Feb 2, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Meta Platforms’ (META) Q4 2025 earnings call.

Meta Platforms (META) builds the social fabric of the internet through its Family of Apps, including Facebook, Instagram, WhatsApp, and Threads. With over 3.5 billion daily users, Meta makes communication tools and advanced AI models, monetizing this massive engagement via a sophisticated advertising ecosystem. While Meta is known as a social media giant, it is developing into a deep technology company, now looking to pioneer what it calls personal superintelligence and making proprietary silicon and global-scale energy infrastructure to power the next generation of computing. In Q4, revenue grew 24% YoY to $59.9 billion, funded by record-breaking holiday ad demand. However, the focal point was a 2026 capital expenditure guide of $115–$135 billion, nearly double 2025 levels, to build out Meta Superintelligence Labs and a new organization, Meta Compute. Zuckerberg is pivoting from the metaverse toward AI-powered wearables, noting that Ray-Ban glasses sales tripled last year. Internally, Meta is seeing a macro-shift in productivity. The company claims that AI coding tools have increased engineer output by 30%, allowing single contributors to handle tasks previously requiring entire teams. After reporting a triple play, the stock rose 10.4% on 1/29…

Continue reading our Conference Call Recap for META by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Feb 2, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Tesla’s (TSLA) Q4 2025 earnings call.

Tesla (TSLA) designs and manufactures electric vehicles, battery energy storage systems, and humanoid robots. Beyond its mass-market Model 3 and Y, the company is distinguished by its “Physics First” engineering and in-house semiconductor design. Tesla serves a global market of tech-forward consumers and utility-scale energy providers, offering insight into the convergence of autonomous mobility and domestic manufacturing. It is currently the only major US automaker operating its own lithium and cathode refineries. Tesla is undergoing a historic pivot, prioritizing an autonomous future over traditional hardware. Management announced the “honorable discharge” of the legacy Model S and X lines, as CEO Elon Musk put it, to convert Fremont factory space for Optimus robot production, targeting 1 million units annually. Despite 2025 delivering Tesla’s first annual revenue decline (falling 3% to $94.8B), the stock rose initially on news of a massive $20B+ CapEx plan for 2026, more than double previous guidance. This capital will fund six new factories and a domestic TerraFab to mitigate geopolitical chip risks. Tesla also confirmed a $2B investment in xAI to integrate Grok for fleet management. While the energy business hit record profits ($12.8B revenue), the focus is now squarely on the April Cybercab production launch and the transition to a subscription-only FSD model. Despite a higher open on 1/29 after posting better-than-expected results, shares fell intraday and closed near session lows, down 3.5% on the day…

Continue reading our Conference Call Recap for TSLA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Feb 2, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Shut your eyes and see.” – James Joyce

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a shaky end to the week and the month for US markets on Friday, things remain somewhat unsteady as we kick off the new month. S&P 500 futures indicate a 0.3% decline at the open, while the Nasdaq is priced to open down twice as much. For both indices, current levels are well off their lows so that it could have been a lot worse.

Treasury yields are slightly lower, with the 10-year yield starting the week at 4.23%. Crude oil is sharply lower, trading down close to 5% as President Trump suggested that the Iranians are looking to come to the bargaining table. In the metals space, it’s a mixed picture with gold up about 1% while silver bounces over 6%. Copper and Platinum, meanwhile, are both lower. After moves like we saw late last week in the space, though, we would expect more wild trading in the days ahead. These types of volatility spikes have a way of lasting more than a few days before things finally settle down.

It was a negative start to the week in Asia as the Nikkei fell over 1%, while Hong Kong and China both slumped by more than 2%. The big loser, though, was South Korea, where the KOSPI plunged over 5%, and trading briefly came to a halt because of circuit breakers. The weakness in that index stemmed from a weekend story in the WSJ where Nvidia CEO Jensen Huang said that the company’s investment in OpenAI will not be the $100 billion previously reported, and that has raised new concerns about the vitality of the AI trade.

Today is one of those rare days, it seems, where the lack of a vibrant technology sector in Europe is a plus. The STOXX 600 is up 0.4%, and the German DAX and Spain’s IBEX 35 each rally over 0.75%. Better-than-expected manufacturing PMIs for January have also acted as a positive catalyst.

In the US today, the only economic report on the calendar is the ISM Manufacturin,g which is projected to rebound slightly from December’s reading of 47.9. Given the surprise strength in the Chicago PMI last week, though, don’t be surprised if that report comes in hot. Outside of economic data, the first major tech report of the week will be Palantir (PLTR) after the close. As we detailed in today’s Chart of the Day, growth-oriented sectors of the market have been messy lately, so PLTR’s report could have big implications for the sector.

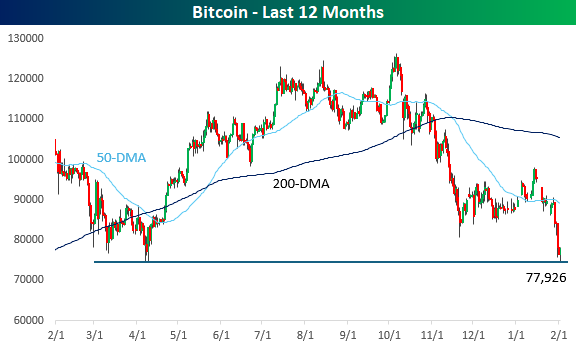

Along with growth-oriented stocks, crypto assets have been terrible performers for the last few months, and over the weekend, Bitcoin tested 52-week lows near $75K. Prices are rebounding slightly this morning along with equity futures, but the burden of proof is firmly on the back of the bulls now as Bitcoin’s price trades near the breakeven price for all of Strategy’s (MSTR) holdings.

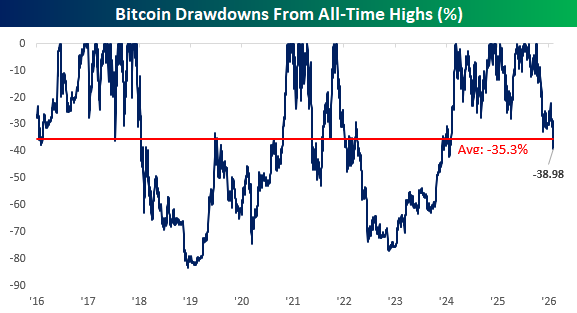

While it’s been a painful few months for crypto, it’s worth pointing out that this remains just a run-of-the-mill decline for Bitcoin. While it’s currently down about 39% from its all-time high, on any given day since 2016, its average drawdown from an all-time high has been over 35%.

Jan 30, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Hi-yo, Silver! – The Lone Ranger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Warsh it is. After months of speculation in the horse race among potential candidates, President Trump announced his boardroom decision, and the winner of “The Apprentice: Federal Reserve” is Kevin Warsh. Futures initially sold off sharply when news of the nomination first hit the tape last night; they have since recovered much of those losses. The major averages are now looking at more modest declines of 0.50% or less. It remains to be seen how Kevin Warsh will act when he’s in the Chairman’s seat, and while he may be considered as more hawkish than some of the other nominees, he’s well respected by the street. Furthermore, all worries over Fed independence over the last six months can probably be put to rest.

It was a lower session to close the week in Asia, as major country benchmarks ended the week with mixed returns. Japan finished the week down 1% while China was down less than half that. On the upside, the Hang Seng had a much better week, rallying 2.4%, but couldn’t hold a candle to South Korea, which rallied 4.7%. Japanese yields pulled in a bit after Tokyo CPI decelerated from 2.0% to 1.5% y/y.

In Europe, it’s a much more positive tone this morning as the STOXX 600 is up nearly 1% with Spain’s 1.8% rally leading the way, although no major benchmark is up less than 0.5%. Banks are seeing some of the largest gains, but the rally has been broad-based with Energy and Materials being the only sectors in the red, while advancers outpace decliners at a 5-2 rate. In economic data, Eurozone GDP rose more than expected 0.3% while CPI in Spain declined more than expected (-0.4% m/m).

The only economic data on the calendar today in the US is PPI at 8:30 and Chicago PMI at 9:45, but the main area of focus will be the President’s nomination of Kevin Warsh to replace Powell. PPI came in much higher than expected on both a headline (0.7% vs 0.3%) and core level (0.5% vs 0.2%), so that has pushed futures down a bit again.

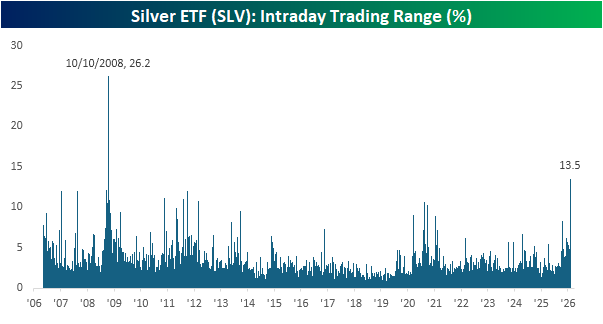

It seems fitting that on the anniversary of the Lone Ranger radio debut in 1933, we’re getting some historic moves in silver over the last 24 hours. Let’s start with the Silver ETF (SLV). In yesterday’s session, the ETF traded as high as $109.83 before cratering to $96.74 and then settling at $105.57. From its intraday high to its intraday low, though, SLV traded in a 13.5% range which was the second largest intraday range in the ETF’s history, trailing only the “marathon” 26.2% intraday range on 10/10/08 during the thick of the financial crisis.

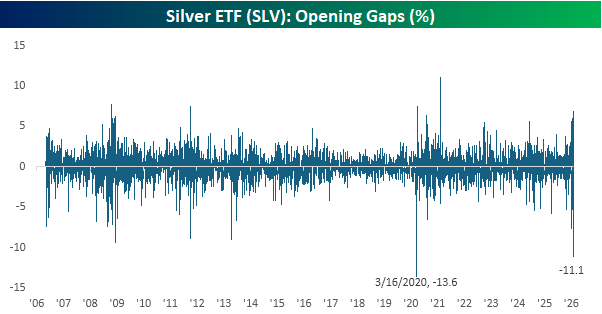

As if yesterday’s session wasn’t enough volatility for you, this morning, the SLV ETF is on pace to gap down 11.1%, which would be just the second time in its history that it opened down more than 10%. The only larger downside gap was a 13.6% decline on 3/16/20 during the heart of the Covid crash. In terms of yesterday’s range and today’s downside gap, recent activity in SLV is right up there with levels of volatility we saw during major market crises. What’s the issue this time around? The really amazing part about today’s downside gap in SLV, though, is that if current levels hold through the end of the day, it will still be up on the week!

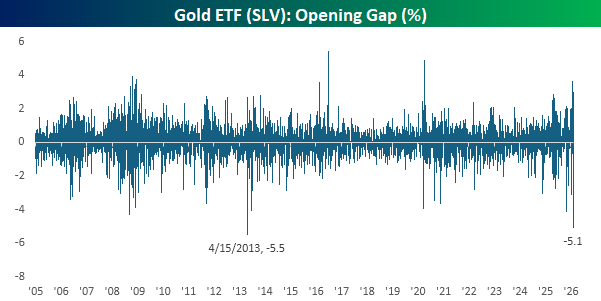

Not to be left out of the volatility party, gold is also poised for a rough start today. The Gold ETF (GLD) is on pace to gap down 5.1%, which would also be the second-largest downside gap in its 20+ year trading history. The only larger downside gap was on Tax Day in 2013, when GLD gapped down 5.5%. Like SLV, though, if current levels hold through the end of the trading day, GLD would also finish the week with a gain!

Jan 29, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You can fool some of the people some of the time — and that’s enough to make a decent living.” – W.C. Fields

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It was only a 0.01% decline, but the S&P 500’s drop yesterday ended a streak of five straight gains. The Nasdaq managed to finish up 0.17%, extending its winning streak to six. This morning, both indices are trading higher, so for the Nasdaq will today be lucky number seven? While Meta (META) and Tesla (TSLA) are doing their part to extend the Nasdaq’s streak, Microsoft (MSFT) is trading the other way after weak margin guidance has that hyperscaler trading down a not so lucky 7% this morning.

Outside of treasuries, the 10-year US Treasury yield is basically unchanged at 4.25%, while the dollar is little changed after a volatile few days to start the week. Precious metals continue to get more precious this morning, with gold up over 4% and breaking through $5,500 per ounce. Silver is up over 5%, platinum is up nearly 5%, and copper is also at a record, trading up close to 7%. For all three metals, their year-to-date gains are leaving equities in the dust.

In Asia overnight, the Nikkei was basically unchanged, but South Korea rallied another 1% as SK Hynix reported strong Q4 results. Hong Kong, China, and India were also higher on the session, while Australia had a marginal decline.

European stocks are mostly higher this morning as the STOXX 600 gains 0.5%, but Germany has been a major outlier with a decline of nearly 1% as earnings results from SAP weigh on the DAX. A January survey of Business and Consumer sentiment came in stronger than expected, showing an unexpected increase relative to December.

With the Federal Reserve behind us, investors will now turn back to earnings and economic data. Earnings this morning have been OK, with EPS and revenue beat rates for the morning coming in at about 67%. The economic calendar is also busy with Non-Farm Productivity, Unit Labor Costs, and jobless claims at 8:30, followed by Factor Orders and Wholesale Inventories at 10 AM.

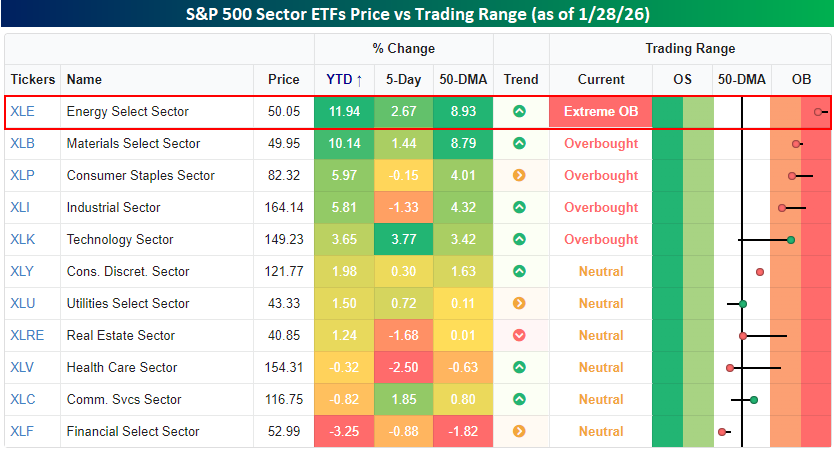

In yesterday’s note, we highlighted the strength in the Energy and Materials sectors and how they were leading all other sectors in terms of year-to-date returns. Through yesterday’s close, Energy and Materials were still leading the performance derby, but Energy is the only sector that remains in ‘extreme’ overbought territory (more than two standard deviations above its 50-DMA). Behind Technology, which has had a run this week, Energy is also the best-performing sector over the last five trading days.

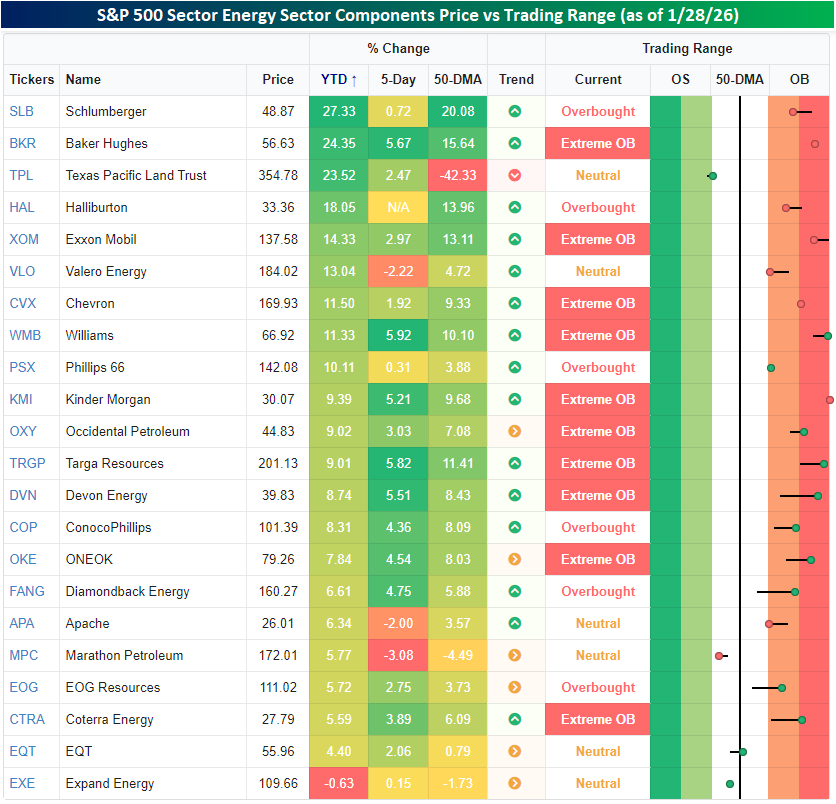

Crude oil prices are up over 12% this year, and natural gas enjoyed a surge during the cold snap, although the contract roll has brought front-month futures prices back down to a three-handle this morning. You don’t have to look any further than these moves in the underlying commodities to understand why energy stocks are doing so well, but strength within the sector, while broad-based, hasn’t been uniform.

As shown in the snapshot below, all but one of the sector’s 20+ components are up YTD. The only outlier is Expand Energy (EXE), which is fractionally lower for the year. On the upside, the two leading stocks in the sector this year have been Schlumberger (SLB) and Baker Hughes (BKR), with gains of more than 20%. Both stocks gapped sharply higher following the early January arrest of Maduro in Venezuela and basically haven’t looked back since. Of the nine stocks in the sector up at least 10%, though, there’s been a smorgasbord of exploration companies, integrated oil companies, and even refiners.

Jan 28, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Union Pacific’s (UNP) Q4 2025 earnings call.

Union Pacific (UNP) operates one of North America’s largest freight rail networks, spanning 23 states across the western two-thirds of the United States. The company moves coal, grain, chemicals, intermodal containers, automotive products, and industrial materials, serving as a critical link in American supply chains. UNP’s performance can speak to the health of the US industrial economy, agricultural exports, energy markets, and truck-to-rail transportation. UNP reported record full-year results with EPS of $11.98 (up 8%), despite 4% volume decline in Q4. The company set best-ever records across safety, freight car velocity (239 miles/day), and terminal dwell (19.8 hours), the average time a railcar sits idle between trips. However, management issued conservative 2026 guidance with mid-single-digit EPS growth, citing 4%+ rail inflation, weak pricing power in agricultural and domestic intermodal markets, and deteriorating macro indicators. The pending $85 billion Norfolk Southern merger dominated the discussion. The STB requested additional information, including walk-away terms, delaying the application but not changing the first-half 2027 closing target. Management expressed confidence in approval, emphasizing competitive benefits and customer optionality. Reporting in-line EPS on a revenue miss, UNP shares rose 0.7% on 1/27…

Continue reading our Conference Call Recap for UNP by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan