Aug 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“But the interest of the Nation must always come before any personal considerations.” – Richard Nixon

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

On this day, 51 years ago, President Nixon became the first U.S. president to resign from office. While there are plenty of others that Americans likely wish had also resigned from office since then, Nixon remains the only President to leave office before his term ended, despite saying in his resignation speech that “I have never been a quitter.” As crazy as the political, social, economic, and geopolitical climate feels today, it has nothing on the backdrop from 51 years ago. If you weren’t around then, just ask someone who was.

There’s no shortage of uncertainty or unease in the backdrop today, but equities are within percentage points of record highs, and interest rates are relatively low versus history. This morning specifically, futures are firmly in positive territory on generally positive earnings news overnight. There’s no economic data on the calendar today, and all the earnings for the week are behind us, so unless the President fires up the Truth Social app, we can expect a relatively quiet summer Friday.

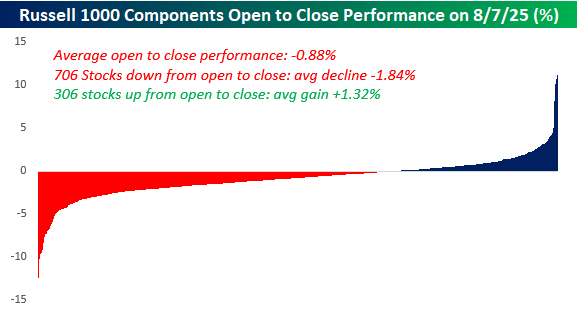

In yesterday’s trading, there were many quitters. Stocks opened the day higher and gave up their gains throughout the trading day. On an average basis, stocks in the Russell 1000 declined 0.88% from the open to close. Of the index’s components, 706 closed lower than they opened, and their average decline from the open to closing bell was 1.84%. On the upside, only 306 stocks (there are more than 1,000 stocks in the index) closed higher than they opened, and their average gain was just 1.32%.

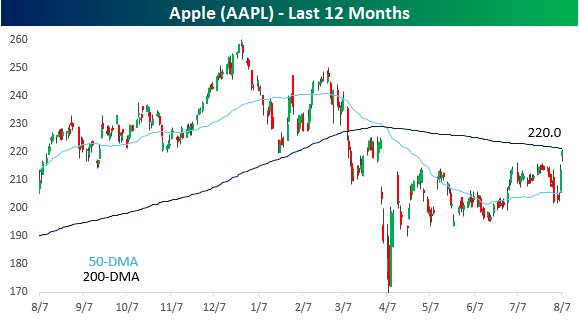

One stock that didn’t quit yesterday was Apple (AAPL). It gapped up around 2% and then added on another 1% from the open to close to finish just below its 200-day moving average (DMA), a level it hasn’t traded above since early March. While the stock didn’t quit Thursday, downward-sloping moving averages have a way of acting as resistance, so whether AAPL can close above its 200-DMA to close out the week will say a lot about how strong this latest two-day rally is. Will today be the day that Cook & Co can say to the bears that they won’t have Apple to kick around anymore?

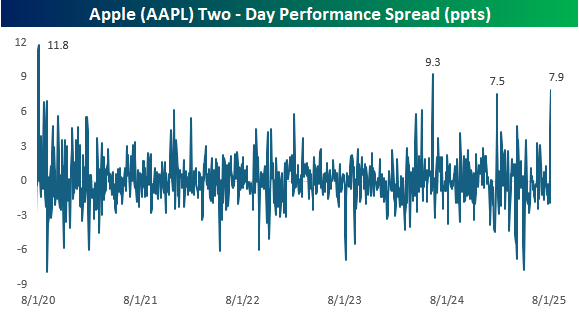

Besides rallying over 8% in the last two days, AAPL also outperformed the S&P 500 by just under 8% since Tuesday’s close, which ranks as one of the strongest two-day rallies relative to the S&P 500 in the last five years. The only two that were stronger were an 11.8 ppt performance spread in early August 2020 after the company reported earnings, and then a 9.3 ppt margin of outperformance after the company’s WWDC conference last summer. Besides those two periods, the only other two-day period of outperformance that was close to the last two days was a 7.5 ppt performance spread following its January report.

Aug 7, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you absolutely can’t tolerate critics, then don’t do anything new or interesting.” – Jeff Bezos

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Stock futures have been rallying all night following the President’s announcement with Apple CEO Tim Cook that the company will invest up to $600 billion in the US over the next four years. Trump also announced 100% tariffs on all imports of semiconductors, but qualified that with the caveat that any companies investing in the US would be exempt from the tariff. We don’t know how this will be tracked or what constitutes significant enough investing, but the initial reaction of markets has been positive.

AAPL shares have also been screaming higher. Yesterday’s 5% gain was the biggest margin of outperformance relative to the S&P 500 since last year’s WWDC conference, and this morning, shares are up another 3%. One semiconductor stock not feeling the love this morning is Intel (INTC). Shares are down over 3% after the President called for the CEO’s resignation, saying in a Truth Social post that he is ‘conflicted’. We can’t remember the last time a U.S. president publicly called for the resignation of a CEO, but then again, there have been a lot of firsts under President Trump.

On the economic calendar this morning, the main reports are jobless claims at 8:30, but we’ll also get Non-Farm Productivity and Unit Labor Costs at the same time.

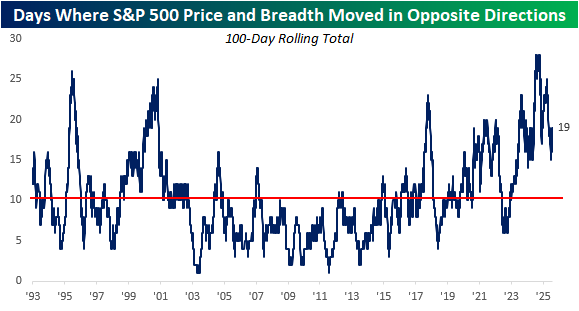

Yesterday was another one of those days when the S&P 500 moved one way, and breadth moved in the opposite direction. As the S&P 500 rallied more than 0.7%, there were 23 more stocks in the index that finished down on the day than up. As the S&P 500 has become increasingly top-heavy in recent years, the daily moves in the index have been increasingly less representative of the performance of the ‘average’ stock.

The chart below shows the rolling 100-day number of days when the S&P 500’s daily price change moved in the opposite direction as breadth. Beginning in the years right before Covid, this reading has been volatile, but the general trend has been higher. While the current level of 19 is well off the record high of 28 from last fall, right before the election, it is still nearly double the historical average of 10.

For most, the current elevated reading brings up memories of the dot-com boom (and subsequent bust), but it doesn’t have to end that way. Back in 2000, the largest stocks in the S&P 500 were incredibly overvalued, so when the bubble popped, they deflated quickly and pulled the index down with them. Today, the ten largest stocks in the index aren’t cheap, but their valuations are less out of step with the rest of the market than they were back in 2000. According to a report from SocGen, the top ten stocks in the S&P 500 account for 40% of the index’s market cap and a third of the profits. That’s an imbalance, but not an incredibly wide one.

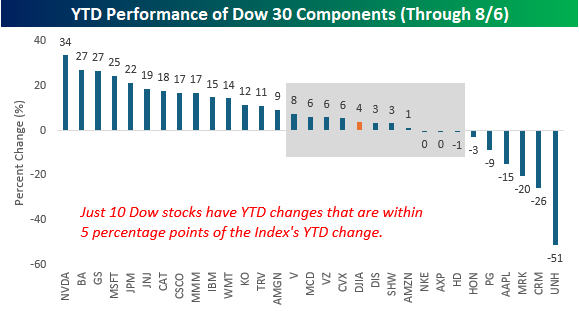

While the Dow Jones Industrial Average is hardly the most widely followed benchmark of US stock market performance, we found it interesting that the index’s 3.9% YTD gain is hardly representative of the YTD performance of the index’s 30 components. As shown in the chart below, just ten stocks in the index have YTD returns that are within five percentage points of the index’s change, and more than half (16) have YTD performances that are at least ten percentage points higher or lower than the index.

Aug 6, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If everyone isn’t beautiful, then no one is.” – Andy Warhol

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning following a slew of earnings reports that have been positive, on balance. There’s no economic data on the calendar, and the only non-earnings event is a just-scheduled 4:30 PM announcement from the President in the Oval Office. The topic of the announcement is unknown, so as usual, the President will keep everyone in suspense.

Overnight in Asia, markets were mostly higher, and in Europe, equities opened the session higher, but have erased those gains intraday, with Health Care leading the way lower.

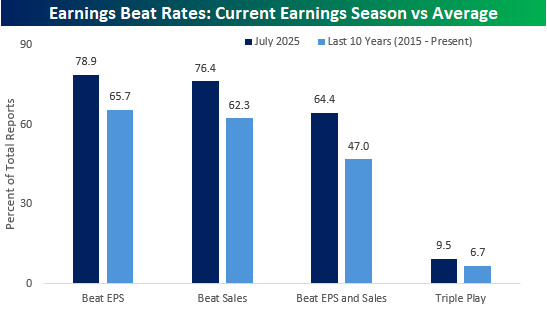

Unlike Warhol’s comment above, one could argue that when everyone looks great, no one does, and the current earnings season provides an example of that logic. The chart below shows the overall earnings and revenue beat rates of companies that reported in July versus the historical average. Whether you look at EPS or revenues, beat rates are well above their averages over the last ten years, and the frequency of Triple Plays is also above the historical average, but to a lesser degree.

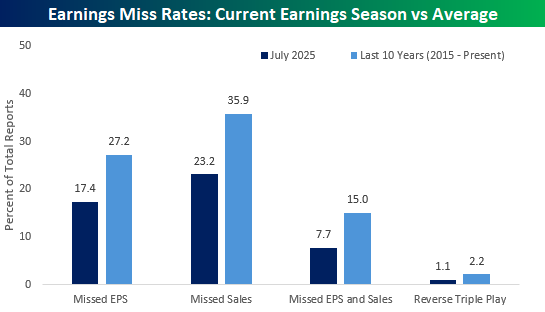

Conversely, companies are also reporting weaker-than-expected results at a much slower pace. The rate of EPS misses is nearly 10 percentage points below the historical average, while the revenue miss rate is over ten percentage points less. With fewer EPS and sales misses, the pace of reverse triple plays is also just half the pace of the average from the last ten years.

Aug 5, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“History is a sequence of random events and unpredictable choices, which is why the future is so difficult to foresee.” – Neil Armstrong

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There wasn’t much in the way of data to speak of at this time yesterday, but the pace of earnings has been strong since last night’s close, and futures are modestly higher ahead of the open with the S&P 500 indicated to open 0.26% higher while the Nasdaq is up 0.40%. The big earnings headliner overnight was Palantir (PLTR), which reported an earnings Triple Play and is trading up nearly 7%. Older economy stocks, however, aren’t faring as well this morning, with Caterpillar (CAT) trading down 3.6%.

The only reports on today’s economic calendar are the Trade Balance at 8:30 a.m. and the ISM Services report at 10:00 a.m. Economists expect the reading to bounce to 51.5, up from 50.8 last month.

Overnight and this morning, global equities have been broadly higher. In Asia, India’s Sensex was the only major index to finish the session lower, while China was up 1% and the Nikkei added 0.6%. Besides follow-through from Monday’s US session, stocks in the region were boosted by positive PMI readings. In Europe, the STOXX 600 was up 0.5% following a mixed batch of PMI readings for the Services sector.

While the equity market reversed much of Friday’s losses on Monday, Treasury yields saw little to no reversal. Take the 10-year yield, for example. After closing at 4.37% last Thursday, the yield plunged to 4.22% on Friday after the jobs report, but on Monday, yields fell even further and finished the day below 4.2%. This morning, yields are slightly higher, but only at the level they closed out last week. At these levels, yields are right near their lowest levels since Liberation Day in early April. The trillion-dollar question for investors now is whether the drop in yields is due to the market pricing in lower inflation or lower economic growth, as they have very different implications for the direction of the equity market.

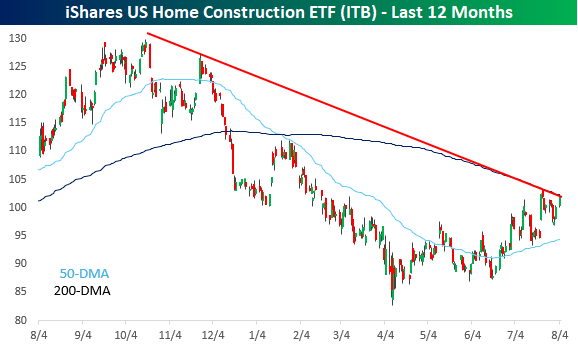

One sector that should benefit from lower yields is homebuilders. The iShares Home Construction ETF (ITB) has rallied 23% off its April lows, but it is still more than 20% off its 52-week high from last summer, so if the drop in yields was due to lower inflation, the group would presumably have plenty of room for more upside. From a technical perspective, ITB finds itself at an important juncture just below its downtrend that has been in place since last summer’s high, as well as the downward-sloping 200-day moving average. A rally in January failed at that level, but the ETF is heading into the latest test with a more established uptrend in place.

Aug 4, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you have to ask what jazz is, you’ll never know.” – Louis Armstrong

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The hangover for bulls came before the weekend last week, and they’re looking to start the week in a party mood with futures on all three major averages in the green and indicated to open about 0.5% higher. That’s only enough to erase a third of Friday’s losses, but it’s better than the alternative. Overnight in Asia, stocks were also firmly higher, while Europe’s STOXX 600 is up 0.6%. There’s no real catalyst for the gains this morning, but there’s also little in the way of economic and earnings data, so there’s not a lot of conviction behind the move.

While equities are moving higher, energy prices are down across the board, with WTI crude oil trading down 2% following the OPEC+ announcement that it would proceed with its September output hike of 547K barrels. Metals are fractionally higher across the board, and treasury yields are unchanged to modestly higher. Given the bounce in equities, you would expect to see crypto also rebound; however, both Bitcoin and Ether are still trading right around where they were last Friday.

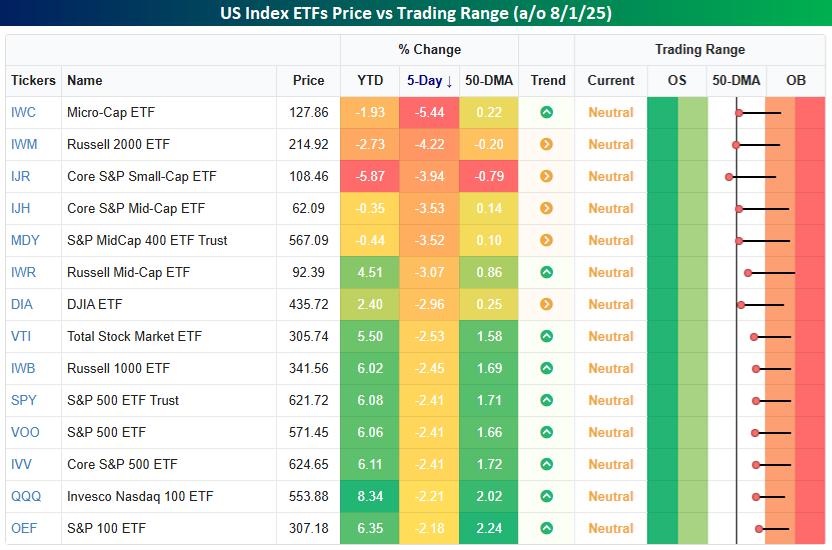

Right on cue, it seems, the typical late summer seasonal weakness has interrupted a market that had a consistent early summer bid. After a string of record highs, the S&P 500 sold off on an intraday basis every day last week. When the bell rang on Friday, the Nasdaq 100 (QQQ) and S&P 500 (SPY) were both down over 2% for the week, while the ne’er-do-well Russell 2000 (IWM) fell over 4%. As steep as the declines were, though, only two of the fourteen index ETFs shown below finished the week below their 50-day moving averages (DMA), and all fourteen were in neutral territory.

Aug 1, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Simple can be harder than complex”– Steve Jobs

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We almost made it through the week unscathed. The mega-caps reported generally good results, economic data didn’t ruffle any feathers, and Fed Chair Powell held to form and was a downer for stocks, but not by a lot. The only other hurdle was the August 1st tariff deadline, and for a President who thrives on volatility, his actions last night certainly shook things up. In a series of actions, Trump issued new tariff duties ranging from 10% to 41%. We cover this in more detail in the commentary of today’s Morning Lineup, and the actual impact will not be as painful as the headline numbers suggest. For a market that was already starting to act heavy, though, the tariff news pushed futures lower.

Along with weakness in US equities, Asian and European stocks fared even worse, bond yields moved slightly higher, oil prices declined, gold was little changed, platinum and palladium are both down close to 2%, and crypto prices are down sharply with declines of 1.5% in Bitcoin and over 3% in Ethereum.

We’re through most of the earnings data for the week, but on the economic calendar, we still have the July Employment report, ISM Manufacturing, Construction Spending, and Michigan Sentiment. Already this morning, the President has been railing against Powell, and if any of this morning’s data comes in weaker than expected, expect the volume on his Truth Social account to get to eleven quickly.

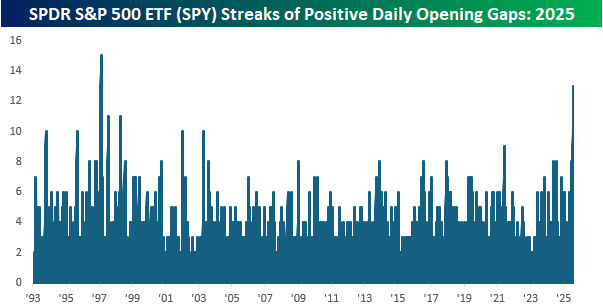

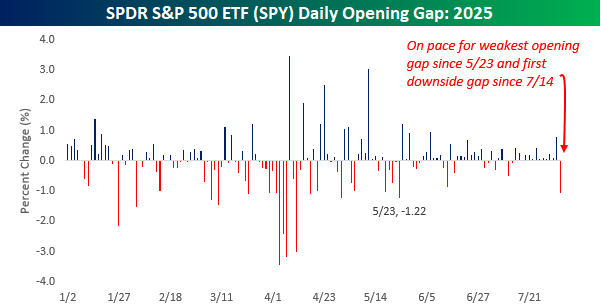

Hold on to your hats for a second, because the S&P 500 is on pace to not only open lower this morning, but at current levels, the decline would be about 1%. As shown in the chart below, the last time the SPDR S&P 500 ETF (SPY) gapped down 1%+ at the open was in late May, and it hasn’t opened lower since July 14th.

With 13 straight days of gains at the open, the streak that is about to end would be the second-longest in SPY’s history. The only streak that was longer ended in February 1997, and there were only two other streaks that lasted longer than ten days – July 1997 and February 1998. The comparisons always seem to go back to the late 1990s, don’t they?