Bespoke’s Morning Lineup – 6/26/26 – Limping into the Weekend

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In bear markets, stocks usually open strong and close weak. In bull markets, they tend to open weak and close strong.” – William J. O’Neill

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong start and intraday sell-off yesterday, futures have equities in the penalty box to start the last session of the week, so we’ll see if bulls can make a stand into the weekend. S&P 500 futures are down 0.40% while the Nasdaq looks to open down just over 1%. Treasury yields are modestly lower, while crude oil trades down more than 2.5% and barely hangs onto the $70 level. Gold prices are modestly higher, while Bitcoin looks to bounce but remains below $60K.

Asian stocks ended the week with a thud. The Nikkei was up over 1% heading into Friday’s session, but a 4.2% decline pushed that index into a 2.7% decline for the week. South Korea fell 5.8% in the session and 7.1% for the week, while onshore China stocks fell a relatively modest 2.3% and just 1.6% for the week. The main culprit for the weakness was in the technology sector, specifically memory stocks. Japanese inflation data didn’t help either as Tokyo CPI accelerated to 1.7% y/y at the headline level versus 1.4% in May,

European stocks don’t have nearly the exposure to technology that Asia and the US have, but that isn’t stopping indices in the region from falling. The STOXX 600 is down nearly 1%, putting it into negative territory for the week. Germany and the UK are leading today’s losses with declines of more than 1%, while Spain has been the region’s outperformer, falling just 0.4%. Looking on the bright side, a survey from the ECB showed consumer near-term inflation expectations falling from 3.9% down to 3.5%.

In the US today, the only economic reports on the calendar are Wholesale Inventories at 8:30, followed by Michigan sentiment at 10 AM. The Michigan report is notoriously negative, so don’t expect much optimism, although the survey of inflation expectations will be watched for signs of improvement.

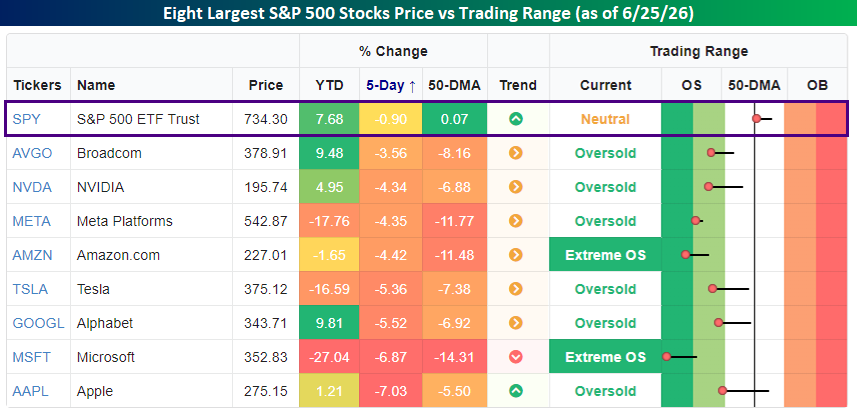

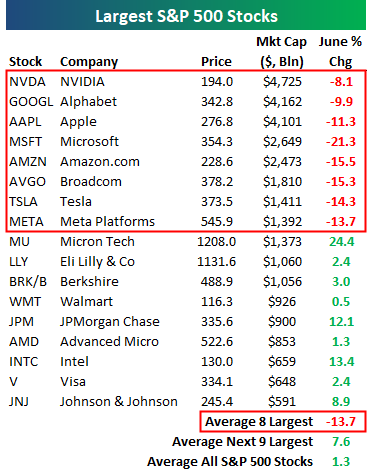

It’s been a rough June for megacap tech stocks. Through yesterday’s close, all eight of the largest S&P 500 stocks are below their 50-day moving averages, and in the case of Amazon.com (AMZN), Meta (META), Microsoft (MSFT), and Tesla (TSLA), they’re also below their 200-day moving averages.

All eight stocks, which account for about 38% of the entire S&P 500, are down anywhere between 3.5% to 7.0% over the last week, and they’re all at oversold levels trading at least 5% below their 50-day moving averages. Despite these oversold levels in nearly 40% of the S&P 500, the index itself is down less than 1% over the last week and remains above its 50-day moving average.

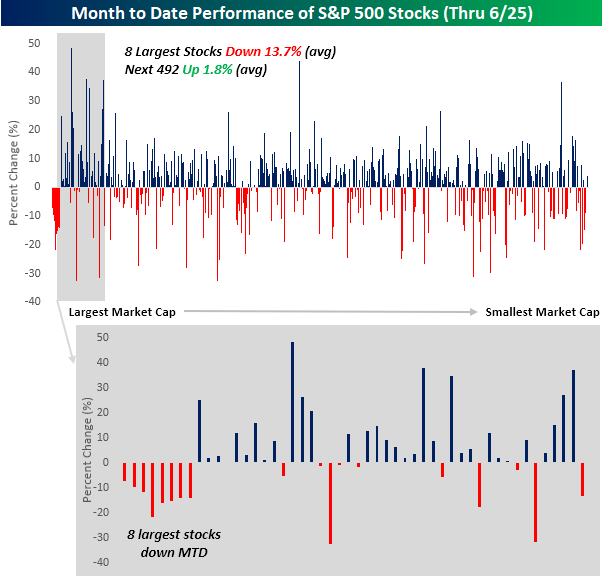

A look at the monthly performance of S&P 500 stocks shows the concentration of weakness among the largest S&P 500 stocks. The chart is sorted by market cap, so the largest stocks are on the left side of the x-axis, and the smallest ones are on the right. Note the deep concentration of red on the left. In fact, besides the eight largest stocks, there’s no other point in the chart where eight stocks in a row have negative returns this month!

Overall, the eight largest stocks in the S&P 500 are down an average of 13.7% this month, while the next 492 are up an average of 1.8%. In June, bigger hasn’t been better.

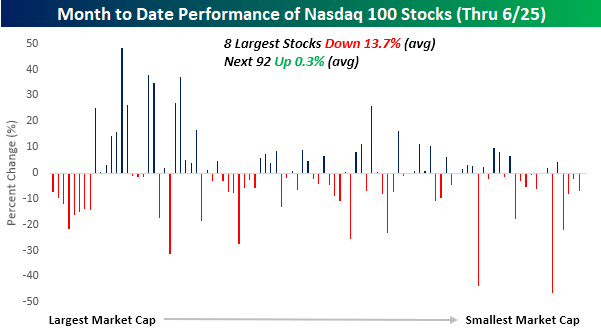

For the Nasdaq 100, it has been a similar trend. The eight largest stocks in the Nasdaq 100, which are also the eight largest stocks in the S&P 500, are down an average of 13.7%, and all are lower this month. Among the 92 other stocks in the index, though, the average performance this month has been a 0.3% gain.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Breadth Disconnects, Price Hikes, PCE – 6/25/26

Log-in here if you’re a member with access to the Closer.

- Consumer electronic devices are beginning to see price hikes as a result of higher memory prices.

- The S&P 500 has had a record share of days over the past 50-, 120-, and 200-trading days where price went in one direction and daily breadth went in the other.

- All rates of change for core PCE ex. rent are above 2%, meaning that even with zero rent core inflation is still comfortably above target.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q2 2026 Earnings Conference Call Recaps: Winnebago (WGO)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Winnebago’s (WGO) Q3 2026 earnings call.

![]()

Winnebago (WGO) is a diversified outdoor-recreation manufacturer of motorhomes, travel trailers, fifth wheels, and boats through brands like Winnebago, Grand Design, Newmar, Barletta, and Chris-Craft. Its mix of entry-level, premium, and luxury products gives investors a useful read on discretionary spending, financing-sensitive big-ticket purchases, dealer inventories, and the gap between affluent and middle-income consumers. Demand weakened from late March as inflation, high interest rates, geopolitical uncertainty, and low consumer confidence delayed purchases. Revenue fell 9.9% to $698.7 million, though Motorhome sales rose and operating profit improved to $9.6 million from a loss, helped by Grand Design Motorized, Newmar, and newer Winnebago products. Dealers remain financially stable but are ordering cautiously, clearing 2026 inventory, and targeting faster inventory turns. Winnebago expects fourth-quarter sales to fall sequentially and by double digits year-over-year. Management is cutting capacity and fixed costs while introducing cheaper products, including the $15,000–$16,000 Transcend Lite and roughly $50,000 Barletta Sanza. Luxury Chris-Craft demand remains stable, while middle-market products face the most pressure, and used RVs are taking share from new units. WGO reported weaker-than-expected EPS and revenue, and cut guidance, as investors shrugged the poor results off and the stock rallied more than 12% on 6/25…

Continue reading our Conference Call Recap for WGO by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Mega-Caps Fall, Russell Rebalance

There are still a few trading days left in June, but so far it has been a rough month for the world’s largest stocks. In the month where SpaceX (SPCX) began trading as the biggest IPO in history with a market cap near $2 trillion, the eight largest stocks in the S&P 500 have all fallen at least 8%, with six of eight down 10%+. Did SpaceX suck the life out of the rest of its mega-cap brethren?

Notably, the eight largest stocks are all down this month for an average decline of 13.7%, but the next nine largest stocks are all up this month for an average gain of 7.6%.

Tomorrow we’re also going to see one of the biggest rebalances in history for key Russell indices. With the halfway point of 2026 coming up, Russell is rebalancing its indices by moving stocks in and out of its large-cap Russell 1,000 and small-cap Russell 2,000.

The small-cap Russell 2,000 is sitting on a nice 20% gain this year mostly on the back of its largest index members.

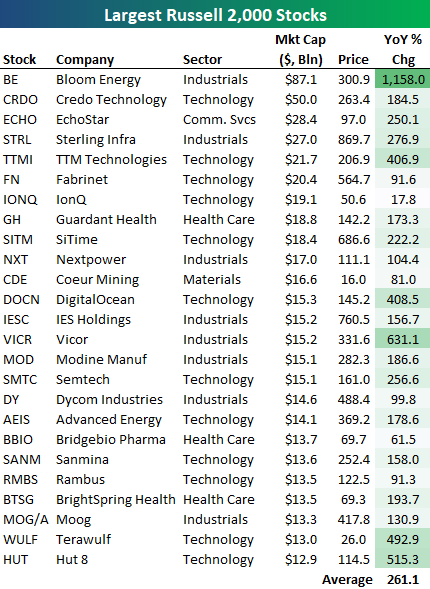

The peak market cap for inclusion in the small-cap Russell 2,000 has historically been $5.7 billion, but right now there are 165 stocks in the index with market caps above that mark, including six stocks with market caps above $20 billion, and two above $50 billion. Bloom Energy (BE) is the Russell 2,000’s largest stock by far at $87.1 billion. It’s up more than 1,100% over the last year.

Russell doesn’t provide a full list of the stocks moving up into the large-cap Russell 1,000 from the small-cap Russell 2,000, but they’ve said that 43 stocks will be making the jump tomorrow. Simply looking at the largest stocks in the Russell 2,000 gives you a pretty good idea of which ones will be graduating into the Russell 1,000.

Below is a list of the 25 largest Russell 2,000 stocks right now along with their year-over-year percentage change. As shown, all 25 of these stocks are up over the last year for an average gain of 261%!

You can bet that the large majority of these names will no longer be in the Russell 2,000 when trading begins next week, meaning the index itself is going to look and act a lot different in the second half of the year.

Want more from Bespoke? You can start by joining our Think BIG mailing list, where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

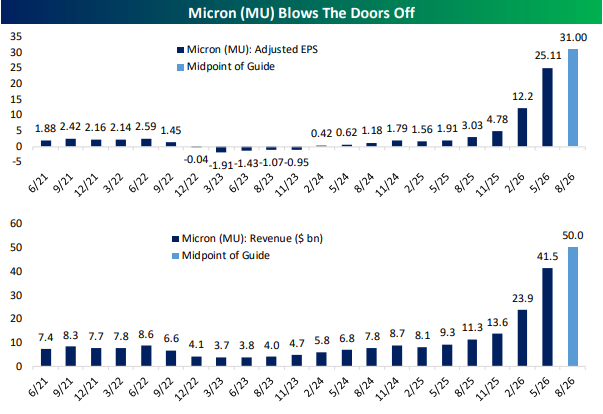

Q2 2026 Earnings Conference Call Recaps: Micron (MU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Micron’s (MU) Q3 2026 earnings call.

![]()

Micron (MU) is one of the world’s largest manufacturers of memory and storage semiconductors, producing DRAM (volatile working memory), NAND (non-volatile storage) flash, high-bandwidth memory (HBM), and Solid-State Drives (SSDs) used in data centers, PCs, smartphones, vehicles, industrial equipment, and other connected devices. These technologies are what allow computers and other devices to hold data and process information quickly. Micron said AI development is creating more demand for memory chips than the industry can currently produce, and it expects shortages to continue beyond 2027. Data center revenue exceeded $25 billion, sales of storage drives used in data centers more than doubled sequentially to over $5 billion, and shipments of Micron’s newest high-bandwidth memory product, HBM4, which is used alongside advanced AI processors, surpassed $1 billion. Scarce supply and steep price increases lifted gross margin to a record 84.9%, and it expects that figure to reach about 86% next quarter. The company also signed 16 multiyear contracts requiring customers to purchase agreed-upon volumes, giving Micron more predictable demand and protecting profitability if market prices eventually fall. Micron plans to spend roughly $27 billion this year to increase production, but building chip factories takes years and requires specialized workers, regulatory approvals, power infrastructure, and highly complex equipment. This means supply growth will likely stay gradual. The stock rallied about 17% on 6/25 after posting its fifth straight triple play…

Continue reading our Conference Call Recap for MU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

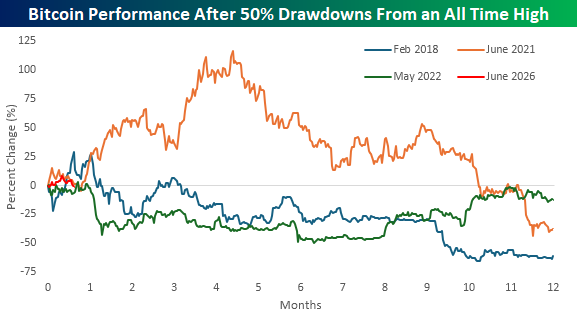

Bitcoin Gets a 50% Buzz Cut

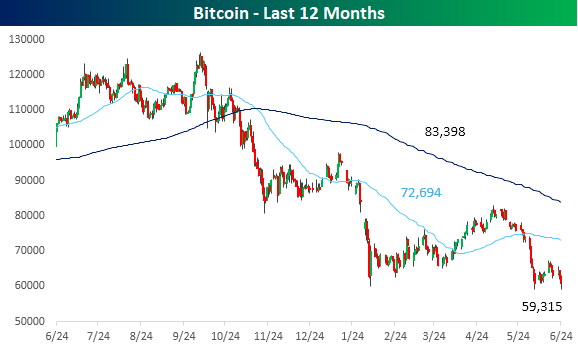

It always comes back – eventually. Bitcoin is making new multiyear lows today as prices break back below $60K to the lowest level since September 2024. Since the high last fall, prices have been in a steady downtrend in a stairstep pattern lower.

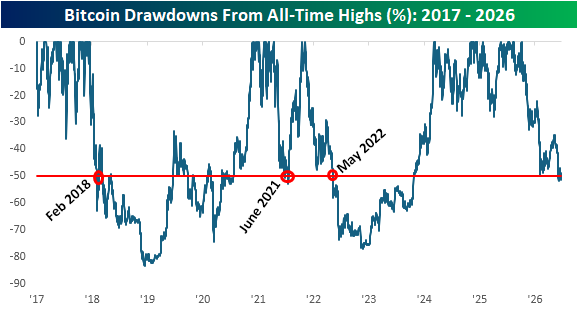

With today’s decline, the current drawdown in Bitcoin has exceeded 50%, a depth it hasn’t reached since late 2023. The chart below shows Bitcoin drawdowns relative to all-time highs dating back to 2007, when its price first closed above $1,000 per coin. This current decline represents the fourth time prices have reached a new record high and then got cut in half, with the last such decline being in May 2022.

The chart below shows Bitcoin in the year after each of the prior periods when prices first fell 50%+ from an all-time high. One of the things you always hear about Bitcoin after it sees a large decline like the current one is that “prices always come back”. That’s an accurate statement, but after prices experienced a 50% haircut in the three prior periods, the road back to new highs wasn’t necessarily short or smooth.

As shown in the chart, one year after each of the prior three periods, Bitcoin was lower a year later than it was when the drawdown first reached 50%. Not only that, but in two of the three periods, it barely even experienced a bounce. The one exception was after the June 2021 drawdown when prices quickly rebounded to new highs, but almost as quickly returned back to new lows. Perhaps the best thing Bitcoin has working in its favor is that you don’t hear much about $500,000 or even million-dollar price targets anymore.

Want more from Bespoke? You can start by joining our Think BIG mailing list, where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

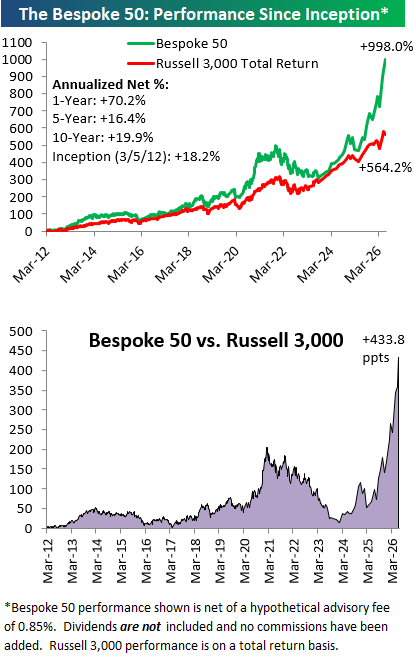

The Bespoke 50 Growth Stocks – 6/25/26

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were no changes to the list this month.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

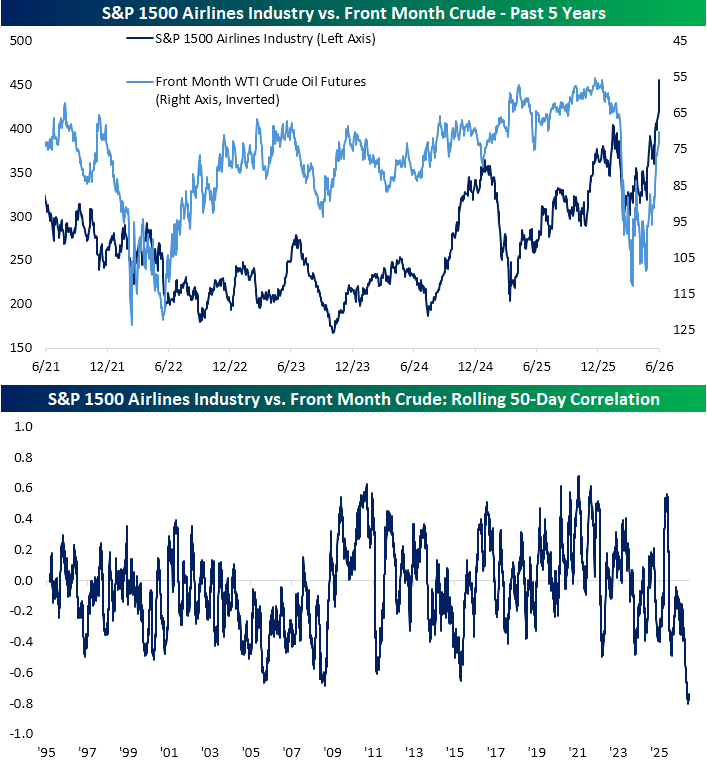

Airlines Exit the Stratosphere

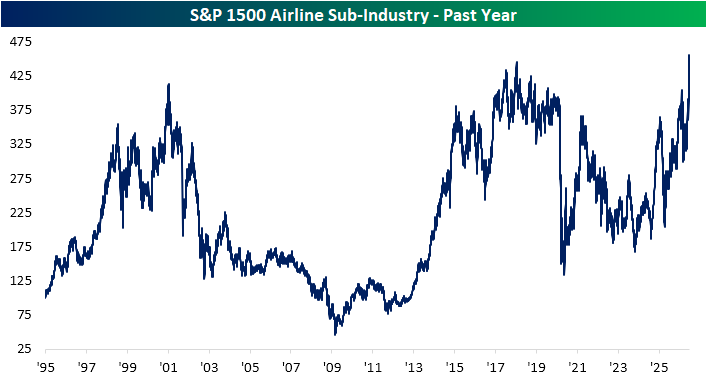

As we discussed in today’s Morning Lineup, across the pond during the European session, travel and leisure names were market leaders. While here in the US travel stocks are being outshined on the session by a still surging AI trade, fueled by strong results from Micron (MU) last night (discussed in last night’s Closer), the group is still performing well. Albeit lower today, the S&P 1500 Hotels, Resorts, and Casinos industry group is up over 9% over the past two weeks, and that pairs with an even higher flying airline industry. Following big gains in the past couple of weeks, the airline industry is now back at record highs.

Looking at the long-term price chart, that break of resistance is significant. Historically, passenger airline stocks have taken years to reclaim prior highs. As shown below, the group peaked in January 2001 and then traded steadily lower throughout the 2000s. After bottoming during the Global Financial Crisis years, the group didn’t reclaim that 2001 high until midway through 2017. Yet still, that breakout was short-lived. The airlines peaked in January 2018, followed by a steep drop two years later at the onset of the pandemic. Impressively, airlines didn’t even return to pre-pandemic (February 2020) levels, let alone the 2018 highs, until earlier this year.

As the saying goes, there are decades where nothing happens, and weeks when decades happen. Having spent years as dead money, airlines have taken a long time to set fresh record highs again. Even legs higher to the upper end of its range have been met with plenty of sizable setbacks. For example, as recently as a few months ago, airline stocks fell over 26% from the February peak to the March low, and it wasn’t until June 12th that they finally moved above the March high. The breakout in the past couple of weeks has only accelerated.

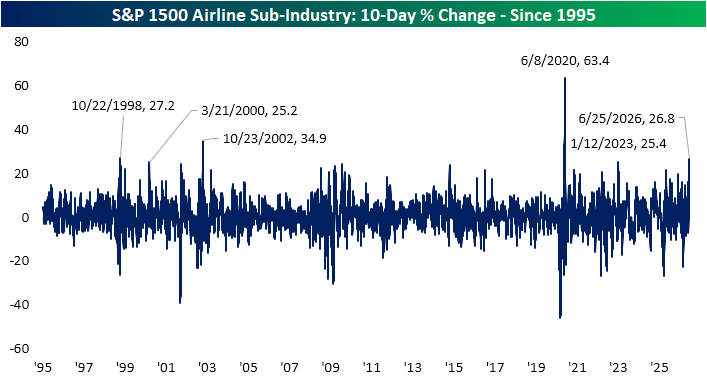

For starters, the group is currently on a five-day winning streak, and as shown below, over the past 10 sessions, it has risen 26.8%. That is one of only a handful of times the group has risen at least 25% in such a span; the most recent other examples being January 2023 and June 2020. Before that, there hasn’t been this sharp a move since October 2002.

Given airlines have risen with such fervor, the group is now running hot. As shown below, it is deeply overbought, trading 2.8 standard deviations above its 50-DMA. Further, the 14-day RSI is now at the highest level since October 2024 and in the 98th percentile relative to all other periods.

Of course, the airline surge is not completely random. The past two weeks’ rally coincides with positive developments on the war front, which has driven energy prices down. As shown below, this year has seen the price of crude oil almost perfectly mirror the price of airline stocks; a dynamic that has at times been the case in recent years, but not consistently.

The steep rise in Energy prices at the onset of the war also saw airline stocks trade sharply lower, and the reverse moves in the past couple of weeks have also been in lockstep, so much so that the rolling 50-day correlation between the industry and crude prices has been at the strongest inverse levels on record.

Want more from Bespoke? You can start by joining our Think BIG mailing list, where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Bespoke’s Morning Lineup – 6/25/26 – Memory Boost

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Nothing is invented, for it’s written in nature first.” – Antoni Gaudi

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are higher across the board this morning, and bulls have Micron (MU) to thank after the company reported blowout earnings with strong margins. Gross margins in the quarter were over nearly 85%, and the company guided margins to 86% next quarter. For perspective, the peak quarter of margins for Nvidia (NVDA) during its run was 77.4% in Q1 2025!

In response to the report, Nasdaq futures are poised to open higher by more than 2% while the S&P 500 looks to gain 0.66%. The lift in futures after the close also led to a rally in Asian stocks overnight, which has flowed over to Europe. Despite the big gain in equities, treasury yields are slightly lower, which should help buoy equities. Crude oil prices are down over 1% and have now essentially erased all their Iran war gains. Gold prices are below $4,000, and crypto is attempting to bounce with a gain of 2.6% but is still below $62,000.

It’s been an incredibly busy day for economic data. The revision to Q1 GDP came in higher than expected. Initial Jobless Claims came in lower than expected, while PCE data was mostly inline, so there wasn’t much in the data to disrupt the rally in equities.

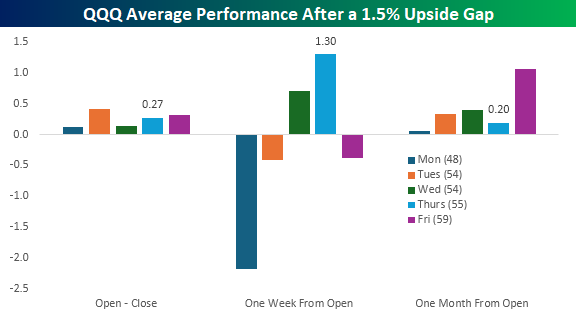

Last night’s earnings results from Micron (MU) have the Nasdaq poised to gap up by roughly 2% at the open, and it comes after another brief dip in which the Nasdaq 100 ETF (QQQ) came close to testing its 50-day moving average (DMA). After the last bounce failed to make a new high, traders will want to see this bounce make a higher high.

The chart below shows the performance of QQQ following upside gaps of at least 1.5% since 1999. In it, we have broken down returns by the day of the week. On the 55 prior days when QQQ gapped up more than 1.5% on a Thursday, its average return from the open to close was +0.27%. One week from the opening gap, QQQ averaged a gain of 1.3%, which is better than any other day of the week. However, the average 0.20% gain in the month after the prior 1.5% upside Thursday gaps is the second-weakest, trailing only Monday upside gaps.

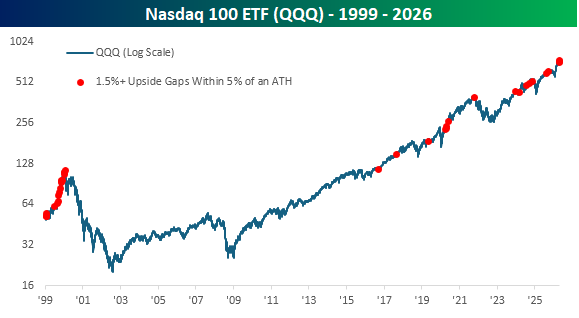

Looking at a long-term chart of QQQ since its inception in 1999, 1.5%+ upside gaps within 5% of an all-time high were frequent in the run-up to the dot-com peak. The frequency obviously dried up after the bubble burst when there wasn’t a new high for more than a decade. Since QQQ first returned to new highs in the last ten years, though, the frequency of these occurrences has been somewhat steady, although the frequency has picked up this month with three occurrences in just the last two weeks.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Silly Season, Abdicating Leaders – 6/24/26

Log-in here if you’re a member with access to the Closer.

- Micron (MU) earnings showed the company grew revenues 345% YoY with margins rising to 84.9% versus 39% one year ago with resulted in EPS to rise 1,214% YoY.

- Several areas that have been high flying in the past year like mega-caps, Bitcoin, and silver have come under pressure.

- New home sales were expected by economists to rise 3.2% MoM in May but fell 7.3% which takes them to the bottom of the range they’ve occupied for the past several years.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!