Big Days Happen in….

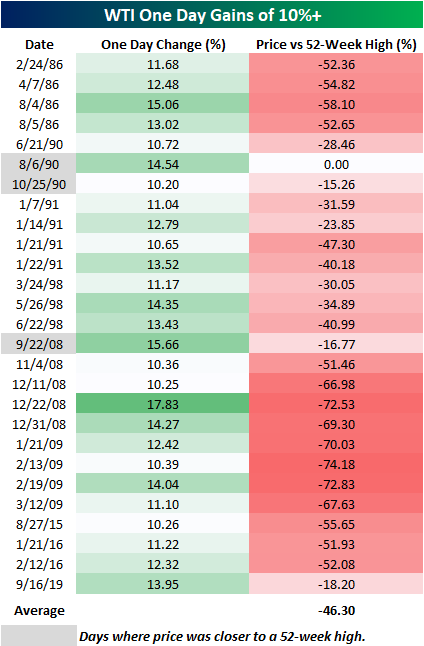

Crude oil rocketed higher today as WTI rallied just under 14% versus Friday’s close in what was the largest one-day gain since 2/19/09. There’s an old saying on Wall Street that big days happen in bear markets, and in the equity market that has tended to be the case as some of the largest percentage gains in stock market history were all during major bear markets. Looking at the largest one-day moves in crude oil shows a similar story as well.

The table below shows every one day gain of 10%+ in WTI going back to 1983, and for each day we have also shown how far crude oil was trading from its 52-week high after the one day gain of 10%+. In the case of today’s gain, WTI prices are still more than 18% below their 52-week high, and while that may sound like a lot, there have only been three other days of the 26 prior ones shown where crude oil rallied more than 10% and finished the day closer to a 52-week high than it did today (gray shaded dates). In fact, of all the days listed below, the average spread between WTI’s closing price on the day of the big gain and its 52-week high was over 46%! Talk about being in the hole! Start a two-week free trial to one of our three membership levels to receive Bespoke’s most actionable ideas.

This Week’s Economic Indicators – 9/16/19

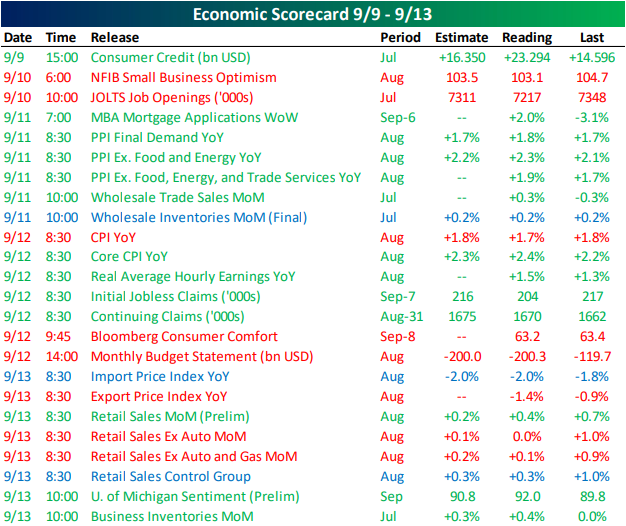

Last week was a solid one in economic data as a majority of US releases improved from the previous period or were better than forecasts were predicting. The only release on Monday was data on consumer credit for July which was much stronger than expected thanks to credit card spending. Tuesday’s JOLTS report and NFIB Small Business Optimism were both forecasted to weaken from the prior month’s release. Actual results were even weaker than these expectations. Despite the weaker JOLTS report, other labor data improved with NFIB data showing a record percentage of businesses reporting quality labor hard to find and NSA jobless claims at a 50-year low. Last week also saw multiple inflation releases including PPI, CPI, and export/import prices. While PPI was stronger than expected across the board, headline CPI was 0.1% below expectations, but core CPI remains solid at 2.4% (above forecasts of 2.3%). Export and import prices, on the other hand, remain in negative territory. Retail sales, released Friday, beat on the headline number but missed when removing auto and gas sales.

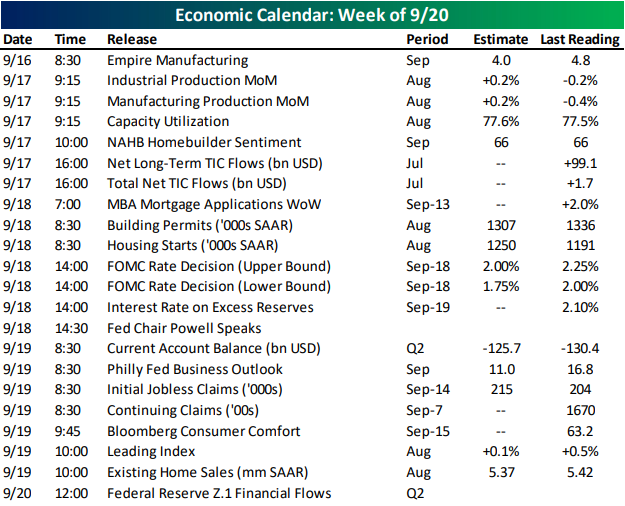

Turning to this week, it is another light start to the week with only Empire Manufacturing released today. The gauge on New York state manufacturing fell to 2.0 which is below both expectations (4.0) and the August reading (4.8). Still to come in manufacturing data this week is the Philadelphia Fed’s index (scheduled for Thursday) and Industrial Production tomorrow. As with the New York Fed’s index, the Philly Fed’s data is also expected to show weaker manufacturing activity in September which contrasts the stronger forecasts for Tuesday’s manufacturing data. A number of housing data points are also penciled in for this week including NAHB Homebuilder Sentiment, weekly mortgage applications, starts and permits, and existing home sales.

Following last week’s rate decision from the ECB, which saw rates cut in addition to a resumption of quantitative easing, on Wednesday markets will get an update on US monetary policy with the FOMC’s rate decision. The market is anticipating a second straight 25 bps cut to the lower and upper bound. Fed Chair Powell will also have a presser half an hour after the release of this rate decision. Although these Fed developments are likely to overshadow economic data, this week will also see the release of the Leading Index for August as well as the second quarter’s current account and the Fed’s Z.1 Financial Flows Report.

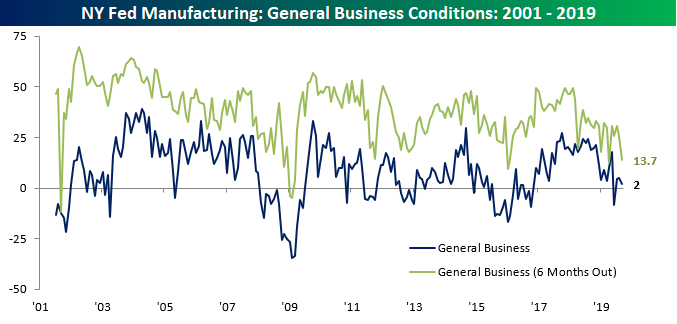

Weaker Than Expected Empire Manufacturing Report

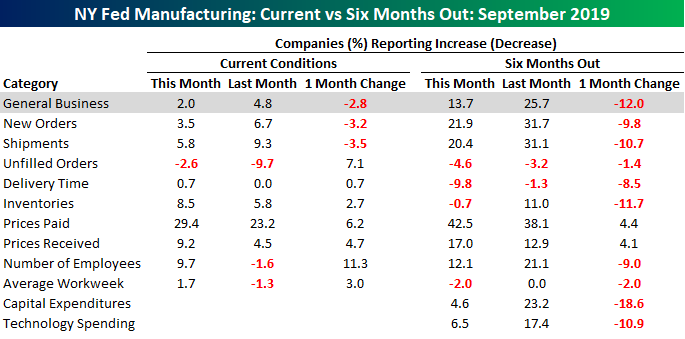

Economists were expecting a bit of weakness in the September Empire Manufacturing report, but the actual reading came in a bit weaker than those forecasts. The release of the headline General Business conditions index dropped 2.8 points from 4.8 down to 2.0. While the index of present General Business conditions only fell slightly, expectations for the next six months were notably weaker falling from 25.7 down to 13.7. While both of these indices are well off their highs from the last year or two, they also aren’t at levels that at this point would be considered dangerous for the economy.

The table below breaks down this month’s report by each of the survey’s sub-indices. As far as present conditions are concerned, New Orders and Shipments both declined, but every other category for present conditions increased, and only one (Unfilled Orders) is contracting. Looking out towards the future, though, sentiment is not nearly as positive. As shown on the right side of the table, the only two indices that increased this month were Prices Paid and Prices Received. So manufacturers are expecting weaker growth and higher inflation. That’s never a good mix!

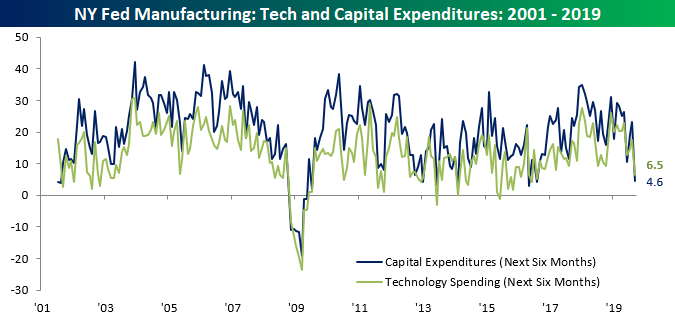

One notable aspect of the table above is the large drops in expectations for Capital Expenditures and Technology Spending. The index that tracks plans for Technology spending fell 10.9 points from 17.4 down to 6.5 in what was the largest monthly drop since May 2016. Plans for Capital Expenditures were even worse as that index fell 18.6 points from 23.2 down to 4.6. For that index, it was the third-largest decline in the report’s history dating back to 2001 and the largest monthly decline since May 2016. Here again, though, while these declines are pretty steep, they aren’t at levels that in the past have been considered recessionary. Then again, back at the onset of the recession in December 2007, both of these levels were higher then than they are now. Start a two-week free trial to one of our three membership levels to receive Bespoke’s most actionable ideas.

Bespoke’s Morning Lineup — Could Be Worse

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

With attacks on Saudi Arabian oil facilities disrupting more than 5% of global supply and oil prices surging by nearly 10%, one would have thought we would be in for a rough day in the equity market. While the opening bell still hasn’t even rung yet, US equity futures are indicating only a modest decline, so it could be worse.

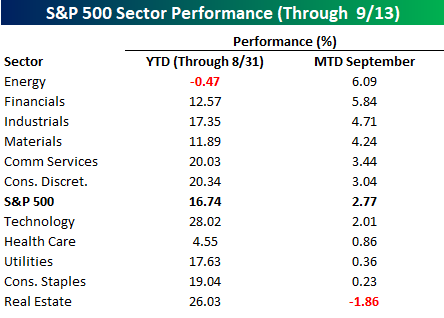

One sector that will benefit from the flaring tensions in the Middle East is the Energy sector. In pre-market trading, the Energy sector ETF (XLE) is trading up close to 5%. Interestingly enough, did anyone notice that heading into this weekend, the Energy sector was the best performing sector so far this month after being the worst performer YTD through the end of August (table below)?

Bespoke Brunch Reads: 9/15/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Vaping

‘It is time to stop vaping’: Kansas reports sixth U.S. death linked to mystery illness by Matthew Lavietes (Reuters)

Low quality vape equipment and ingredients, especially tied to THC, are being linked with sudden deaths around the country. [Link]

Vape Store Owners Are Freaking Out About Trump’s Ban by Francisco Alvarado (Vice)

Rising vape use among youth has gotten the attention of the White House, and the ban proposed this week in response has Florida vape shop owners incensed. [Link]

Energy

Saudi Arabia Shuts Down About Half Its Oil Output After Drone Strikes by Summer Said and Jared Malsin (WSJ)

Drones used by Yemeni Houthi rebels set off a series of explosions which shuttered half of Saudi oil output over the weekend. Officials hope to have the capacity mostly restored by Monday. [Link; paywall]

The Growing Market for Clean Energy Portfolios & Prospects for Gas Pipelines in the Era of Clean Energy by Charles Teplin, Mark Dyson, Alex Engel, and Grant Glazer (Rocky Mountain Institute)

New research suggests clean energy portfolios that combine various renewables with battery storage are approaching cost parity with new construction natural gas plants, and will be cheaper to build than operating gas plants by 2035. [Link]

Weird News

Google Maps shows sunken car where missing man’s body was found (BBC)

A happenstance search led to a wild find: a car that was the watery tomb of a Florida man who has been missing since 1997. [Link]

Tough-guy jaywalker glares at driver, gets instant karma by Lauren Steussy (New York Post)

Jaywalking isn’t the end of the world but holding up traffic while staring down a driver is the sort of thing that cries out for swift adjustment by the fates of fortune. [Link; auto-playing video]

Real Estate

Millennials, priced out of homes locally, shop for investment properties online by Patrick Sisson (Curbed)

Priced out of home markets, investors can access the housing market in the rest of the country via online marketplaces which make buying and selling property a breeze. [Link]

The affordable housing crisis, explained by Patrick Sisson, Jeff Andrews, and Alex Bazeley (Curbed)

Inadequate construction, rising labor and materials costs, subsidies from the government that favor homeowners, slower turnover in the housing market, and more contribute to a massive challenge for home renters. [Link]

Labor Markets

Carl Icahn moving hedge fund to Miami, whether his workers like it or not by Josh Kosman (New York Post)

Icahn Enterprises is fleeing New York, and employees that don’t want to join on the trip to Florida will be out of a job with no severance per internal memos. [Link]

UPS to hire 100,000 workers this holiday season and pay $14 to $30 an hour by Adam Shapiro (Yahoo!)

Large seasonal hiring at the package carrier this year is in-line with past years, with wages running at a robust pace as well. [Link]

Seafood Fixing

StarKist Hit With $100 Million Fine in Tuna Price-Fixing Case by Micah Maidenberg (WSJ)

After Chicken of the Sea let the government know about price fixing in canned tuna, it avoided prosecution, but Bumble Bee’s $25mm fine in 2017 pales in comparison to what the DoJ wrung out of StarKist this week. [Link; paywall]

Modern Living

The Dangers of Love in the Age of Dating Apps by Akiva Thalheim (Washington Square News)

As young people have opted in to dating apps, they’ve joined a world that is designed to be addictive and dehumanizing, an interesting parallel to the trajectory of social media sites. [Link]

Remembrance

The Worst Day Of My Life Is Now New York’s Hottest Tourist Attraction by Steve Kandell (BuzzFeed)

An essay reflecting on the evolution of how we treat 9/11, 18 years after the tragedy. Detachment, tchotchkes, and tourist intrusions on the most personal of events. [Link]

Gambling

Billion Dollar Fantasy: Inside the War Between FanDuel and DraftKings that Rocked the Gambling Industry by Albert Chen (Sports Illustrated)

An excerpt of a pending book that peels back the history of the FanDuel-Draft Kings weekly fantasy battle which eventually led to FBI and DoJ investigations. [Link; auto-playing video]

Old Asteroids

Scientists Discover New Evidence of the Asteroid That Killed Off the Dinosaurs by Robert Lee Hotz (WSJ)

Drilling on the floor of the Gulf of Mexico has provided new evidence of the asteroid 100-mile wide crater, 12 miles deep. [Link; paywall]

Indexing

JPMorgan Creates ‘Volfefe’ Index to Track Trump Tweet Impact by Tracy Alloway (Bloomberg)

An exhaustive analysis of the President’s tweets has showed a rising likelihood of having a market-moving impact in recent months. [Link; soft paywall, auto-playing video]

Old Is New

Vinyl set to outsell CDs for first time since 1986 by Will Richards (NME)

33 years ago, CD sales volumes rose above those of vinyl – already in decline thanks to 8-tracks and cassettes – but thanks to MP3s and audiophiles, that’s now reversed. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — 9/13/19

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we talk about the huge rotations under the surface of equity markets on the week. In addition to a recap of the week that was in US and global equity market price action, we take a look at global and domestic US economic data, commodity markets, and the ECB’s policy decision this week. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 9/13/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

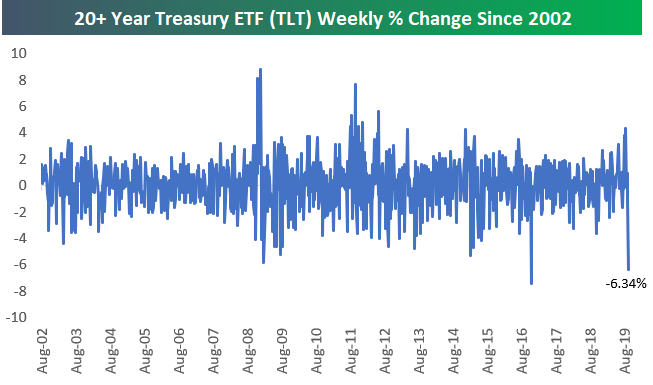

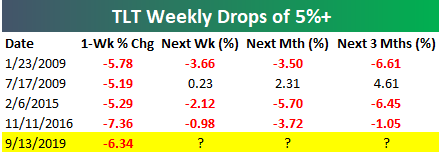

Long-Term Treasury ETF (TLT) Has 2nd Biggest Weekly Drop Ever

Outside of equities, we saw a massive move higher in Treasury yields this week and a massive drop in Treasury bond prices. For the 20+ year Treasury ETF (TLT), this week’s 6.34% drop was its second worst week on record since it began trading back in 2002.

Below is a look at TLT’s historical weekly percentage change, and we also show how TLT has performed in the weeks and months following one-week drops of more than 5% like we saw this week. As shown in the table, TLT has normally continued lower for a while following big down weeks. Start a two-week free trial to one of our three membership levels to receive Bespoke’s most actionable ideas.

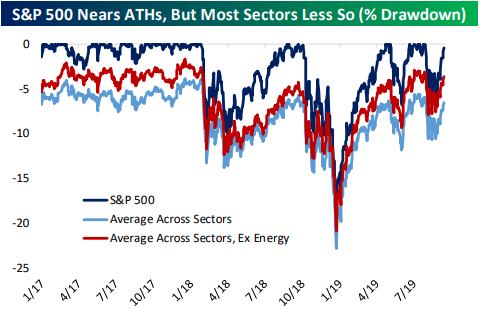

S&P 500 Nearing ATHs But Individual Sectors Not So Much

The past week has been a solid run for the US equity market as a whole. The S&P 500 continues to edge ever closer to prior all-time highs; opening today within half a percent of this level. As shown in the chart below, on average across all sectors, though, it is a little bit less optimistic. The average sector is still 6.5% below record highs. Excluding energy, which is by far the furthest (in terms of price and time) from its all-time high, the average across sectors jumps up to 3.6%. Consumer Staples and Utilities are the only sectors within 1% of their highs while the Tech sector is not far behind only 1.5% away. Start a two-week free trial to one of Bespoke’s three membership levels to receive our most actionable research.

Betting Markets and the Election

One way to keep track of the evolving Presidential primaries and general election news is the website electionbettingodds.com which shows what the betting market is predicting for upcoming election outcomes. In the charts below, we show the current probabilities of a primary and general election win for each of the various candidates (officially announced and otherwise) with a 1% or higher chance of winning. Elizabeth Warren now has a commanding lead in the Democrats’ primary with a 34.9% chance of victory with Biden and Sanders in second and third.

Where things get more interesting is to figure out which candidates have the best chance of winning the general election assuming they win their primary. For example, President Trump’s odds of winning his primary are 88.1%, but his odds of winning the general election for the Presidency are priced at 43.7%.

By dividing that 43.7% by the 88.1% chance of primary victory we can get to a 49.6% general election pricing assuming the candidate wins their primary. This conditional probability probably shouldn’t be taken too seriously, but it’s got some interesting results. Among candidates polling over 5%, Beto O’Rourke has the highest odds (80%) of a general election win if he takes the primary while other Democratic hopefuls Andrew Yang and Bernie Sanders are priced at 60%+ odds. Biden’s general election odds are at 55% if he wins the primary, while Warren — the current front runner — is at 49.9%. Notably, although Trump is close at 49.6%, no Republican has a conditional priced probability over 50% to win the general.

All of that said, these conditional relationships can be very unstable and are complicated to arbitrage, so we probably shouldn’t place too much faith in the detail of their message, but it’s still interesting to see that markets are implicitly optimistic about the electability of a candidate like Sanders or Yang relative to more mainstream candidates like Warren, Harris, or Biden. Start a two-week free trial to one of our three membership levels to receive Bespoke’s most actionable ideas.