Jan 21, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Halliburton’s (HAL) Q4 2025 earnings call.

Halliburton (HAL) is a global company specializing in oilfield services, covering the entire lifecycle of a reservoir. It manufactures high-tech drilling equipment and provides essential services like hydraulic fracturing, cementing, and well construction. The company serves major national oil companies and independent producers across 70 countries. As the primary barometer for the North American shale market, Halliburton provides insights into global energy demand and the transition toward long-term energy security. HAL delivered $5.7 billion in revenue for Q4, above estimates of $5.4 billion. While North American revenue dipped 7% due to softer land activity, international markets surged 7%, particularly in Latin America and the North Sea. The dominant theme was a market rebalancing in 2026. Management expects equipment attrition to tighten the market quickly if demand rises. The most striking update was a potential rapid re-entry into Venezuela, where HAL could mobilize in weeks once legal terms are finalized. Additionally, a new 400 MW commitment for modular power systems positions the company to capitalize on the Eastern Hemisphere’s growing data center and AI infrastructure needs. HAL shares rallied close to 5% on 1/21 in reaction to better-than-expected results…

Continue reading our Conference Call Recap for HAL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jan 21, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A country, a style or an epoch are interesting only for the idea behind them.” – Christian Dior

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The week started on a down note, and as we approach the opening bell for the second trading day of the week, futures aren’t indicating anything in the way of a turnaround, as a previously modestly higher picture has turned red. Treasury yields are basically flat, while crude oil is modestly higher. Investors continue to pile into gold, though, as futures are up another 2%+. Unlike other days when gold rallies, though, other precious metals are seeing much more modest gains. Bitcoin is also lower once again and firmly back below $90K.

Outside of the US, Asian markets were mixed. The Nikkei was down 0.4%, but Hong Kong, China, and South Korea bucked the trend with modest gains. In Europe, the picture is much more uniform as major equity markets are down across the board. The STOXX 600 is down 0.6% with Germany leading the way lower.

For US markets this morning, we’ll get Leading Indicators, Construction Spending, and Pending Home Sales at 10 AM, but the main focus will be on Davos, where President Trump is scheduled to speak right about now.

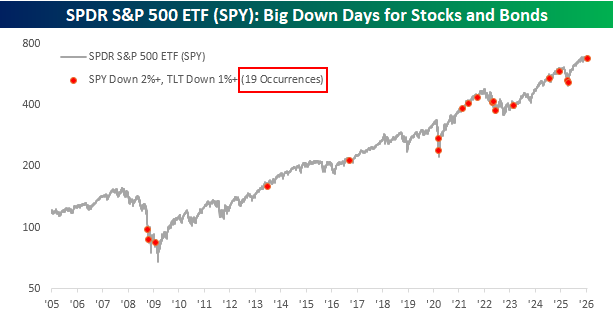

Yesterday was an interesting day in markets as the S&P 500 ETF (SPY) fell over 2% while long-term Treasuries, as proxied by the ETF TLT, also declined by over 1%. On their own, the weakness in both asset classes was hardly unprecedented. Since the start of 2005, there have been 212 other days when SPY fell more than 2%. For TLT, declines like yesterday are even more common, with 627 other one-day drops of at least 1%.

What made yesterday’s drops in both ETFs more notable was that they occurred in tandem with each other. Since the start of 2005, there have only been eighteen other days when SPY fell over 2%, and TLT dropped by more than 1% on the same day. The chart below shows the performance of SPY since the start of 2005, and the red dots indicate each of those other occurrences. There were multiple occurrences near the lows of the Financial Crisis in late 2008/early 2009. From mid-2009 up until the onset of Covid, there were only two other occurrences, but in the post-Covid era, the frequency of occurrences has been much more common as higher inflation has acted as a secular headwind for bonds and a tailwind for gold.

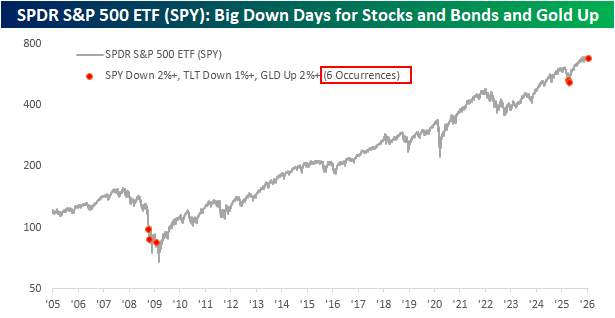

As uncommon as it is for the S&P 500 to drop at least 2% and long-term treasuries (TLT) to fall over 1% on the same day, what makes yesterday even more of an outlier is that Gold also surged more than 2%.

A 2%+ rally in Gold, on its own, isn’t all that uncommon. Yesterday was the 183rd occurrence since the start of 2005 and the 17th in just the last year, but this type of rally practically never happens on a day when the S&P 500 falls over 2% and long-term treasuries fall more than 1%. Since the start of 2005, it’s only happened five other times!

Following the President’s rhetoric towards Europe, and Greenland specifically, over the weekend, concerns over a pickup in the sell America trade started to resurface again yesterday, and the moves in US stocks, bonds, and gold yesterday could easily fit into that narrative. If global investors were looking to “sell America,” this is exactly the type of price action you would expect to see. But if investors were selling America, what were they buying?

Accounting for the losses on Monday when US markets were closed, there wasn’t a lot of buying in global stocks. Europe’s STOXX 600 was down about 2% from Friday’s close through Tuesday, and the Nikkei was down just as much. There wasn’t a lot of buying to be found in international bonds either, as yields in Europe also moved higher, and JGB yields surged to multi-decade highs.

For now, it probably makes more sense to write off yesterday’s moves as a one-off and potentially traders just trying to front-run any potential sell-America trade, but investors should keep a close eye on how the markets react in the days ahead. What makes yesterday’s drops in stocks and bonds while gold rallied stand out even more though, was in where it occurred in the market cycle. As shown in the chart below, of the five other times when SPY fell over 2%, TLT fell more than 1%, and GLD rallied at least 2%, three occurred deep into the Financial Crisis, and the other two occurred right near the lows of the tariff-tantrum. Yesterday’s occurrence came just after the S&P 500 closed the prior session within 1% of an all-time high.

Jan 20, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a discussion of US financial asset purchase by the rest of the world in addition to a checkup on major index technicals (page 1). We then provide a decile breakdown of today’s declines (page 2) before finishing with a rundown of the latest Philly Fed numbers (page 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jan 20, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Fastenal’s (FAST) Q4 2025 earnings call.

Fastenal (FAST) is a maker of industrial and construction supplies, specializing in fasteners, safety gear, and MRO (Maintenance, Repair, and Operations) products. Beyond simple retail, the company is a supply chain powerhouse that embeds itself into customer workflows through Onsite locations (miniature warehouses inside client facilities) and FMI (Fastenal Managed Inventory) technology, an automated network of industrial vending machines and smart bins. FAST serves heavy manufacturing and construction clients, governments, and data centers. Fastenal capped a recovery year with a strong Q4, posting $2.03 billion in sales (up 11%) and record annual revenue of $8.2 billion. Despite a “sideways” industrial economy and mixed signals from the PMI, the company achieved market share gains by pivoting toward large-account “ultra-high spend” sites ($50K+ monthly), which now account for over half of revenue. A key highlight was the acceleration of FAST’s digital moat: FMI and eBusiness now represent 62.1% of sales, creating sticky relationships that outperformed the broader market. Looking toward 2026, FAST anticipates continued double-digit growth, supported by a fresh leadership transition with Jeff Watts named as the next CEO. FAST reported a revenue beat on in-line EPS, resulting in a loss as much as 5% for the stock on 1/20…

Continue reading our Conference Call Recap for FAST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jan 20, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers D.R. Horton’s (DHI) Q1 2026 earnings call.

D.R. Horton (DHI) is the largest homebuilder in the United States by volume. The company designs and constructs high-quality, attainable homes primarily for entry-level and first-time buyers, who represent over 60% of its business. Its scale spans 126 markets across 36 states, providing insight into the health of the American consumer and the broader housing market. Management reported a disciplined start to 2026, beating revenue expectations with $6.9 billion despite “cautious consumer sentiment.” To combat affordability headwinds, DHI aggressively utilized mortgage rate buy-downs, maintaining a floor as low as 3.99% for some buyers. This strategy successfully drove a 3% increase in net sales orders. A key focus this quarter was “rightsizing” product; the builder is transitioning to smaller floor plans and higher-density communities to lower monthly payments. Despite broader economic uncertainty, the company reiterated its guidance to close up to 88,000 homes this year. On better-than-expected results, DHI shares opened 2.9% lower on 1/20, though erased most of the losses intraday…

Continue reading our Conference Call Recap for DHI by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jan 20, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Remember, your mind is like a parachute: If it isn’t open, it doesn’t work. So keep an open mind!” – Buzz Aldrin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If this is the price we pay for a three-day weekend, maybe we should have kept the market open. It’s looking like a terrible Tuesday for US equities as the S&P 500 is poised to open down 1.4% while the Nasdaq is indicated 1.7% lower. Over the weekend, President Trump escalated his rhetoric towards Greenland and threatened tariffs on European allies if a deal isn’t reached. Today also marks the first anniversary of Trump’s second inauguration, and it’s been eventful to say the least.

Equity indices in Asia were weak, given the declines in US equity futures and the global trade tensions. The Nikkei was down over 1%, but India was the only other country down more than 1%. South Korea’s KOSPI declined 0.4%. Yes, you read that correctly- South Korean stocks had a daily decline for the first time in 2026. The more concerning aspect of the weakness in Asia, though, is in the bond markets where JGB yields are surging to multi-decade highs in their biggest one-day moves since the Liberation Day turmoil last April.

European stocks are much weaker this morning, and in early trading, the STOXX 600 is down 1.3%. Spain is leading the declines with a drop of 1.7%, followed by Germany (-1.6%), and Italy (-1.5%). The weakness this morning stems from President Trump’s announcement over the weekend that he would put tariffs of 10% on the imports of eight European countries beginning on 2/1, which will increase to 25% on 6/1, if no deal is reached on Greenland. Making matters worse are reports that the President will put 200% tariffs on imports of French wine if French President Macron refuses to join the Gaza Board of Peace.

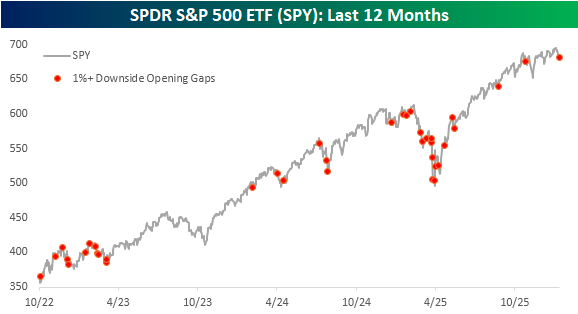

Whenever we see large declines like the market is poised for this morning, it always helps to put the move in perspective. The chart below shows SPY’s performance during the current bull market, and the red dots indicate every other time that SPY gapped down at least 1%. While today’s occurrence is only the third in the last eight months, since October 2022, there have been 37 other occurrences, which works out to an average of once per month.

Today’s gap down in SPY comes as the market has been stuck in a holding pattern for the last several weeks. Based on pre-market trading, SPY is trading right now at the same levels it traded in back in late October.