Small Business Capex Divergences

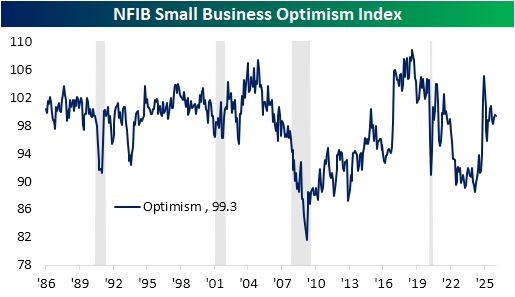

This morning, the National Federation of Independent Business (NFIB) published their monthly read on small business sentiment. As shown below, the headline index was pretty much uninteresting with a marginal drop of 0.2 points to 99.3. This index has now consistently been narrowing following the surge in response to the 2024 election, and the latest reading is not only in the middle of that post-election range, but also in the middle of the historical range, ranking in the 49th percentile.

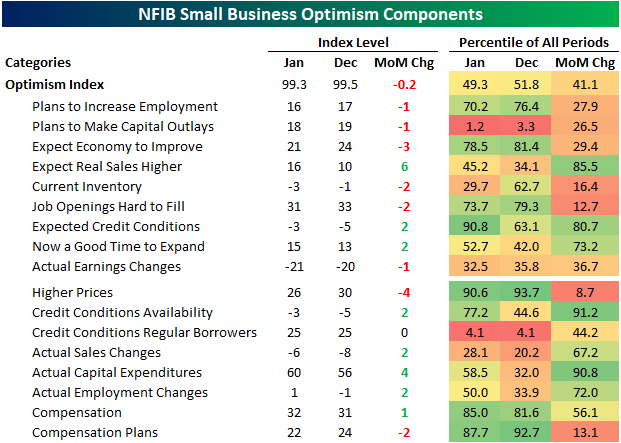

While the headline index isn’t jumping off the page, there have been some interesting details under the hood. The January drop in the index occurred on weak breadth as six of the nine inputs fell month over month. Non-inputs to the Optimism Index saw stronger breadth, with five of the eight indices rising.

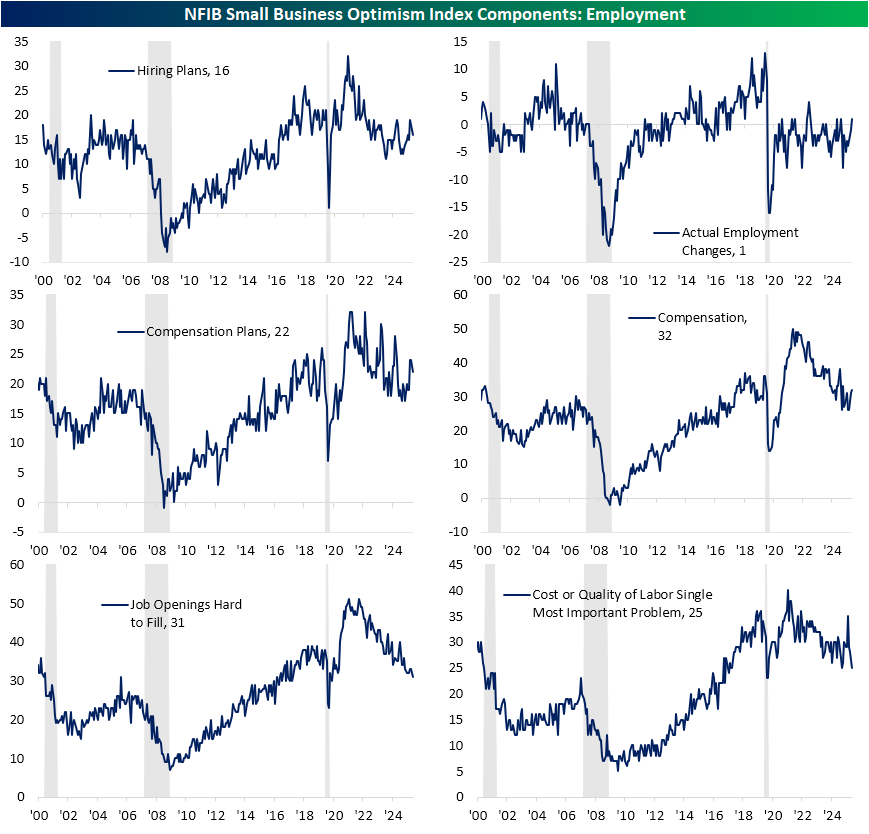

Among several topics we discussed in our Morning Lineup today, we noted how labor market indices included in the NFIB report have been trending in the right direction. In the charts below, we show a more granular look at each of the six relevant indices to this category. As shown, hiring and compensation plans did fall in January, but that was counteracted by observed upticks in actual employment and compensation. For actual employment changes, January saw a net positive reading (meaning firms saw net hiring during the month) for the first time since last April. Further, since 2020, positive readings have also been somewhat uncommon, only occurring 17.8% of the time.

While those readings were not at any sort of significant high, this month’s report saw the lowest share of respondents reporting jobs as hard to fill since July 2020. Additionally, labor was cited as the biggest single problem for only a quarter of firms, tying last May for the lowest share since May 2020.

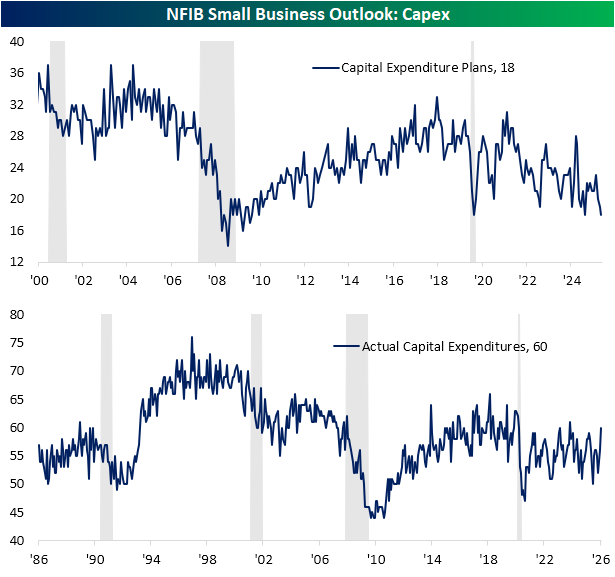

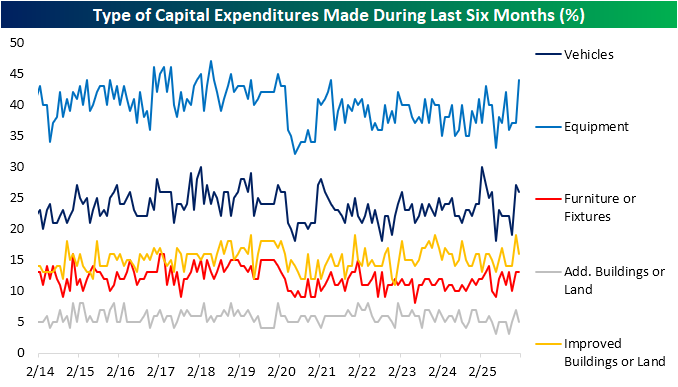

Looking to the other side of the production function, capex has seen an interesting divergence. Capex plans dropped to 18 for the joint lowest reading since 2010. Conversely, actual capital expenditures have risen sharply, hitting the high end of the past few years’ range.

In the breakdown of spending, equipment seems to be the driving force of that capex spend. That category registered its strongest reading since May 2021, while vehicle spending has also remained elevated.

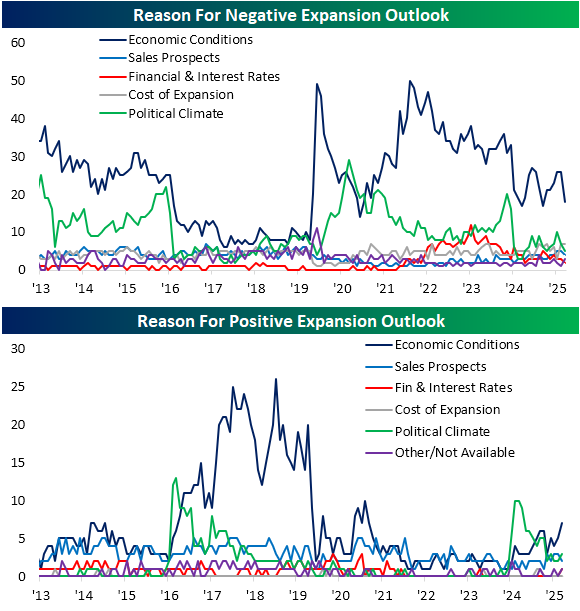

The share of firms viewing now as a good time to expand was middling versus history, as that index is in the 52nd percentile following a 2-point jump in the index to 15. As shown below, economic conditions are the predominant reason for both negative and positive expansion outlooks. While the former has seen that reason fall to the low end of its recent range, those pointing to the economy as a reason to expand hit the highest level in nearly five years.

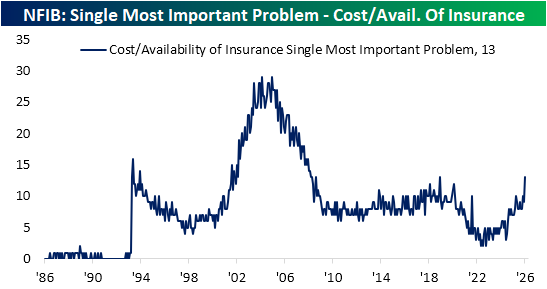

Finally, we would note that there was a 4-point drop in the index for higher prices, and the share of respondents reporting inflation as their biggest problem was unchanged at 12%. In other words, inflation did not appear to see any dramatic increase in importance. However, a related series showing the share of respondents reporting cost or availability as their biggest problem has surged up to 13%, tying December 2018 for the highest reading since August 2008.

The Triple Play Report: 2/5/26 After the Close

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

The Triple Play Report: 2/5/26 Before the Open

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

The Triple Play Report: 2/4/26 After the Close

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 2/10/26 – Software Investors Become More “Choiceful”

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We are all wrong so often that it amazes me that we can have any conviction at all over the direction of things to come.” – Jim Cramer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After two big days of gains, investors are taking some profits this morning as futures on the major averages are all down a modest 0.2% or less. Bonds are catching a bid, though, as the 10-year yield is all the way down to 4.17% after testing 4.3% yesterday. Oil prices are modestly higher, while precious metals are modestly lower, with gold and silver each down less than 1%. When was the last time each of those moved under 1% on the same day?

In international markets, Asia was positive with Japan surging another 2%, while other major benchmarks were all up less than 0.5%. In Europe, the tone is also modestly positive, with the STOXX 600 up 0.1% while no other major benchmark is up or down more than 0.3%.

In the US today, small business sentiment unexpectedly fell in January, and at 8:30, we got the latest reports on the Employment Cost Index and Retail Sales. ECI was weaker than expected, and Retail Sales (for December) came in well below forecasts.

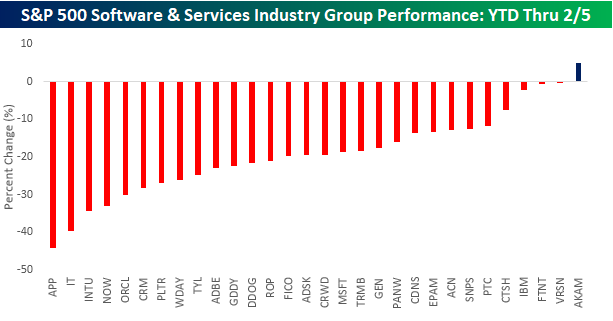

Through last Thursday’s close, the S&P 500 Software and Services Group was easily the worst-performing industry group in the S&P 500. With a decline of over 20% YTD, the group was down more than twice as much as the next closest group (Autos & Auto Parts). Over the last two days, Software has bounced back sharply, rallying more than 5%, but Semiconductors, which weren’t down nearly as much YTD heading into last Friday, are up by more than 8%!

Within the Software group, we wanted to look at which stocks led it to the downside and whether the rebound has been a reversal of the YTD trend or have investors become more discerning, trying to decipher the winners from the losers. The chart below shows the YTD performance of the industry group’s components through last Thursday’s close. Leading the way down was AppLovin (APP), which was down a staggering 44% through last Thursday. Along with APP, Gartner (IT), Intuit (INTU), ServiceNow (NOW), and Oracle (ORCL) were all down 30% for the year! In terms of winners, there practically weren’t any as Akamai (AKAM) was the lone stock in the group up YTD.

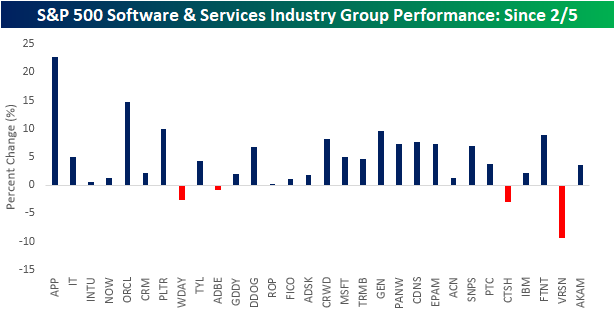

After sharp declines like we have seen in software stocks this year, when you see a bounce, it’s usually the biggest losers that bounce the most, while the stocks that held up the best don’t see nearly the juice. Based on that logic, you would expect the stocks mentioned above that were down 30% YTD to be up the most over the last two days, while a stock like AKAM would underperform. Looking at how the group’s stocks have performed in the last two trading days, that hasn’t exactly played out.

With gains of 22.7% and 14.7% since last Thursday’s close, APP and ORCL have been two of the best performers during the current bounce, but the other three stocks that were down over 30% have all either performed in line with or below the average performance of stocks in the group. At the other end of the spectrum, even after rallying YTD through last Thursday, AKAM still managed to rally in the last two trading days. Not only that, but stocks in the group that held up relatively well during the pullback this year have also outperformed on the way up.

The fact that we haven’t simply seen the biggest losers YTD bounce the most over the last two trading days, and vice versa, can be interpreted as a healthy sign suggesting that rather than indiscriminately going in and buying whatever is down the most, investors have been more discerning in their actions, attempting to weed out the ultimate winners and losers. Whether they end up being right is a big if, but it still strikes us as a healthy sign.

The Closer – Alphabonds, Flow Show, Expectations – 2/9/26

Log-in here if you’re a member with access to the Closer.

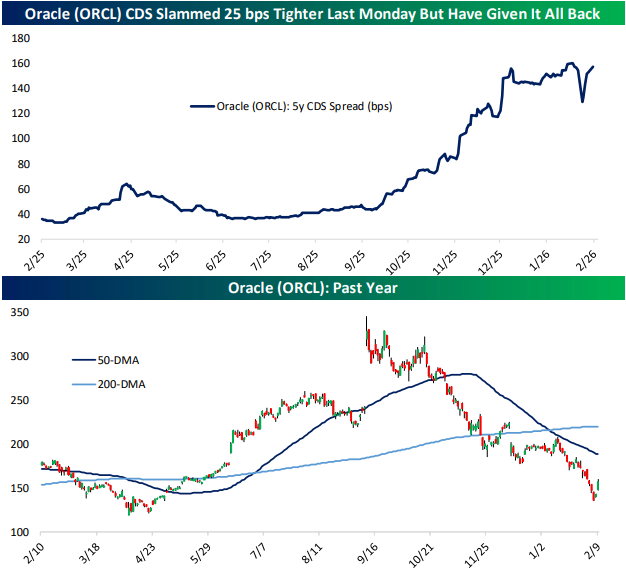

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the sale of $20bn of debt from Alphabet (GOOGL) in addition to an update on Oracle (ORCL) credit spreads (page 1). Next up, we show the bounce in AI driven names (page 2). We then recap the latest findings of the New York Fed’s Survey of Consumer Expectations (pages 3 and 4) before capping off with a review of the latest positioning data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Will Analysts Start Downgrading Software?

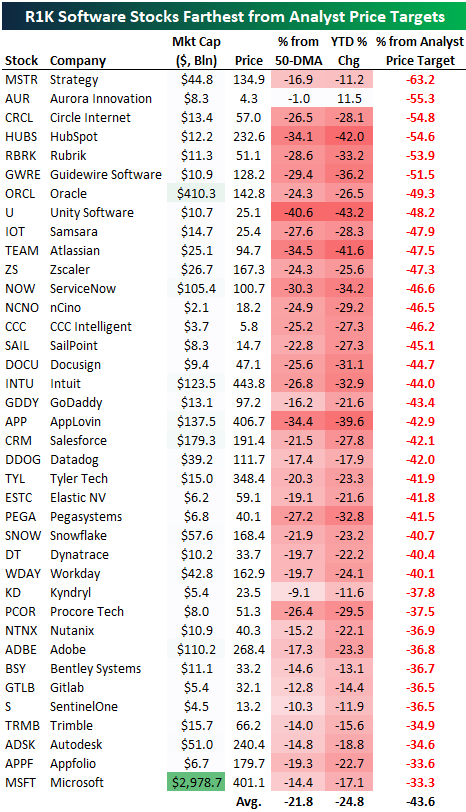

Because of the recent plunge in the group, the average software stock in the Russell 1,000 needs to gain more than 50% to get back to its consensus analyst price target! The rapidity of the decline hasn’t given analysts who cover the group time to catch up to the downside. With share prices now dramatically lower than price targets, analysts have to decide whether to hold firm or start cutting estimates.

Below is a list of the Russell 1,000 software stocks that are now the farthest below their average analyst price targets. Strategy (MSTR) is the farthest below its average price target at 63%, followed by another five stocks that are more than 50% below: Aurora (AUR), Circle (CRCL), Hubspot (HUBS), Rubrik (RBRK), and Guidewire (GWRE).

Oracle (ORCL) came into the week trading at $142.80, but analysts covering the stock still have an average price target of $282, or nearly double that level. Other large software stocks with $100+ billion market caps that are at least 33% below their price targets include ServiceNow (NOW), Intuit (INTU), AppLovin (APP), Salesforce (CRM), Adobe (ADBE), and Microsoft (MSFT).

As shown below, the software stocks listed came into the week down an average of 24.8% year-to-date and 21.8% below their 50-day moving averages.

Unless share prices have a quick V-shaped recovery, analysts will likely be forced to start lowering price targets, which would potentially act as a further headwind.

Software Getting Skinny

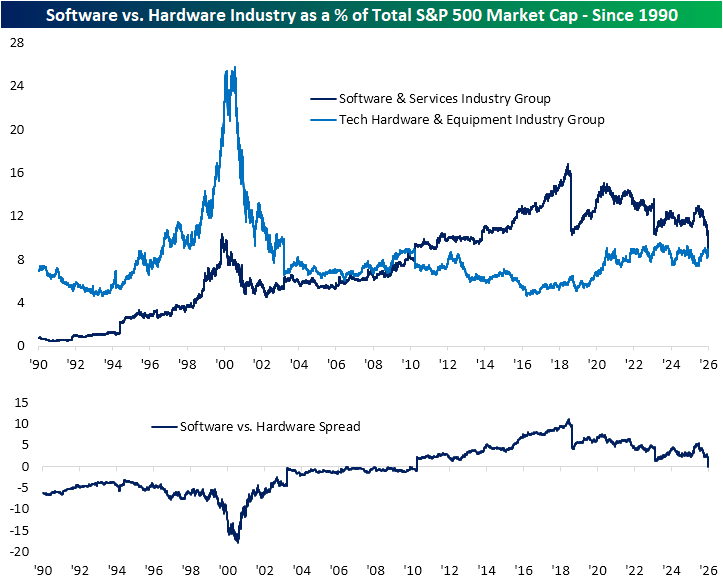

In the past couple of weeks, we have repeatedly highlighted the weakness in the software stocks. Fears that AI will pose a significant threat to the sector have caused large losses in terms of both price and weighting. In the charts below, we show the industry’s weighting in the S&P 500 versus other industries within the Tech sector. Last Thursday, the Software and Services industry saw its market cap as a share of total S&P 500 market cap fall below 9% for the first time since July 24, 2011. A significant portion of that drop has come from a dramatic move over the past several months; however, that is also in the context of a longer-term drawdown since the peak weighting in the summer of 2018, shortly before a reclassification that shifted several large-cap Tech names into other sectors.

The recent declines also put the software industry’s weighting on par with one of its peers in the Tech sector: the Tech Hardware and Equipment industry. In fact, at the low last Thursday, Software saw its weighting in the S&P 500 fall below that of Tech Hardware and Equipment for the first time since April 30, 2010. Whereas there have been steadier trends in software weighting over the long run, Hardware and Equipment has seen a relatively stable range of readings in the mid to high single digits since the early 2000s. That followed extremely elevated weights that crossed into the mid-20% range during the height of the Dot Com era. Fast forward back to today, even with the lower weighting in Software recently, Tech hardware hasn’t been picking up much.

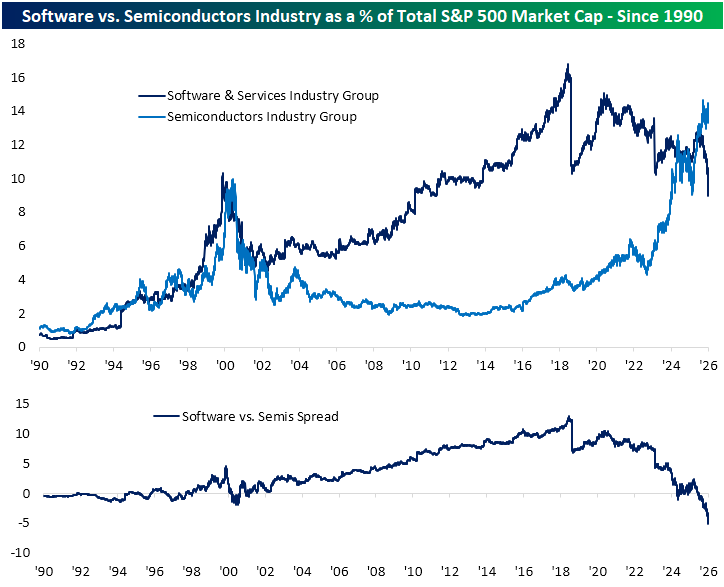

The third and final industry that comprises the Tech sector is Semiconductors, and its weight trend is the polar opposite. This is a group that has been an absolute star of the show since AI came to the mainstream in late 2022, and as a result, it is now hovering around a record share of the S&P 500’s market cap. Today, its weight is up to 14.3%, which is again still a far cry from the Tech Hardware and Equipment Industry over a quarter century ago. That also leaves software in the dust as there is now a record 5 percentage-point difference in the weightings of the two industry groups.

Bespoke’s Morning Lineup – 2/9/26 – Hangover Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“All the measures of the Government are directed to the purpose of making the rich richer and the poor poorer.” – William Henry Harrison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be appearing on Investopedia’s Express Live today at 10:00 AM Eastern. You can view the segment on YouTube or LinkedIn.

Whether it’s staying up late watching the Super Bowl last night or too much excitement from Friday’s rally that took the DJIA above 50K for the first time, US equity futures are subdued to kick off the week. The S&P 500 is on pace for a decline of 0.15% at the open, while the Nasdaq is down twice as much. Down, but nothing major.

Outside of equities, yields are higher with the 10-year yield up 4 bps to just under 4.25%. Crude oil is modestly higher, erasing earlier losses, while gold has bounced back above $5K per ounce and silver rallies 4% to get back above $80 per ounce. Crypto had a respite from selling on Friday and moved back above $70,000, but the bounce hasn’t lasted long. This morning, we’re not only back below $70K but barely hanging onto $69K.

There’s not a lot on the data calendar today, but we will hear from a few Fed officials. More importantly, December Retail Sales will be released tomorrow, the January Non-Farm Payrolls report will hit the tapes on Wednesday, and then on Friday, we’ll get CPI for January.

Asian markets took the cue from Dow 50K on Friday and kept the rally going to kick off the week. The Nikkei surged almost 4%, while South Korea rallied just over 4%. Snap elections in Japan were positive for PM Takaichi, giving her party a supermajority, which should pave the way for her to implement her high-spending growth agenda.

In Europe, the tone isn’t quite as exuberant this morning, but stocks are broadly higher. The STOXX 600 is up 0.3%, and the UK is the only major benchmark facing losses. The February Investor Confidence survey from Sentix came in higher than expected as it unexpectedly moved into positive territory.

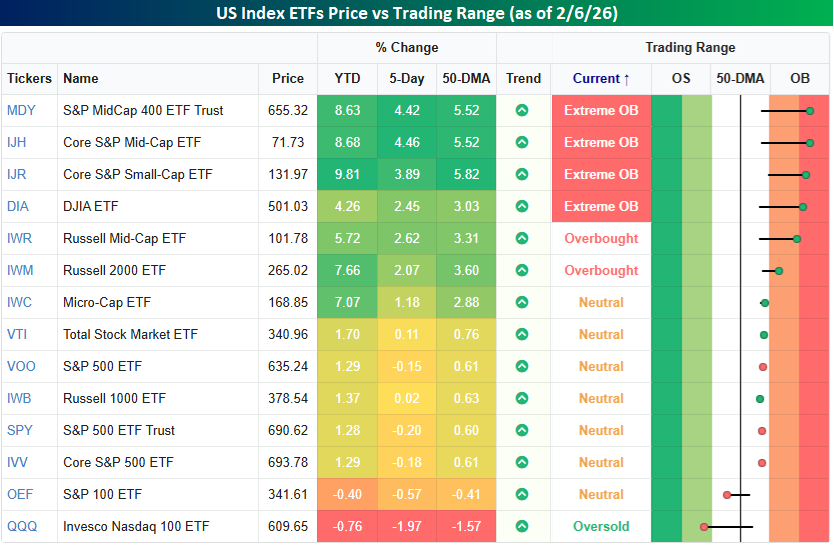

The diverging performance of small and large-cap stocks continued last week. The most overbought US index ETFs to close out the week are all generally smaller-cap and non-tech focused, while anything associated with mega-caps was down. In a week when the Dow (DIA) was up over 2% and closed at an all-time high, the Nasdaq 100 (QQQ), S&P 100 (OEF), and even the S&P 500 (SPY) were all lower. The Nasdaq 100’s 2% decline moves that index not only below its 50-DMA but also into oversold territory. At the other extreme, smaller and mid-cap indices, along with the Dow, are at various degrees of overbought levels.

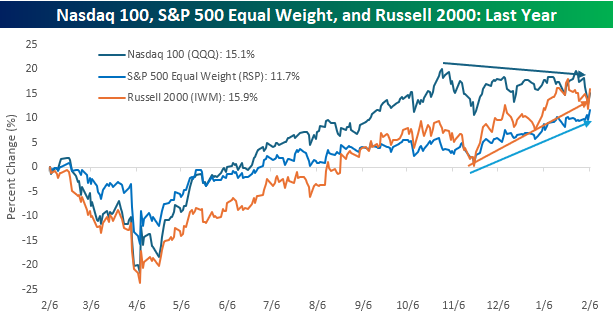

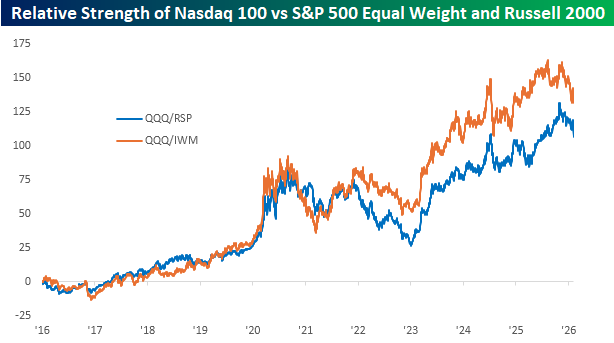

Looking at the performance of the Nasdaq 100, S&P 500 Equal Weight (RSP), and the Russell 2000 (IWM) ETFs over the last year shows an interesting shift. Since its peak last October, the Nasdaq 100 has been drifting lower while both the S&P 500 Equal Weight and Russell 2000 have rallied. The result is that the Russell 2000 is now outperforming the Nasdaq 100 over the last year, and the S&P 500 Equal Weight Index is rapidly closing the gap.

It’s been a rough three to four months for the mega-cap stocks relative to the rest of the market, but from a longer-term perspective, the recent underperformance of QQQ relative to RSP and IWM looks like much more benign as the longer-term trend remains intact. Whether that means this is just a temporary setback or that there’s much more mean reversion left in store remains to be seen, but for investors riding the mega-cap rally for the last several years are hanging on with white knuckles, hoping that, like the presidency of William Henry Harrison, this is a short stint.

Brunch Reads – 2/8/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

“You Talkin To Me?”: On February 8, 1976, Taxi Driver opened in US theaters. The movie follows Travis Bickle, played by a young Robert De Niro, who is an insomniac Vietnam War veteran who takes a job as a New York City night-shift cab driver. Most of the film tracks his routine: endless nights cruising through Manhattan, listening to his own running commentary about the city’s crime and decay, and watching people from a distance without really connecting to them. He makes an awkward attempt at a relationship with Betsy, a campaign worker tied to a presidential candidate, but his social disconnect quickly sabotages it and deepens his resentment.

As Travis becomes more isolated, he starts fixating on the idea that the city needs to be “cleaned up,” a belief that slowly hardens into a personal mission. He begins physically training, buying guns, and rehearsing violent fantasies, convincing himself that he’s preparing for something meaningful rather than slipping further out of control.

It slowly becomes clear that his need for purpose has overtaken his ability to think rationally, and he sets his sights on a decisive act that he believes will finally give his life direction. What follows forces the audience to confront questions about violence, alienation, and how easily personal despair can be mistaken for righteousness.

Consumers & Retail

As American retail store anchors fade, private clubs are taking over more commercial real estate (CNBC)

As consumer spending splits along income lines, private membership clubs are anchoring shopping centers as retailers chase affluent, high-frequency visitors rather than broad foot traffic. Developers say these clubs fill large vacant spaces, generate steady dues-driven revenue, and keep members on-site longer, benefiting nearby dining, fitness, and luxury retail. The model is spreading from coastal cities to mid-sized markets, though its success depends on local wealth, density, and whether exclusivity can be sustained without overexpansion. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.