since February 2021.

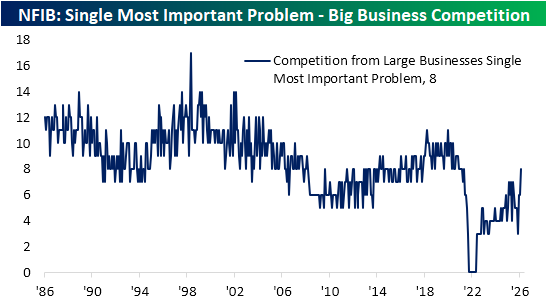

On the heels of the rise in poor sales concerns have been worries about competition from big business. As shown below, that problem has surged from negligible readings in 2022 to 8% of responses in February, the most since May 2021.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Chart of the Day – A High Friction Relationship

Bespoke’s Morning Lineup – 3/10/26 – The Whole is Worse than the Parts

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we’re at a bottom. I really do.” – Mark Haines, CNBC, 3/10/09

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a dramatic reversal late in yesterday’s session on hopes that the war in Iran would be ‘complete’ soon, futures were higher for the overnight session and into this morning. As the opening bell approaches, though, futures have been drifting lower, and all of the major averages are on pace to open fractionally lower. Treasury yields are little changed, and crude oil has been volatile, sitting under $90 per barrel. While that seems low relative to Sunday night, it’s still much higher than anything seen in the months leading up to the war in Iran. Gold prices are up over 1.5%, and silver is surging 5% as it’s currently trading at the same price as WTI! Bitcoin has been quietly grinding higher over the last few days, and this morning, it’s above $70K.

Earnings season is largely in the rearview mirror, but after the close, we’ll hear from Oracle (ORCL), which could be a major catalyst tomorrow for different parts of the AI ecosystem. The only economic reports on the calendar today are small business optimism from the NFIB, which came in weaker than expected (98.8 vs 99.5), and then at 10 AM, we’ll get Existing Home Sales for February.

Asian markets followed the lead of the late-day reversal in US equities and traded sharply higher overnight. It wasn’t enough to entirely erase Monday’s losses, but the Nikkei rallied just under 3% while South Korea surged over 5%. Chinese stocks rallied a more modest 0.7%, and while February exports surged 39.6% y/y, exports to the US declined 17%. Those lost exports to the US were scattered across Europe and Southeast Asia, and many of those likely ended up finding their way into the US in a roundabout way. In Japan, GDP rose 0.3% q/q, which was higher than expected, and in South Korea, growth contracted less than expected.

European stocks are also sharply higher this morning as the US reversal occurred after those markets closed for trading yesterday. The STOXX 600 is up 2.3%, and Germany, Italy, and Spain are all up over 2% as well.

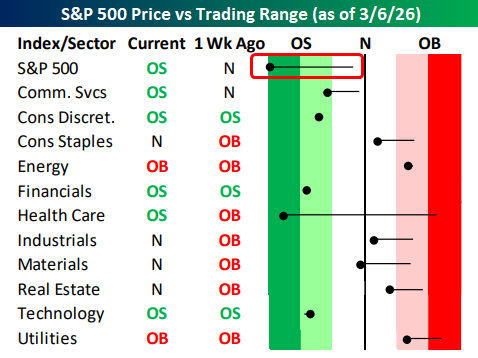

When you looked at page two of the Morning Lineup to see where sectors closed out last week relative to their trading ranges (image below), you may have done a double-take at seeing that the S&P 500 was in ‘extreme’ (2+ standard deviations) oversold territory and more oversold than any sector. In fact, the only other sector in extreme oversold territory was Health Care (after being in extreme overbought territory a week earlier), and just four other sectors were oversold while five were still above their 50-DMAs.

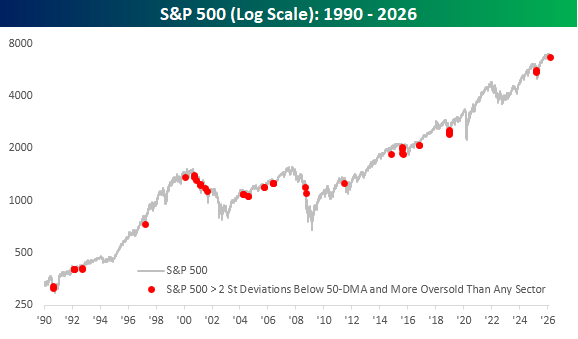

We were curious to see how often it is that the S&P 500 trades in ‘extreme’ oversold territory and is also more oversold than any other sector. Since sector data begins in 1990, there have only been 49 other days when this was the case, and a lot of them occurred during the dot-com bust from early 2000 to late 2001, but as the chart below illustrates, it’s hardly just a bear market phenomenon.

The Closer – Crude Craziness, Risk Bounce, Expectations – 3/9/26

Log-in here if you’re a member with access to the Closer.

- Markets continue to try to make sense of the Iran situation, making for a historic reversal today for crude prices.

- High volatility has showed that it works both ways with both crude and equities rebounding from sizable losses.

- Preliminary EPA estimates showed that nearly a third of consumer vehicles sold were EVs, hybrids, or fuel cell last year.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/9/26

Happy Birthday!

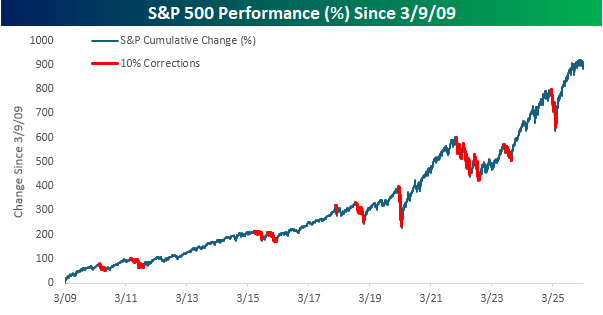

Just how low can stocks go? That was the question posed by the Wall Street Journal on Monday morning, March 9, 2009. Just like this year, March 9th fell on a Monday, following a Friday where the S&P 500 closed sharply lower on economic fears.

That’s where the similarities end. In 2009, the S&P 500 closed below 700 for the first time since 1996; this year, it’s trading not far below 7,000, or roughly ten times higher. Back then, strategists were debating if the index would crater another 27% to reach 500. Having already dropped 56% from its 2007 highs, another leg down felt entirely plausible, but in hindsight, it was the low. Compare that to today: when was the last time you saw mainstream analysts calling for a 27% drop, even with equities right near record highs?

The analysis from that article serves as a reminder of the investor tendency to extrapolate current trends into the future. If stocks are up, they’ll stay up; if they’re sliding, the bottom is always miles away. Analysts often add a ‘countertrend’ hedge in their forecasts just to cover their bases, but take today’s ‘temporary sell-off’ forecasts with a grain of salt. They’re only echoing what the market has been doing. The only way to know for sure is to watch, listen, and let the tape tell the story.

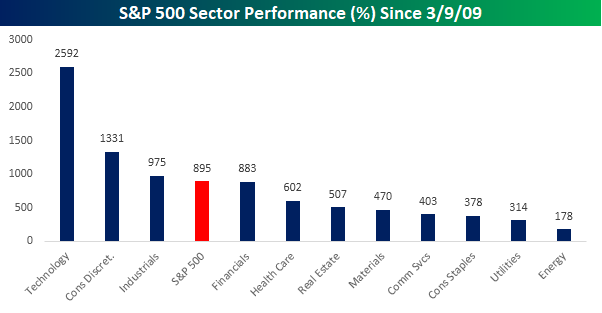

The ride since March 2009 has been incredibly rewarding for those who stayed the course. Since that Monday close, the S&P 500 has rallied 895% (excluding dividends), and more than half of all sectors have risen more than fivefold. Technology has been the top-performing sector with a gain of over 2,500%, followed by Consumer Discretionary, which is up by just over half of that amount. Rounding out the top three, Industrials is the only other sector that has outperformed the S&P 500 since the March 2009 low. While all eleven sectors are higher since March 2009, Energy (178%) and Utilities (314%) have been the worst performers, along with Consumer Staples (378%) and Communication Services (403%), which are the only other sectors that are up less than half as much as the S&P 500.

Have you ever heard anyone say that big gains are right around the corner? Of course not. Looking back at the last 17 years, it seems like the market has done nothing but go up. How many times have you heard someone say that the easy money has been made?

Investing always looks easy in retrospect, but in the moment, it never is. And the last 17 years? The S&P 500 has experienced two bear markets, three other near bear markets (-18%+ from a peak), and a total of 12 different declines of at least 10%. It’s nothing like the period from 2007 to 2009, but there were plenty of moments when putting new money into the market felt like anything but easy. That’s the trick. It’s only easy in retrospect.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up: