Sep 4, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 20 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

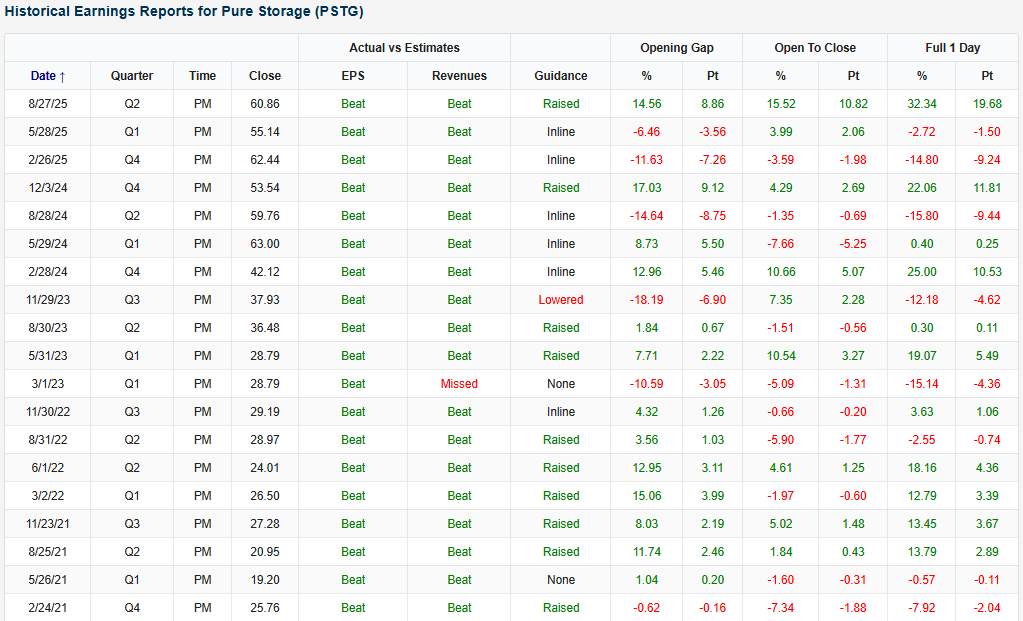

Pure Storage (PSTG) is an example of a company that recently reported an earnings triple play after the close on 8/27. On a streak of ten EPS and revenue beats, the stock rallied 32% on 8/28 in reaction to this quarter’s triple play. That rally brought the stock to a new all-time high!

Here’s how AI describes the company: Pure Storage (PSTG) is a data storage company that develops all-flash hardware systems and cloud-based software to help enterprises manage rapidly growing volumes of data. Its core platform runs on the Purity operating system, which standardizes and simplifies storage across block, file, and object formats while enabling features like automated upgrades and data reduction. The company sells both physical arrays such as FlashArray for high-performance workloads and FlashBlade for analytics and AI, as well as subscription models like Evergreen//One, which delivers storage on demand with predictable costs and built-in refreshes. Pure has also expanded into cloud-native infrastructure through Cloud Block Store and Portworx, which allow customers to run applications seamlessly across public clouds and containerized environments like Kubernetes. More recently, the company introduced its Enterprise Data Cloud architecture, a framework designed to unify data management across global data estates, reduce IT complexity, and improve efficiency in areas such as power consumption and cooling. With customers spanning Fortune 500 firms, hyperscalers, and cloud-first enterprises, Pure Storage positions itself as a leader in modernizing data centers for AI, analytics, and next-generation application development.

Pure Storage posted strong Q2 FY26 results, with revenue up 13% to $861 million. Nearly half of sales now come from subscriptions, which grew 15% to $415 million, showing that customers are steadily moving away from one-time hardware purchases toward ongoing service contracts. Annual recurring revenue rose 18% to $1.8 billion, and the company’s backlog of contracted sales reached $2.8 billion, signaling confidence in long-term demand. Growth was broad, but international markets stood out with a 26% gain compared to 7% in the US. Customers continued to choose PSTG’s higher-end systems like FlashArray//XL, which lifted product gross margin to 68% and total gross margin to 72.1%. The company also recognized its first revenue from Meta’s deployment of DirectFlash technology, a high-margin deal expected to scale to multiple exabytes. Over 300 new customers were added, bringing Fortune 500 penetration to 62%. Management raised its full-year revenue outlook to 14% growth, citing a healthier pipeline of large deals, strong demand for FlashBlade in AI and analytics, and growing adoption of its storage-as-a-service offerings.

Looking at the snapshot below from our Earnings Explorer, Pure Storage (PSTG) has been a strong triple play name over the past several years. Since the beginning on 2021, the company has reported ten triple plays with just one revenue miss in 2023. This quarter’s positive stock reaction is also its best since its 2015 IPO.

You can read more about PSTG and the 19 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Aug 28, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Best Buy’s (BBY) Q2 2026 earnings call.

Best Buy (BBY) is the largest specialty retailer of consumer electronics in North America, offering everything from laptops, gaming consoles, and mobile phones to home theater systems and appliances. The company operates as a true omnichannel player, blending its digital presence with a nationwide store network where 45% of online orders are picked up in-store. Best Buy is notable for its deep vendor partnerships with tech leaders like Apple, Microsoft, Samsung, and Nintendo, as well as new collaborations like IKEA. Its scale, Geek Squad services, and immersive in-store showcases make it a unique lens into consumer tech adoption and spending habits across households. Sales rose 1.6% to $9.4B, with EPS of $1.28 and comps up 1.6%, driven by strong gaming (Switch 2 launch) and record laptop sales, the best Q2 volume in 15 years. Online sales grew to 33% of domestic revenue, while deal-focused consumers continued to anchor around big promotional events. Best Buy launched its third-party marketplace, tripling mobile accessories and expanding into new categories, and rolled out AI-powered search ahead of the holiday season. Tariffs remain a manageable headwind as sourcing shifts away from China. Home theater and appliances lagged, but are being addressed with sharper pricing and faster fulfillment. BBY shares fell as much as 8.9% from the open on 8/28, despite better-than-expected results…

Continue reading our Conference Call Recap for BBY by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 28, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers CrowdStrike’s (CRWD) Q2 2026 earnings call.

CrowdStrike (CRWD) is a cybersecurity company best known for its Falcon platform, which provides endpoint protection, cloud security, identity defense, and next-gen SIEM solutions. Its technology combines real-time threat intelligence, AI-driven analytics, and managed detection to stop breaches at scale. CrowdStrike serves enterprises across industries, from Fortune 500s to SMBs, with a growing partner ecosystem that includes Amazon, NVIDIA, and managed service providers. CrowdStrike’s Q2 was defined by acceleration: record net-new ARR of $221M pushed total ARR to $4.66B (+20% YoY), ahead of expectations. Demand was fueled by AI security concerns, with management highlighting adversaries using GenAI and positioning CrowdStrike as the leader in securing AI models, workloads, and identities. Charlotte AI, its autonomous SOC analyst, grew more than 85% sequentially, while Next-Gen SIEM (Security Information and Event Management) ARR surged 95% YoY, bolstered by the announced acquisition of Onum for real-time data pipeline detection. Identity protection, now extending to non-human and AI agents, topped $435M ARR, and cloud security surpassed $700M ARR (+35%). Falcon Flex licensing continued to gain traction, with early re-Flex deals driving about 50% ARR uplift. Partnerships with Amazon, NVIDIA, and MSSPs further supported platform adoption. CRWD shares fell 7.25% after hours on 8/27, but rebounded 12.5% from the low on 8/28…

Continue reading our Conference Call Recap for CRWD by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 28, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers NVIDIA’s (NVDA) Q2 2026 earnings call.

NVIDIA (NVDA) is the global leader in accelerated computing, best known for its GPUs that power artificial intelligence, gaming, data centers, and increasingly robotics and autonomous systems. The company develops full-stack platforms that span hardware, software, and networking, giving it unmatched influence over the direction of AI infrastructure. Its chips support everything from generative AI model training to enterprise cloud workloads, while its gaming and professional visualization products serve millions of consumers and businesses worldwide. The company posted record revenue of $46.7B, driven by 56% YoY growth in data center sales. The star was the Blackwell GB300 platform, now ramping at 1,000 racks per week with 10x inference efficiency and broad adoption from OpenAI, Meta, and others. CEO Jensen Huang emphasized the explosive shift to “reasoning” and “agentic” AI, which can require 100x more compute than one-shot models and is fueling demand for robotics and physical AI. Networking revenue nearly doubled YoY to $7.3B, led by InfiniBand and Spectrum-X. Rubin, NVIDIA’s next-gen platform, remains on track for 2026. Geopolitics remain a headwind, with H20 shipments to China dependent on US licensing. Shares were down as much as 3.1% in after-hours trading on 8/27 after posting better-than-expected EPS and revenue results…

Continue reading our Conference Call Recap for NVDA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 27, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Williams-Sonoma’s (WSM) Q2 2025 earnings call.

Williams-Sonoma (WSM) is a specialty retailer of premium home goods, serving consumers across furniture, kitchenware, textiles, and décor through brands like Pottery Barn, West Elm, and its namesake, Williams-Sonoma. The company differentiates itself with in-house design, exclusive collaborations, and a strong omnichannel model that blends e-commerce with over 450 stores. Its reach spans both direct-to-consumer and B2B, with the latter supplying commercial-grade products to industries from hospitality to design. With a “digital-first, but not digital-only” approach and a growing portfolio of emerging brands like Rejuvenation and GreenRow, WSM provides a window into higher-income consumer demand and home furnishing trends. WSM delivered a 3.7% comp, with all brands positive, and EPS rising nearly 20% to $2.00. Furniture returned to growth, led by newness and collaborations, while Rejuvenation logged its seventh straight double-digit comp, and B2B sales rose 10%. Management hit on AI, already live in customer service and supply chain forecasting, yielding measurable productivity gains. Tariffs remain a central risk (rates doubled since Q1 to 28%), but WSM is offsetting costs through vendor concessions, US sourcing, and selective pricing. Despite housing market weakness and high rates, strong brand momentum led the company to raise revenue guidance to 2–5% comp growth. WSM shares rose 3.2% at the open on 8/27 following better-than-expected results, though gave up the gains quickly…

Continue reading our Conference Call Recap for WSM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Aug 27, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers MongoDB’s (MDB) Q2 2026 earnings call.

MongoDB (MDB) is a modern database provider built around its flexible document model, allowing developers to manage structured, semi-structured, and unstructured data at scale. Its flagship product, MongoDB Atlas, is a fully managed cloud database that has become the backbone for applications in finance, healthcare, manufacturing, and technology. Over 70% of the Fortune 500 rely on MongoDB for mission-critical workloads, from billing systems at Deutsche Telekom to connected car platforms at major automakers. By integrating capabilities like search, vector search, and streaming directly into its database, MongoDB reduces the need for multiple disparate tools, positioning itself as a core part of the AI infrastructure stack. In Q2 of fiscal 2026, MongoDB posted revenue of $591M (+24% YoY), with Atlas growing 29% and now making up 74% of sales. Growth was fueled by larger enterprise workloads scaling faster and durable customer additions, with total customers nearing 60,000. AI was a recurring theme: startups and enterprises are increasingly turning to Atlas for vector search and agent-based applications, though management noted AI adoption remains early. Competitive positioning against Postgres (an open-source relational database system that’s widely used across industries) was discussed, with MongoDB’s JSON-first architecture and integrated search cited as advantages. Management also highlighted progress in legacy app modernization and a strong Q3 guide despite expected non-Atlas headwinds. Following the triple play, MDB shares rallied more than 30% on 8/27. That’s the company’s best post-earnings reaction since its 2017 IPO…

Continue reading our Conference Call Recap for MDB by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan