BNPL Fiscal Policy Drives Gold to New Highs

Japanese stocks surged over 4% to start the week after Sanae Takaichi was elected to lead Japan’s ruling party, positioning her to become the country’s first female prime minister. Last night’s rally propelled the Nikkei above 46,000 for the first time and extended the rally from the April lows to more than 56%!

The 4% gain in the Nikkei, however, is somewhat misleading, particularly for US investors. This is because Takaichi is seen as a fiscal dove; she once called recent Bank of Japan (BoJ) rate hikes “stupid,” and one of her advisers has publicly stated the BoJ shouldn’t raise rates this fall. Given her preference for expansionist monetary policy, the Yen plunged nearly 2% against the dollar immediately following the news. As a result, the Nikkei’s 4% gain in nominal terms is nearly cut in half on a dollar-adjusted basis. Still, even a 2% rally is impressive!

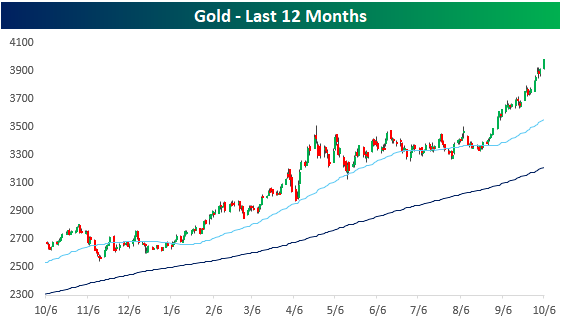

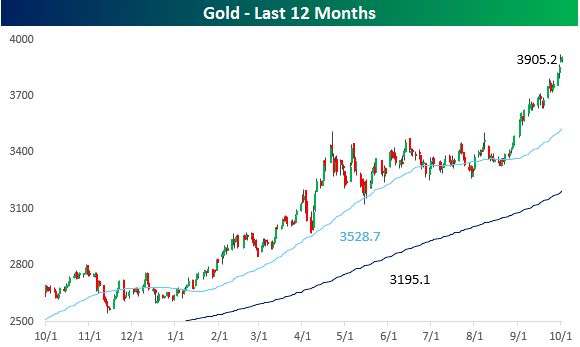

With one of the world’s five largest economies now being led by a noted fiscal dove who favors easy monetary policy and expanded government spending, investors concerned about profligacy are flocking to gold, continuing the massive breakout from its period of summer consolidation. As of early Monday afternoon trading, gold was less than 1% from crossing $4,000 for the first time.

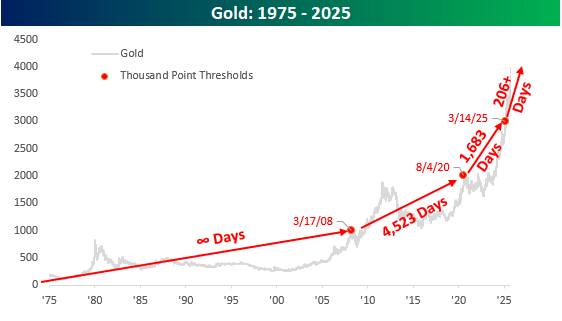

The chart below shows gold’s long-term performance, noting the first time it closed above each thousand-point threshold. While every thousand points represents a smaller percentage gain relative to gold’s overall price, it’s still worth highlighting how each one has been crossed in closer proximity to the last. It took infinity days for gold to first close above $1,000. The next thousand took 4,523 days, and then it took less than half that time to first cross $3,000. Now, less than seven months later, here comes $4,000. Simple math says that each subsequent thousand-point threshold will be crossed more quickly, and the more that governments around the world take a “buy now, pay later” approach to governing, the faster each domino will fall by the wayside.

Bespoke’s Morning Lineup – 10/6/25 – Lucky Seven

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A minute’s success pays the failure of years.” – Robert Browning

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If futures are any indication, today would be the S&P 500’s seventh straight day of gains as positive international markets, M&A news, and the government shutdown continue to provide an upside lift to equities. Overnight, the Nikkei rallied more than 4.7% for its best day since April after the election of Takaichi as the new leader of the LDP. Takaichi is a noted dove, and her advisers have already come out against a fall rate hike by the BoJ. The rally in Japanese stocks has been accompanied by rising yields and a weak yen, so despite the big gain on a nominal basis, the EWJ ETF is only up a bit more than 1%.

In Europe, the tone isn’t as positive, but the STOXX 600 is still in positive territory with a gain of 0.1%. At the country level, Germany and the UK are higher, while France, Italy, and Spain are all lower. France is notably weak, with a decline of 1.3% as PM Lecornu resigned, continuing the trend of political turmoil in the country.

Getting back to the US, the data calendar is light today and for the remainder of the week (with or without a shutdown), and earnings season won’t really start until next week, although we’ll hear from Constellation Brands (STZ) after the close today and then Delta (DAL) and Pepsi (PEP) on Thursday.

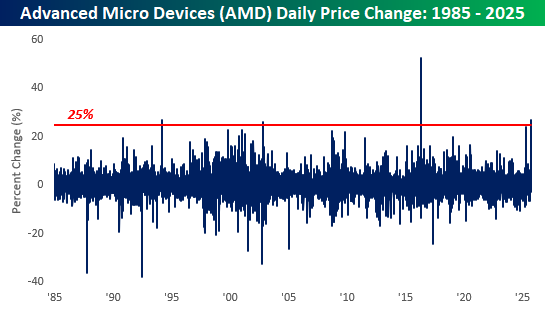

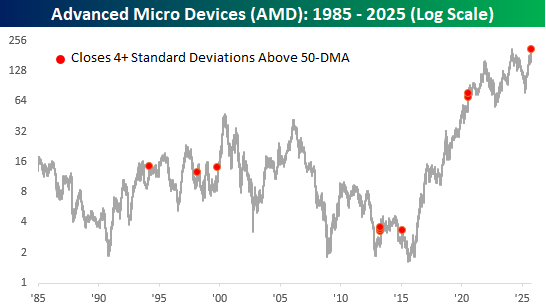

Shares of Advanced Micro Devices (AMD) are on pace to trade more than 25% higher this morning on news of its chip supply deal and equity investment with OpenAI. If AMD manages to finish the day with a gain of 27% or more (a percentage level it has reached throughout the morning), it will rank as the second-largest one-day gain for the stock since at least 1985.

With today’s gain, shares of AMD will also be trading at “extremely extreme” overbought levels. Over the last 45 years, there have only been a handful of other days when the stock traded four or more standard deviations above its 50-DMA, and if the stock holds onto these gains throughout the trading session, today would be another one.

The Bespoke Report – Equity Market Pros and Cons – Q4 2025

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q4 2025.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, sign up for Bespoke’s 50/20 special today. Our 50/20 special gets you a full year of Premium for half off, then 20% off per month after the first year. SIGN UP HERE.

Bespoke’s Morning Lineup – 10/3/25 – Bitcoin Rallies Right on Cue

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’m a greater believer in luck, and I find the harder I work the more I have of it.” – Thomas Jefferson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are higher again this morning as the S&P 500 looks to push further into record territory with a gain of 0.23%. Gains in the Nasdaq are more than twice as much as the index looks to start the session with a gain of half a percent. Oil prices are lower, trading at $61.5 per barrel, while the 10-year yield is very little changed at a very well-behaved 4.10%. Gold is fractionally higher, while silver is lower, and other precious metals like platinum and palladium are up closer to 2%. Even copper is up over 1.5%. Crypto is also having a strong morning as Bitcoin rallies more than 1% to $119K and Ether is right below $4,400.

We’re supposed to get weekly jobless claims at 8:30, but those will be delayed by the shutdown. But Challenger Job Cuts declined 25.8% year/year.

Overnight in Asia, it was a very strong session as the Nikkei was up nearly 1%, while Hong Kong, Korea, and Australia all surged over 1%. Korea surged 2.7% taking its YTD gain up to 48%! The overnight gain was driven by rallies in Samsung and SK Hynix, which rallied 4.7% and 12%, respectively, after the two companies announced an advanced memory chip deal with OpenAI. These two stocks have also been driving most of the gains for Korea all year.

In Europe this morning, we’re also seeing broad-based strength as the STOXX 600 gains 0.7% with Germany and France leading the way with gains over 1%. This morning’s strength comes as Unemployment for the region unexpectedly increased to 6.3% from 6.2%

The rally in gold just keeps chugging along. This morning, prices are once again attempting to close above $3,900 for the first time, on pace for the sixth straight day of gains and the ninth daily gain in the last ten. Investors have been looking in awe at charts like Nvidia (NVDA), Western Digital (WDC), and other hyper-growth stocks, but gold is screaming “what about me?” as its chart has also gone vertical. As of this morning, the price is more than 10% above its 50-day moving average (DMA) and 22% above the 200-DMA.

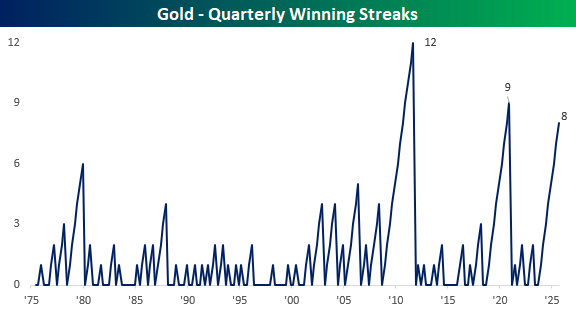

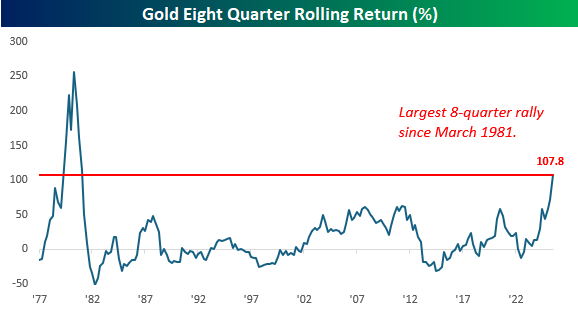

On a quarterly basis, gold is also reaching rare air. Its Q3 gain of 16.1% was the eighth straight, which ranks as the third-longest quarterly winning streak since at least the early 1970s. The longest was 12 quarters ending fourteen years ago in Q3 2011, while the second longest ended at nine in Q4 2020.

Besides the 16% gain last quarter, gold has also had three other double-digit percentage quarterly gains during the current streak. In total, gold’s price has more than doubled in the last eight quarters, and as shown in the chart below, it has been the largest eight-quarter gain since Q1 1981. Most people have literally never seen anything like it!

The Closer – TSM Premium, Loans, EV Records – 10/2/25

Log-in here if you’re a member with access to the Closer.

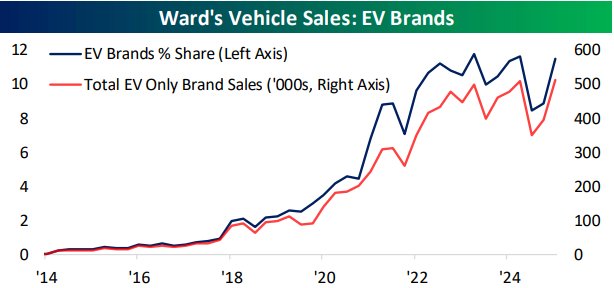

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the premium in shares of Taiwan Semiconductor (TSM) trading in the US versus abroad (page 1) followed by a dive collapses of loan and crude prices (page 2 and 3). Next up, we dive into alternative data in the form of freight truck orders (page 3), housing inventories and prices (pages 4 and 5), and vehicle sales (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 10/2/25 – Rally Rolls On

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The most common market take can be described as “person who didn’t see this coming is now 100% confident about what happens next.” – Morgan Housel

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are higher again this morning as the S&P 500 looks to push further into record territory with a gain of 0.23%. Gains in the Nasdaq are more than twice as much as the index looks to start the session with a gain of half a percent. Oil prices are lower, trading at $61.5 per barrel, while the 10-year yield is very little changed at a very well-behaved 4.10%. Gold is fractionally higher, while silver is lower, and other precious metals like platinum and palladium are up closer to 2%. Even copper is up over 1.5%. Crypto is also having a strong morning as Bitcoin rallies more than 1% to $119K and Ether is right below $4,400.

We’re supposed to get weekly jobless claims at 8:30, but those will be delayed by the shutdown. But Challenger Job Cuts declined 25.8% year/year.

Overnight in Asia, it was a very strong session as the Nikkei was up nearly 1%, while Hong Kong, Korea, and Australia all surged over 1%. Korea surged 2.7% taking its YTD gain up to 48%! The overnight gain was driven by rallies in Samsung and SK Hynix, which rallied 4.7% and 12%, respectively, after the two companies announced an advanced memory chip deal with OpenAI. These two stocks have also been driving most of the gains for Korea all year.

In Europe this morning, we’re also seeing broad-based strength as the STOXX 600 gains 0.7% with Germany and France leading the way with gains over 1%. This morning’s strength comes as Unemployment for the region unexpectedly increased to 6.3% from 6.2%

The rally in gold just keeps chugging along. This morning, prices are once again attempting to close above $3,900 for the first time, on pace for the sixth straight day of gains and the ninth daily gain in the last ten. Investors have been looking in awe at charts like Nvidia (NVDA), Western Digital (WDC), and other hyper-growth stocks, but gold is screaming “what about me?” as its chart has also gone vertical. As of this morning, the price is more than 10% above its 50-day moving average (DMA) and 22% above the 200-DMA.

On a quarterly basis, gold is also reaching rare air. Its Q3 gain of 16.1% was the eighth straight, which ranks as the third-longest quarterly winning streak since at least the early 1970s. The longest was 12 quarters ending fourteen years ago in Q3 2011, while the second longest ended at nine in Q4 2020.

Besides the 16% gain last quarter, gold has also had three other double-digit percentage quarterly gains during the current streak. In total, gold’s price has more than doubled in the last eight quarters, and as shown in the chart below, it has been the largest eight-quarter gain since Q1 1981. Most people have literally never seen anything like it!

The Closer – Shutdown, Memory DRAMa, PMIs – 10/1/25

Log-in here if you’re a member with access to the Closer.

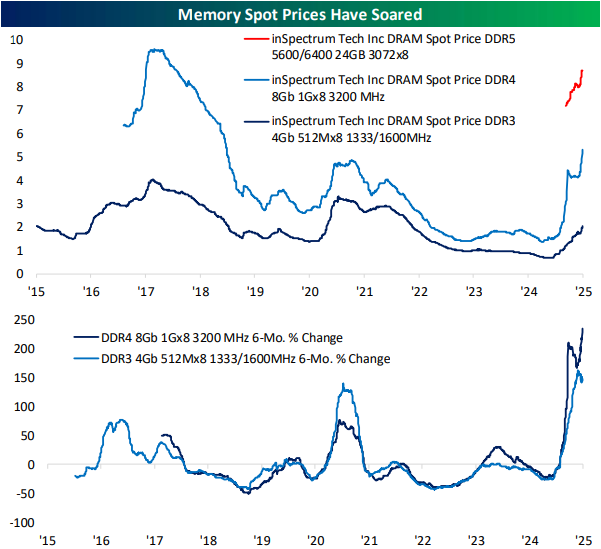

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a dive into ADP’s employment figures and a note on alternative data given the government shutdown’s effects on data releases (page 1). Next, we update the latest PMI data (page 2). Turning over to stocks, we provide some updates on performance of various baskets (page 3) in addition to a look at the surge in memory prices and related stocks (page 4). We finish tonight’s report with a look at rates (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke Market Calendar — October 2025

Please click the image below to view our October 2025 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases.

Note: Due to the government shutdown, scheduled release dates are subject to change. Click here to view Bespoke’s premium membership options.

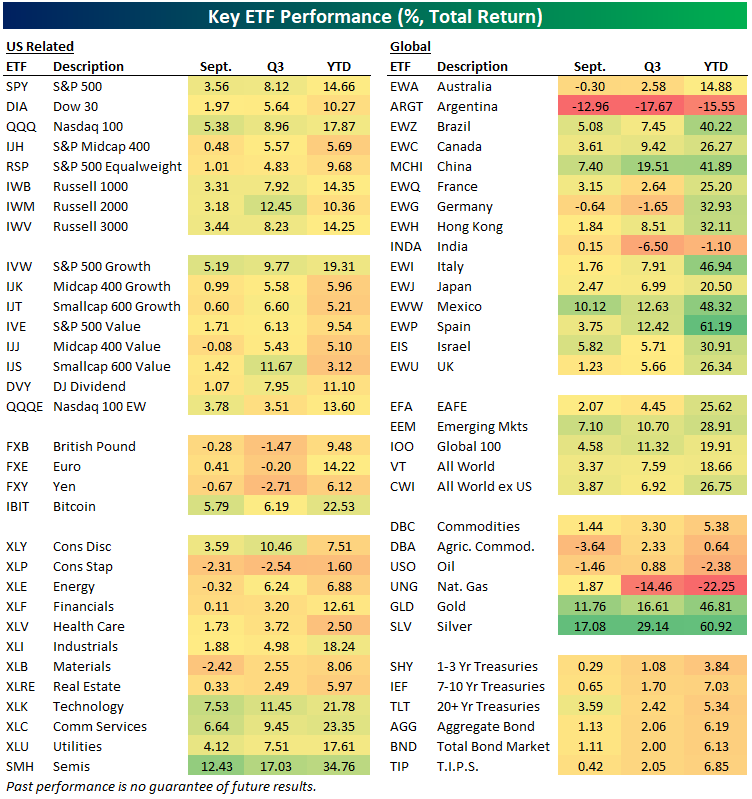

Key ETF Performance in September, Q3, and YTD

Below is a check-up on asset class performance using our key ETF matrix. For each ETF, we show its September, Q3, and YTD total return.

US index ETFs posted solid gains in both September and for all of Q3, with the Nasdaq 100 (QQQ) leading the way in September but the small-cap Russell 2,000 (IWM) leading for the full quarter. Small-cap value (IJS) did well in Q3 in particular.

Notably, the S&P 500 Equalweight (RSP) was up much less than the cap-weighted S&P (SPY) in September, as the mega-caps once again drove upside performance.

Looking outside the US, Argentina (ARGT) was the only real area of pain in September, although Germany (EWG) and Australia (EWA) were both down slightly as well. China (MCHI) and Mexico (EWW) were the two best country ETFs in September with gains of 7%+, while China (MCHI) led the way for all of Q3 with a gain of 19.5%. On the year, Spain (EWP) is still up the most at 61.2%.

Gold (GLD) and silver (SLV) were on fire in September with gains of 11.8% and 17.1%, respectively. Treasury ETFs were up slightly across the board during the month as rates fell, with longer duration up the most.

Bespoke’s Morning Lineup – 10/1/25 – Efficient Market?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When one tugs at a single thing in nature, he finds it attached to the rest of the world.” – John Muir

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss the market setup heading into the fourth quarter. To view the segment, click on the image below.

The government shut down at midnight, and futures are moderately lower this morning, with the S&P 500 and Nasdaq trading down 0.5%. All the market-related headlines, therefore, have attributed the weakness to the shutdown, and we can only imagine that somewhere out there, Eugene Fama is smashing his head against a wall. The prospect of a shutdown has been well known for weeks now, and betting markets were pricing in a near certainty of one yesterday, so if markets really were concerned and there was even a bit of truth to the Efficient Market Hypothesis, the S&P 500 wouldn’t have traded up 0.4% yesterday. So, why is the market lower? There could be multiple reasons, and the fact that it’s the first day of a new quarter, where investors rebalance their holdings, could be one of them.

Outside of equities, US Treasury yields are modestly lower, oil is down half a percent, and gold is up 1% and above $3,900 as it marches towards $4,000 per ounce. Crypto is catching a bid with Bitcoin up 2%, while Ethereum and Solana are both up 4%.

On the data calendar this morning, we got the ADP report at 8:15, which showed an unexpected decline, and ISM Manufacturing and Construction Spending will hit the tape at 10 AM. Despite the weaker ADP report, futures have seen little reaction.

In international markets, Japan finished the first day of the quarter with a decline of nearly 1% following a weaker-than-expected Manufacturing PMI reading, while India and South Korea traded up nearly 1%. Both Hong Kong and China were closed for holidays. European stocks are higher across the board, with the STOXX 600 up 0.7% despite a slightly weaker-than-expected Manufacturing PMI reading that remained in contraction territory.

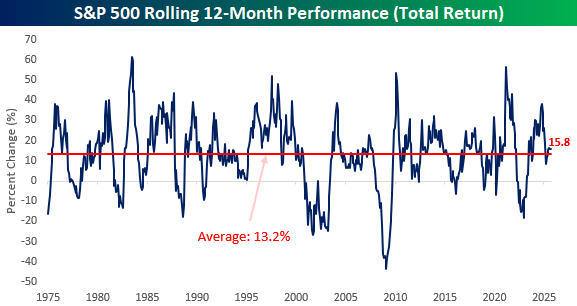

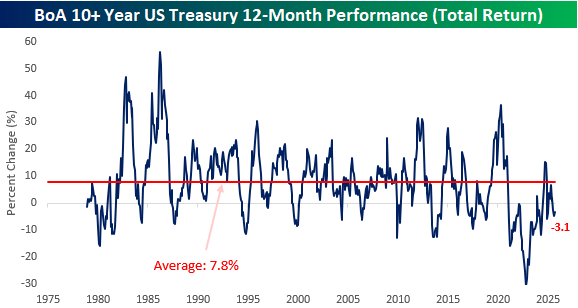

As we head into the final quarter of the year, we wanted to take a look at the 12-month moves of some major asset classes over the last five decades to see how the recent moves stack up relative to history.

Starting with equities, the S&P 500’s total return of 15.8% over the last year is surprisingly only modestly better than the long-term average of 13.2%, ranking in just the 53rd percentile relative to history. Last year at this time, the trailing 12-month return was over 35%!

Treasury yields remain stuck in their bear market. While a decline of 3% doesn’t really seem like a big deal, we’re talking about treasuries here – traditionally referred to as a risk-free asset. Not only that, but the average 12-month return has been closer to 8%, and there have only been two months in the last five years when the trailing 12-month return was better than the long-term average.

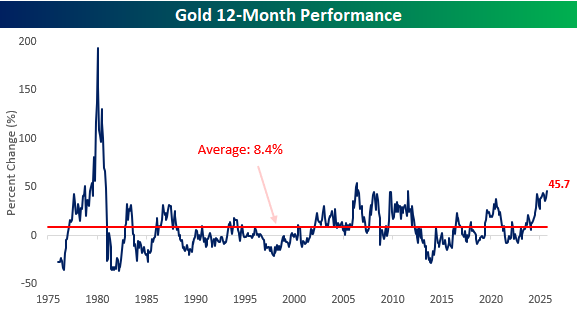

Gold is off to one of the hottest starts in decades this year, and over the last 12 months, its 45.7% gain ranks as the strongest since the mid-2000s, and the only period where there was a significantly larger 12-month gain was in the late 1970s/early 1980s.