Mar 12, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dick’s Sporting Goods’ (DKS) Q4 2025 earnings call.

Dick’s Sporting Goods (DKS) is one of the largest sporting goods retailers in the US, selling athletic footwear, apparel, equipment, and outdoor gear through stores and digital channels. The company serves athletes, teams, and casual sports enthusiasts while increasingly positioning itself at the intersection of sports and culture. Its growing ecosystem includes experiential retail concepts like House of Sport, youth sports platform GameChanger, and a retail media network that connects brands directly with athletes and fans. Management highlighted steady consumer demand and strong product momentum across footwear, apparel, and hardlines, with Q4 comparable sales up 3.1% on top of a 6.6% comp last year, producing a nearly 10% two-year stack. Executives emphasized that shoppers are still spending on innovation and premium launches, especially in running, basketball, and women’s sports, while major events like the 2026 World Cup are expected to support demand. The biggest focus remains the turnaround of Foot Locker following its acquisition, where DKS is implementing its “Fast Break” merchandising reset, removing roughly 30% of unproductive SKUs and testing store redesigns that are generating strong comps. Meanwhile, experiential formats like House of Sport and Fieldhouse continue to expand, and digital platforms such as GameChanger and the Dick’s Media Network are emerging as new engagement and advertising channels. The company guided to 2%–4% comps in 2026 with Foot Locker expected to inflect around back-to-school. DKS shares opened 4.6% higher on 3/12 after reporting EPS and revenue beats…

Continue reading our Conference Call Recap for DKS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Mar 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great things are not accomplished by those who yield to trends and fads and popular opinion.” – Jack Kerouac

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Money Movers yesterday to discuss the moves in the energy market and their impact on the equity market. To view the segment, click on the image below.

After a mixed session yesterday where the Nasdaq finished up 8 basis points (bps) while the S&P 500 fell 8 bps, US futures are firmly lower this morning, with the S&P 500 and Nasdaq both indicated to open down by about 35 bps. The primary culprit is crude oil, where prices are up over 5% and back above $90 as Iran stepped up attacks on tankers in the Persian Gulf. Energy Secretary Chris Wright was also just on CNBC and noted that the US is not yet ready to escort tankers through the Strait of Hormuz, but could be mobilized later this month. As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy.

With crude oil prices rising, treasury yields are higher again as investors focus on the potential inflationary impacts. Gold prices are essentially flat, silver is up 2%, and Bitcoin is down fractionally but still above $70K.

Stocks were down across the board in Asia overnight, as the Nikkei was down 1.0%, while China’s Shanghai Composite was only down 0.1%, and the Kospi fell 0.5%. Relative to the last two weeks, it was a muted session! Given the spike in crude oil prices and the region’s dependence on energy imports, you could make the argument that it could have been worse.

In Europe, equities are also taking the overnight spike in crude oil prices in stride. The STOXX 600 is down just 0.4%, while Germany is fractionally higher. We’re also starting to see impacts of the conflict showing up in corporate results as UK travel firm On the Beach lowered guidance, citing a sharp slowdown in travel bookings for locations in the Eastern Mediterranean.

On the economic calendar this morning, we just had jobless claims, Building Permits, and Housing Starts at 8:30. Initial claims came in 2K lower than expected, while continuing claims were 1K higher, so from this perspective at least, the labor market remains very well behaved. With respect to the housing numbers, permits were lower than expected (1376K vs 1410K) while starts were much higher than expected (1487K vs 1341K), although much of the strength was due to multi-family units.

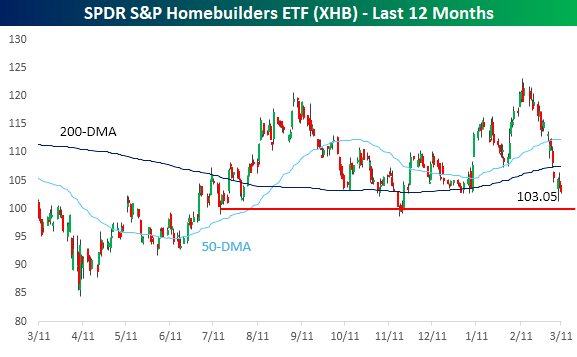

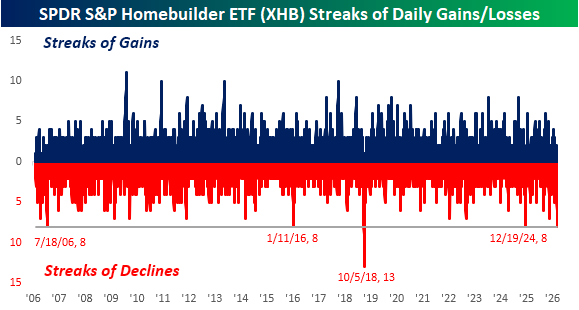

With treasury yields moving higher, it’s been a rough month for homebuilder stocks. The SPDR S&P Homebuilder ETF closed at $121.36 on 2/13, but has since declined more than 15% through yesterday’s close. Those highs in February were enough to push the group to 52-week highs, but the gains for 2026 quickly evaporated, and it’s now close to testing support at the $100 level.

Part of that 15% decline since the February highs includes what is now an eight-day losing streak, which is tied for the longest losing streak in the ETF’s entire history. The last time there was a streak this long was over a year ago in late 2024, and the only longer streak was 13 days ending in October 2018.

Mar 11, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Oracle’s (ORCL) Q3 2026 earnings call.

Oracle (ORCL) develops enterprise software, databases, and cloud infrastructure used by companies and governments to run core operations like finance, HR, supply chains, banking systems, and healthcare records. Its flagship technologies include the Oracle Database, Fusion ERP/HCM applications, and Oracle Cloud Infrastructure (OCI), which competes with hyperscalers in AI computing and cloud services. Oracle’s Q3 fiscal 2026 call centered on explosive growth tied to AI and cloud adoption. Multicloud database revenue surged 531% YoY, while AI infrastructure grew 243%, with management saying demand for GPU and CPU compute still exceeds supply. The company has secured 10+ gigawatts of future data-center power capacity and signed $29B in new infrastructure contracts, while its remaining performance obligations climbed to $553B. Oracle is embedding AI directly into enterprise software, with 1,000+ AI agents already inside its applications, and executives argued AI will strengthen, not replace, large enterprise SaaS platforms. A major push is also underway to run Oracle databases across Microsoft Azure, Google Cloud, and AWS, accelerating cloud migrations as companies move sensitive data to environments where it can be used with AI. ORCL shares rose as much as 12.5% on 3/11 after posting better-than-expected results…

Continue reading our Conference Call Recap for ORCL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Mar 11, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers AeroVironment’s (AVAV) Q3 2026 earnings call.

AeroVironment (AVAV) is a US defense technology company that develops autonomous drones, loitering munitions, counter-drone systems, directed-energy weapons, and space communications technologies for the US military and allied nations. Its portfolio includes battlefield-proven systems like the Switchblade loitering munition, Puma and Jump reconnaissance drones, Titan RF counter-UAS (Uncrewed Aircraft System) jammers, and the LOCUST directed-energy anti-drone system. AVAV reported a mixed quarter, with results missing expectations due to government funding delays, supply-chain shipping issues, and the termination of the Space Force’s SCAR (Satellite Communication Augmentation Resource) program. Despite the short-term setback, management emphasized strong underlying demand, pointing to $1.1B in funded backlog and $4.6B in year-to-date awards, and guided for record Q4 revenue with FY26 sales expected between $1.85B–$1.95B. The company is ramping production aggressively, including a new 140,000-sq-ft Utah factory capable of producing $2B of systems annually, to meet surging demand for Switchblade drones, Titan counter-UAS systems, and reconnaissance platforms. Management repeatedly linked demand growth to current geopolitical tensions, noting that conflicts involving large-scale drone warfare, including Iran’s regional attacks, are accelerating global military demand for both offensive drones and defensive counter-drone systems. Shares fell as much as 10% on 3/11…

Continue reading our Conference Call Recap for AVAV by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Mar 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I attack ideas. I don’t attack people. Some very good people have some very bad ideas.” – Antonin Scalia

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be on CNBC at 11 AM Eastern to discuss markets and today’s CPI.

Futures were in a holding pattern ahead of today’s CPI, with the S&P 500 and Nasdaq both indicated to open down about 0.1% despite Oracle (ORCL) trading up over 10% in reaction to earnings. Treasury yields moved higher ahead of the report, with the 10-year yielding 4.17%, and crude oil was up over 4% to $87 per barrel. Gold and Bitcoin prices are down about 1%.

For Asian equities, the last several days have been something of an all-or-nothing trade where the major averages in the region are either all sharply higher or lower. Last night, there was more dispersion. While Japan and South Korea were both up 1.4%, Hong Kong was fractionally lower, and India declined 1.7%. In South Korea, exports for the first 10 days of March were up 55.6% y/y, with chip exports surging more than 175%. In Japan, PPI fell 0.1% versus expectations for an increase of 0.1%.

In Europe, the move was more uniform, and unfortunately for bulls, it was mostly lower. The STOXX 600 is down nearly 0.5%, with Germany leading the losses with a decline of nearly 1% as German CPI for February rose 0.2%, which was right in line with forecasts.

In the US, the only economic report on the calendar today is February CPI, which given the events of the last two weeks, has become much less pertinent to the market. While it may not be a major focus of the market this morning, CPI was right in line with expectations as headline increased 0.3% m/m and core increased 0.2%

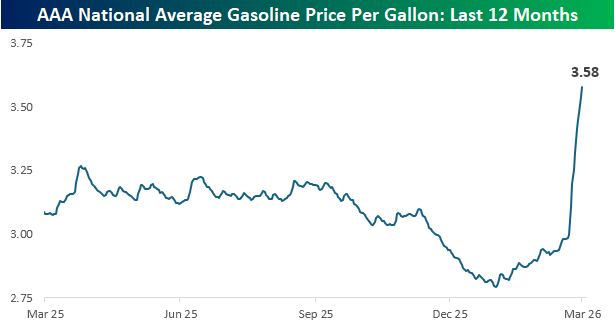

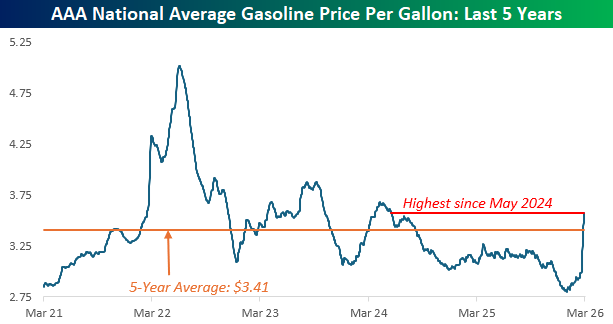

Through yesterday’s close, average prices at the pump have now surged to $3.58 per gallon, which represents a 20% increase this month alone. In the span of two months, prices have spiked from a 52-week and multi-year low to a 52-week high, easily surpassing the prior peak from last spring.

As shocking as the one-year chart looks, taking a longer-term look at crude oil prices shows a less dire picture. Current gasoline prices are now at the highest level since May 2024, but they’re still nearly 30% below the 5-year peak from June 2022, and less than 5% above the 5-year average. That doesn’t make it any easier to stomach, but at least it provides some decent perspective.

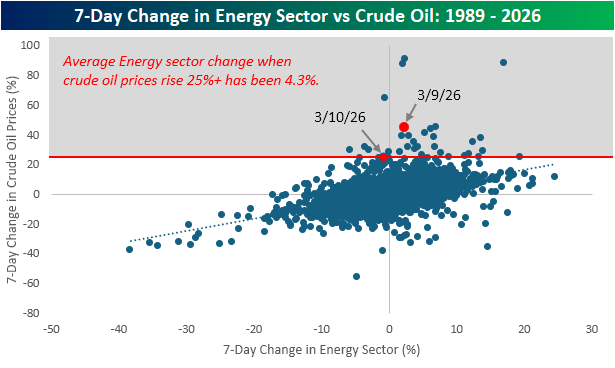

In the seven trading days since the war on Iran started, crude oil prices are up 25%, and as of yesterday, the seven -day change was over 45%. With such large increases, it seems like a disconnect that the S&P 500 Energy sector is up just 2%. The chart below compares the 7-day change in the S&P 500 Energy sector to the 7-day change in crude oil prices. While there has historically been a positive correlation between the two, in periods when crude oil prices have spiked 25% or more, the average change in the Energy sector has been a gain of 4.3%. The implication of those muted gains? The market views these price spikes as temporary.

Mar 10, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Kohl’s (KSS) Q4 2025 earnings call.

Kohl’s (KSS) is a US department store chain with roughly 1,150 locations that sells apparel, footwear, home goods, beauty, and accessories, targeting primarily low- to middle-income households. The retailer blends national brands with a large portfolio of proprietary labels (Sonoma, LC Lauren Conrad, Tek Gear, Jumping Beans) and has leaned heavily on its Sephora at Kohl’s shop-in-shop partnership to attract younger shoppers and drive traffic. Kohl’s is a useful barometer for value-oriented discretionary spending in the US. The company reported a difficult but stabilizing quarter as comparable sales fell 2.8% and net sales declined 3.9%, though EPS of $1.07 benefited from tight inventory control and expense cuts. Management attributed weak traffic largely to financially strained value consumers and admitted missteps in fall seasonal inventory allocation and insufficient promotional intensity during key holiday periods like Black Friday and Cyber Monday. The turnaround strategy centers on restoring proprietary brands, sharpening price points (including more $10-and-under items), improving “trip assurance” by increasing inventory depth, and driving traffic through Sephora, impulse merchandising, and digital improvements. Digital sales rose low single digits, but conversion remains an issue. Guidance for 2026 calls for comps between down 2% and flat with EPS of $1.00–$1.60, reflecting cautious expectations as lower-income shoppers remain pressured by macro conditions. KSS reported a revenue miss on stronger EPS, as the stock rose as much as 11% on 3/10, but completely erased those gains intraday…

Continue reading our Conference Call Recap for KSS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan