Aug 22, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 28 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

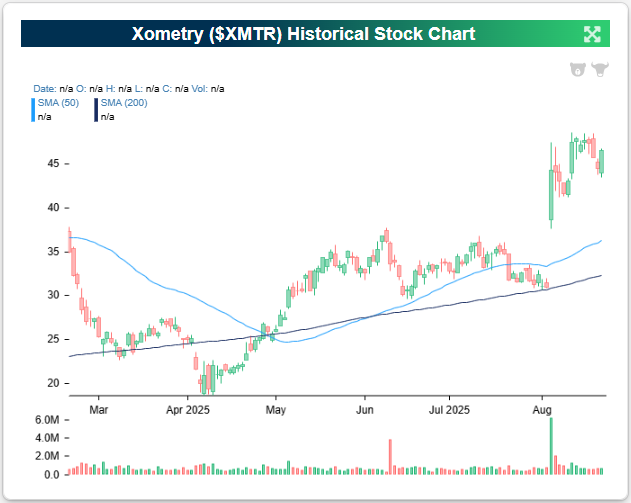

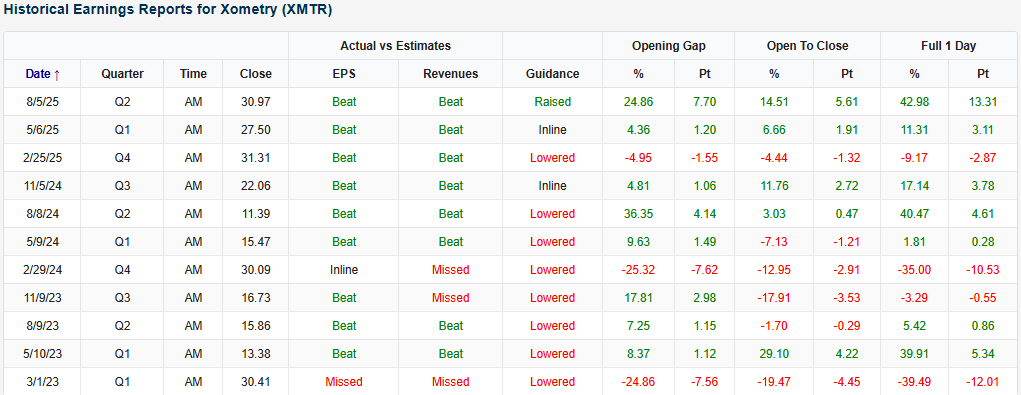

Xometry (XMTR) is an example of a company that recently reported an earnings triple play before the open on 8/5. On a streak of six EPS and revenue beats, this quarter’s triple play saw the stock 43% higher on the day. That rally brought the stock out of the red on the year, and it has since climbed another 10%. What a month it’s been for XMTR shareholders!

Here’s how AI describes the company: Xometry (XMTR) is a technology company that operates a global AI-powered marketplace for on-demand manufacturing, connecting businesses that need custom parts with a network of more than 4,300 suppliers. Its platform covers a wide range of processes, including CNC machining, 3D printing, injection molding, sheet metal fabrication, and urethane casting, making it a one-stop solution for industries such as aerospace, defense, automotive, medical devices, and robotics. The company differentiates itself by offering instant quoting, dynamic pricing algorithms, and supplier-matching tools that leverage machine learning to improve accuracy and speed in sourcing. For enterprises, Xometry provides software integrations like Teamspace, which enables collaborative procurement across organizations, and Workcenter, a cloud-based platform that helps suppliers manage workflow, capacity, and payments. Through its asset-light model, Xometry addresses inefficiencies in the traditionally fragmented and offline manufacturing market, helping buyers diversify supply chains and reduce costs while allowing small and mid-sized manufacturers to monetize excess capacity and reach new customers globally.

XMTR turned in a strong Q2, with revenue up 23% from last year to $163 million, led by 26% growth in its core marketplace and a 31% jump overseas. The customer base keeps expanding, with nearly 75,000 active buyers, up 22%, and more large accounts spending above $50,000 annually. Profitability improved as well, with gross margin climbing to a record 40.1%, helped by smarter AI-driven pricing and new tools that speed up quoting and order processing. Recent product rollouts included instant quotes for new materials, a system that reads technical drawings automatically, and the launch of Teamspace in Europe, which makes it easier for teams to manage projects together. Suppliers also got a lift from a new mobile app that lets them track jobs and share updates more easily. Growth came across industries like aerospace, defense, automotive, and robotics, with a major European aerospace firm choosing Xometry as a preferred supplier, an account that could generate over $10 million annually. Management pointed out that marketplace margins have steadily climbed over the past four years, showing how scale and data continue to strengthen the model.

Looking at the snapshot below from our Earnings Explorer, Xometry (XMTR) reported its first triple play after a string on lower guidance. A 40% pop for the stock post-earnings isn’t totally new for XMTR, but it’s an impressive swing nonetheless. Beat rates have also been strong the last several quarters, a positive sign that the stock is on the right track.

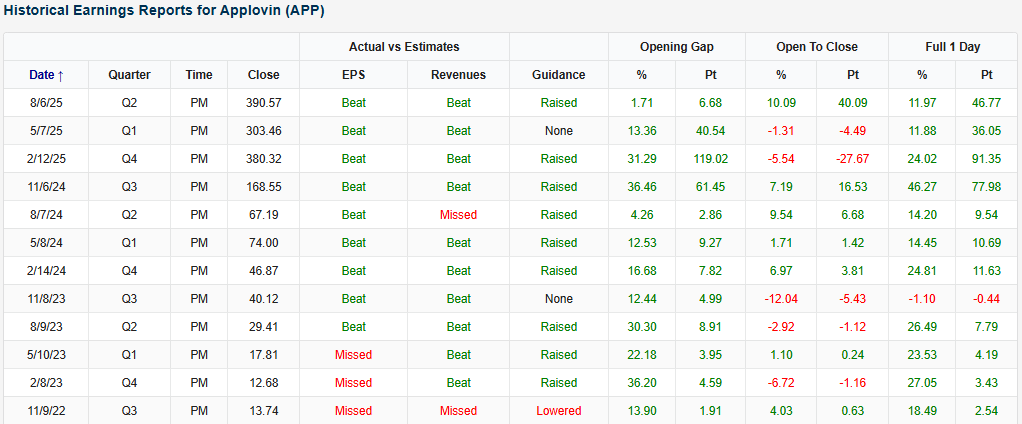

As a bonus to this installment of the Triple Play Report, we’d like to point out a hard-hitting stat from one of the Triple Play stocks found within today’s report. Advertisement technology company Applovin (APP) has gained more than 10% on each of its last seven earnings reaction days and 11 of its last 12. We can’t think of another stock that has done this. These massive moves higher on basically every earnings report in the last couple years is one reason why it has been a 10-bagger since the start of 2024!

You can read more about XMTR, APP, and the 26 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Aug 21, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Walmart’s (WMT) Q2 2026 earnings call.

Walmart (WMT) is the world’s largest retailer, operating supercenters, neighborhood markets, Sam’s Club warehouses, and a rapidly growing e-commerce platform. It serves over 250 million customers weekly across the US and 18 countries, offering everything from groceries and apparel to electronics and pharmaceuticals. Walmart posted 5.6% constant-currency sales growth, driven by 26% US e-commerce growth, a 6% Sam’s Club comp, and 10.5% international growth (China +30%, Walmex +6%). Delivery speed is a standout: one-third of orders arrived in under 3 hours, 20% in under 30 minutes. Tariffs remain a headwind, yet Walmart expanded rollbacks to 7,400 items, up nearly 2,000 from Q1, with grocery rollbacks up 30%. Consumer resilience was mixed: higher-income households fueled share gains, while middle and lower-income cohorts traded down. Advertising revenue surged 46% globally, membership income rose 15%, and the marketplace grew 17%. AI dominated discussion, with “Sparky” and other super-agents set to transform shopping, associates’ work, and supplier tools. On mixed results, WMT shares tumbled more than 5% on 8/21…

Continue reading our Conference Call Recap for WMT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 19, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Home Depot’s (HD) Q2 2025 earnings call.

Home Depot (HD) is the world’s largest home improvement retailer, operating more than 2,300 stores across the US, Canada, and Mexico. It serves both do-it-yourself (DIY) customers and professional contractors (“Pros”) with an assortment of building materials, home improvement products, appliances, and tools. Beyond retail, the company has built a powerful logistics and digital platform, offering same-day and next-day delivery, and is expanding deeper into wholesale distribution with acquisitions like SRS (roofing, landscaping, pool) and pending GMS (drywall, ceilings, steel framing). HD reported Q2 sales of $45.3B, up 4.9% YoY, with US comps +1.4%. Smaller projects and seasonal categories drove momentum, while large renovations remain weak amid high rates and economic uncertainty. Management stressed that consumers remain healthy, with $11T in tappable home equity, but are deferring (not canceling) big projects. Technology and AI-powered delivery improvements produced record speed, boosting digital sales by 12% and lifting spend among repeat users. Pro initiatives are accelerating, with SRS exceeding expectations and GMS adding 400 distribution nodes. Trade credit accounts are already driving double-digit lifts in Pro spend. Merchandising strength was broad-based, with 12 of 16 departments comping positive, a sales record in battery-powered tools, and strong appliance gains. Despite misses on the top and bottom lines, HD shares rose as much as 3.2% on 8/19…

Continue reading our Conference Call Recap for HD by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 19, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Viking’s (VIK) Q2 2025 earnings call.

Viking (VIK) is a leading operator of river, ocean, and expedition cruises, built around culturally immersive, destination-focused travel. Its fleet spans 85 river vessels and 12 ocean ships, all designed with a uniform, understated luxury (no casinos, no children, and no nickel-and-diming) that appeals to affluent, “culturally curious” travelers, particularly older demographics seeking comfort and enrichment. Viking controls or has priority access to over 100 docking sites worldwide, giving it a competitive moat in river cruising. The company provides insight into global travel demand trends, discretionary spending patterns among wealthier consumers, and how tourism is shifting toward experiential, high-end travel. Viking reported an 18.5% revenue increase in Q2 2025, fueled by 8.8% capacity growth and an 8% rise in net yields. Bookings remain robust: 96% of 2025 capacity is already sold, and 2026 is 55% booked at higher rates. Egypt and India itineraries sold out quickly, showing strong demand for new cultural destinations. The company highlighted river versus ocean dynamics, river pricing accelerated while ocean moderated slightly, but both segments maintain high occupancy above 95%. Management stressed that marketing, not discounting, is their lever when demand softens. VIK posted better-than-expected revenue on in-line EPS, though the stock fell 5.5% at the open on 8/19…

Continue reading our Conference Call Recap for VIK by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 19, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Palo Alto Networks’ (PANW) Q4 2025 earnings call.

Palo Alto Networks (PANW) is the world’s largest pure-play cybersecurity firm, serving enterprises, governments, and critical infrastructure across the globe. Best known for pioneering the next-generation firewall, the company now offers an integrated portfolio spanning network security, cloud security, and AI-driven security operations. Its platform-based model helps organizations consolidate fragmented security tools into unified systems, improving both outcomes and cost efficiency. Fiscal Q4 2025 marked a milestone as PANW became the first dedicated cybersecurity company to surpass a $10B revenue run rate. Management leaned heavily into AI security, highlighting Prisma AIRS and AI Access as demand surges (GenAI traffic up 890% YoY). Platformization dominated deal flow, including a $100M+ consulting firm win, driving net retention to 120%. Network Security momentum came from SASE (ARR +35% YoY) and Prisma Access Browser (3M licenses sold in Q4). Cortex/XSIAM continued to scale, cutting response times to under 10 minutes for many clients. The proposed CyberArk acquisition would make identity a new platform pillar. Despite global tariff uncertainty, US-based manufacturing insulated margins. The company’s triple play is its first since 2022, and the stock popped 6.4% at the open on 8/19 as a result…

Continue reading our Conference Call Recap for PANW by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 13, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 24 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Below is a blurb from our newest Triple Play Report to give you an idea of the insights that are included in this piece.

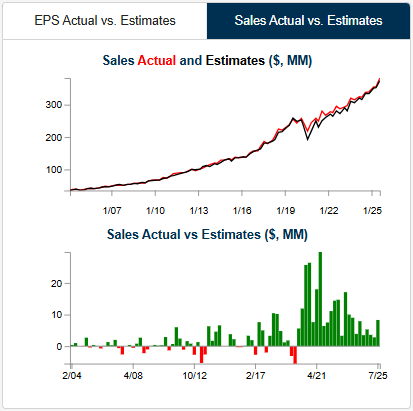

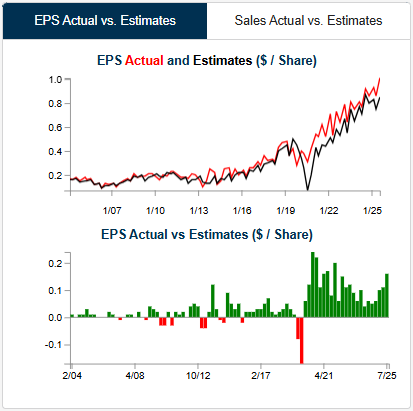

Merit Medical (MMSI) is a medical device maker involved in cardiology, radiology, endoscopy, and dialysis access maintenance. Its catheters, stents, embolization products, and hemostatic solutions are designed to improve procedural efficiency and patient outcomes. MMSI sells primarily to hospitals, outpatient centers, and physician offices. Recent growth has been fueled by acquisitions such as Cook Medical’s lead management portfolio, EndoGastric Solutions’ assets, and BioLife’s patented StatSeal and WoundSeal products, which expand MMSI’s offerings in high-value niches like vascular closure, indwelling catheter bleeding control, and cardiac intervention.

Below is a look at EPS and sales versus consensus estimates for MMSI from our Earnings Explorer tool. Notably, MMSI has beaten both top and bottom line estimates on each of its last 23 quarterly reports dating back to the start of 2020, and as you can see in the charts, both have been trending sharply higher. In addition to the strong EPS and sales results, MMSI completed the triple play this quarter by raising guidance. Shares reacted positively with a gain of 2.3% on its earnings reaction day on 7/31, but the stock didn’t quite see the “pop” that most triple plays do on such strong results.

The most interesting thing we heard on MMSI’s triple-play earnings call this quarter was related to tariffs. As a maker of all kinds of medical devices, MMSI estimated earlier in the year that tariffs would cost the company roughly $26 million. On this call, however, the company noted that the easing of tariffs had cut their cost-impact estimates down to just $7 million at the high end.

Several other triple-play companies have also provided positive news on the tariff front recently.

You can read more about MMSI and the 23 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.