Bespoke’s Morning Lineup – 1/27/20 – A Case of the Mondays

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

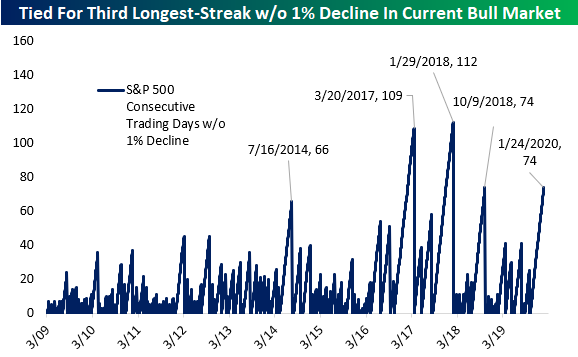

It’s going to be one of those days. US futures are down sharply this morning primarily on news of the spreading coronavirus and the Chinese government’s attempts to control it. S&P 500 futures are set to open down about 1.5% which would end the current streak of days without a 1% decline at 74.

Bespoke Brunch Reads: 1/26/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

Clearview

The Secretive Company That Might End Privacy as We Know It (DNYUZ)

An Australian technologist and app developer has launched a massive new surveillance tool designed to identify people in public places based on a complex algorithm. [Link]

Clearview AI Says Its Facial Recognition Software Identified A Terrorism Suspect. The Cops Say That’s Not True. by Ryan Mac, Caroline Haskins, and Logan McDonald (Buzzfeed News)

A controversial new company claims to have amassed a database of billions of photos which can be used to identify suspects using public sources. But the big claims – and the dystopian future they represent – are being called into question. [Link]

Metro Matters

Houston Is Now Less Affordable Than New York City by Peter Holley (Texas Monthly)

While land is cheap in Houston and wage levels are lower, reducing costs of living, the huge sprawl and lack of public transit actually makes it a relatively expensive city to live in. [Link]

NYC Moves to Ban Cashless Stores in Blow to Visa, Mastercard by Jennifer Surane (Bloomberg)

With some companies saying they will no longer accept cash at storefronts in New York City, the local government may enforce cash acceptance in order to protect access for customers that have a low income and lack access to electronic payments. [Link; soft paywall]

Eastern Europe

Belarus’ hi-tech export close to $15bn in 2019 (BelTA)

It’s unusual to think about Belarus when you mention high tech exports, but the tiny country is developing its focus on those types of goods and has made huge strides given their tiny size. [Link]

Health

98.6 Degrees Fahrenheit Isn’t the Average Anymore by Jo Craven McGinty (WSJ)

Changes in the human body over the last couple of centuries tied to more sedentary lifestyles have reduced the “normal” temperature of the human body. [Link; paywall]

Wuhan coronavirus may have been transmitted to people from snakes by Jessica Hamzelou (NewScientist)

The spreading coronavirus which started in Wuhan, China came from an animal, but the specific one in question may have been a snake. [Link]

Tired Nation: Americans Now Averaging Less Than 6 Hours Of Sleep Per Night by John Anderer (Study Finds)

While the amount of sleep every person needs varies, broad averages for the amount of sleep Americans get has made a new low. [Link]

Size Does Matter

Daily Fantasy Player Files Lawsuit Against MLB Over Astros Scandal by Darren Rovell (Action Network)

A New York daily fantasy player has named MLB as well as two teams in a cheating scandal that has rocked the league after unravelling this winter. [Link]

The IRS Decided to Get Tough Against Microsoft. Microsoft Got Tougher. by Paul Kiel (ProPublica)

An effort by the IRS to seal a massive tax dodge by Microsoft (via Puerto Rico) was stymied by a combination of administrative dancing, lawsuits, and Congressional lobbying that ultimately led to a change in the law in the software company’s favor. [Link]

Politics

The Black Swan Chart Of 2020 (Global Macro Monitor)

After a multi-decade high in voter turnout during 2018 midterm elections, voters are indicating rabid enthusiasm for the coming Presidential contest. That sort of turnout surge would create chaos for modelers and present a very different set of challenges for campaigns than low-turnout elections like 2016. [Link]

Unwired

Did someone put this Baltimore drug corner on Google Maps? by Dan Rodricks (Baltimore Sun)

An enterprising Google Maps user created a Google Maps listing for a drug corner in south Baltimore. This corner is known for its easy heroin availability. [Link]

Sonos Will Soon End Software Support for Its Older Speakers by Lauren Goode (Wired)

After 10+ years of use, the oldest generation of popular Sonos speakers are set to have their support cut off, in a move that may be poorly received by some of the company’s original customers. [Link]

Hyperbole

Guggenheim Says Central Bank-Driven ‘Ponzi Scheme’ Must Collapse by Ross Larsen, Sonali Basak, and Sridhar Natarajan (Bloomberg Quint)

The head of Guggenheim Investment Partners has decided to use some pretty ridiculous language to assess the current state of markets, but it speaks to still-restrained sentiment that people are regularly saying this sort of thing in public. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 1/24/20

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Utilities Go Up, Up, and Away

News of the coronavirus spreading further in the last 24 hours has sent a risk-off attitude throughout markets. One result of these moves has been a more distinct breakout of treasury yields as the 20+ Year Treasury ETF (TLT) has broken out of the downtrend that it has been in since the summer. At its current levels today, it is now at its highest level since October.

TLT is not the only ETF to have benefitted from a more risk-averse sentiment. As of this writing, Utilities (XLU) is the only sector ETF looking to close higher today. XLU’s rally hasn’t just been confined to today either. With interest rates falling, Utilities (XLU) have gone on an absolute tear recently. Since eclipsing its prior high just below $65 a little over a week ago, XLU has rallied roughly 5%.

Given this massive rally, breadth has been extremely strong. Now at 70.5, the 10-day advance/decline line has become very stretched. In fact, it is very rare to see these levels in the Utilities sector’s 10-day A/D line as there has only been one other period since 1990 that it was higher (June 2017) when it reached 72.14. Start a two-week free trial to Bespoke Institutional to access our Morning Lineup and Closer which will also grant access to our Daily Sector Snapshot.

Clean Energy Outshining

Looking across the ETF space, there are only a handful with dividend yields above 10%. While most high yielding ETFs are income-focused funds there is currently one outlier: the VanEck Vectors Coal ETF (KOL). This ETF focuses on equities associated with coal mining, equipment, and transportation. As investors have favored more sustainable options over fossil fuels, the deterioration in KOL’s share price over the past couple of years has elevated the yield to more than 11.5%. In other words, that high yield has come at a cost.

KOL has already fallen over 8% in 2020 and that is in the context of a 21.25% decline in 2019 and more general weakness of the energy sector. While KOL has majorly lagged the S&P 500, its underperformance is even more dramatic when compared to clean-energy focused ETFs which have gained favor as ESG investing has stepped into the spotlight as we discussed in last week’s Bespoke Report. As shown below, the Solar ETF (TAN) was actually one of the top-performing of these in 2019, notching a 66% gain and now adding another 8.21% YTD. Likewise, the SPDR S&P Kensho Clean Power ETF (CNRG) and Invesco WilderHill Clean Energy ETF (PBW) also rose twice as much as the S&P 500 in 2019. Though CNRG’s year to date outperformance versus the S&P 500 is marginal, the general trend has remained in place so far.

KOL has not only been in a downtrend over the past year but over the past week it has broken down further. That comes after a gap down in late December which broke through support that had been in place since August. While KOL has legged lower, clean energy ETFs have gone parabolic.

Overall, the price changes of these ETFs and their underlying stocks helps to illustrate the general rotation out of fossil fuel focused stocks and into those that are more climate-conscious. Some of this recent strength for CNRG and PBW comes as a result of the strong performance of electric vehicle stocks like Tesla (TSLA) and Nio (NIO) which are some of the largest holdings. Similarly, TAN owes some of its gains in recent weeks to the strong performance of its top holdings. While not as large as TSLA’s 30% gain in 2020, TAN’s top holding of SolarEdge (SEDG) has experienced a similar rally to NIO of around 15% year to date. That is after it rose 167.8% in 2019. Start a two-week free trial to Bespoke Institutional to access our Bespoke Report, Chart Scanner, custom portfolios, and much more.

Bespoke’s Morning Lineup – 1/24/20 – Semis Continue to Rip

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

What a difference a few months makes. It was only six months ago that Intel (INTC) was starting to be considered an also-ran in the semiconductor space. After a number of management shakeups and production issues in its rollout of chips using 10nm technology, INTC was losing market share to AMD, and the stock languished. When the company reported earnings last July, its stock declined 1% in reaction to the report. While that wasn’t a sharp decline, it was the fifth time the stock had reacted negatively to earnings in the prior six quarters. Not only that, but the stock was also near 52-week lows when the Philadelphia Semiconductor Index was near 52-week highs. INTC used to be the leader in the semiconductor space, but last July it seemed to be looking more like Bethlehem Steel in the early 1990s than a leading company in the technology sector.

That report last July marked what was a low point for INTC on a relative basis, though. Ever since then the stock has been rolling, and even before last night’s earnings triple play the stock was already in the midst of a multi-year breakout that will likely look even more convincing after today. In pre-market trading, the stock has been losing some steam from its overnight highs, but it is still up over 5% after what was already a strong move heading into the report.

The Closer – Yellow Brick Road, Primary Placement, Leading Away – 1/23/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with the implications of the uptick in Australian inflation expectations before turning to US politics. We show the current standings of the major Democratic candidates headed into the primaries. Next we recap the Conference Board’s Leading index and KC Fed manufacturing data. We finish with our weekly look at EIA data and an abridged version of our Fixed Income Weekly.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

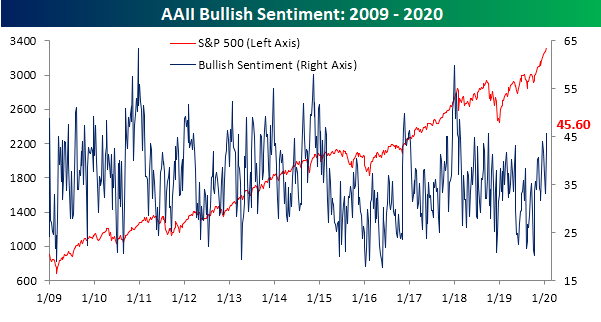

Sentiment Spikes

In the span of just two weeks, the percentage of respondents in AAII’s investor sentiment survey reporting as bullish has risen from the middle of the past few years’ range of 33.07% to 45.6% (and from 41.83% last week), the highest reading since early October of 2018. Back then, bullish sentiment peaked out just slightly higher at 45.66% before turning lower as stocks sharply sold off.

Bearish sentiment is another story. In spite of the strong bullish reading, bearish sentiment was actually lower in the final weeks of 2019 and the first week of this year. Now at 24.77%, bearish sentiment is low but still within a normal range of one standard deviation of the past year’s average of 30.04%.

Last week, we noted that AAII’s weekly reading on neutral sentiment fell below its historical average for the first time in 22 weeks. Although the week-over-week decline was fairly small at just around one percentage point this week, that slide has continued as neutral sentiment has fallen further to 29.63%. This is the first time that the sentiment reading has fallen below 30 since the first week of last year.

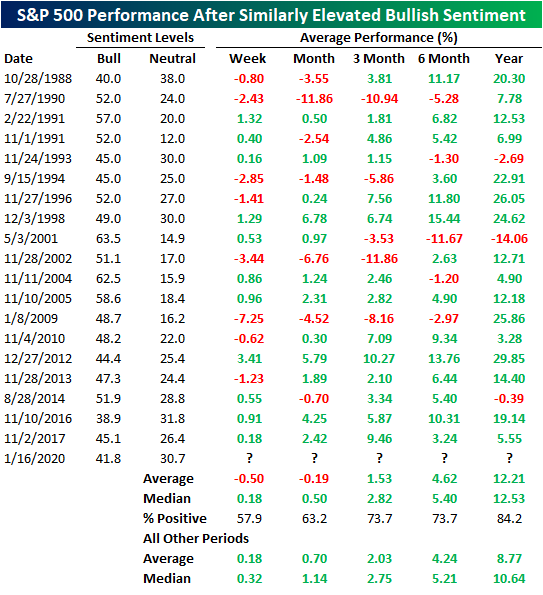

Neutral sentiment dropping so low indicates that investors have become increasingly polarized; mostly placing themselves in the bullish camp. In fact, in the past two weeks, both sentiment readings have reached fairly elevated levels relative to the past year. Bullish sentiment is now more than 1 standard deviation above the past year’s average of 33.7% while neutral sentiment is 1 standard deviation below its average of 36.26% over the past year. This was the first time this has occurred while bearish sentiment remained within its normal range since early 2018. As shown below, of the 20 prior times in the history of the survey that bullish sentiment has been similarly elevated (over 1 standard deviation above the past year’s average) while neutral sentiment is simultaneously extended below its average without having done so in the prior six months has resulted in near term underperformance compared to other periods. The S&P 500 has averaged declines in the next week and month following such readings. Fortunately, longer-term returns have been stronger and more consistently positive. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

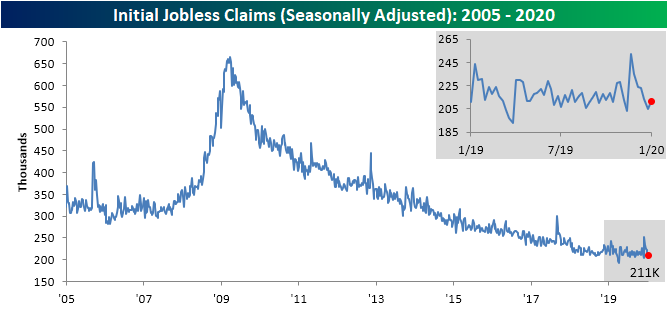

Claims Higher As Expected

Last week, initial jobless claims fell for a fifth consecutive week reaching 204K (revised up to 205K this week) which was the lowest level since November. As expected this week, claims rose off of these lows albeit by a less than expected amount. Initial jobless claims were expected to increase to 214K but instead only rose to 211K. All in all, the picture claims are sending about the labor market is a healthy one.

Although seasonally adjusted claims were up this week, the four-week moving average has fallen further. The moving average has fallen each of the past three weeks as the much higher readings from around Thanksgiving have rolled off the average. This week’s print brings the average to 213.25K which is the lowest since the end of September. Additionally, that is a drop of over 20K from the recent peak of 233.5K in the final week of 2019.

Non-seasonally adjusted jobless claims experienced a substantial decline of 71K this week as the indicator works off of its seasonal and annual peak that seems to have been put in place last week. Now at 267.6K, the indicator is still well below its average for the current week of the year since 2000.

Again, the 71K week-over-week drop in the non-seasonally adjusted number may sound like a significant move, but the large size of that move can mostly be boiled down to seasonality. In fact, since 2000 non-seasonally adjusted claims have averaged a decline of 147.9K in the third week of the year (current week). No other week of the year comes even close in seeing this sort of move.

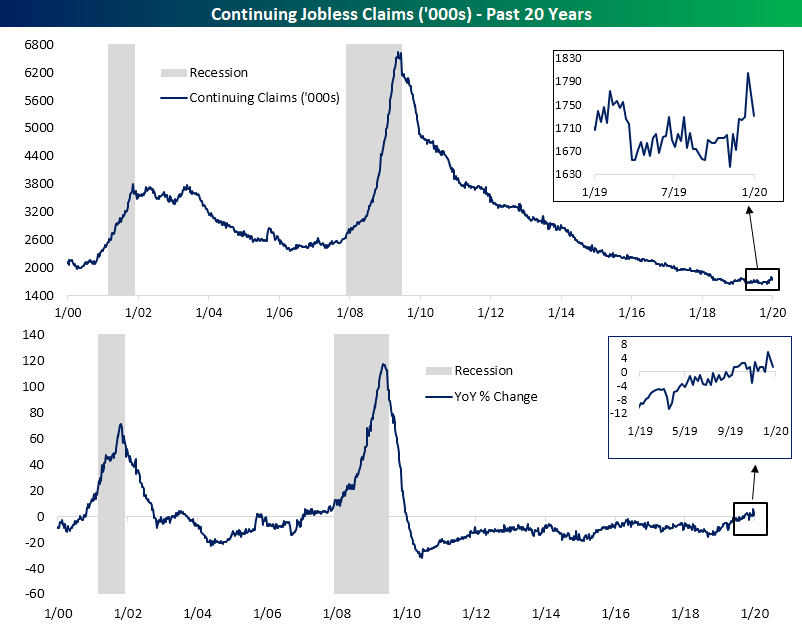

While initial jobless claims have improved in recent weeks, continuing claims have yet to fully share in the improvement. This week and last have changed that picture somewhat as continuing claims similarly were lower than forecasts, falling to 1,731K compared to the 1,750K expected reading. As shown in the charts below, just two weeks ago continuing claims totaled 1,804K which was the highest reading since April of 2018. Since then, though, they have started to fall back into last year’s range. Despite the improvement over the last few weeks, continuing claims have still been rising on a y/y basis for the first time this cycle. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – 1/23/20 – More Corona

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The coronavirus is increasingly starting to show up around the world today, and authorities are taking additional steps to contain its spread. Travel has not only been restricted into and out of the city of Wuhan but has reportedly been expanded to other cities as well. Additionally, as we type this Singapore just announced its first confirmed case. Macau has even announced that all parties and festivities tied to the New Year celebration have been canceled, and the CEO of WYNN has said that they will not rule out closing its casinos on the island. Imagine if New York city just canceled the Times Square ball drop on New Year’s Eve? Even if the outbreak is contained, already it is having an economic impact.

Remember back in 2008 during the Financial Crisis when no one wanted to go home long on a Friday and risk a negative news event coming out over the weekend? Well, that’s the case in China now as the Shanghai Composite fell nearly 3% ahead of the week-long Lunar New Year holiday. With the coronavirus continuing to spread and no one knowing how the great migration in China during this holiday period will impact the spread, it is only natural that traders looked to lighten up in what will be their last chance to trade until next Friday.

While it’s only natural, today’s drop was the Shanghai Composite’s worst one-day decline on the last day of trading heading into the Lunar New Year holiday on record. While the last few days have been a downer for Chinese stocks, the uptrend from last summer’s lows remains intact, and if the steps being taken in China to contain the virus are successful, those sales will quickly turn into buys when traders come back next week from the holiday.