Bespoke Brunch Reads: 5/8/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Blood In The Streets

Paul Tudor Jones says he can’t think of a worse financial environment for stocks or bonds right now by Yun Li (CNBC)

Macro hedge fund manager Paul Tudor Jones argues that the environment couldn’t get much worse, which at least has the ring of a contrarian opportunity…after all, if things can’t get worse, next they have to get better. [Link]

The Popping of the Bubble Stocks: An Update by Ray Dalio (LinkedIn)

Bridgewater’s Dalio declares a bubble in US equities has popped, but isn’t optimistic about the path forward for the market from here. [Link]

Tiger is suffering one of the biggest hedge fund drawdowns in history by Robin Wigglesworth (FTAV)

Massive tech hedge fund Tiger has been cut nearly in half this year as tech and growth stocks that it tends to hold get uniquely crushed. It’s unclear whether the fund can weather declines these large and remain a going concern. [Link; registration required]

Stocks and Bonds Are Falling in Lockstep at Pace Unseen in Decades by Gunjan Banerji (WSJ)

The combined drop in stocks and bonds isn’t unprecedented, but it’s highly unusual and it is extreme, putting pressure on investors across markets for it’s unusual one-two hit to brokerage balances and retirement accounts. [Link; paywall]

Citi acknowledges trading error after flash fall in some European shares by Joshua Franklin and Philip Stafford (FT)

A human error by a Citibank trader led to an 8% collapse in benchmark Swedish equity index on Monday; the drop didn’t last long despite the “bungled” execution on a basket of shares Citi was trading for a client. [Link; paywall]

Blue Bird

‘I Don’t Really Have a Business Plan’: How Elon Musk Wings It by Ryan Mac, Cade Metz and Kate Conger (NYT)

An inside look at the aggressive and free-wheeling world that Elon Musk inhabits, with little negative feedback and lots of micromanagement. [Link; soft paywall]

Investment Management

Wells Fargo Accidentally Kills Off FA in Letter to Clients by James Rogers (Financial Advisor IQ)

After an advisor left Wells Fargo’s wirehouse for an affiliate of Kestra Financial, WFC accidentally sent out a letter to his clients announcing his death. [Link]

Fidelity to Allow Retirement Savers to Put Bitcoin in 401(k) Accounts by Anne Tergesen (WSJ)

The 401k giant will soon allow investors to allocate retirement funds to bitcoin, opening the tax-advantaged investment accounts of employees at more than 20,000 companies to the crypto markets. [Link; paywall]

This $500 Billion Private Club for Family Offices Is Booming by Benjamin Stupples (Bloomberg)

As the number of family offices bloom, they’re starting to share information and education via an informal club that hosts regular events for its 250 members representing AUM of nearly half a trillion dollars. [Link; soft paywall]

Slowing Demand

Former Fed Vice Chair Quarles Says U.S. Is Likely to Suffer Recession by Rich Miller (Bloomberg)

After being ousted from the Fed when his term on the FOMC was complete, former Vice Chair for Supervision Randall Quarles thinks the Fed will need to hike so much that a recession will take place. [Link; soft paywall]

Americans Are Showing Inflation Fatigue, and Some Companies See a Breaking Point by Sharon Terlep (WSJ)

After spending two years busily buying everything they could get their hands on, American consumers are starting to balk at some of the prices that they’re being charged for discretionary items. [Link; paywall]

A third of small retailers can’t pay rent as financial struggles spike again by Ben Unglesbee (Retail Dive)

One in three smaller retailers are unable to cover their rent, with almost half saying their rent has risen over the next six months; smaller retailers aren’t able to absorb costs and pass on price hikes as well as larger retailers. [Link]

Shaky Lending

Used-Car Dealer Debuts Subprime Auto Bond Even as Sector Weakens by Adam Tempkin and Charles E Williams (Bloomberg)

Car-Mart, a used auto retailer targeting subprime quality buyers, priced an ABS backed by lower-quality loans yesterday and was able to sell them despite a steep concession demanded by investors. [Link; soft paywall]

‘Buy now, pay later’ is sending the TikTok generation spiraling into debt, popularized by San Francisco tech firms by Joshua Bote (SFGate)

Buy now, pay later (BNPL) is a way to take on debt at a potentially lower cost than credit cards. But 91% of consumer loans in California from 2020 were BNPL loans, and the seductive nature of the loans which lower the upfront cost of paying for big ticket items is starting to prove a challenge for some borrowers. [Link]

Data Privacy

CDC Tracked Millions of Phones to See If Americans Followed COVID Lockdown Orders by Joseph Cox (Vice)

CDC policymakers used anonymized location data to see how the public responded to curfews and other activity restrictions. While there is no evidence the CDC misused the data, FOIA requests reveal significant potential privacy concerns from the project. [Link]

Google lines up with Apple and Microsoft to nix passwords in favor of nearby-device authentication by Rob Pegoraro (Fast Company)

Major device and software companies are moving towards an open architecture that relies on identify verification on a smartphone in order to access other systems like laptops or PCs. [Link]

Location, Location, Location

$1-million milestone: Orange County median home price hits seven figures. by Andew Khouri (MSN/LAT)

Orange County is a sprawling Southern California polity with a diverse population, but housing has rapidly spiraled out of reach: the median home price has topped $1mm, a 22% jump versus a year ago. [Link]

I-Team: Body found in barrel in Lake Mead may date back to 1980s, more likely to appear as water recedes, Las Vegas police say by David Charns (8NewsNow)

A murder victim who was stuffed into a barrel in the 1980s was discovered in Lake Mead recently; authorities expect more such remains to emerge as brutal drought lowers the lake’s level. [Link]

Ball Games

What the heck is going on with the baseball? Everything you need to know about MLB’s scoring drought (ESPN)

Offense as measured by both batting average and scoring is among the lowest in league history to start this season as home runs disappear thanks to an intentional set of changes to the ball itself which may have gone further than expected. [Link; auto-playing video]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Equity Market Pros and Cons — Q2 2022

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q2 2022.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking!

On page two of the report, you’ll see a full list of the pros and cons that we lay out. We then provide slides for each “pro” or “con” that we’ve highlighted.

To read this report and access everything else Bespoke’s research platform has to offer, start a two-week trial to Bespoke Premium.

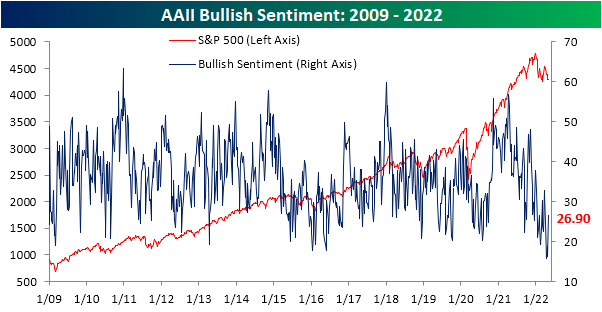

Bulls Bloom

The latest reading on sentiment from the American Association of Individual Investors showed bulls stepped back in as the S&P 500 generally rallied in the past week. After a historic low of only 16.4% last week, the percentage of respondents reporting as bullish rose back up to 26.9%. That is the first time over a quarter of respondents reported as bullish since the end of March. The double-digit weekly increase was also the largest since last October.

The increase in optimism was met with a 6.5 percentage point drop in the share of respondents reporting bearish sentiment. Even after that decline, over half of the respondents responded as bearish. That is the first time with back-to-back weeks of over 50% readings since May 2020. The current level of 52.9% is also still in the top 3% of all readings going back to the start of the survey in 1987.

That means in spite of a small improvement, sentiment continues to heavily favor bears. The bull-bear spread returned to a more normal but still very low reading of -26.

Fewer respondents were also reporting that they expect equity market prices to hold steady as neutral sentiment fell to 20.3%. That was the lowest reading since November 2020 when it was only one percentage point lower than now. Click here to learn more about Bespoke’s premium stock market research service.

Fed Day Follow Up

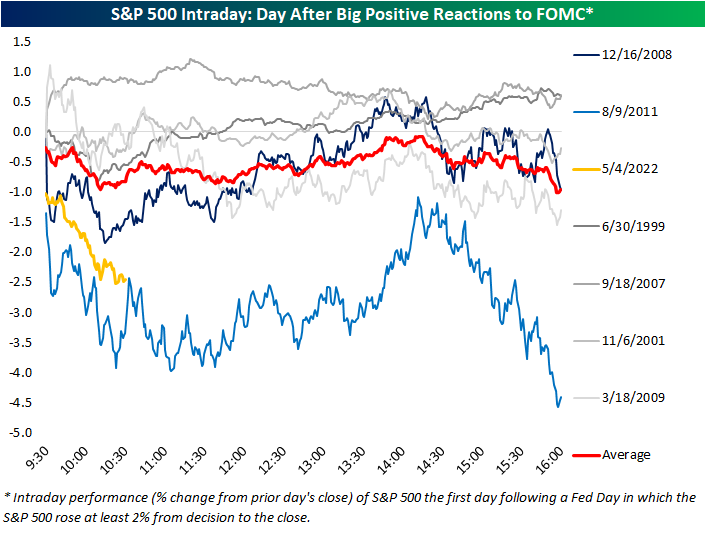

In last night’s Closer, we recapped the market reaction to the FOMC’s 50 bps rate hike noting that equities really took off once Fed Chair Powell ruled out the possibility of 75 bps hikes on the horizon. By the close, the S&P 500 rallied 2.55% from right before the decision (1:59 PM). As shown below, that marked the third-best S&P 500 reaction to a Fed day since 1994 when the FOMC began to announce its decision on the same day as the meeting.

Given today’s massive declines, the S&P has already erased its 2%+ post-FOMC gain. Below we show the S&P’s intraday performance the day after each Fed day when the index rallied over 2% post-meeting (1:59 to the close). For each day, the date shown represents the day of the FOMC meeting. On average, the S&P 500 has tended to gap down the following day and continue to trade lower throughout the first post-FOMC session as we are seeing today.

Today’s performance is certainly on the weaker end of these occurrences, though. In fact, like the other two largest post-FOMC rallies that saw over 3% gains in the afternoon of Fed days, December 2008 and August 2011, today saw a significant gap lower with continued losses through mid-morning. The continued selling today is setting up to more closely resemble the August 2011 occurrence. Following the December 2008 instance, on the other hand, the S&P 500 found a low in the late morning and even briefly went positive the day after the big post-FOMC gain.

While today is shaping up to look like another time the market rallied hard in response to the FOMC, taking a step back to look at all Fed day afternoon performance (1:59 to the close) versus next-day performance (full day), there is not much of a strong trend. As shown below, the S&P 500’s performance from 1:59 to the close on a Fed day is a statistically poor explainer of next-day performance. That being said, today does stand out as one of the worst Fed day follow-ups on record. Click here to learn more about Bespoke’s premium stock market research service.

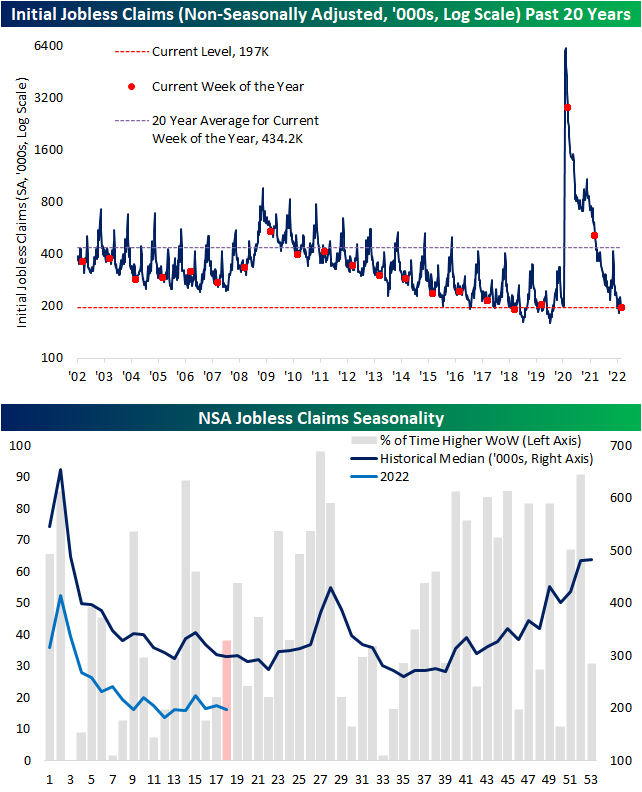

Claims Come Off the Lows

Initial jobless claims have come off of multi-decade lows in the past few weeks with the most recent print released this morning marking the most significant increase in some time. Claims are back up to 200K for the first time since the week of February 11th. Additionally, the 19K week over week increase was the largest one-week uptick since last July when they rose 33K and the level of claims was more than double what it is now.

Non-seasonally adjusted claims are also still at historically strong levels albeit having come off the lows. The only comparable week of the year that has seen a lower reading on claims was in 2018 when they were roughly 7K below current levels.

In terms of seasonal trends, claims will likely continue to fall modestly in the coming weeks before running into some seasonal headwinds in the late spring and early summer.

Continuing claims are delayed an additional week to initial jobless claims and this reading set a new low in the most recent print. Claims fell below 1.4 million for the first time since February 1970 reiterating the point that there are a historically small number of people filing continued unemployment claims. Click here to learn more about Bespoke’s premium stock market research service.

The Bespoke 50 Growth Stocks — 5/5/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were four changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

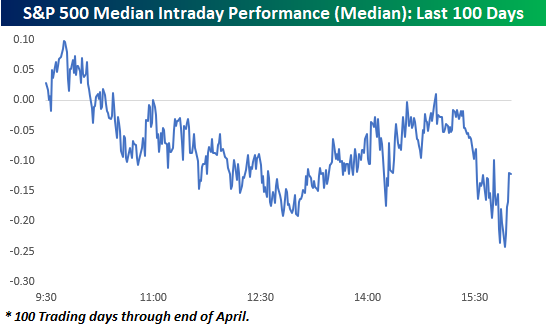

The Quitter Market

If it seems to you like the market simply can’t hold on to gains this year, you aren’t mistaken. The chart below shows an intraday composite of the S&P 500 on a median basis over the last 100 trading days through the end of April. The general pattern during this period has been for the market to open modestly higher, but then sell off for the remainder of the morning. It has then regained its footing shortly after mid-day but then sells off into the close.

How does the last five months or so compare to history? The charts below really put the recent trend of intraday weakness into perspective.

The first chart shows the number of days over a rolling 100-trading day period that the S&P 500 tracking ETF (SPY) traded in positive territory on an intraday basis but finished the day down. The reading currently stands at 38 and was as high as 40 (red line) in the last week of April. As shown in the chart below, there hasn’t been another period that the S&P 500 has had so much trouble holding onto intraday gains in more than a decade (October 2010)!

For the Nasdaq 100 (QQQ), it has been a similar story. As recently as April 22nd, the trailing number of times in the last 100-trading days that QQQ traded in positive territory on an intraday basis but finished the day lower reached 42 and currently stands at 40. Like SPY, the recent reading of 42 was the highest number of occurrences in a 100-trading day span since October 2010.

For both indices, the currently elevated frequency of giving up intraday gains has been extremely uncommon for the post-financial crisis period. Interestingly enough, though, in the ten years before the financial crisis, these types of periods were a lot more common, especially for the Nasdaq. Could it have anything to do with the fact that the last 12 years have also been one of the more accommodative monetary environments investors have ever experienced? Click here to learn more about Bespoke’s premium financial markets research.

Bespoke’s Consumer Pulse Report — May 2022

Asset Class Performance

The S&P 500 (SPY) is down nearly 4% since the last FOMC meeting on March 16th when the Fed lifted off of the “zero bound” by hiking rates 25 basis points. As we approach the second rate hike of this cycle tomorrow, below is a snapshot of recent asset class performance using our key ETF matrix. For each ETF, we show its total return since the close on the date of the last FOMC meeting (3/16) as well as its total return since February 19th, 2020, which was the stock market’s closing high prior to the start of the COVID pandemic.

Starting with performance since the Fed hiked rates for the first time back in March, we’ve seen across-the-board declines in US equities with the exception of a few sectors. Small-caps and the Nasdaq have been hit hardest since the March rate hike, while the Dividend ETF (DVY) has managed to post a small gain. Communication Services and Financials have been the hardest hit sectors with declines of 8%+, while Energy and Consumer Staples are both up more than 5%. Outside of the US, not one country ETF is up since the Fed hiked rates, and Germany and China are both down ~10%. The China ETF (ASHR) is down more than any ETF in our matrix since the first rate hike, but the 20+ Year Treasury ETF is right on its heels with a decline of 10.1%. Even gold and silver are now down since 3/16, while energy and agricultural commodities are in the green.

As asset prices have fallen in 2022, we’ve seen quite a few areas of financial markets really start to give up post-COVID gains. The S&P 500 has still posted a total return of nearly 28% since pre-COVID, but the small-cap Russell 2,000 is up less than 15% at this point. Looking at US sectors, Energy is up the most since 2/19/20 with a gain of 61%. Materials and Technology are still up 40%+, while Industrials and Financials are up just 18%. Two sectors — Utilities and Communication Services — have posted total returns of less than 10% since the pre-COVID high.

Outside of the US, India and Canada are both solidly green since the pandemic began, but countries like Brazil, Germany, Hong Kong, Italy, and Spain are all in the red. Commodity ETFs have been some of the best since the pandemic, although USO (oil) specifically is actually down 14% since the close on 2/19/20.

Treasury ETFs are down on a total return basis since pre-COVID, with TLT down the most at 15%. The only bond ETF that has offered some protection post-COVID is the inflation-protected TIP, which is up 8.42%. Click here to learn more about Bespoke’s premium financial markets research.

Bond Market Massively Oversold

The sell-off in bond prices over the last six months has been extreme to say the least. There are a number of ways we could highlight the carnage for bond investors, but one way is to look at how far bond indices are trading below their 200-day moving averages. As shown below, the Bloomberg US Aggregate Bond Market Total Return index is currently 8.5% below its 200-day moving average.

Going back to 1988 when daily price data begins, the 200-DMA spread is currently 2x more negative than any prior extreme oversold reading. Click here to learn more about Bespoke’s premium financial markets research.