Daily Sector Snapshot — 7/25/25

Top Quotes from Recent Earnings Calls: 7/25/25

The Q2 2025 earnings season is well underway, and we sifted through earnings calls from the hundreds of companies that have reported since Wednesday’s (7/23) close, looking for some of the most interesting macro-related quotes from management teams that may serve as broader signals about the state of the economy, consumers, and markets. Below are twenty of the most revealing quotes that we pulled from this batch of calls, offering a window into what executives are seeing across industries and geographies right now.

- “We see AI powering an expansion in how people are searching for and accessing information, unlocking completely new kinds of questions you can ask Google… Our AI features cause users to search more as they learn that search can meet more of their needs. That’s especially true for younger users.” – Sundar Pichai, CEO, GOOGL

- “If you think about Marketplace and Medicaid members, what these folks have been hearing from every major media outlet for the last 6 months is that Congress is going to take away their health insurance. And that I think does drive a certain level of behavior when compounded with macroeconomic uncertainty… Then those folks are coming into the system and colliding with a provider ecosystem that is largely still operating in a fee-for-service manner [that] is concerned about losing revenue. And that’s where we’re seeing, I think, some of the aggressive billing and coding.” – Sarah London, CEO, CNC

- “Thus far, we believe the economy has been fairly resilient. Demand for transportation fuels remains strong, and I’m feeling more optimistic overall. The next key question is whether we’ll see further refinery rationalization.” – Gary Simmons, COO, VLO

- “I think we’ll probably have autonomous ride-hailing in half the population of the U.S. by the end of the year. That’s at least our goal, subject to regulatory approvals. I think we’ll technically be able to do… [And] the service areas and the number of vehicles in operation will increase at a hyper-exponential rate.” – Elon Musk, CEO, TSLA

- “This is a great time to be in the US wireless industry, as a customer, and as a participant. In the last 3 to 4 years, [customers have seen] speeds grow 3 to 4x, and data consumption grow 3 to 4x. And at the same time, customers have paid less in real terms for the product. And as an industry, we’ve seen a 50% growth in free cash flow, which is the one metric that really matters from a value creation perspective for the industry as a whole.” – Srinivasan Gopalan, COO, TMUS

- “No, I don’t think we can make any comments yet about consumer confidence. The demand for health care largely over time appears to have been inelastic. I don’t know that anything is necessarily changing that… We had good commercial growth in a lot of categories. We had declines in areas… that were government or no payer-sponsored business… Behavioral health admissions were down… Some of that was because we shrunk supply in certain facilities… So I think… we’re still pretty confident… in the demand for health care across our markets, and we don’t see that being disrupted too much in the short run here.” – Samuel N. Hazen, CEO, HCA

- “I used the word cautious optimism at the end of the first quarter. I would now turn my way all the way to optimism around the macro environment… I think Japan is reindustrializing… South Asia is growing at north of 10%… The Middle East are trying to create now diversified economies of which technology forms a strong piece… Europe has remained remarkably resilient… We come into North America and every company is now convinced that technology forms the basis of how do you scale revenue while not spending that much on CapEx and that much on labor expenses.” – Arvind Krishna, CEO, IBM

- “Joblessness is trending in the right direction. While GDP has been pulled down a little bit, it’s still positive for the back half of the year. And I think that all lends to a customer that’s more willing to get out there and spend and travel and do some things that they want to do.” – Robert D. Isom, CEO, AAL

- “The competitive environment is stable, not improving, but not deteriorating. So we have steady fiber overlap. That’s not new. Cell phone Internet continues at its pace for now. But just as big when you think about the overall market and funnel is the overall market is challenged because there’s an incredibly low amount of moves and new build… and then in addition to that, you have a reversion to mobile-only customers and [the Affordable Connectivity Program] accelerated that… reverting mobile-only back to the pre-pandemic level.” – Christopher Winfrey, CEO, CHTR

- “We’ve seen three quarters of revenue growth above our expectations, which we attribute at least in part to customers hedging against tariff uncertainty.”- David Zinsner, CFO, INTC

- “We have our arms around the what. I think the industry generally doesn’t have their arms around the why… The prevalence of behavioral conditions is up… People did not go for services during the pandemic, and now they are. There’s some pent-up demand. The supply side is finding interesting ways to code, to bundle codes… using AI… It’s happening nationally… not just Medicaid, not just Medicare… it’s across the board.” – Joseph Zubretsky, CEO, MOH

- “We’re seeing some pressure as energy project spending shifts to the right, partly due to economic uncertainty and regulatory issues. [Liquified Natural Gas] demand remains strong, but sustainable fuel projects have been the most impacted. Fortunately, things have cleared up over the last 10 days, and we expect positive momentum to return. Long term, the outlook for our energy segment remains extremely bullish, we’re simply in a normal part of the cycle.” – Vimal Kapur, CEO, HON

- “Many of the companies driving AI and data center growth don’t have strong infrastructure or utility capabilities, and some aren’t interested in building behind-the-meter power systems—our specialty. While we don’t have a specific project to announce right now, we’re positioning ourselves to capture growth as it emerges.” – James R. Fitterling, CEO, DOW

- “What I think feels different is it was just tough to get volume back even with promotions, [but] we’re starting to see the volume return. And I think that’s a strong sign that it’s a broad-based recovery… But to me, that’s very encouraging.” – Robert Jordan, CEO, LUV

- “There’s still pent-up demand. I have 0 doubt about that. How that gets released is going to… be the economic environment and how new vehicle affordability plays out in the coming months and years. If it doesn’t manifest itself in new vehicles, some of it tends to move into used vehicles. So you have to be agile in terms of how you move between the segments… But there is no doubt that there is and will remain our opportunity in the After-Sales side of the business.” – Michael M. Manley, CEO, AN

- “Tariffs are going to have — will not have a material impact on our growth rate when you look at our revenue growth year-on-year. They do have an impact on margin performance… because you’re passing it through. They’re largely a pass-through for us. So you see that in this updated guide as well.” – Kevin S. Krumm, CFO, FLEX

- “I met with the customer a couple of months ago that said that they were shifting some of their production from Asia into Mexico [because of tariffs], and we’ve got a strong service product coming out of Mexico… Over the long term, we think that, that will be a positive for us even if it doesn’t happen today or next week.” – Kenyatta Rocker, EVP of Marketing & Sales, UNP

- “We’ve had, I think, some very productive conversations with the administration with commerce over the last several weeks, and they’re listening to us. And I think they understand and share the same objective we do, which is to have U.S. manufactured vehicles be competitive in the U.S. and on the global stage… If logic prevails here, that seems to make a lot of sense to protect the competitiveness of U.S. manufactured vehicles.” – Jason Cardew, CFO, LEA

- “We recognize our consumers are under pressure from car prices and other costs, which have outpaced wage growth and higher interest, virtually double the rates we saw just a few years back.” – Daryl Kenningham, CEO, GPI

- “NATO members are now targeting defense spending increases to 5% of GDP… We recently secured software-defined radio awards from the German and Czech armed forces… replacing indigenous providers, a direct result of our resilient interoperable, battlefield proven technology and expanding global footprint.” – Christopher Kubasik, CEO, LHX

- “While enthusiasm for the boating lifestyle remains high, the uncertainty is prompting buyers to delay purchases until the economic outlook is clearer.” – Brett McGill, CEO, HZO

Q2 2025 Earnings Conference Call Recaps: Centene (CNC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Centene’s (CNC) Q2 2025 earnings call.

![]()

Centene (CNC) is a government-focused managed care company that provides health insurance through Medicaid, Medicare Advantage, and Affordable Care Act (ACA) marketplaces. Serving over 28 million members across all 50 states, Centene specializes in delivering healthcare services to low-income, vulnerable, and medically complex populations. Its Ambetter brand makes it the largest player in the ACA exchanges, while its scale in Medicaid gives it deep insight into US healthcare policy shifts, cost trends, and regulatory impacts. Q2 2025 was defined by a $2.4B earnings hit tied to a sharp deterioration in ACA marketplace risk pools, as healthy members left and high-utilizing members surged, exacerbated by program integrity enforcement. Medicaid margins were also pressured by rising costs in behavioral health, home care, and high-cost drugs, especially in Florida and New York. Medicare Advantage showed stable improvement, and Part D exceeded expectations with margins above 1%. The EPS miss on better-than-expected revenue resulted in a 4.5% gain for the stock on 7/25…

Continue reading our Conference Call Recap for CNC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Intel (INTC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Intel’s (INTC) Q2 2025 earnings call.

![]()

Intel (INTC) is one of the world’s largest semiconductor manufacturers, known for designing and producing CPUs, GPUs, and other chips that power PCs, servers, data centers, and edge devices. The company serves a broad customer base, from global cloud providers and enterprises to governments and OEMs. Intel is a key bellwether for both the technology supply chain and global manufacturing policy, particularly as a US-based chipmaker amid rising geopolitical tension and AI-fueled demand for compute. On the Q2 2025 call, Intel reported $12.9B in revenue (above estimates), but posted a GAAP EPS loss due to $800M in tool impairments and $1.9B in restructuring charges. CEO Lip-Bu Tan emphasized discipline across the board: right-sizing the organization (cutting 50% of management layers), cutting $5B in CapEx YTD, and pausing unprofitable fab expansions. AI was a major focus, with Intel repositioning around inference and “agentic AI,” while acknowledging its historic software gaps. Panther Lake (18A) and Granite Rapids are ramping, but Tan noted rebuilding trust in both x86 and foundry will take time and results. On mixed results, INTC shares were down 9% on 7/25…

Continue reading our Conference Call Recap for INTC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Boston Beer (SAM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Boston Beer’s (SAM) Q2 2025 earnings call.

![]()

Boston Beer (SAM) is one of the largest craft brewers in the US, best known for its Samuel Adams beer, Twisted Tea, Truly Hard Seltzer, Angry Orchard cider, Dogfish Head ales, and most recently, Sun Cruiser RTD (Ready To Drink) spirits. The company serves a wide range of consumers across beer, cider, and spirits alternatives, especially younger and flavor-seeking drinkers, while offering investors a window into evolving alcohol trends and consumer behavior. Its outsized focus on “beyond beer” categories (over 85% of volume) positions it uniquely within a declining beer industry. Despite a tough environment marked by weak summer demand and pressure on Hispanic consumers, Boston Beer posted 1.5% YoY revenue growth, a 380 bps YoY improvement in gross margin to 49.8%, and EPS growth of 24% to $5.45. Sun Cruiser saw strong distribution growth and is already a 4-share brand in RTD spirits. Twisted Tea lost floor space and may be overpriced in some packs, while Truly saw traction in its high-ABV “Unruly” line. Productivity gains and procurement savings helped offset $15–20M in expected tariff costs. Better-than-expected results lifted the stock as much as 12.9% on 7/25…

Continue reading our Conference Call Recap for SAM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 7/25/25 – Complacency?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When you’re good at something, you’ll tell everyone. When you’re great at something, they’ll tell you.” – Walter Payton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are sitting on modest gains as the S&P 500 looks to close out the week with a 1% gain. The S&P 500 has traded higher every day this week, and the number of record closing highs is starting to pile up with 13 on the year so far. That’s nowhere near last year’s total of over 50, but considering where the market was three months ago, it’s impressive to say the least.

While US equity futures hang onto positive territory, Asian stocks finished in the red even as the Nikkei started off the session at new highs. The reversal stemmed from concerns over a more aggressive BoJ. European stocks are also firmly in negative territory, with the STOXX 600 down about 0.5%. Outside of equities, energy commodities are modestly higher, while metals prices are lower across the board. In crypto, Bitcoin and Ethereum are both lower. It’s also worth pointing out that Bitcoin is now down near $116,000 after hitting a high of $123,000 eleven days ago.

The pace of earnings so far this month has been positive, economic data has been hanging in there, and we’re even starting to get some sense of clarity on tariffs, so you can’t fault investors for being optimistic. Today, we’ll get a bit of a break from the data, though, as the earnings and economic calendars are relatively light, but you never know when the President will drop a tariff-related headline.

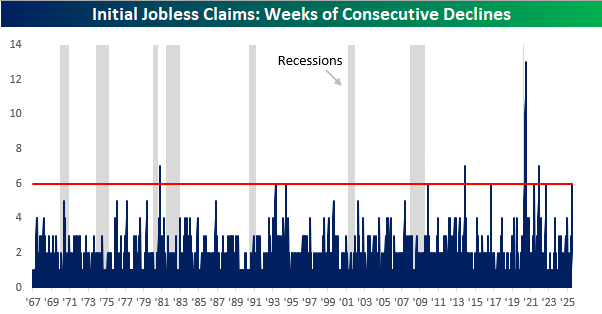

While there’s not a lot of economic data today, we wanted to take a moment to look back at yesterday’s initial jobless claims report, which came in weaker than expected and declined on a week-over-week basis for the sixth time in a row. As shown in the chart below, this was just the 11th streak of six or more weekly declines. Of those prior ten streaks, only four were longer, with just one stretching more than seven weeks. That record was the 13-week stretch coming out of the Covid lockdowns. We also included shading to indicate recessions, and you typically don’t see these kinds of streaks leading up to the onset of a recession.

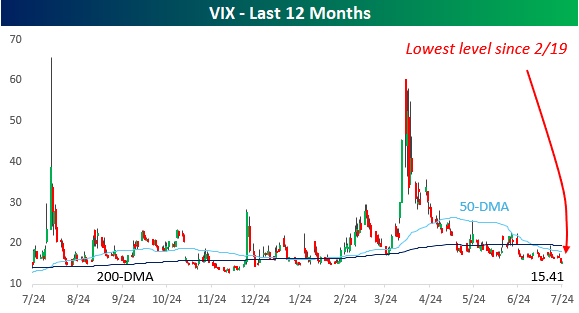

The market has been treading a steady path higher over the last several weeks, and one place the lack of volatility has shown up is in the VIX. This week, it dropped below 16 to its lowest levels since 2/19. That was right at the peak before the tariff-takedown, so it’s only natural to wonder if there’s a sense of complacency setting in.

The Closer – More Earnings, AI Laggards, ECB – 7/24/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after a review of the latest earnings including a luxury name and some AI basket members (pages 1 and 2), we review the performance of some AI adjacent stocks that have lagged behind (page 3). Next, we turn over to European rates (page 4) and finish with recaps of the latest economic data including flash PMIs (page 5) and new home sales (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day: Squeezed

Q2 2025 Earnings Conference Call Recaps: Alphabet (GOOGL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Alphabet’s (GOOGL) Q2 2025 earnings call.

![]()

Alphabet (GOOGL) is the parent company of Google and a global leader in internet services, digital advertising, AI innovation, cloud infrastructure, and consumer technology. Its products, ranging from Google Search and YouTube to Android, Chrome, and Google Cloud, serve billions of users and millions of businesses worldwide. With deep investments in AI models (like Gemini), autonomous driving via Waymo, and custom silicon (TPUs), it stands at the forefront of applied machine learning. The company delivered a strong Q2 with 14% revenue growth to $96.4B, driven by strength in Search, YouTube, Cloud, and AI subscriptions. Search queries surged, helped by new AI tools like AI Overviews and AI Mode. YouTube Shorts hit 200B daily views, with Shorts now monetizing at parity, or better, than in-stream ads in some regions. Cloud revenues grew 32%, with a record $106B backlog, though capacity remains constrained. AI was central throughout the call. Gemini usage grew 35x YoY, and token processing doubled to 980 trillion/month. CapEx was raised to $85B for the year to meet AI infrastructure demand. GOOGL shares opened 3.5% higher on 7/24 in reaction to its results…

Continue reading our Conference Call Recap for GOOGL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Chipotle (CMG)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Chipotle’s (CMG) Q2 2025 earnings call.

![]()

Chipotle (CMG) is a fast-casual restaurant chain known for its customizable burritos, bowls, tacos, and salads made with fresh, responsibly sourced ingredients. With over 3,400 locations across the US, Canada, and select international markets, Chipotle blends classic culinary methods with a highly efficient operating model. Chipotle’s Q2 saw 3% revenue growth to $3.1B but a 4% comp sales decline, as traffic weakened in May before rebounding in June and July. Management blamed low consumer confidence and a tougher value landscape, but emphasized successful marketing campaigns (Summer of Extras) and strong product launches like Adobo Ranch. Back-of-house upgrades, including a full rollout of produce slicers and a new equipment package, are expected to improve prep efficiency and expand catering. Internationally, locations in Kuwait are now outperforming US averages. CMG reported weaker revenue on in-line EPS, putting the stock in reverse, down close to 14% on 7/24…

Continue reading our Conference Call Recap for CMG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: