Bespoke’s Morning Lineup – 12/4/25 – That’s What You Call Volatile

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s not the pace of life I mind. It’s the sudden stop at the end.” – Thomas Hobbes

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s very little going on in futures trading this morning as the S&P 500 and Nasdaq are both indicated to open ever so slightly higher. Treasury yields, meanwhile, are moving up about 3 bps across the curve, with the 10-year yield up near 4.10%. Crude oil is modestly higher, up 0.7%, but the big move remains in the natural gas space as prices are now above $5 for the first time in close to three years. In the metals space, gold and other precious metals are all lower, but the losses are contained at less than 1%. Even the crypto space is quiet as Bitcoin, Ethereum, and Solana are all up or down less than 1%.

In Asia, equities were mixed. While South Korea and China were marginally lower, Hong Kong finished up 0.7% while Japan surged 2.3%. Two catalysts behind the move were a strong 30-year JGB auction and a rally in tech stocks. Shares of Softbank rallied more than 9% following reports that it plans to increase its investment in OpenAI before the end of the year.

European stocks have been trading broadly positive this morning. The STOXX 600 is up 0.4%, and every major country’s benchmark index is trading up on the day. Germany is leading the way higher, up 0.8% as auto stocks rally following yesterday’s announcement from the Trump Administration that it would lower fuel-efficiency standards. Italy and the UK, however, are just barely hanging on to gains of 0.1%. In economic data, Retail Sales for the Eurozone were unchanged in October, and slightly higher than expected on a y/y basis (1.5% vs 1.4% forecast).

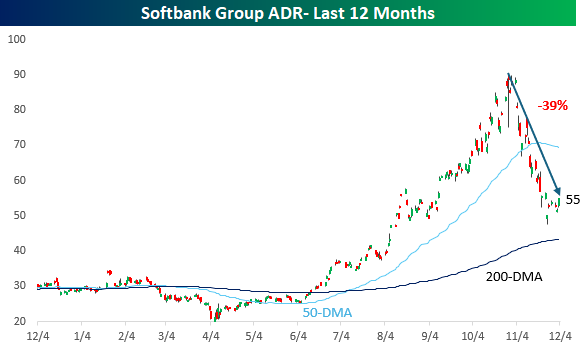

Getting back to Softbank, shares rallied 9% overnight, following a 6% gain on Wednesday. The chart below shows the performance of Softbank ADRs over the last year, and the last three months have been, to put it mildly, a roller coaster. Heading into today’s session, the stock is down 39% from its high in late October. Yet, despite that plunge, it was still 26% above its 200-DMA and 4% above where it closed 3 months ago. It’s hard to remember a stock that has plunged that much over six weeks, yet was still well above its long-term moving average and positive over the last three months.

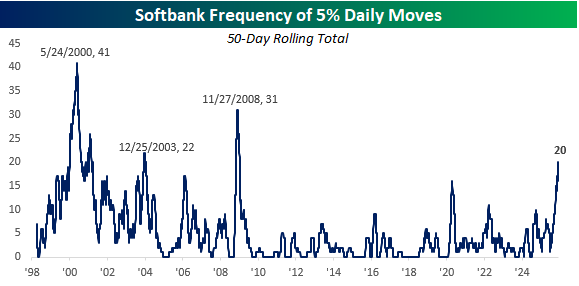

The volatility in Softbank is also evident in the day-to-day moves of Softbank stock. With last night’s 9% rally, the stock has now moved 5% or more in 20 of the last 50 trading days. To find a period where the stock saw more volatility in its day-to-day moves, you have to go back to November 2008. In the stock’s entire history, there have only been three periods when the stock had more 5% daily moves in a 50-trading-day span. The other two were in December 2003 and May 2000, when there were 41 in 50 trading days! It’s not like Softbank is a small-cap stock either. With a market cap of over $150 billion, it’s the fourth-largest stock in the Nikkei 225!

The Closer – Consumer Check, Growth vs. Value, Cold Start – 12/3/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look into a handful of baskets (page 1) in addition to the outperformance of value versus growth (page 2). Next, we offer a look into the latest string of cold weather and what that means for natural gas (page 3). After that, it’s a dive into the latest ISM (page 4) and S&P Global PMI data (page 5) before closing out with reviews of industrial production (page 6) and some earnings (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 12/3/25 – Nvidia Sits This Rally Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Sometimes reality is too complex. Stories give it form.” – Jean Luc Godard

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view this morning’s Squawk Box interview, please click the image below.

Yesterday was a true turnaround Tuesday as the S&P 500, Nasdaq, and even Bitcoin erased most, if not all, of Monday’s declines. This morning, risk assets continued to move higher as the S&P 500 and Nasdaq both look to open 0.2% higher while Bitcoin tests $93K. Gold and other metals are also up 0.5% to 1%, and even crude oil is up 1% and back above $59 per barrel. Treasury yields are also moving lower for the second day in a row, with the 10-year yield back down to 4.06%.

After being starved of economic data for several weeks, this morning we’ll get ADP Employment and PMI readings for the services sector, both current reports. In addition, the backlog of data will continue to ease as September reports covering Import Prices (8:30), Industrial Production (9:15), and Capacity Utilization (9:15) will also hit the tape.

In Asia overnight, the Nikkei rallied over 1% as Hong Kong fell 1% while South Korea added on another 1.0% after Q3 GDP came in higher than expected (1.3% vs 1.2% q/q). In Europe, the picture is more muted as the STOXX 600 gains 0.2%, and the only other countries moving up or down 0.2% or more are Italy (+0.5%) and Spain (+1.5%). Europe’s gains come as PMI reading for the services sector generally surprised to the upside. The only exception was Spain, which ironically is also the country with the largest gain on the day so far.

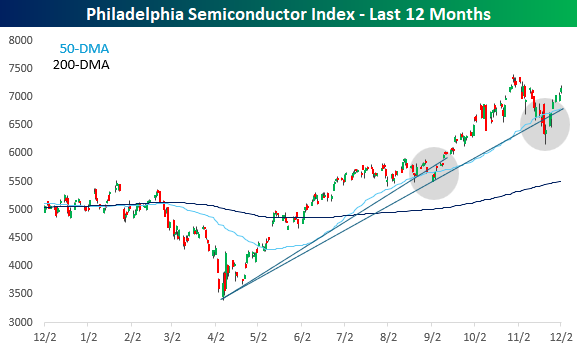

In last night’s Closer, we highlighted multiple equity baskets, which shed some light on how the economy is doing, and their performance is especially important given the lack of official economic data. Another index we follow closely as a gauge of the economy is semiconductors, which, many years ago, we branded the transports of the 21st century. When semis rally and outperform the market, it usually serves as a confirmation of a rally in the broader market and economy. Conversely, when semis falter and underperform, it serves as a red flag.

As shown in the chart below, the Philadelphia Semiconductor Index (SOX) has performed extremely well since the April low. In retrospect, it’s been a smooth ride higher, although there were two speed bumps – in September and just recently – where the trend higher and the 50-DMA was briefly violated. In the moment, both pullbacks felt concerning, but as semis recovered, the selloffs were chalked up to consolidation. The SOX isn’t out of the woods yet, but through yesterday’s close, it was less than 3% from a new high.

On a relative strength basis, semis have also bounced back nicely. In late October and early November, the relative strength of the SOX briefly made a new high, and now just seven trading days after the recent low, it’s back within a 3% range of that high.

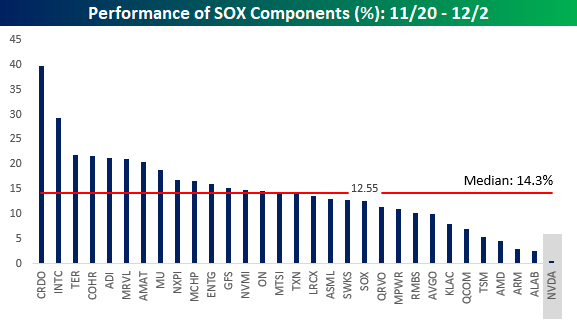

What really stands out about the rally in the SOX off the closing low on 11/20 is the breadth. Since the low, every stock in the index has traded higher, and the median gain has been 14.3%. What’s most impressive, though, is that Nvidia (NVDA) has sat out the rally with a gain of just 0.45% making it the worst-performing stock in the index. NVDA is the largest stock in both the SOX (by a wide margin) and the S&P 500, and during a period when it has essentially been flat, the two indices rallied 12.55% and 4.44%, respectively. It looks like the market can, in fact, rally without NVDA.

The Closer – Planes, Trains, and Automobiles – 12/2/25

Log-in here if you’re a member with access to the Closer.

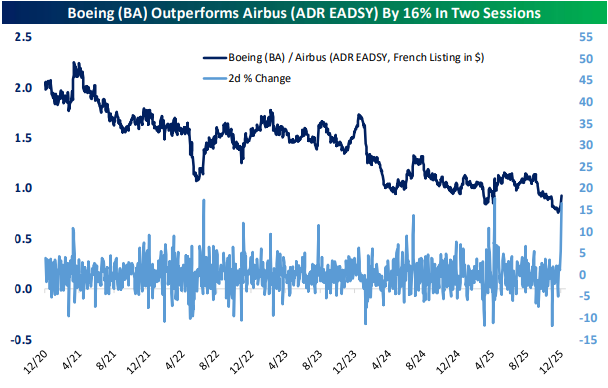

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a look into some valuation metrics for the crypto treasury company Strategy (MSTR) (page 1) followed by a look into the historic strength of Boeing (BA) relative to Airbus (EADSY) (page 2). Next, we pivot into auto sales (page 3) before closing out with a dive into a handful of baskets (page 4) in addition to the Logistics Managers Index and related stocks (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

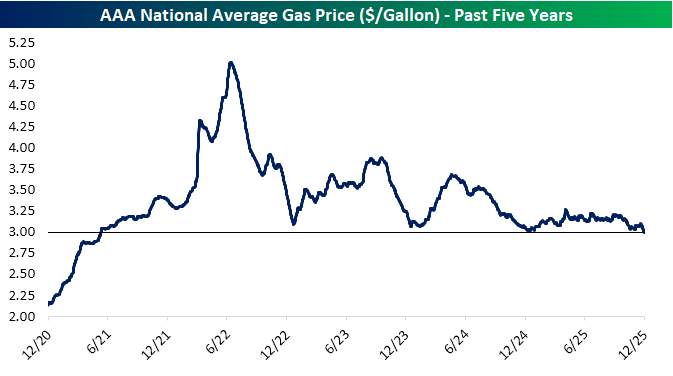

Early Christmas Gift: Gas Prices Below $3

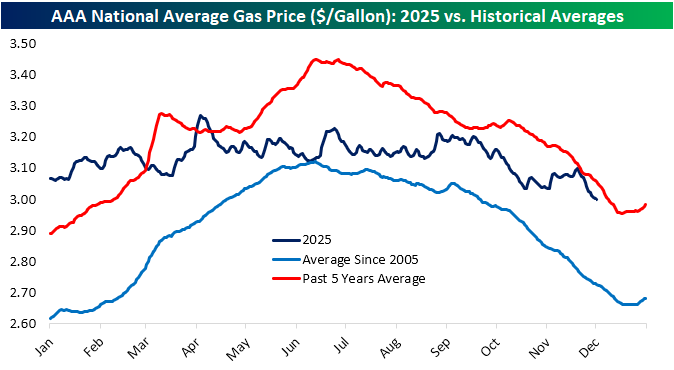

Christmas has come early for the American consumer as the national average for a gallon of gasoline according to AAA fell fractionally below $3 yesterday for the first time since May 2021. As shown below, gas prices have been muted this year with far smaller swings than has been the case for most of the past few years (more on this below). Over the past year, prices have remained in the low $3 range with the the highest price attained being $3.27 in early April. It’s now at $2.99/gallon.

The usual seasonal pattern for gas prices – which has been historically consistent with a ramp higher in the first half of the year followed by declines in the second half – has been less pronounced this year. Prices traded flat through September and have been trending lower since.

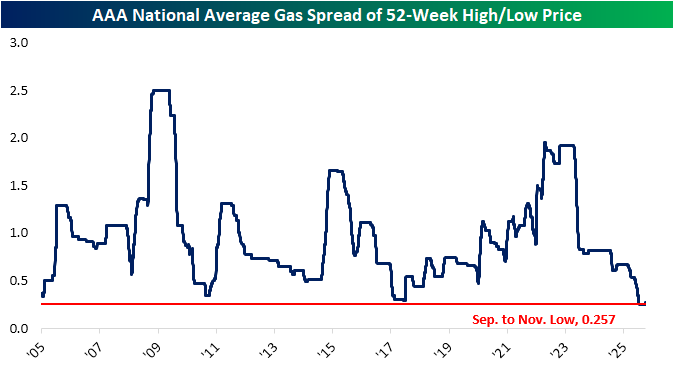

Prior to this week’s fresh low below $3/gallon, there had only been a 25.7 cent difference between the past year’s high and low price, which is the smallest high/low spread on record for the AAA series dating back to 2005.

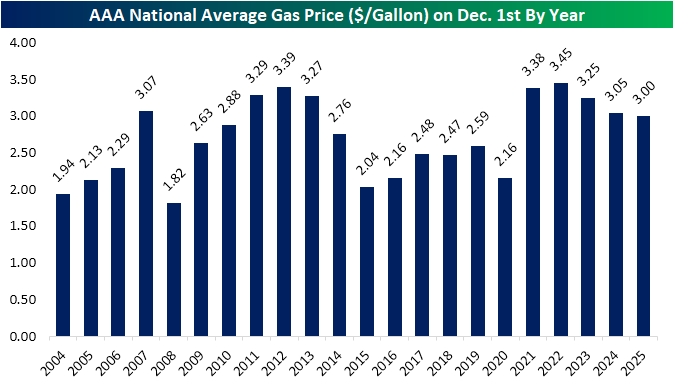

At current levels, prices are down 5 cents versus one year ago. 2025 is now the third year in a row with a lower price of gas year-over-year as of December 1st, although we saw prices in the low to mid-$2 range in the second half of the 2010s.

While the narrative for much of 2025 has been “uncertainty” for the consumer, gas prices have been extremely stable and are now back in the $2s as we enter the peak of the holiday shopping season.

Historic Health Care Relative Strength

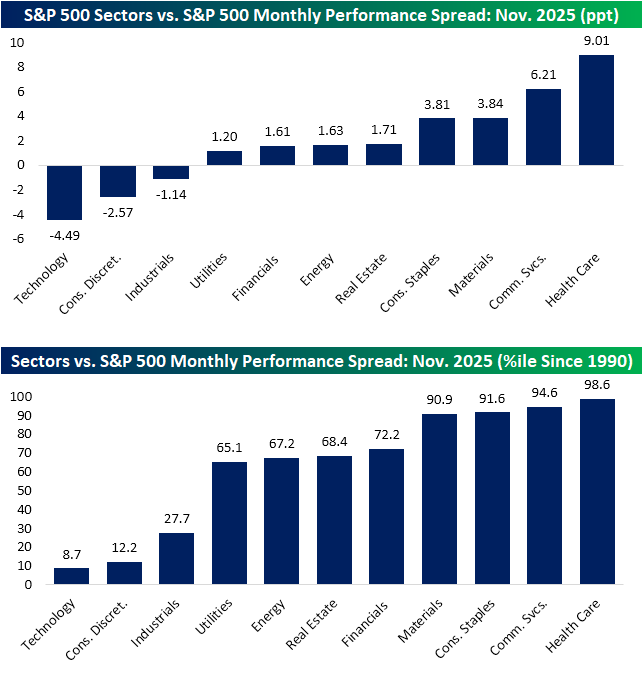

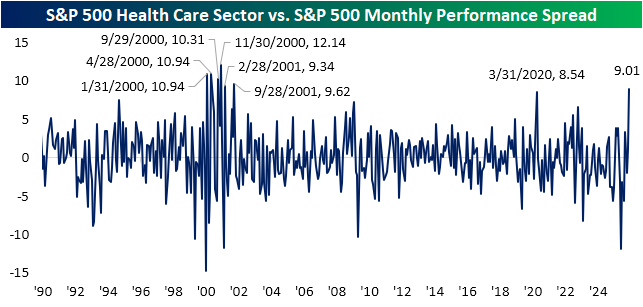

While stocks are getting off to a quiet start to December, the S&P 500 staged a solid recovery in the final week of November to manage a modest 13 bps gain on the month. Below, we show the performance spread of each S&P 500 sector versus the overall index in November. As shown, a majority of sectors actually outdid the index during the month with only Technology, Consumer Discretionary, and Industrials having underperformed. Tech in particular was a significant underperformer given it’s oversized weight; the monthly performance spread ranked in the bottom decile of all months since 1990. Conversely, Materials, Consumer Staples, Communication Services, and Health Care’s performance relative to the S&P 500 ranked in the top decile for all months since 1990. Health Care beat the S&P by nine percentage points in November, which was in the 98th decile for all months since 1990.

As shown below, it has been exceptionally uncommon for Health Care to outperform the broader market by such a wide degree. The last time the sector’s one-month outperformance was nearly as strong was in March 2020 when it outpaced the S&P 500 by a slightly smaller 8.54 percentage points. Prior to that, the only period with 9 percentage points or more like this November was a string of months in 2000 and 2001. Additionally, we would note that this latest big month for Health Care came only six months after one of its worst months on record versus the broad market; in May the sector fell 5.7% versus the S&P 500’s gain of 6.2%.

Health Care fell almost 1.5% yesterday to start off December and is again weak today. That was the sector’s first decline on the first trading day of a month since May. As shown below, that ends the longest streak of daily gains on the first day of a month since a seven month long streak ending in July 2017.

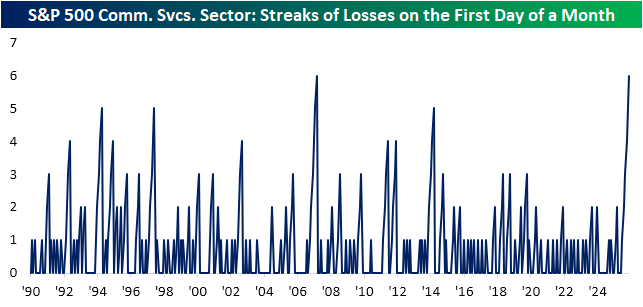

Switching over to a different sector, Communication Services also fell yesterday with an over 1% decline. That extends a losing streak of declines on the first day of a month to six months. Given the sector reshuffling in 2018, Communication Services has a different makeup today than it did in the years prior to the reshuffling. With that caveat in mind, there has only been one other period in which it fell on the first day of a month each month for half a year: October 2006 through March 2007.

Bespoke’s Morning Lineup – 12/2/25 – Code Red

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Colonel Jessup! Did you order the Code Red?!” – Lieutenant Daniel Kaffee, A Few Good Men

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Silicon Valley is abuzz this morning following reports that OpenAI CEO Sam Altman declared a ‘code red’ on Monday as competition from Google and Anthropic intensifies. To fight the threats, initiatives like an advertising model, AI agents, and a personalized “Pulse” service for individual users have been temporarily put on hold. This latest story is just another example of how quickly the currents can change in the AI space, and that no one’s lead is safe.

Going back to the internet era, remember the ‘browser wars’? Google Chrome now dominates the browser space with about 70% market share, but you may find it hard to believe that it wasn’t released until 2008, more than eight years after the Internet bubble burst! There’s still a lot of runway left in the battle for AI supremacy.

US stocks started off December with broad-based declines as the S&P 500 fell 0.5%, but the Dow fared worse, falling nearly 1% as the Nasdaq outperformed, falling just 0.38 as Nvidia’s 2% gain propped that index up. The real area of weakness, though, was in the small-cap Russell 2000, which fell 1.25%. So much for the broadening trade.

Bulls started off the overnight session looking to put up a fight as S&P 500 futures rally 0.25% while the Nasdaq looks to open 0.38% higher. Crude oil is down fractionally as it wasn’t able to trade back above $60 in yesterday’s rally, while gold falls 1%, silver plunges 2%, and platinum falls even more (-2.38%). Crypto had a rough start to December, but has bounced back over 2% this morning, trading back above $87K.

Asian stocks saw mostly muted moves overnight. The one exception was South Korea, as the Kospi rallied nearly 2% following confirmation from US officials that tariffs on exports to the US would be cut to 15%. In Europe, the tone is also positive as the STOXX 600 bounces 0.3% with Germany rallying 0.60%.

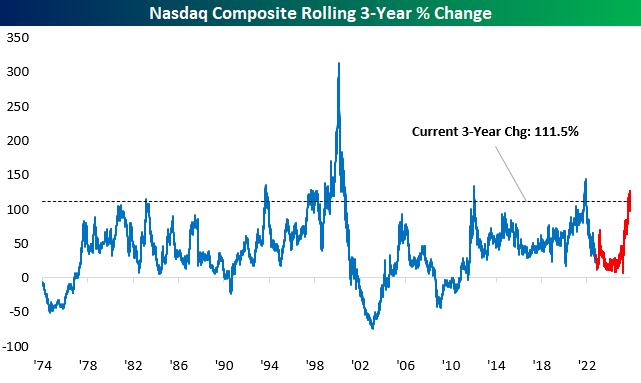

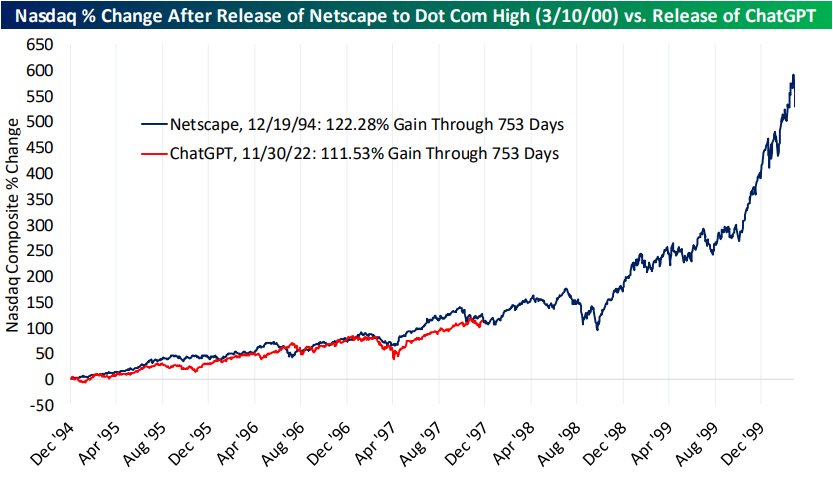

In last night’s Closer, we looked at the performance of the Nasdaq over the three years since the release of ChatGPT and compared that performance to other major tech releases of the last 50 years. Since the launch of ChatGPT in late 2022, the Nasdaq has rallied more than 100% ranking as the strongest three-year return since the period coming out of Covid and the massive tech investment to facilitate the work-from-home era. Outside of that period, the only other three-year period that was stronger was the one coming out of the Financial Crisis.

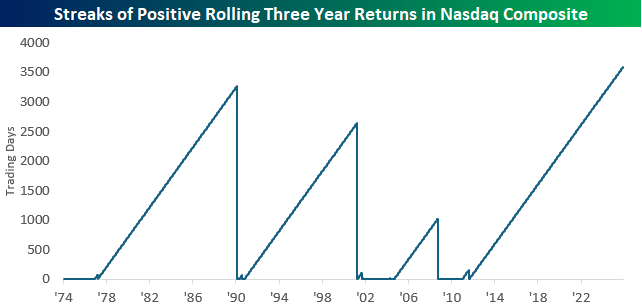

In addition to the massive rally of the last three years, what stood out in the chart was how long it has been since the Nasdaq had a negative rolling three-year return. The last time it was negative was in August 2011, just after S&P downgraded the AAA sovereign US credit rating more than 14 years ago! The chart below shows streaks of positive readings in the Nasdaq’s rolling three-year return, and at a length of 3,590 trading days, the current streak easily ranks as the longest. Besides that, three years ago the Nasdaq was under 11,500, or more than 50% below current levels. In other words, barring a large decline, the current streak of positive three-year returns isn’t going away soon.

The Closer – Year 3 of ChatGPT, KISS, PMIs – 12/1/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look into the first three years of ChatGPT (pages 1 and 2) followed by an update of our KISS basket (page 3). Next, dive into economic data in the form of PMIs and Mexico remittances (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: Deere (DE)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Deere’s (DE) Q4 2025 earnings call.

![]()

Deere (DE) is the world’s leading maker of agricultural, construction, and forestry machinery, serving farmers, contractors, and governments with everything from high-horsepower tractors and combines to precision sprayers, excavators, skid steers, and forestry harvesters. While farming equipment may not be traditionally associated with complex digital systems, DE is standing out with new products that incorporate automation, computer vision, satellite connectivity, and autonomy, giving investors a view into the digitization of global agriculture and infrastructure. The company’s platform, the John Deere Operations Center, now covers more than 500 million engaged acres. This quarter highlighted a tough Large Ag market, but better results elsewhere as tariffs surged to a $1.2B pretax headwind for FY26 and farm fundamentals stayed soft due to high global crop stocks and elevated input costs. Demand for biofuels was a bright spot, with US corn exports projected to hit all-time highs, and soybean crush volume set for a record year. Technology adoption grew nicely: See & Spray (Deere’s computer-vision spraying system that uses cameras and AI to detect weeds in real time and apply herbicide only where needed) covered 5M+ acres with ~50% herbicide savings, and autonomous tillage expanded toward commercial rollout. Construction markets improved with data center builds, infrastructure spending, and a 25% increase in earthmoving order books. As a result of a weaker Large Ag market, DE shares declined 5.8% on 11/26…

Continue reading our Conference Call Recap for DE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Market Calendar — December 2025

Please click the image below to view our December 2025 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.

Note: Due to the government shutdown, scheduled release dates are subject to change. Click here to view Bespoke’s premium membership options.