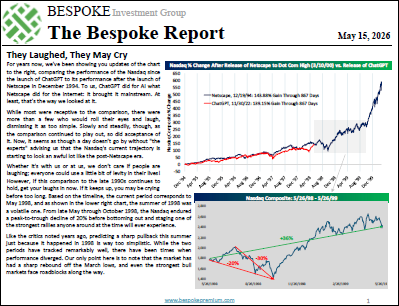

The Bespoke Report – 5/15/26 – The Laughed, They May Cry

The S&P has continued to leg higher in a picture-perfect breakout that now looks less like a “V” and more like a checkmark.

The market continues to follow the post-Netscape pattern, and more and more investors are starting to embrace the comparison. Is now the wrong time to be rooting for that comparison?

We cover everything going on across markets and the economy in this week’s Bespoke Report newsletter.

To read this week’s newsletter and gain access to the rest of Bespoke’s daily research, start a 30-day trial to one of our three unique membership levels. CLICK HERE to sign up today!

Nasdaq Gets Extended

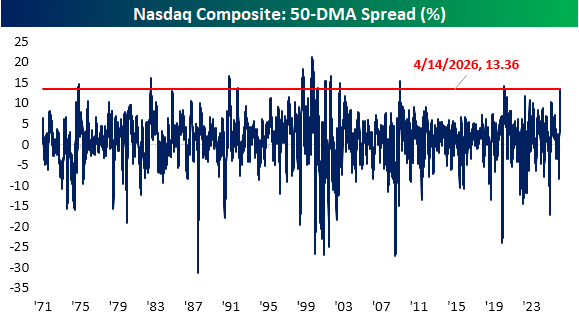

The sharp rally off of the March 30th low has seen the Nasdaq climb 25.9%. Back at the time of the low, the Nasdaq was extremely oversold, trading 2.85 standard deviations below its 50-DMA. In percentage terms, the Nasdaq was down 8.4% below that same moving average, which was a lot, but far from any sort of record setting reading.

Fast forward to yesterday’s close, the opposite was true. While the index wasn’t even extremely overbought (only 1.9 standard deviations above its 50-DMA), it did finish 13.4% above its 50-DMA for the most extended reading since June 2020. Going back throughout the over 50 years of history of the index, such extreme readings in the 50-DMA spread have been uncommon. Prior to the 2020 instance, the only other times it traded as far above its moving average was in 2009, various points in the 1990s to the Dot Com bubble burst in the early 2000s, 1982, and 1975.

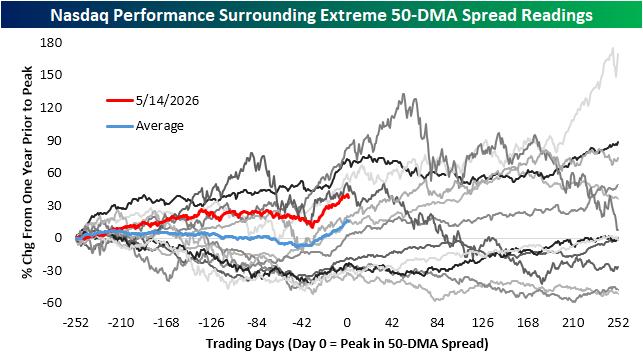

In the chart below, we show how the Nasdaq performed in the one year before and after those historic peaks in the 50-DMA spread. For each line below, day 0 indicates the peak reading in the 50-DMA spread. As shown, of the dozen previous periods, the Nasdaq has been higher versus one year prior seven of the times. This latest rally ranks as the fifth largest of those at 40%. Only the 1992, 1999, and 2000 instances saw bigger gains. Of those periods with larger gains, the following year only saw the index higher twice (up 9.5% after the 1992 instance and 75% after the January 1999 instance) whereas the others were more immediately leading up to the early 2000 Dot Com peak.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

S&P 500 is Still Overbought

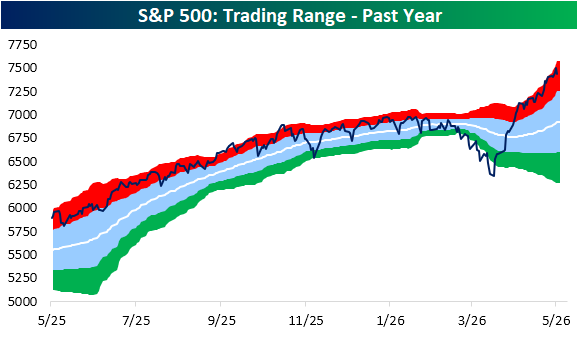

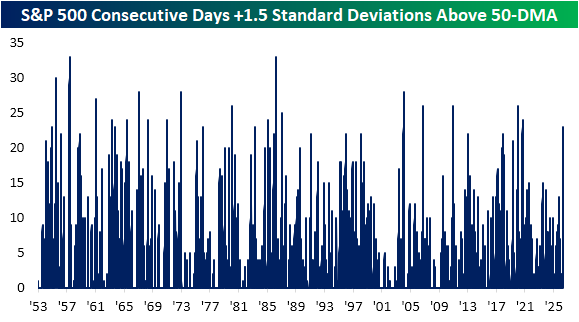

Although the index is lower to round out the week, the S&P 500 repeatedly reached more record highs recently. With the rally largely unabated, the index has been in overbought territory (> one standard deviation above its 50-DMA) every single session since April 14th. Not only has the S&P been overbought, but firmly so. Of the 24 consecutive sessions in overbought territory, the past 23 have seen the index close at least 1.5 standard deviations above its 50-DMA.

As shown below, this is now the longest streak of firmly overbought readings (consecutive trading days with the index at least 1.5 standard deviations above its 50-DMA) since September 2020. Looking back to the start of the 5-day trading week in 1953, there have been a total of 22 other streaks of at least 23 days. The longest of these extended to 33 straight sessions in March 1983 and May 1967.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Striking Breadth Levels

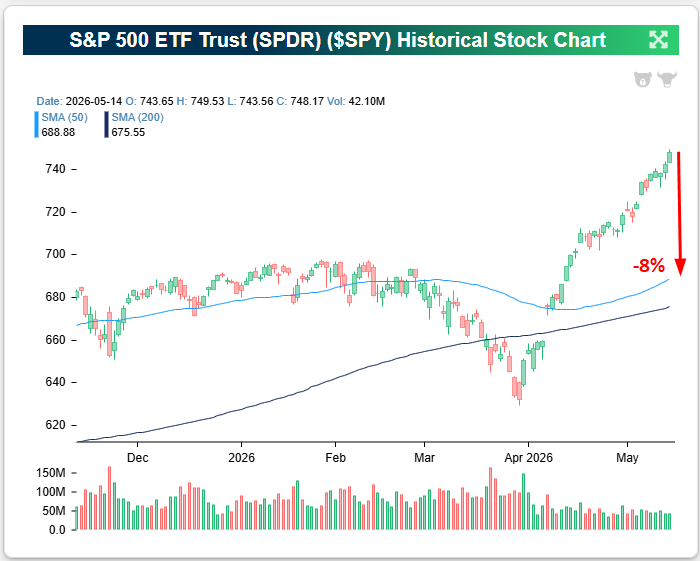

The S&P 500 has been driven higher by large-cap hyperscalers and semiconductors over the last month. This has pushed the index significantly above its 50-day moving average, indicating it’s well above trend right now.

As shown below, the index would need to fall 8% just to get back down to its 50-DMA from these levels!

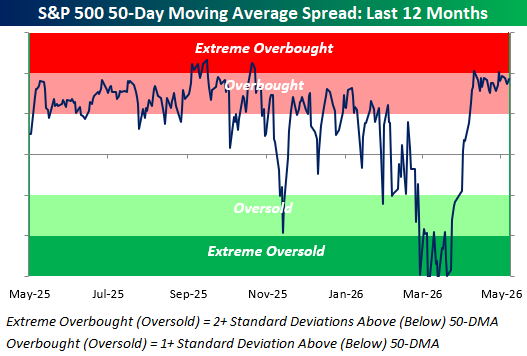

The S&P’s price has now been “overbought” (more than one standard deviation above its 50-DMA) for 23 straight trading days:

But while price is overbought, the underlying breadth in the index looks absolutely horrific.

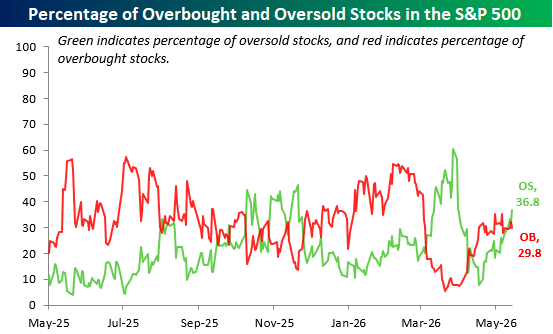

With the S&P remaining at overbought levels for more than a month, one would expect a majority of stocks in the index to be overbought as well. In reality, though, more than a third (36.8%) of S&P 500 stocks are actually “oversold” (more than one standard deviation below the 50-DMA), while just 29.8% are overbought.

The fact that so many more stocks are oversold than overbought in the S&P, even with the index’s price elevated well above its 50-DMA, highlights the narrowness of the recent rally.

Passive index investors have benefited even with the narrowness, but active investors without exposure to the AI infrastructure stocks have had a rough go of it.

Want to read more in-depth market analysis from Bespoke? Join our Think BIG mailing list or Bespoke Premium by starting a trial today! Click below for details on how to sign up for Premium:

Bespoke’s Morning Lineup – 5/15/26 – Rough End to the Week

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I always like to look on the optimistic side of life, but I am realistic enough to know that life is a complex matter.” – Walt Disney

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It may be Friday, but investors are in no mood to celebrate as equity futures are sharply lower. The Nasdaq is leading the losses, declining 1.28% while the S&P 500 is poised to open down by just under 1% (-0.90%). Treasury yields continue to march higher as they have all week, and in the commodity space, WTI crude oil is spiking 3% to just under $104 per barrel while gold is down over 2.5%. Bitcoin is also lower, falling by just 1%.

The weakness in US futures follows a lousy night in Asia. The Nikkei fell 2%, China was down over 1%, and South Korea plunged over 6%. Following these declines, all of Asia’s major indices finished the week lower. Higher yields contributed to the negative tone, and in South Korea, a potential labor strike at Samsung pressured that stock.

Weakness in Asia worked its way into Europe, and stocks are likewise lower across the board with declines of more than 1%. Here again, the primary culprit is higher yields, although CPI in Italy rose less than expected.

Getting back to the US, there’s not much in the way of earnings reports this morning, but at 8:30, we’ll get the release of the May Empire Manufacturing report, followed by Industrial Production and Capacity Utilization at 9:15.

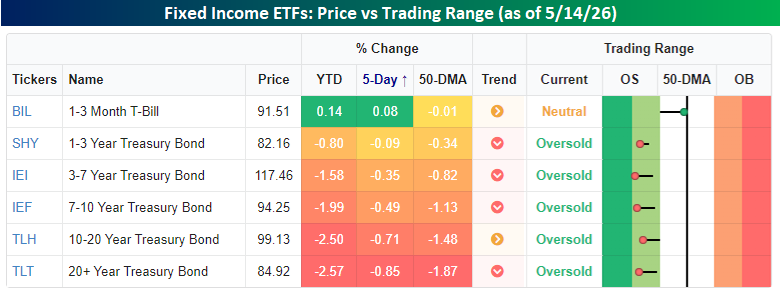

With inflation headlining the week’s economic data, and much of it surprising to the upside, yields have been an unavoidable and uncomfortable focus for investors. Almost across the entire yield curve, we’ve seen yields move higher this week, pushing the prices of the underlying bonds lower.

The snapshot of Treasury ETFs across the yield curve shows the story. Except for the shortest duration treasuries, prices have moved lower over the last five trading days (since last Thursday’s close), and the magnitude of the declines increases the further you go out on the curve. The magnitude of the declines hasn’t been extreme, but any treasury ETF with a duration of more than a year is currently oversold and will only get more oversold at the open today. YTD, it’s also been a year to forget, with declines nearly across the board.

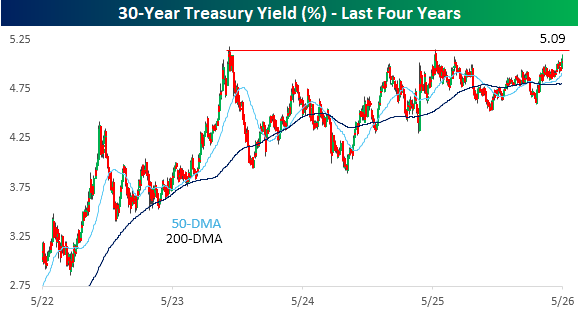

Of all the points on the yield curve, the 30-year is probably at the biggest crossroads. For nearly three years now, right above 5% has been a level the 30-year has flirted with multiple times, but each time it got there, the sellers didn’t have the firepower for a meaningful breakout. This week has been the third major test of that level as the yield pushes up towards 5.10% this morning. Will the third time be the charm or a strikeout?

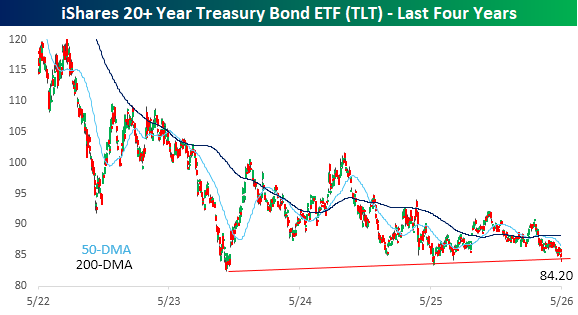

The iShares 20+ Year Treasury ETF (TLT) is the opposite of the 30-year yield. Prices plunged during 2022 and into early 2023 as the Fed hiked rates and inflation surged. As price pressures eased, yields and treasury prices stabilized, and while there was a rally off the 2023 lows into mid-2024, momentum quickly stalled out. Ever since then, prices have been stuck in the mid-80s, and this morning, TLT is trading down over 1% and testing support right around $84. It’s been a multi-year bear market for fixed income in the post-COVID era, and if these support levels don’t hold, the sector could be in store for a new leg lower.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – New Highs and No Breadth, Freight, Trade Prices – 5/14/26

Log-in here if you’re a member with access to the Closer.

- The rebound in AI Doom stocks has broken over the past week while proxies for OpenAI have ripped higher.

- The past month has seen a historic consistency of new highs despite breadth hardly notching any new highs.

- Both import and export prices rose significantly more than expected in April data.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

The Triple Play Report: 5/14/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 5/14/26 – Dow 50,000

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Chinese restaurants in America today outnumber the five largest fast food chains in the US all combined.” – Donald Trump

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US futures are in rally mode this morning as strong earnings from Cisco (CSCO) push that stock to record highs. The S&P 500 is on pace to open higher by about 0.3% while the Nasdaq is up 0.2%. Dow futures are leading the way, gaining 0.81%, which would put the index back above 50,000. The picture for US markets is positive now, but there’s a busy schedule of economic data on the calendar, kicking off with jobless claims and Retail Sales at 8:30.

Treasury yields are pulling back a bit with the 10-year yield down 4 bps to 4.44%. Oil prices are modestly lower, but WTI remains above $100. There have been no major developments out of the Middle East. Both gold and Bitcoin are little changed.

Asian markets were mixed overnight, with Japan down 1%, while Chinese stocks fell 1.5%. South Korea, meanwhile, bucked the trend, rallying 1.8%. The meetings between Trump and Xi and their entourages are obviously the major story of the day, and investors will be looking for any headlines coming from those meetings. In Europe, equities are higher across the board with the STOXX 600 up 0.6%, led higher by a 1.5% rally in Germany.

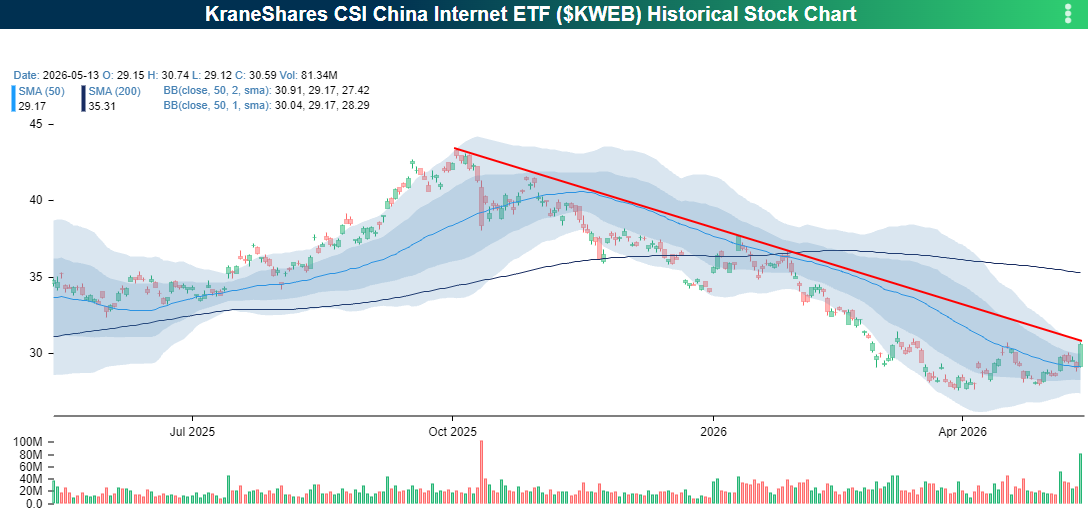

With all the attention shifting to China over the last 24 hours, investors rotated into Chinese stocks yesterday as the KraneShares China Internet ETF (KWEB) rallied just under 5% on strong volume for its best day since late January. Despite the rally, the stock finished yesterday’s session just below the downtrend line that has been in place since last October. KWEB has clearly stabilized since early April following steady losses over the preceding six months, but for bulls to get excited, they’ll need to see that downtrend get broken.

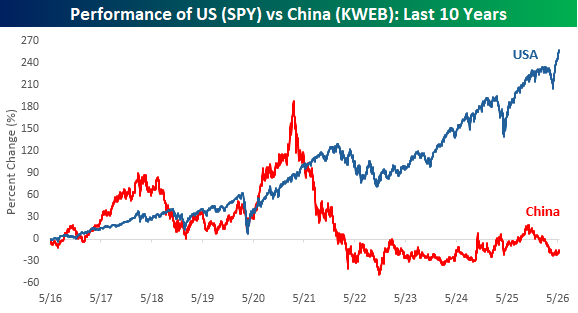

Chinese tech and US stocks have followed interesting paths over the last decade. While the performance was a close race between the world’s two superpowers in the last half of the last decade, in the post-Covid era, the two ETFs have followed diverging paths. Five years ago, the performance of KWEB and SPY in the prior five years was nearly identical. Since then, they have moved completely in opposite directions. As a result, the trailing 10-year performance of SPY is a gain of over 250% compared to a decline of 15% for KWEB! You can debate all you want about which world leader has the upper hand on a diplomatic basis heading into this summit, but from a market perspective, Trump is holding the nuts.

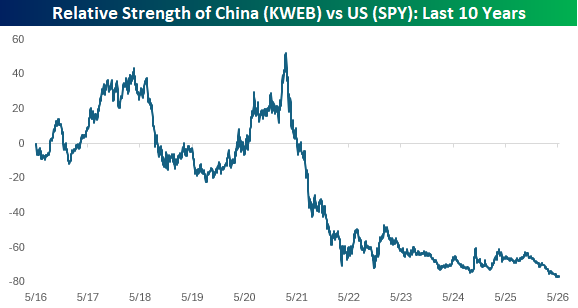

The relative strength of KWEB versus SPY further illustrates the sharp contrast. Chinese tech stocks fell off a cliff (almost literally) in the second half of 2021 and haven’t recovered since. Just in the last two weeks, the relative strength of KWEB versus SPY hit a record low.

At the individual stock/ADR level, Chinese stocks have experienced mixed returns this year. The snapshot below from our Trend Analyzer shows where nine of the largest/most active Chinese ADRs are trading relative to their trading ranges. YTD, some of these ETFs have seen big gains while others are down double-digits.

On a short-term basis, practically all these ADRs are doing well, as Pinduoduo (PDD) is the only one trading below its 50-DMA, while Trip.com (TCOM) is the only other ETF on the list that is not currently at overbought levels.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Brazil, Hot PPI, Hawks Speak – 5/13/26

Log-in here if you’re a member with access to the Closer.

- The Brazil ETF (EWZ) was down 4% today, breaking support at its 50-DMA.

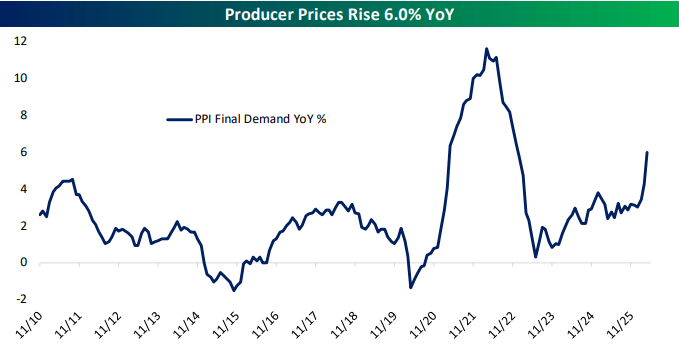

- Other than the 2022-2022 period of very high inflation, April saw the highest PPI reading since the current iteration of the final demand series was introduced back in 2010.

- Today’s Fedspeak in the wake of the latest inflation data was decisively hawkish.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

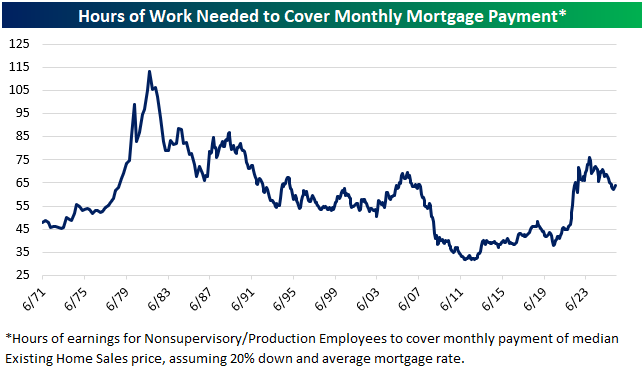

High Costs, High Equity, Prices Flat – A Look at Housing

Based on mortgage rates, home prices, and average hourly earnings, it currently takes roughly 64 hours of work to cover a monthly mortgage payment.

Below is a look at this reading going back to the early 1970s so you can see how housing affordability has shifted over the last five decades.

Affordability was at its worst in the late 1970s/early 1980s when mortgage rates spiked into the teens, but from there it was a steady trek lower all the way until the early 2010s as rates declined.

At its nadir in 2012, it took just over 32 hours of work to cover a monthly mortgage payment, so the current number is double that.

We’ve at least seen affordability get a little better over the last few years. At its peak in October 2023, it took 76 hours of work to cover a mortgage payment, which was the highest reading since late 1990.

As you can see in the chart, while mortgage costs are indeed high relative to the last couple of decades, these types of levels were routine through the 1980s and 1990s.

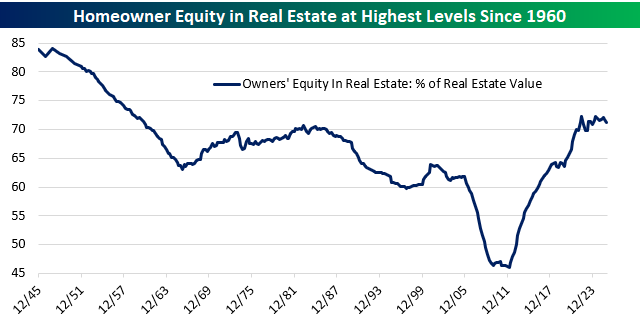

While affordability is worse now than it was during the ultra-low rate environment in the years after the Financial Crisis, homeowners are sitting on a boatload of equity. As shown below, homeowner equity plunged to just over 45% at its low point after home prices crashed in the late 2000s and early 2010s.

Low mortgage rates throughout the 2010s spurred a bounce-back in both home prices and loan activity, and then when prices spiked again in the early 2020s after COVID hit, homeowners were suddenly sitting on their highest amount of equity since 1960!

While home prices haven’t gone up in a few years, they also haven’t dropped, so that homeowner equity in the system remains a nice cushion.

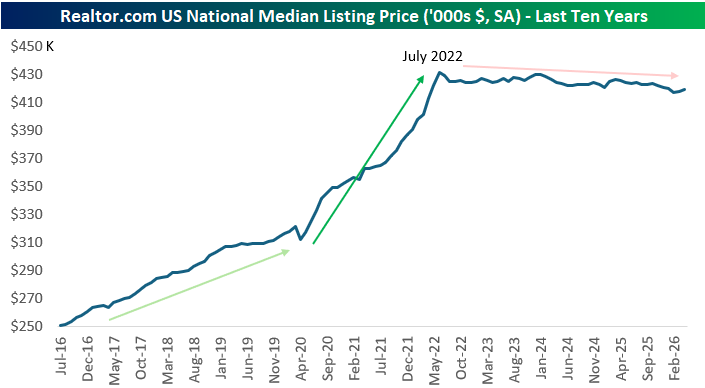

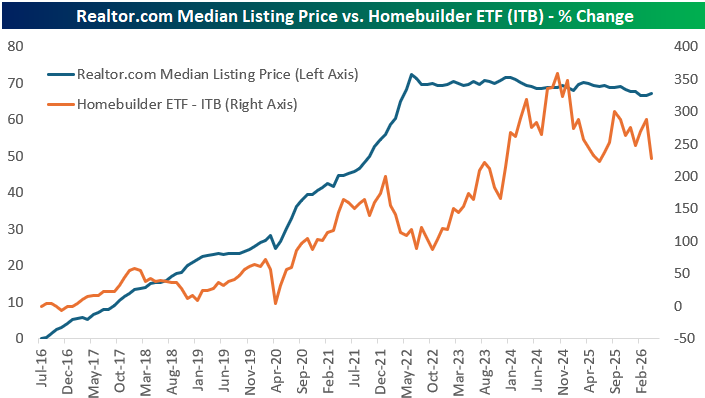

Speaking of home prices, below is a look at the median listing price of homes from Realtor.com data over the last ten years.

After a huge move higher in listing prices in the first two years after COVID hit in early 2020, we’ve seen prices flat-line.

The two-year post-COVID surge could have just been one big multi-year pull forward in prices, however.

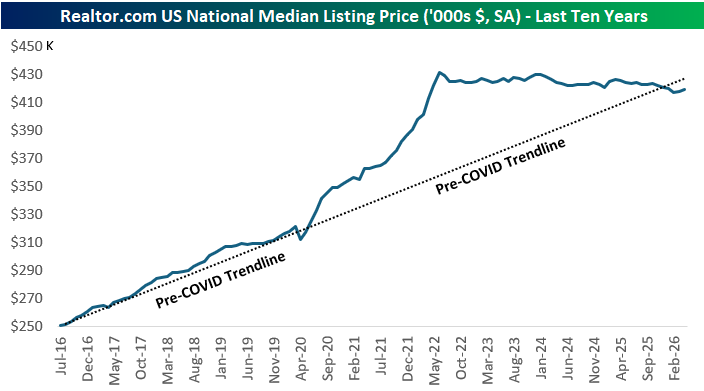

As shown below, if we extend out the pre-COVID trendline in listing prices all the way out to current levels, we’re currently right on trend. We just didn’t get there in a straight line.

Below is a look at the change in the median listing price versus the change in the homebuilder ETF (ITB) since 2016:

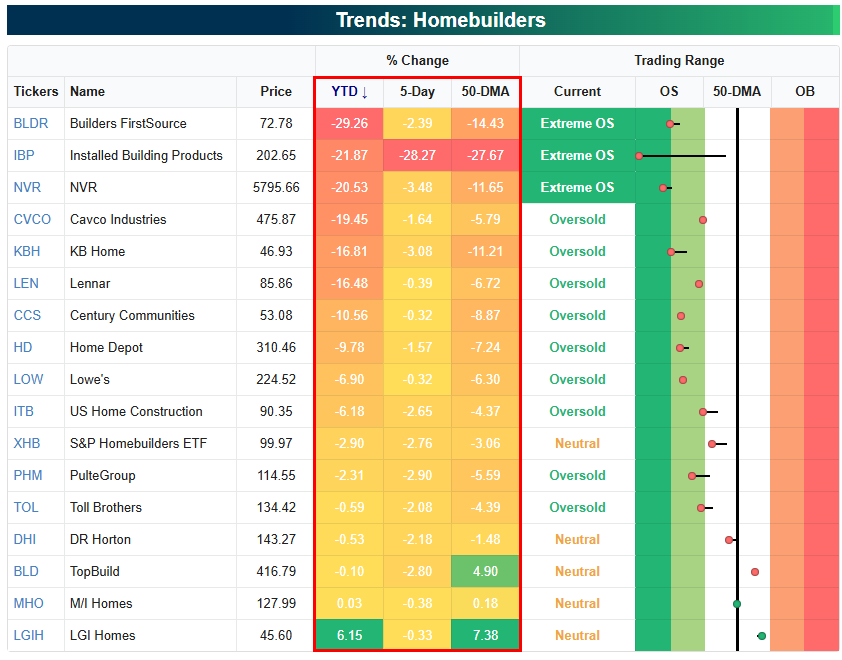

As shown below, the homebuilder space continues to get beaten up, with most stocks in the group at least 5% below their 50-DMAs in oversold territory. It’s been a rough 2026 so far, with ITB down 6.2% versus a gain of 9% for the S&P 500.

It’s likely that the builders will need to see some combination of lower rates or higher prices to get back on track.

Want to read more in-depth market analysis from Bespoke? Join our Think BIG mailing list or Bespoke Premium by starting a trial today! Click below for details on how to sign up for Premium: