Aug 19, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Viking’s (VIK) Q2 2025 earnings call.

Viking (VIK) is a leading operator of river, ocean, and expedition cruises, built around culturally immersive, destination-focused travel. Its fleet spans 85 river vessels and 12 ocean ships, all designed with a uniform, understated luxury (no casinos, no children, and no nickel-and-diming) that appeals to affluent, “culturally curious” travelers, particularly older demographics seeking comfort and enrichment. Viking controls or has priority access to over 100 docking sites worldwide, giving it a competitive moat in river cruising. The company provides insight into global travel demand trends, discretionary spending patterns among wealthier consumers, and how tourism is shifting toward experiential, high-end travel. Viking reported an 18.5% revenue increase in Q2 2025, fueled by 8.8% capacity growth and an 8% rise in net yields. Bookings remain robust: 96% of 2025 capacity is already sold, and 2026 is 55% booked at higher rates. Egypt and India itineraries sold out quickly, showing strong demand for new cultural destinations. The company highlighted river versus ocean dynamics, river pricing accelerated while ocean moderated slightly, but both segments maintain high occupancy above 95%. Management stressed that marketing, not discounting, is their lever when demand softens. VIK posted better-than-expected revenue on in-line EPS, though the stock fell 5.5% at the open on 8/19…

Continue reading our Conference Call Recap for VIK by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 19, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Palo Alto Networks’ (PANW) Q4 2025 earnings call.

Palo Alto Networks (PANW) is the world’s largest pure-play cybersecurity firm, serving enterprises, governments, and critical infrastructure across the globe. Best known for pioneering the next-generation firewall, the company now offers an integrated portfolio spanning network security, cloud security, and AI-driven security operations. Its platform-based model helps organizations consolidate fragmented security tools into unified systems, improving both outcomes and cost efficiency. Fiscal Q4 2025 marked a milestone as PANW became the first dedicated cybersecurity company to surpass a $10B revenue run rate. Management leaned heavily into AI security, highlighting Prisma AIRS and AI Access as demand surges (GenAI traffic up 890% YoY). Platformization dominated deal flow, including a $100M+ consulting firm win, driving net retention to 120%. Network Security momentum came from SASE (ARR +35% YoY) and Prisma Access Browser (3M licenses sold in Q4). Cortex/XSIAM continued to scale, cutting response times to under 10 minutes for many clients. The proposed CyberArk acquisition would make identity a new platform pillar. Despite global tariff uncertainty, US-based manufacturing insulated margins. The company’s triple play is its first since 2022, and the stock popped 6.4% at the open on 8/19 as a result…

Continue reading our Conference Call Recap for PANW by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 13, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 24 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Below is a blurb from our newest Triple Play Report to give you an idea of the insights that are included in this piece.

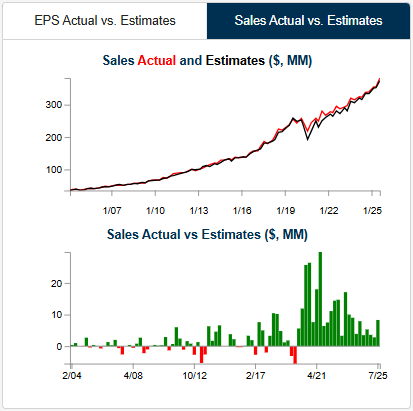

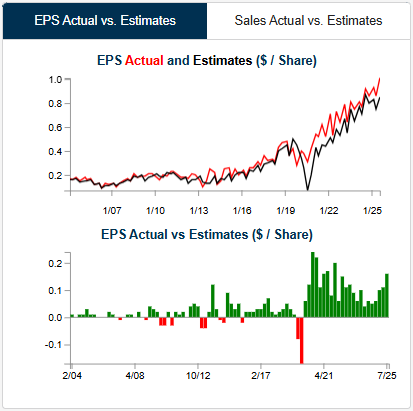

Merit Medical (MMSI) is a medical device maker involved in cardiology, radiology, endoscopy, and dialysis access maintenance. Its catheters, stents, embolization products, and hemostatic solutions are designed to improve procedural efficiency and patient outcomes. MMSI sells primarily to hospitals, outpatient centers, and physician offices. Recent growth has been fueled by acquisitions such as Cook Medical’s lead management portfolio, EndoGastric Solutions’ assets, and BioLife’s patented StatSeal and WoundSeal products, which expand MMSI’s offerings in high-value niches like vascular closure, indwelling catheter bleeding control, and cardiac intervention.

Below is a look at EPS and sales versus consensus estimates for MMSI from our Earnings Explorer tool. Notably, MMSI has beaten both top and bottom line estimates on each of its last 23 quarterly reports dating back to the start of 2020, and as you can see in the charts, both have been trending sharply higher. In addition to the strong EPS and sales results, MMSI completed the triple play this quarter by raising guidance. Shares reacted positively with a gain of 2.3% on its earnings reaction day on 7/31, but the stock didn’t quite see the “pop” that most triple plays do on such strong results.

The most interesting thing we heard on MMSI’s triple-play earnings call this quarter was related to tariffs. As a maker of all kinds of medical devices, MMSI estimated earlier in the year that tariffs would cost the company roughly $26 million. On this call, however, the company noted that the easing of tariffs had cut their cost-impact estimates down to just $7 million at the high end.

Several other triple-play companies have also provided positive news on the tariff front recently.

You can read more about MMSI and the 23 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Aug 7, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Zillow’s (ZG) Q2 2025 earnings call.

Zillow (ZG) is a digital real estate platform that connects home buyers, sellers, renters, and real estate professionals through a comprehensive suite of tools, listings, and services. Best known for its Zestimate feature and mobile-first experience, Zillow has evolved into a transaction-focused ecosystem, offering mortgage origination through Zillow Home Loans, property management tools, and its agent CRM, Follow Up Boss. It operates the #1 rental and for-sale real estate websites in the US, with an average of 243 million monthly unique users. Zillow reported 15% revenue growth YoY, outperforming a flat housing market, with standout gains in rentals (up 36%) and mortgages (up 41%). Multifamily listings rose 45% to 64,000, supported by expanded distribution via Redfin and Realtor.com. Enhanced markets drove 27% of connections, with Zillow Home Loans adoption in the double digits and expected 40%+ origination growth in Q3. Product innovation was a major theme, including AI-powered agent tools, the immersive SkyTour feature, and the affordability-focused BuyAbility tool. Executives maintained a confident tone on reaching 2025 goals, despite macro housing stagnation and affordability headwinds. ZG shares recorded an up-and-down day on 8/7 after posting mixed results…

Continue reading our Conference Call Recap for ZG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 7, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Duolingo’s (DUOL) Q2 2025 earnings call.

Duolingo (DUOL) is the world’s most popular language-learning platform, offering gamified courses in over 40 languages through its mobile app and website. The company has expanded into adjacent educational verticals like math, music, and, most recently, chess. Duolingo serves a wide global user base, with particularly strong growth among English learners in Asia. Its tiered subscription model, including Super and Max plans, supports both free and paid users. What makes Duolingo stand out is its use of AI to personalize learning experiences at scale and its viral, irreverent brand voice. Duolingo posted another strong quarter, raising full-year guidance on the back of 40% DAU (Daily Active User) growth, an 8% Max subscriber mix, and record profitability. Growth in Asia (especially China, boosted by a Luckin Coffee partnership) was a standout. The company highlighted progress in its new “Energy” system, which has lifted DAUs, revenue, and time spent, while drawing some user backlash. AI-related costs fell as token prices dropped, improving gross margins. Video Call remains the “killer feature” of Max, and the team is adding bilingual dialogue and engagement-based fine-tuning. Social media strategy was reined in after controversial AI remarks, affecting US virality but now stabilizing. The stock was up as much as 31% on 8/7 after the triple play but gave up half of those gains intraday…

Continue reading our Conference Call Recap for DUOL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 7, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cheniere Energy’s (LNG) Q2 2025 earnings call.

Cheniere Energy (LNG) is the largest producer and exporter of liquefied natural gas (LNG) in the United States and a top-five global LNG supplier. Operating major export terminals at Sabine Pass (Louisiana) and Corpus Christi (Texas), Cheniere transforms US shale gas into LNG for delivery to over 45 countries. The company serves utilities, energy companies, and governments, offering flexible, long-term supply contracts that help anchor energy security worldwide. What sets Cheniere apart is its vertically integrated, brownfield-driven growth model, expanding capacity through debottlenecking and modular additions rather than full greenfield builds. The company finalized FID (Final Investment Decision) on Corpus Christi Midscale Trains 8 & 9 and achieved substantial completion of Train 2 in Stage 3. Debottlenecking added about 1 MTPA (Million Tons Per Annum) in capacity at low cost, while a new 1 MTPA long-term contract with JERA (Japan) marked a strategic commercial milestone. Management emphasized robust LNG demand in Europe (up 25% YoY) and a strong long-term outlook in Asia despite short-term softness. LNG shares hovered around flat in 8/7’s session despite stronger-than-expected results…

Continue reading our Conference Call Recap for LNG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan