Jul 30, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Booking’s (BKNG) Q2 2025 earnings call.

Booking (BKNG) is the world’s largest online travel platform, operating global brands like Booking.com, Priceline, Agoda, KAYAK, and OpenTable. It facilitates millions of accommodations, flights, car rentals, and restaurant reservations, serving both leisure and business travelers. Its Genius loyalty program and Connected Trip vision (bundling multiple travel components into one seamless booking) position it to drive both engagement and margins. Booking delivered a standout quarter, with room nights up 8%, gross bookings up 13%, and adjusted EPS up 32% YoY. Alternative accommodations grew 10%, outpacing hotels, and the Connected Trip saw 30%+ transaction growth. Asia was the fastest-growing region, while US consumers showed caution via shorter stays and lower ADRs. AI tools like Priceline’s Penny and OpenTable’s Concierge are boosting efficiency and conversion, and direct bookings now exceed 65% of B2C volume. BKNG shares were up less than 1% on 7/30 on EPS and revenue beats…

Continue reading our Conference Call Recap for BKNG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jul 30, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Polaris’ (PII) Q2 2025 earnings call.

Polaris (PII) is a manufacturer of powersports vehicles, including off-road vehicles (ORVs), snowmobiles, motorcycles (Indian and Slingshot), and marine products, like Bennington pontoons. Polaris dominates niche markets such as utility and recreational side-by-sides, offering high-quality vehicles with strong dealer support. The company serves outdoor enthusiasts, farmers, commercial users, and lifestyle buyers, while also providing parts, gear, and accessories to enhance the ownership experience. Polaris exceeded expectations despite a 6% sales decline, driven by industry weakness and tariffs. Share gains across every segment were fueled by standout products like the XPEDITION and the newly launched RANGER 500, targeting value-focused buyers at $9,099. Tariffs remain a headwind, with an estimated $230M annualized impact, though the company has cut its China sourcing by nearly half and aims to reduce exposure by 35% by year-end. Retail demand was flat but stable, with utility vehicles showing strength, while promotions and interest rates pressured margins. PII shares were up 16.9% on 7/29 after posting stronger than expected results and launching new vehicles…

Continue reading our Conference Call Recap for PII by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jul 30, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers JetBlue’s (JBLU) Q2 2025 earnings call.

JetBlue (JBLU) is a US-based low-cost carrier, offering free in-flight Wi-Fi, live TV, and extra legroom options. Serving leisure and value-conscious travelers across the US, Latin America, and transatlantic routes, JBLU operates a primarily Airbus fleet, including its efficient A220 and A320 aircraft. The company also runs a growing travel products business through its Paisly platform and has built a loyal following through its TrueBlue rewards program. JBLU delivered a modest operating profit in Q2 as it advanced its JetForward transformation, generating $180M in EBIT YTD. The standout announcement was Blue Sky, a new partnership with United Airlines that enables cross-selling, loyalty integration, and Paisly white-label expansion. It is expected to drive $50M in incremental EBIT by 2027. Close-in bookings surged mid-quarter, particularly around peak travel, though management remains cautious about calling the shift permanent. The forecast for grounded aircraft tied to Pratt & Whitney engine issues improved, clearing a path for low single-digit capacity growth in 2026. The stock was up 6.7% on 7/29 on better-than-expected results…

Continue reading our Conference Call Recap for JBLU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jul 30, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 21 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

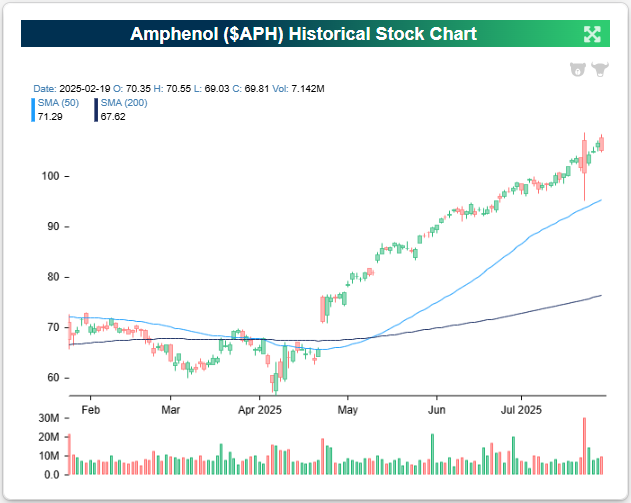

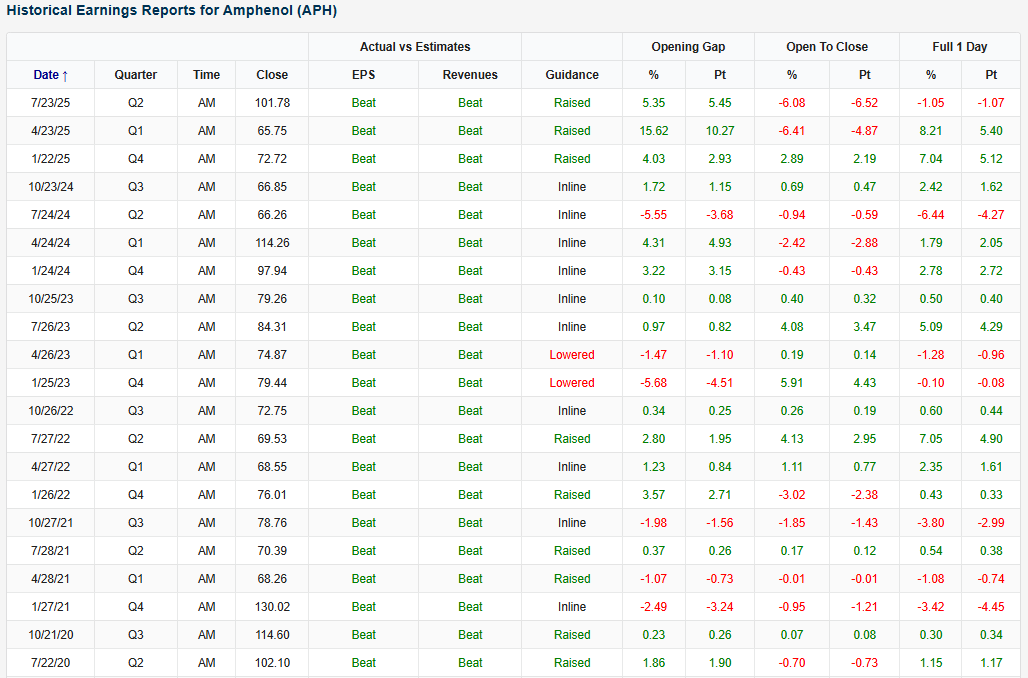

Amphenol (APH) is an example of a company that recently reported an earnings triple play before the open on 7/23. It was the company’s third straight triple play, but the stock turned negative that day after the positive moves in reaction to the two prior triple plays.

Here’s how AI describes the company: Amphenol (APH) is one of the world’s largest designers, manufacturers, and marketers of electrical, electronic, and fiber optic connectors, as well as interconnect systems, coaxial and specialty cables, and high-performance sensors. The company’s core function is to enable high-speed signal transmission and power distribution across a wide range of demanding environments, serving industries such as automotive, aerospace, defense, industrial, IT/data communications, mobile devices, and broadband. Amphenol operates through three primary business segments: Harsh Environment Solutions, Communications Solutions, and Interconnect and Sensor Systems. The Harsh Environment Solutions segment provides ruggedized connectors and interconnects used in military, commercial aerospace, automotive, and heavy industrial markets. Communications Solutions serves the mobile devices and IT/data communications markets, supplying connectors for smartphones, tablets, servers, and networking equipment. Interconnect and Sensor Systems covers a broad industrial and transportation footprint, including sensors and interconnects used in factory automation, rail, green energy, medical, and hybrid-electric vehicle applications.

Amphenol posted a blockbuster Q2 with record sales of $5.65B, up 57% YoY and 41% organically, as every end market delivered double-digit organic growth. The standout driver was AI-fueled demand in the IT datacom segment, which surged 133% organically and now makes up 36% of total sales. CEO Adam Norwitt said the company actually shipped “substantially more than expected,” including some Q3 volume, because “our team outperformed even our customers’ very high expectations.” Roughly two-thirds of both YoY and sequential IT datacom growth came from AI-related products, which Amphenol delivers across the stack, from chipmakers to hyperscalers, thanks to its critical role in high-speed, power, and fiber-optic interconnects. Even with some pull-forward, Q3 sales are only expected to dip mid-single digits, and Norwitt emphasized they’re still winning new AI programs and expanding capacity globally, supported by elevated CapEx. Outside of AI, defense sales rose 25% YoY, with global geopolitical tensions driving long-term opportunity, and European industrial sales turned positive, with broad strength in factory automation, medical, and alternative energy.

Looking at the snapshot below from our Earnings Explorer, Amphenol (APH) has been on a triple play hot streak, with very strong EPS and revenue beat rates, 91% and 94%, respectively, since 2001 when our database begins. The company’s EPS beat streak goes back to 2020 and 2016 for revenue.

You can read more about APH and the 20 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Jul 29, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Whirlpool’s (WHR) Q2 2025 earnings call.

Whirlpool (WHR) is one of the world’s largest home appliance manufacturers, producing major brands like Whirlpool, Maytag, KitchenAid, JennAir, and Amana. The company makes washers, dryers, refrigerators, ovens, dishwashers, and small kitchen appliances, primarily for the residential market. It serves both individual consumers and homebuilders, with a particularly dominant presence in North America, where 80% of its products sold are manufactured domestically. Whirlpool offers investors insight into global consumer health, the US housing cycle, and international trade dynamics, especially around tariffs and supply chains. Whirlpool faced ongoing headwinds from weak consumer sentiment and a flood of tariff-free Asian imports, which intensified promotional pressure and delayed expected tariff benefits. Net sales fell 3% YoY (ex-currency), and MDA (Major Domestic Appliances) North America margins held at about 6% despite volume and mix challenges. The company rolled out its largest product refresh in a decade, including customizable KitchenAid appliances and new JennAir cooktops. Management remains confident that Whirlpool’s US-based manufacturing footprint positions it to gain share as tariffs take hold. The company missed EPS and revenue estimates, and the stock fell as much as 12% on 7/29…

Continue reading our Conference Call Recap for WHR by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jul 29, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Boeing’s (BA) Q2 2025 earnings call.

Boeing (BA) is one of the world’s largest aerospace and defense companies, manufacturing commercial airplanes, military aircraft, satellites, and space systems. Best known for its 737, 787, and 777 jetliners, Boeing also supports a wide range of defense and government programs globally, including fighter jets, surveillance platforms, and secure satellite communications. With over $600 billion in backlog, Boeing is a bellwether for global trade, supply chain resilience, and international defense. The company reported $22.7B in revenue (+35% YoY) and delivered 150 commercial aircraft (the most since 2018) with strong progress stabilizing 737 and 787 production. The 737 MAX ramp hit 38/month, though rework hours remain a hurdle for FAA approval to move to 42. Certification delays for the 737-7 and -10 pushed to 2026 due to anti-ice system redesigns. Defense saw margin improvement and a $2.8B Space Force win, while BGS posted 19.9% margins with new Navy and Korean contracts. Boeing also praised new zero-tariff trade deals with Japan and the EU as vital tailwinds for global demand. Despite better-than-expected results, BA shares fell more than 4% on 7/29…

Continue reading our Conference Call Recap for BA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan