Bespoke’s Morning Lineup – 11/20/25 – Jensen Saves the Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great ideas come from everywhere if you just listen and look for them. You never know who’s going to have a great idea.” – Sam Walton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Strong results from Nvidia (NVDA) have pushed global markets higher. The stock is trading up over 5% in the pre-market, and as a result, S&P 500 and Nasdaq futures are both trading more than 1% higher. Even Russell 2000 futures, which have no exposure to NVDA, are up over 1%. Heck, the Dow is even trading higher!

International markets were also higher overnight in Asia and this morning, with gains of mostly 1% or more. Treasury yields are basically unchanged, crude oil is back to $60 per barrel, gold is flat, and crypto assets are up at least 3%.

We’re finally getting some economic data this morning, and the main report was the September Non-Farm Payrolls report, which showed 119K jobs created versus forecasts for an increase of 50K. Despite the larger-than-expected increase, the Unemployment Rate ticked up to 4.4% versus estimates of 4.3%. More timely data on jobless claims came in at a relatively benign 220K.

In his last press conference following the Federal Reserve’s October meeting on 10/29, Fed Chair Powell made comments regarding the consumer, noting that “Data available prior to the shutdown show that growth in economic activity may be on a somewhat firmer trajectory than expected, primarily reflecting stronger consumer spending.” He then went on to simply state, “Consumers are still spending.”

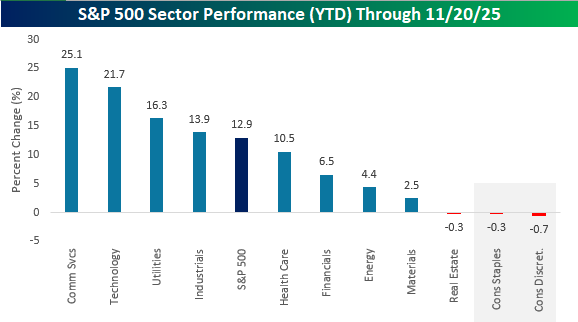

Based on data that the Federal Reserve has, consumer activity still looks strong, but the stock market seems to be sending a different message. The chart below shows YTD sector performance, and while the S&P 500 is still up close to 13% on the year, the Consumer Discretionary sector is the worst performer, and Consumer Staples is tied for the second worst. Both sectors are also two of just three sectors down on the year.

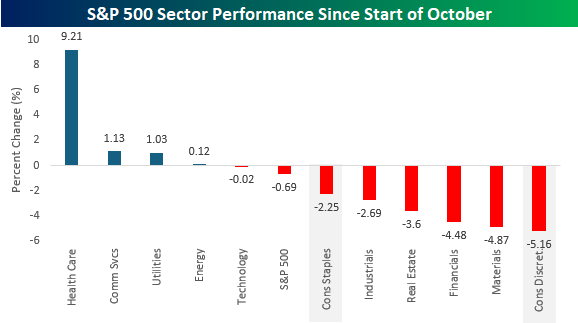

While neither consumer sector was a market leader at any point this year, both sectors have seen significant underperformance since the start of October, when the government shutdown started. While only four sectors are higher, Consumer Staples is down three times more than the S&P 500, and Consumer Discretionary is the worst-performing sector with a decline of 5.2%.

The Closer – NVDA, Morning Sell Offs, COST Low – 11/19/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a dive into the much anticipated earnings report from NIVIDIA (NVDA) (page 1) followed by an updated look at our Picks and Shovels basket (page 2). After that, we check in on how the S&P 500’s intraday pattern has shaped up (page 3) before closing out with a look at Costco (COST) which hit a rare 52-week low today (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 11/19/25 – Waiting

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we anticipate seldom occurs, what we least expected generally happens.” – Benjamin Disraeli

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After rallying off the morning lows yesterday, the major averages rallied back near the unchanged line but then drifted lower in the final hour of trading. This morning, equity futures are fractionally higher, while the 10-year yield is unchanged. Crude oil is sharply lower with a decline of 2.7% down to $59 per barrel on reports that the US and Russia may be near an agreement to end the war in Ukraine. Lower oil prices should be a welcome signal for anyone worried about inflation.

In Asia overnight, it was a mixed session with no major index up or down 1%, so maybe we’re starting to see some stabilization following a couple of days of weakness. It was a similar picture in Europe, as the STOXX 600 is up 0.1% and no major country benchmark is up or down 0.5%. Eurozone CPI increased 0.2% m/m in October, which was slightly higher than the 0.1% forecast, but core CPI was right in line with expectations, rising 0.3%.

Tom Petty said, “waiting is the hardest part,” and the market and investors can’t wait for Nvidia (NVDA) earnings after the close in hopes that it will help to get the market rally back on track. While results are widely expected to be good, if not great, the stock’s reaction will say a lot about the market’s posture heading into year-end.

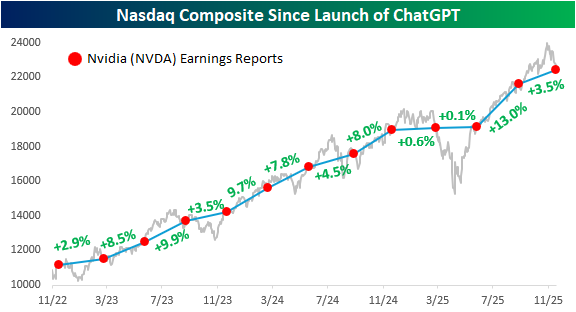

The chart below from yesterday’s Chart of the Day shows the performance of Nasdaq since the launch of ChatGPT, and each red dot indicates days when Nvidia (NVDA) reported earnings. The label between each pair of dots shows how the S&P 500 performed in that span. What’s amazing about the last three years is that in every period between NVDA earnings reports, the Nasdaq has traded higher. That kind of consistency is extremely uncommon and won’t last forever.

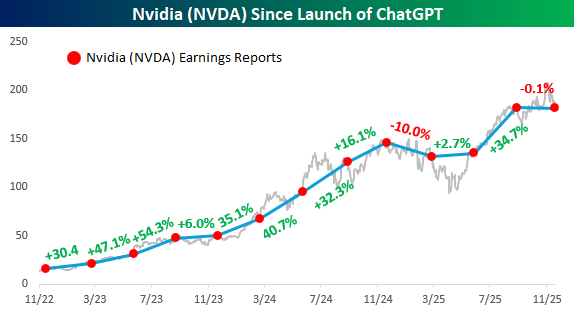

Below we show the same chart but have swapped out the Nasdaq for NVDA. While NVDA’s run has been impressive, it hasn’t traded higher between each of its earnings reports over the last three years. It fell 10% from last November to March of this year, and through yesterday’s close, it’s once again on pace for a decline, although a much more modest one than three quarters ago. If there’s one takeaway from the chart, the smooth, seemingly uninterrupted pace of gains since the launch of ChatGPT has ended.

The Closer – Jobs, CLO Quality, Credit – 11/18/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look into how jobs data is shaping up (page 1) followed by a look into collateralized loan obligations (page 2), auto ABS, and office CMBS (page 3). Next up, we dive into credit card delinquencies (page 4) and New York Fed consumer credit data (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 11/18/25 – Vibe Shift

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Bitcoin is like anything else: it’s worth what people are willing to pay for it.” – Stanley Druckenmiller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

In the world of spreadsheets, any financial model can tell you with precision what a stock or asset should be worth, but in the real world, just as the S&P 500 rarely has an ‘average’ annual return, stocks and other assets rarely trade at the price where they should trade. It doesn’t take long in the market to learn that sentiment is often just as important as fundamentals, and the last few weeks show that sentiment about what things are worth in many areas of the financial market has been shifting.

S&P 500 and Nasdaq futures are down about 0.5% with the Dow slightly weaker as a 3.4% decline in Home Depot (HD) following earnings drags on that index. The risk-off sentiment has treasury yields moving modestly lower, with the 10-year yield down to 4.10%. Crude oil is little changed but below $60 per barrel, gold is down over 1%, and Bitcoin is modestly lower after briefly breaking below $90,000 overnight (more on that below).

Asian stocks traded sharply lower in the aftermath of selling in the US yesterday. Japan and South Korea both fell over 3%, while Hong Kong was down closer to 2%, and China got off ‘easy’ with a fall of just 0.8%. The declines in Japan’s Nikkei and South Korea’s KOSPI now have those indices down over 6% from their respective highs, but Japan is still up over 22% YTD and South Korea is up over 60%, so they’re still handily outperforming the S&P 500.

Europe is also taking a defensive tone this morning as major indices in the region are all down between 1% and 2%. There’s been no real catalyst behind the move besides the overall risk-off tone across global markets.

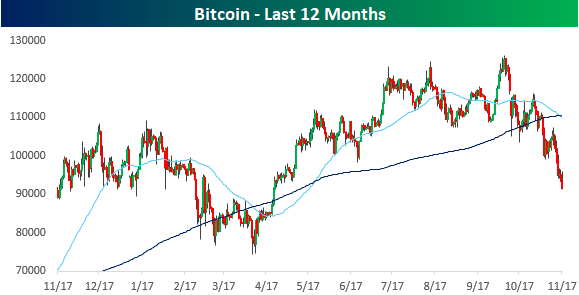

What people are willing to pay for Bitcoin today is a lot lower now than it was six weeks ago. After hitting record highs in early October, Bitcoin prices have been in free-fall, dropping more than 27% from their highs and to their lowest level since the tariff-tantrum in April. From a technical perspective, the 50-DMA has now crossed down through the 200-DMA, indicating a shift in the trend for crypto.

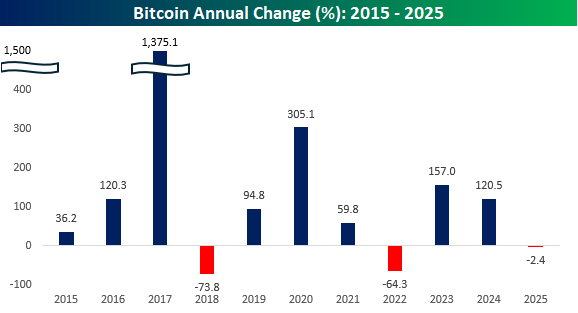

More notable about the recent weakness is that prices are now on pace for just the third down year since 2015. It’s been a painful six weeks, but if there’s any consolation, “HODLers” can take some comfort that this year’s decline is nowhere nearly as steep as the 64.3% decline in 2022 and the 73.8% decline in 2018.

With a decline of around 27% from its recent high, Bitcoin’s decline has been contained, at least relatively speaking. The chart below shows Bitcoin’s historical drawdowns from record highs, and the current decline has been tame compared to the historical norms. Since 2017, on any given day, Bitcoin’s median decline from an all-time high has been 40%.

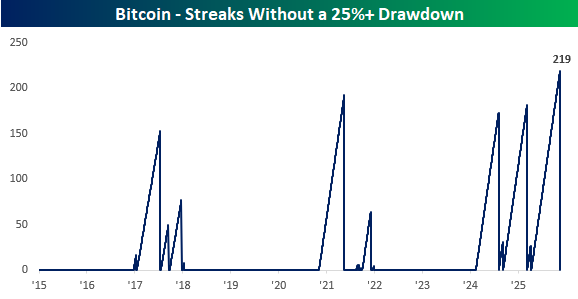

What’s notable about the recent decline is that, over the weekend, Bitcoin ended a streak of 219 days without trading in a 25% drawdown. That was the longest streak since at least 2015.

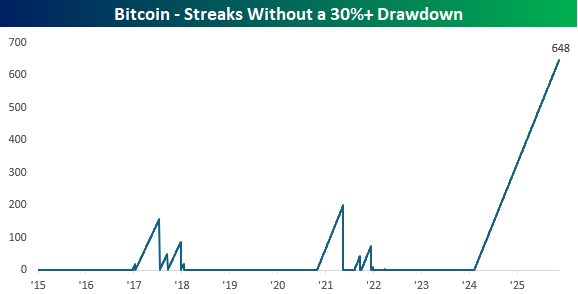

While Bitcoin’s just-ended streak without a 25% decline was historic, one could argue it’s even more overdue for a 30% decline. Through yesterday, Bitcoin has gone nearly 22 months without falling more than 30% from an all-time high, but it is getting close…

The Closer – Baskets & Bitcoin – 11/17/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with an update on major equity index technicals following today’s decline (page 1) in addition to updates on a number of baskets including those tracking momentum, unprofitable tech, private equity, travel stocks, and more (pages 2 & 3). We then review Bitcoin’s bear market (page 4) before diving into the charts of a couple hyper-scalers (page 5). After that, we provide our quarterly update of our Best of Breed Basket (pages 6 & 7). We finish with recaps of the latest economic data (pages 8 & 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

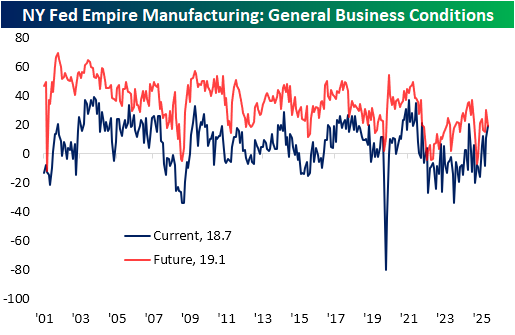

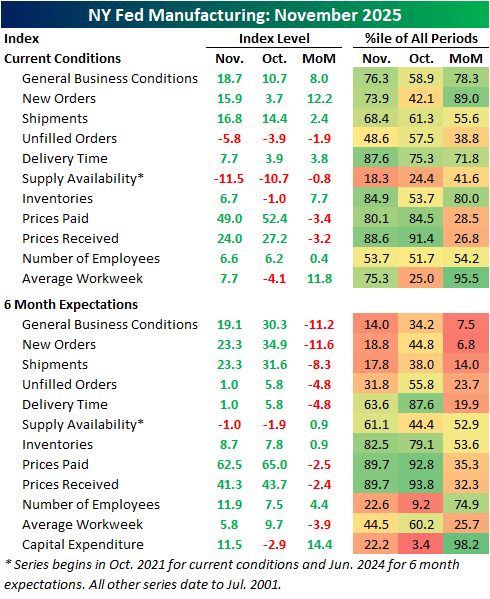

Empire Fed Rising

The first regional Fed manufacturing report covering the month of November hit the tape this morning in the form of the New York Fed’s Empire Manufacturing Survey. The headline index rose 8 points month over month to 18.7, moving the index to the top quartile of historical readings. Outside of last November’s reading of 20.2, this was also the highest reading in the index since April 2022.

Breadth in this month’s report was solid, with six of ten categories rising month over month while four declined. Of the decliners, both price indices moderated. New orders picked up materially, as did both employment indices. Current condition indices are mostly solid now, with only two in contraction (unfilled orders and supply availability), and those same two indices are also the only ones below their median historical readings.

Six-month expectations, on the other hand, leave room for improvement. Across the board, only five expectation indices are above their historical median, with the two price indices the most elevated, just shy of top decile readings. The headline index experienced a double-digit drop in November. In other words, the report showed optimism about current conditions but uneasiness for the months ahead.

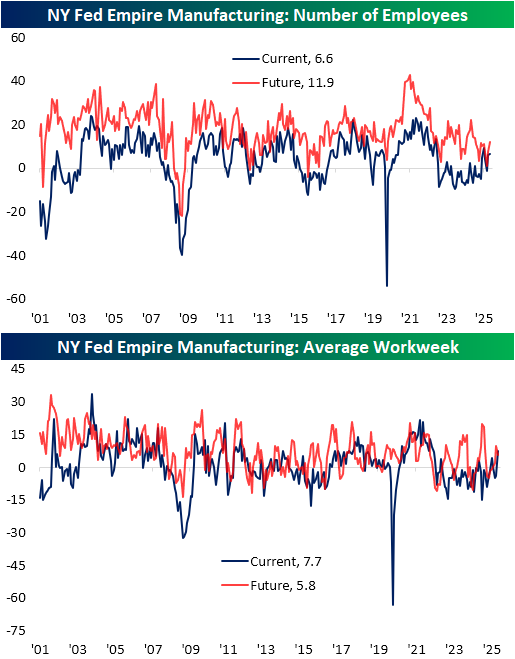

One of the stronger categories for current conditions was employment. Number of employees wasn’t much to write home about, as the current conditions index rose a modest 0.4 points to 6.6. Expectations were also higher, reaching the most elevated reading since January. Average workweek was much stronger as the index surged from contractionary territory, up 11.8 points to 7.7. Put differently, in just one month, that index went from the bottom to the top quartile of historical readings. In fact, the index for current conditions is now the highest since May 2022.

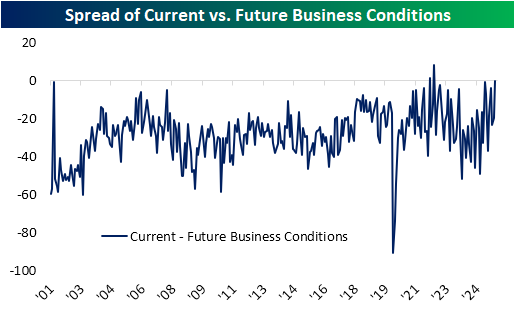

Circling back on the spread between current conditions and expectations, it was a weird month as current conditions improved and expectations deteriorated. Below, we show the spread in those readings for the headline index. As shown, optimism has been the historical norm, as positive spreads (current conditions stronger than expectations) have been extremely rare. In fact, it’s only happened twice, the first in April 2022 and the second a few months later in July 2022. While the November reading wasn’t positive, it came close with the third-highest reading on record at -0.4.

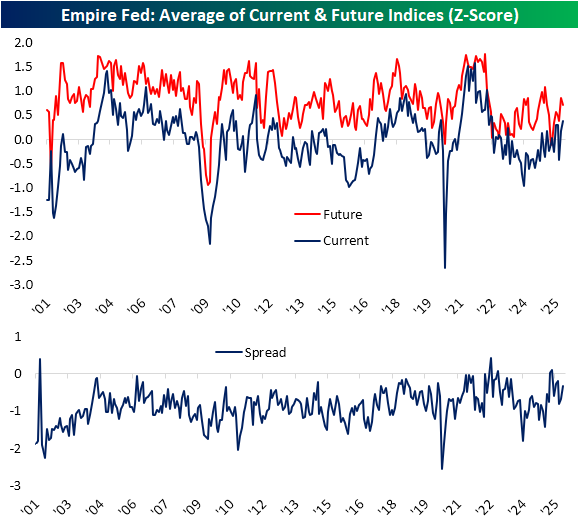

Standardizing and averaging across all categories, the spread between the two is less extreme. Again, current condition indices are solid at the strongest levels since the summer of 2022 while expectation indices were down slightly this month. Taken as a spread, there were higher readings as recently as three months ago, including a rare positive reading in April and May. Regardless, the move upward in November still ranks in the 90th percentile since the start of the survey in 2001.

Bespoke’s Morning Lineup – 11/17/25 – 11?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s no such thing as simple. Simple is hard.” – Martin Scorsese

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s looking (for now) like another positive start to the week as S&P 500 and Nasdaq futures are indicated higher. We say for now, because the tone was much more positive before the sun came up on the East Coast. In fact, futures on the Dow have actually moved into negative territory while the Nasdaq’s gain has been whittled down to 0.25%. The primary driver of the Nasdaq’s gain is a 4% rally in Alphabet (GOOGL) following news that Berkshire Hathaway acquired 18 million shares during Q3.

After moving up as high as 4.15% on Friday, the 10-year yield is down over 3 bps to 4.11%, crude oil is flat and barely hanging on to $60 per barrel, gold is modestly lower, and Bitcoin is higher, reversing overnight weakness that took its YTD performance negative for the year.

The week started on a mixed note in Asia. South Korean stocks rallied close to 2% as Samsung and SK Hynix rallied, but Japan and China both traded lower on geopolitical concerns after China advised citizens not to travel to Japan following comments made by the new Japanese PM Takaichi, regarding Taiwan. JGB yields in Japan also moved higher as the 20-year yield hit its highest levels since 1999.

European stocks started off the week higher but have reversed lower since the open and are now down across the board as the STOXX 600 falls 0.5%, led lower by a 1% drop in Spanish stocks.

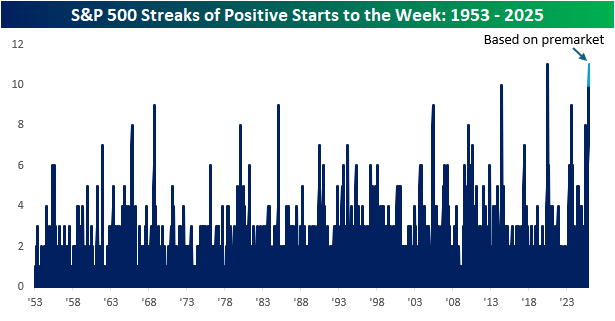

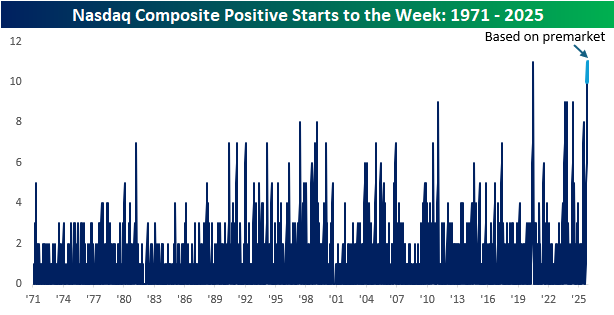

Futures don’t look as positive as they did earlier, but as of this writing, they’re still higher, and if that pace remains the case, it will be historic for both the S&P 500 and Nasdaq. Heading into this week, both indices have had positive returns on the first trading day of the week for ten straight weeks, which was one short of each index’s respective record streak from July 2020 coming out of the Covid crash lows.

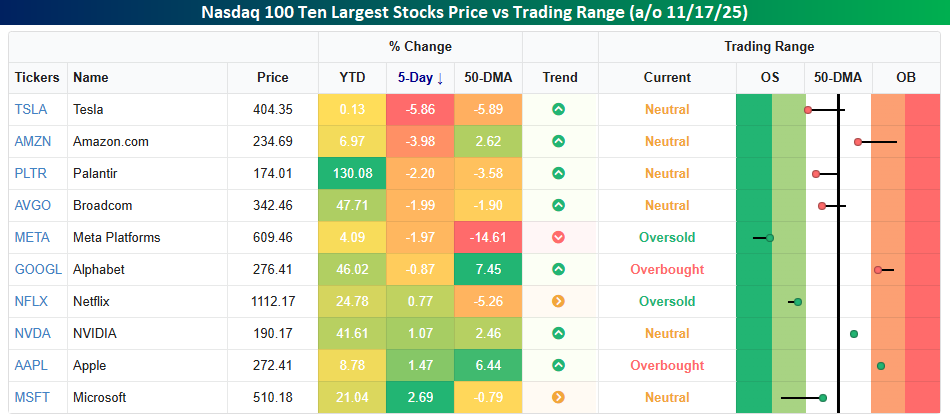

Within the Nasdaq, there’s been some bifurcation in returns lately. On a YTD basis, the ten largest stocks in the index are all still up, but the range of returns varies widely. Palantir (PLTR) easily leads the group with a gain of over 130%, but three others in the top ten are still up at least 40% YTD. Last week, though, returns were much more scattered. Led lower by Tesla’s (TSLA) decline of nearly 6%, five of the ten largest stocks in the index were basically down at least 2%. At the other end of the spectrum, Microsoft (MSFT), Apple (AAPL), and Nvidia (NVDA) were all up over 1%.

Relative to their respective 50-DMAs, the ten largest stocks are also all over the place. Meta (META) is an extreme as it closed out the week nearly 15% below its 50-DMA, but TSLA and Netflix (NFLX) are also more than 5% below their 50-DMAs as well. Meanwhile, two stocks in the S&P 500 – Alphabet (GGOGL) and AAAPL) – are more than 5% above their 50-DMAs.

Brunch Reads – 11/16/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Fed’s First Steps: The Federal Reserve officially opened on November 16, 1914, marking the start of a new central banking system designed to stabilize the US economy. Its creation came after decades of financial panics, especially the Panic of 1907, which showed how vulnerable the country was without a central authority to manage money and support banks during stress.

At the time of its opening, the Fed’s main job was to provide an “elastic currency,” act as a lender of last resort to banks, and make the financial system less prone to sudden collapses. The twelve regional Reserve Banks began issuing Federal Reserve Notes and offering short-term lending to member banks, giving the country its first coordinated monetary framework.

Over the years, the Fed’s responsibilities expanded well beyond its original mandate. The Great Depression pushed it into more active monetary policy, post-war reforms gave it a dual mandate of stable prices and maximum employment, and modern crises, from the 1970s inflation period to 2008 and the pandemic, led to new tools like open-market operations, emergency lending programs, and large-scale asset purchases.

Today, the Federal Reserve plays a central role in the global financial system. It sets interest rates, regulates major banks, oversees payment systems, and steps in during periods of economic or market stress. Even with its expanded powers, the core purpose remains the same as it was on day one: to keep the US financial system stable and functioning during good times and bad.

Education

Harvard Says It’s Handing Out Too Many A’s. Students Are Fighting Back. (WSJ)

Harvard is facing a blowup over grade inflation, with a new report saying too many students are getting A’s and not enough real evaluation is happening. Students say they’re already stretched thin and feel blindsided by the idea that their hard-won grades are suddenly a problem, while faculty worry that tougher standards will scare students away from their classes. The fight has turned into a bigger question about what academic rigor should look like at an elite school. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – Rolling Over – 11/14/25

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. While stocks eked out gains this week, it was a turbulent ride and under the hood some of the biggest winners this year are under major pressure. That’s not just true of the riskiest and most aggressively priced stocks, as crypto has taken hits along with precious metals. Even the juggernaut AI narrative is being tested, with surging credit spreads that represent market skepticism about the epic capex binge under way. US economic data remains scarce but we got lots of updates from China this week showing a surprising slowdown in that economy. Meanwhile the Federal Reserve has sounded the hawkish siren all week and markets are moving to reflect less support than previously expected.