The Closer – Earnings Onslaught, Trade, Jobs – 7/29/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after recapping a busy night of earnings (pages 1 and 2), we dive into the latest update of trade data (page 3). Next, we look at the changes in home prices (page 4) before pivoting to a look at job openings in the form of the JOLTS release (page 5) and Indeed data (page 6). We cap off with a dive into consumer confidence figures (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Top Quotes from Today’s Earnings Calls: 7/29/25

The Q2 2025 earnings season is well underway, and we sifted through earnings calls from the 92 companies that have reported since Monday’s (7/28) open, looking for some of the most interesting macro-related quotes from management teams that may serve as broader signals about the state of the economy, consumers, and markets. Below are twenty of the most revealing quotes that we pulled from this batch of calls, offering a window into what executives are seeing across industries and geographies right now.

- UPS (UPS): “[Small businesses] are finding that in today’s environment, credit conditions have tightened up a bit on them. So it’s not that they don’t have access to capital in the ways that they have seen in prior years. So there are a number of just challenges that this group is faced with.” – Carol Tomé, CEO

- Proctor & Gamble (PG): “The volatility the consumer is seeing isn’t necessarily grounded in their current reality, but more about what they expect in the future. So consumers are being more careful with their consumption. They’re using up pantry inventory and looking for value, either in smaller packs and promotions, or in larger pack sizes from club stores and online.” – Andre Schulten, CFO

- Merk (MRK): “The CDC’s Advisory Committee on Immunization Practices subsequently voted to recommend ENFLONSIA for use in infants younger than 8 months of age for their first RSV season and include this new option in the Vaccines for Children Program, an important step in ensuring access.” – Dean Li, President

- Enterprise Products (EPD): “This past quarter was dominated by headlines about tariffs and trade… We’ve been clear about the risk of weaponizing U.S. energy exports. These kind of actions rarely hurt the intended target and often backfire hurting our own industry more… We’re fortunate this administration understands the importance of energy and global trade even if the Commerce Department may need a little reminder.” – James Teague, Co-CEO

- CBRE Group: “There is a lot of capital out there. We have it and other people have it that wants to buy real estate, and there is a huge amount of sell-side interest on the part of owners of real estate that haven’t been able to sell it for the last few years… We expect the sales activity and the refinancing activity to both continue strong in the back half of the year. We’re not expecting interest rates to move in a way that alter that materially.” – Robert Sulentic, CEO

- Nucor (NUE): “If we think about the resiliency of [non-residential construction] on the construction market in general. That took off really post-COVID, and it has remained robust for a long period of time, and we anticipate that remaining robust… So again, the demand drivers for this segment [steel products tied to commercial, industrial, and infrastructure builds] are really robust, and we expect them to remain that way, again, throughout the rest of this year and quite frankly, beyond.” – Leon Topalian, President, CEO

- PayPal (PYPL): “Today, almost 3.5 billion people rely on digital wallets as their go-to method for shopping and transferring funds… That’s 83% of global digital payments happening through wallets… But among those billions of users, there are hundreds of regional wallets represented. This fragmented system of wallets poses tremendous challenges and immense friction in a global commerce ecosystem.” – Alex Chriss, CEO

- Hartford Financial (HIG): “Yes… I think we spoke about it equally in the past. [Litigation finance and social inflation] are still a fact of life, still a tax. It’s still a burden. It’s not fair. It’s not what our court system was intended to [support]. But I’m also equally optimistic that more and more people across the industry and businesses are getting involved and trying to take a legislative corrective action [to curb these excesses]… I think it’s getting a little bit more national attention, particularly in D.C., and I was really actually encouraged by former Attorney General Barr’s comments on the need just to put some limits on these injury claims, including noneconomic limits.” – Christopher Swift, CEO

- Waste Management (WM): “I think you actually are seeing a little bit of strength in the economy that we haven’t had. We’ve talked about kind of an industrial recession over the last probably 5 or 6 quarters. And I think that’s largely kind of dissipated and we’re seeing it in roll-off and in [construction and demolition].” – James Fish, CEO

- Carrier Global (CARR): “We have not seen a big switch from repair over replace. We are watching the consumer. Movement was slower in 2Q than we had expected. Movement was a bit light in July, but it started to pick up towards the end of July, a bit more because of some of the heat in the country… Interest rates have continued to be high, which has put a damper on residential new construction and also people moving to buy new homes.” – David Gitlin, CEO

- Johnson Controls (JCI): “China is maybe a longer discussion, but I was there recently and maybe the one tidbit is that, that market is gradually turning into a more mature market in the sense of that the retrofit part of the market continues to steadily increase, which is different than a number of years ago when it was sort of a new construction new build market. So it’s starting to look a little bit more like some of our Western markets.” – Joakim Weidemanis, CEO

- Asbury Automotive (ABG): “The average age of a passenger car on the road is 14.5 years old, and the average truck is nearly 12 years old… recent and upcoming models have more technology and innovative powertrains, which should create opportunity for our service departments for years to come.” – Daniel Clara, COO

- Koninklijke Philips (PHG): “We continue to see strong demand in North America, with patient volumes remaining high and procedures still on the rise. Health systems are increasingly focused on productivity… finding ways to serve more patients at lower cost. At the same time, there’s growing interest in ambulatory solutions to extend care beyond hospital walls. Most importantly, we see this demand trend holding steady into next year. – Roy Jakobs, CEO

- Universal Health (UHS): “We continue in certain markets to be hampered by our inability to hire all the staff that we need. It’s still a tight labor market. And again, while it is not the pervasive issue that it was at the height of the pandemic, staffing scarcity continues to be an issue in some markets.” – Steve Filton, CFO

- UnitedHealth (UNH): “The American health system’s long-standing cost problem is accelerating. We are embracing our responsibility to continue to drive better health outcomes while trying to keep healthcare affordable for all Americans.” – Tim Noel, CEO

- Sysco (SYY): “Traffic to restaurants [was] down approximately 1% in the quarter, certainly better than Q3. We believe Q3 was a bit of an anomaly… external news was quite negative, consumer confidence dropped, the conversations about tariffs and the impact on consumer confidence [lowered traffic to restaurants] … We’re expecting the current conditions to continue for 2026.” – Kevin Hourican, CEO

- Lithia Motors (LAD): “I believe that manufacturers have already begun to either decontent cars or not charge for other upgrades… Consumers can save other dollars… So a finite 15% increase when we think about the tariff… is just another thing in our daily lives… As the world moves on and as [tariffs] start to change the industry, those with more cash and more ability to code solutions for customers [to] make it easier are those that are going to be able to grow market share and be less impacted by whatever changes do come from tariffs, franchise laws, or whatever else.” – Bryan DeBoer, CEO

- Royal Caribbean (RCL): “We see a very healthy customer. When we dig into that customer, they have great jobs, they have strong balance sheets, and they’re confident in spending and making sure that they’re receiving the vacation experience that they’re looking for. So again, I think all turns are green on the customer at this point in time, and they’re traveling all over the world. We’re seeing that not just in North American, but we’re also seeing that in European travel activity.” – Jason Liberty, CEO

- Boeing (BA): “[Supply chain] constraints tomorrow get resolved and then there’s new constraints, and you just constantly are working each one of those down… We’re in a perpetual rate increase kind of environment.” – Robert Kelly Ortberg, CEO

Q2 2025 Earnings Conference Call Recaps: Whirlpool (WHR)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Whirlpool’s (WHR) Q2 2025 earnings call.

![]()

Whirlpool (WHR) is one of the world’s largest home appliance manufacturers, producing major brands like Whirlpool, Maytag, KitchenAid, JennAir, and Amana. The company makes washers, dryers, refrigerators, ovens, dishwashers, and small kitchen appliances, primarily for the residential market. It serves both individual consumers and homebuilders, with a particularly dominant presence in North America, where 80% of its products sold are manufactured domestically. Whirlpool offers investors insight into global consumer health, the US housing cycle, and international trade dynamics, especially around tariffs and supply chains. Whirlpool faced ongoing headwinds from weak consumer sentiment and a flood of tariff-free Asian imports, which intensified promotional pressure and delayed expected tariff benefits. Net sales fell 3% YoY (ex-currency), and MDA (Major Domestic Appliances) North America margins held at about 6% despite volume and mix challenges. The company rolled out its largest product refresh in a decade, including customizable KitchenAid appliances and new JennAir cooktops. Management remains confident that Whirlpool’s US-based manufacturing footprint positions it to gain share as tariffs take hold. The company missed EPS and revenue estimates, and the stock fell as much as 12% on 7/29…

Continue reading our Conference Call Recap for WHR by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Boeing (BA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Boeing’s (BA) Q2 2025 earnings call.

![]()

Boeing (BA) is one of the world’s largest aerospace and defense companies, manufacturing commercial airplanes, military aircraft, satellites, and space systems. Best known for its 737, 787, and 777 jetliners, Boeing also supports a wide range of defense and government programs globally, including fighter jets, surveillance platforms, and secure satellite communications. With over $600 billion in backlog, Boeing is a bellwether for global trade, supply chain resilience, and international defense. The company reported $22.7B in revenue (+35% YoY) and delivered 150 commercial aircraft (the most since 2018) with strong progress stabilizing 737 and 787 production. The 737 MAX ramp hit 38/month, though rework hours remain a hurdle for FAA approval to move to 42. Certification delays for the 737-7 and -10 pushed to 2026 due to anti-ice system redesigns. Defense saw margin improvement and a $2.8B Space Force win, while BGS posted 19.9% margins with new Navy and Korean contracts. Boeing also praised new zero-tariff trade deals with Japan and the EU as vital tailwinds for global demand. Despite better-than-expected results, BA shares fell more than 4% on 7/29…

Continue reading our Conference Call Recap for BA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Daily Sector Snapshot — 7/29/25

Chart of the Day: Powell’s Tenure Ticks Down

Bespoke Wealth Management Report – July 2025

Please click here or on the link below to read our latest quarterly Wealth Management Report. You can learn more about Bespoke’s wealth management services available to investors here or by calling our office at 914-315-1248.

Below are links to prior quarterly Wealth Management Reports:

Q2 2025 Earnings Conference Call Recaps: Cadence Design (CDNS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cadence Design’s (CDNS) Q2 2025 earnings call.

![]()

Cadence Design Systems (CDNS) is a provider of electronic design automation (EDA) software, intellectual property (IP), and hardware systems that enable the design and simulation of complex semiconductors, systems, and AI infrastructure. Its tools are essential for chipmakers, hyperscalers, automotive companies, and aerospace firms tackling the rising complexity of modern designs, especially in AI, 3D-IC packaging, and high-performance computing. Cadence’s JedAI platform and agentic AI tools like Cerebrus AI Studio and Verisium set it apart in automating silicon design workflows. CDNS beat Q2 expectations and raised full-year guidance as demand surged across EDA, IP, and system design. Revenue rose 20% YoY to $1.275B, with non-GAAP EPS hitting $1.65. Hardware systems posted their best quarter ever, and IP revenue jumped 25% YoY on AI and HBM4 strength. The company launched its LPDDR6 IP and Millennium M2000 AI Supercomputer powered by NVIDIA Blackwell. Agentic AI tools continued expanding, and more than 50% of advanced node designs now use Cadence Cerebrus. While China headwinds briefly impacted bookings, strength in the US, Japan, and Korea more than offset. A $141M DOJ/BIS settlement will be paid in Q3. The stock was up as much as 10% on 7/29 after posting the triple play, its first since February 2023…

Continue reading our Conference Call Recap for CDNS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 7/29/25 – Lucky Seven?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I can’t change the fact that my paintings don’t sell.” – Vincent van Gogh

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Can we get lucky number seven? Futures on all three major indices are indicated higher this morning as the market prepares for a surge in economic and earnings-related news. On the economic calendar, the two major reports of the day are JOLTS and Consumer Confidence at 10 AM, and then after the close, we’ll get several notable earnings reports, including Starbucks (SBUX) and Visa (V). Already this morning, we’ve gotten reports from Boeing (BA), Procter & Gamble (PG), and UnitedHealth (UNH), to name a few.

In Asia, markets were mixed, with Japan down nearly one percent while China was up fractionally. Investors are still waiting for details and results from the US-China trade talks in Stockholm, but there have been no major economic reports to speak of. In Europe, yesterday’s session experienced weakness throughout the trading day as most major indices finished near their lows of the day, but this morning, there have been broad-based gains with the STOXX 600 up nearly 75 bps while Germany, France, Italy, and Spain are all up over 1%.

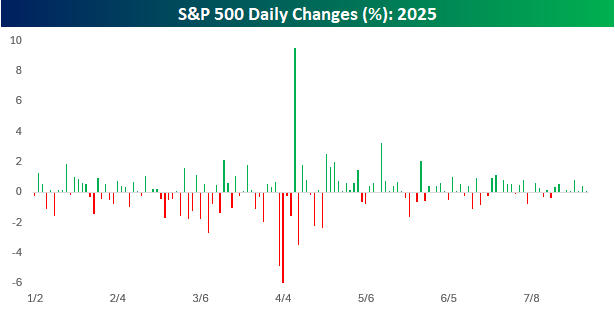

While it’s not the longest winning streak of the year, and the magnitude of the daily gains has been far from impressive, yesterday was the S&P 500’s sixth straight day of closing at a record high. That’s already impressive, but looking back at where the market was three months ago, it’s hard to even believe that the S&P 500 is anywhere near a new high! As things currently stand, this streak is tied for the longest since the six days ending last July, and if we close higher today, it will be the longest streak since the eight days ending on 11/8/21.

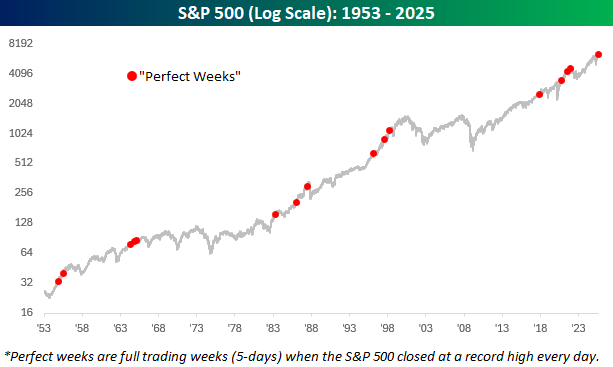

Yesterday’s positive session followed what had been a ‘perfect week’ for the market, where it not only closed higher every day, but it also closed at record highs on each one of them. That doesn’t happen often. The last time there was a full week of trading, and the S&P 500 closed at a record high on all five days, was in November 2021. Since the five-day trading week in its current form started in late 1952, there have now only been sixteen perfect weeks, which are highlighted in the chart below.

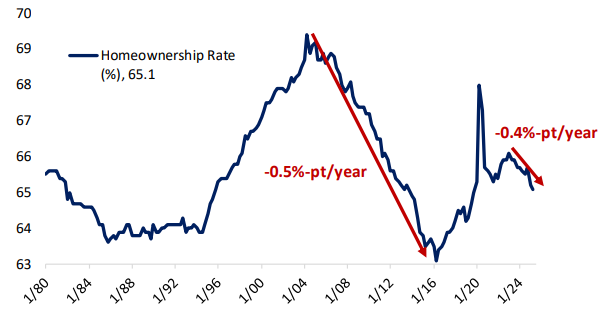

The Closer – Europe Reversal, Homeownership, Population Growth – 7/28/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look into the engulfing candles out of Germany and Sweden (page 1). We also review the latest European and American earnings (page 2) before pivoting into Census data on homeownership and vacancy rates (page 3) in addition to population growth (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!