Sep 7, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no law. It’s just the best lawyers always win.” – Ron Baron

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

Trade disputes and the potential for moving towards more closed borders on commerce has weighed on futures this morning. Futures are down across the board, but the Nasdaq is taking it hardest as additional restrictions on Apple iPhone usage for Chinese government employees could be coming. In the other direction, both the US and Europe are considering adding additional tariffs on Chinese steel imports.

On the economic side of things, Non-Farm Productivity and Unit Labor Costs were both higher than expected, and jobless claims came in lower than expected on both an initial and continuing basis. That kind of data won’t do much to weigh down interest rates, but it will certainly pressure stock prices.

Given its reputation, September has started just how you would expect it to. While the S&P 500 barely avoided finishing the first three trading days of the month down 1%, the Nasdaq finished down 1.16% month to date yesterday. The chart below shows the index’s performance during the first three trading days of the month for all years since 1971, and the red bars indicate years that the index was down 1%+. As shown, 1%+ declines in the first three trading days haven’t been particularly uncommon, especially in the last six years.

So, does a bad start to September for the Nasdaq mean anything with respect to the rest of the month? The table below lists each year that the Nasdaq was down 1%+ in the first three trading days of the month. For each year, we also show the index’s YTD performance heading into the month along with its performance for the remainder of the month. Of the sixteen prior years shown, the Nasdaq’s average change for the rest of the month was a decline of 2.85% (median: -3.70%) with gains less than a third of the time. That’s considerably worse than the 0.85% average decline for all years since 1971.

While it appears that months which start out poorly for the Nasdaq lead to further declines over the course of the rest of September, there is a caveat. If you look at the years when the Nasdaq was up over 10% heading into September but then traded down over 1% in the first three trading days, performance wasn’t nearly as bad. In fact, the S&P 500’s average rest of month performance was a gain of 0.61% (median: 1.56%) with positive returns four out of seven times.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Sep 6, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s not what you look at that matters, it’s what you see.” – Henry David Thoreau

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

It’s another weak morning for US equity futures as the backdrop of higher rates and oil prices weigh on sentiment. Futures are lower across the board, but not by a large amount. The key report of the day will be ISM Services at 10 AM. Plus, there are a number of conferences today, so be on the look out for individual company news throughout the day.

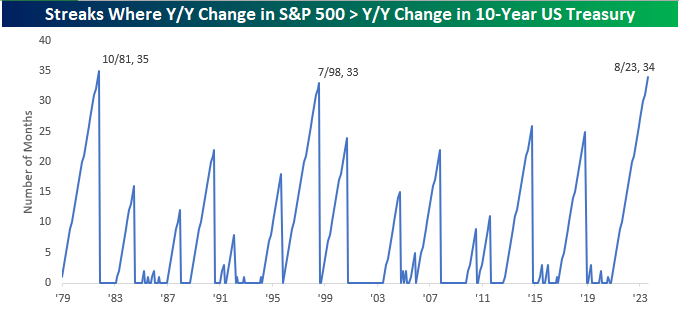

176 years ago today, Henry David Thoreau moved in with Ralph Waldo Emerson and his family after living in a woodshed on Walden Pond for two years. Two years in a shack is a long time, but bonds have been out behind, or maybe more accurately, in front of the woodshed for even longer. As measured by the Bank of America 10+ Year US Treasury Index, August was the 31st straight month that the year/year total return for US Treasuries was negative, easily surpassing the 15th month streak than ended in December 1980. Not only has the y/y change in long-term Treasuries been negative for more than two and a half years, but the y/y change has also lagged the y/y total return of the S&P 500 for 34 straight months.

Since 1979, there have only been two other periods where the 10-year underperformed the S&P 500 on a y/y basis for more months. The most recent ended in July 1998 at 33 months while there was a 35-month streak ending in October 1981. Given the way the numbers work out, unless treasuries stage a monster rally and/or stocks take a sharp leg lower this month, it’s almost a guarantee that the current streak will at least tie, if not exceed, the 35-month streak from 1981. In at least the last forty years, there hasn’t been a worse time to be creditor of Uncle Sam.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Sep 5, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I anticipate sluggish growth in the second half of this year” – Janet Yellen, 9/5/08

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

It may be Tuesday, but equity markets have a case of the Mondays today as equity futures are lower across the board with the Nasdaq leading the way lower. The catalyst for the weakness this morning appears to be weaker economic data out of China and Europe, but the reason for saying ‘appears’ is that sluggish growth would suggest a rally in bonds, but that hasn’t been the case as Treasury yields are higher across the curve. There’s not a lot of economic or earnings data to deal with today, but conference season is kicking off on Wall Street, and that can often be a time where companies lower forecasts, so be on the lookout for that throughout the day.

The quote above came just over two months into what was the second half of the year that then San Francisco Fed President Janet Yellen was referring to when she forecasted ‘sluggish’ growth. Sluggish would never be considered an adjective with a positive connotation, but it still doesn’t imply contraction. During the third quarter of 2008, though, the US economy contracted 2.1%, which was the largest decline in US economic activity since Q4 1990. Keep in mind that when Yellen made that comment, the third quarter was already more than two-thirds into what was a 2.1% quarterly decline in GDP, and yet Fed officials along with their counterparts in the White House, as well as most Wall Street economists were still forecasting growth! If you think that was bad, Q4 was even worse as the economy fell off a cliff. In the wake of the Lehman bankruptcy, GDP declined 8.5% for its largest decline since 1958! By the end of 2008 ‘sluggish’ growth wouldn’t have just been good, it had become a pipe dream!

This brings us to one of the morning’s lead headlines across just about every financial media outlet we have scanned, and that is the fact that Goldman Sachs has lowered its odds of a recession in the next 12 months down from 20% to 15%. Giving odds for a recession in such a precise manner certainly makes for great headlines and it’s always good to have baseline forecasts but to think that something as complicated as the US economy can be forecasted with such precision is at best naïve.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Sep 1, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Security is mostly superstition. It does not exist in nature, nor do the children of men as a whole experience it. Avoiding danger is no safer in the long run than outright exposure. Life is either a daring adventure or nothing.” — Helen Keller

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

It may be the Friday before Labor Day weekend (doesn’t it seem like we were just saying Memorial Day?), but it’s a bananas day for economic data with Non Farm Payrolls and ISM Manufacturing both being reported on the same day. Not only that, but there’s a couple of Fed speakers on the calendar as well. Bostic already spoke, and the key item from his speech was that there is “a shaking out that’s about to happen” in the debt markets which hardly sounds like an endorsement of higher rates. Shortly after the open, we’ll also hear from the usually hawkish Cleveland Fed President Mester.

Leading up to the Non Farm Payrolls report, futures have actually been picking up steam and are firmly in positive territory as treasury yields fall. The catalyst has been some better than expected earnings after the close on Thursday. In Europe, the major indices are higher despite a weaker than expected manufacturing PMI for August. It’s a good start, but the upcoming data is likely to have more of an impact on where things go from here. Investors have been encouraged by secondary employment reports suggesting some slack in the labor market, so a much stronger than expected report this morning would be a disappointment but could also be viewed as an outlier.

If you’ve been paying attention to the market this year, you know that Nvidia has been the biggest market winner by far, gaining over 230% through the end of August. Not only has it led every other S&P 500 stock, but its 13,275% gain also easily makes it the best performing stock over the last ten years. The next closest behind Nvidia during the last decade was AMD with a gain of ‘only’ 3,120%. If you really want to kick yourself heading into the weekend, just think, if you had invested $10,000 in Nvidia ten years ago, you’d have more than $1.3 million today. Now that’s an inflation hedge!

Realistically, even if you had the foresight to buy it ten years ago, would you really have had the stomach to hold it for ten years? The chart below shows the stock’s distance from all-time highs dating back to its IPO in 1999. Look at the swings. In October 2002 at the depths of the dotcom bust, Nvidia was down 90% from its all-time high. It recovered all those losses and more in the subsequent bull market, but during the Financial Crisis, it fell more than 85%. In its entire history as a public company, Nvidia’s average distance from an all-time high has been 40%. How many investors are willing to hold on to a stock in a 40% drawdown, let alone a drawdown of 90%?

Even in the last ten years, Nvidia has caused more stress than most doctors would consider healthy. The average distance it has traded from an all-time high is over 25%, and there have been two different periods when the stock fell over 50%, including a 66% drawdown as recently as last October. It’s always nice to dream of what could have been, but in some ways maybe it’s better if you never owned it at all. Think about it, how frustrated would you be if you bought NVDA ten years ago only to sell it after a 20% gain thinking you were smart, or even worse, selling it at a 15% or even 30% loss before it turned around. And if you did buy it ten years ago and managed to hold it all this time? Congratulations! You made the investment of a lifetime.

When hearing stories like this, the first thing most of us ask is, “What’s the next Nvidia?” The most important takeaway of the story, though, isn’t how Nvidia did from point to point but how it did in between. The biggest rewards in the market go hand in hand with the biggest risks, and if you want the former, make sure you’re prepared for the latter.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Aug 31, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’ve always said Thomas Edison invented the movie camera to show people killing and kissing.” – Quentin Tarantino

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

In 2017, Netflix CEO Reed Hastings was asked what the company’s biggest competitor was. Analysts were expecting him to say something like TikTok, YouTube, or maybe even cable TV, but he famously answered that the company’s most formidable competitor was sleep. His exact comment was, “You get a show or a movie you’re really dying to watch, and you end up staying up late at night, so we actually compete with sleep…And we’re winning.”

Love them or hate them, consumers are faced with a never-ending stream of video content from the countless number of streaming options to traditional movies, and even TV. None of them would have been possible, though, without Thomas Edison and his invention of the Kinetograph (the first known movie camera) 126 years ago today. We can safely assume that as big and important as Edison may have thought his invention would be, he would have never been able to ‘picture’ how important video would become in today’s culture. Today’s big invention is AI, and while hopes are high for how it will impact the world in the coming years, it’s ultimate impact will probably look nothing like what people today expect.

This morning futures are higher with the Dow leading the way following strong results from Salesforce.com (CRM). The stock is trading up over 5% and contributing more than 80 points to the Dow. A ton of economic indicators were just released and there was little in the way of surprises. Initial jobless claims were lower than expected while continuing claims were slightly higher. Likewise, Personal Income was slightly weaker while Personal Spending was slightly stronger. With respect to the PCE data, though, they were all in line with forecasts. So, while they’re still on the high side, at least there weren’t any big surprises. There wasn’t a big reaction in equity futures, but there was some slight improvement.

It’s been a nice rally since last Friday as the S&P 500 is looking to make it five straight gains in a row. With the rebound, you would expect individual investor sentiment to rebound as sentiment typically tracks stock prices closely, but at this point, investors aren’t buying it. According to the weekly survey from the American Association of Individual Investors (AAII), bullish sentiment did improve this week, but it increased by less than a percentage point, increasing from 32.3% to just 33.1%.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Aug 30, 2023

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I am not a person of opinions because I feel the counter arguments too strongly.” – Mary Shelley

Start a two-week trial to Bespoke Premium now to get full access the Morning Lineup.

If there’s one topic we can be confident that Mary Shelley wouldn’t be weighing in on if she was around today, it would be the economy. No matter which side you choose, there’s good evidence to support your view. Recession? How can we even entertain the thought with jobless claims and the unemployment rate both still at extremely low levels and the Atlanta Fed GDP Now tracking Q3 growth at 5.9%? OK, but with the yield curve on pace for a record streak of inversion, leading indicators down for more than a year straight, and manufacturing surveys deeply in negative territory, how can you not have a recession in your forecast? There’s merit to both arguments.

It’s a busy day for economic data, and it started off with the ADP Employment report. After a weaker than expected JOLTS report and a Consumer Confidence report which showed softening sentiment towards the labor market yesterday, the ADP report continued that trend coming in at 177K versus forecasts for an increase of 200K and follows four months where the reported number was well over 250K. Besides ADP, there is plenty of other data to contend with this morning including Wholesale Inventories (less bad than expected), revised GDP (down to 2.1% from 2.4%), Personal Consumption (slightly weaker), and Core PCE (2.0% vs 2.2% forecast). The only other report on the calendar today is the Pending Home Sales report (10 AM), which is expected to show a decline of 1%.

With two trading days left in August, it’s impressive to see that after heading into the week going all month without back-to-back positive days in the S&P 500, the S&P is now looking to string together its fourth straight positive day. That’s the good news. The bad news is that we’re heading into one of the toughest parts of the calendar. As shown in the composite chart of the S&P 500’s tracking ETF (SPY) over the last ten years, September has been the weakest part of the late summer/early fall consolidation period.

Below the chart, we have also included gauges from our Seasonality Tool which show how performance in the week and month after today’s date over the last ten years has compared to all other one week and one-month periods throughout the year. In the week after 8/30’s close, SPY’s median gain of 0.18% ranks in the 44th percentile relative to all other one-week periods. Over the next month, though, the median decline of 1.21% ranks in just the fourth percentile relative to all other rolling one-month periods. Just another reason very few people like to see summer end.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.