Oct 31, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 20 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

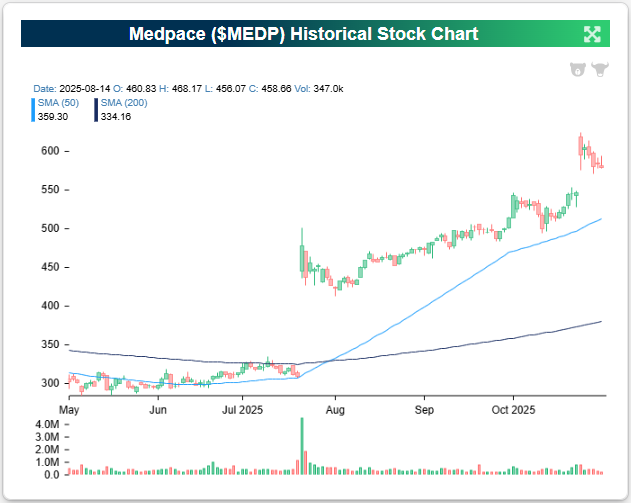

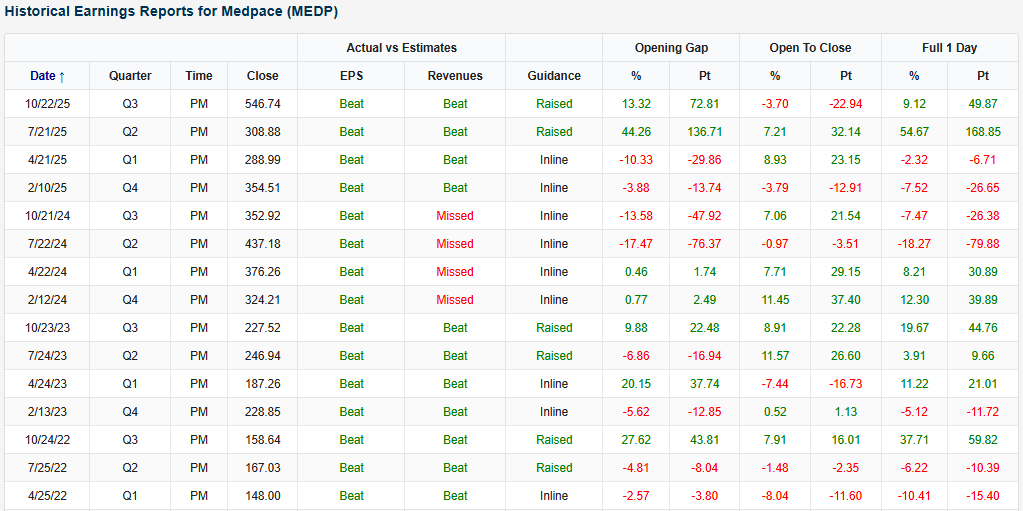

Medpace (MEDP) is an example of a company that recently reported an earnings triple play after the close on 10/22. MEDP reported its second straight triple play, and the stock was up 9.1% on 10/23. After the previous quarter’s triple play report, the stock skyrocketed 54.7%! It hit another all-time high after its latest triple play and is up 74.7% YTD.

Here’s how AI describes the company: Medpace (MEDP) is a global clinical research company that helps biotech and pharmaceutical firms bring new drugs to market by managing every stage of the clinical trial process. The company handles trial design, patient recruitment, site coordination, data analysis, and regulatory submissions under one roof, which gives it tight control over quality and timing. Its work spans a range of therapeutic areas but has become especially concentrated in metabolic disease, oncology, and cardiovascular trials, with a growing portion of business tied to obesity and GLP-1 drug development. A large part of its future revenue comes from its “backlog” of awarded projects that have yet to start, giving strong visibility into client demand.

Medpace’s quarter showed how it is benefiting from the surge in obesity and metabolic disease drug development, which has become one of the hottest areas in biotech. Revenue climbed 23.7% to $659.9 million as the company managed a growing volume of late-stage GLP-1 studies, which are larger, faster-paced, and more expensive to run because of high site and investigator costs. After several quarters of disruption from study cancellations, management said the environment has improved sharply, with fewer cancellations and more consistent client funding. That allowed the value of awarded but not-yet-launched projects to grow 30% from last year, positioning the company for continued growth as those trials move into active enrollment. Hiring was strongest in the US, where most GLP-1 trials are based, and India remains a key location for back-office and data work as Medpace scales up to meet record demand.

Looking at the snapshot below from our Earnings Explorer, Medpace (MEDP) has started to find its footing again after hitting somewhat of a rough stretch in 2024, headlined by revenue misses and heavy declines for the stock after reporting. In the last year, though, MEDP has been consistent with EPS and revenue beats, and with two recent triple plays, investors are coming back around to the stock. Historically speaking, MEDP has been a reliable earnings bet against estimates, with EPS and revenue beat rates going back to 2016 of 89% and 78%, respectively, which are both meaningfully above average.

You can read more about MEDP and the 21 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Oct 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Procter & Gamble’s (PG) Q1 2026 earnings call.

Procter & Gamble (P&G) is one of the world’s largest consumer goods companies, producing household staples across ten core categories like Fabric Care, Baby Care, Grooming, Oral Care, and Skin & Personal Care. Its iconic brands (Tide, Pampers, Gillette, Olay, and Crest) are used by billions globally and dominate supermarket shelves in over 180 countries. P&G gives investors a read on consumer confidence, pricing power, and retail spending trends across income levels and regions. P&G’s Q1 FY26 call reflected steady results amid a soft global consumption backdrop. Organic sales rose 2% with flat volumes and modest pricing gains, marking the 40th straight quarter of growth. Management highlighted competitive pressure in Fabric and Baby Care, especially in the US and Europe, but pointed to innovations like Tide’s biggest upgrade in 20 years and premium Olay launches in China as key demand drivers. China sales rose 5% while Latin America surged 7%. The company also discussed its restructuring, including cutting up to 7,000 non-manufacturing roles and a $1.5B cost-savings target through “Supply Chain 3.0.” Tariffs remain a $500M headwind, but guidance for 0–4% organic growth was reaffirmed. On better-than-expected results, PG shares were up 3% at the open on 10/24…

Continue reading our Conference Call Recap for PG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Oct 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Intuitive Surgical’s (ISRG) Q3 2025 earnings call.

Intuitive Surgical (ISRG) develops and manufactures robotic-assisted surgical systems, most notably the da Vinci and Ion platforms. These systems combine robotics, advanced imaging, and AI to help surgeons perform minimally invasive procedures with greater precision and consistency. The company serves hospitals and healthcare networks globally, with applications spanning general surgery, urology, gynecology, thoracic, and lung biopsy procedures. ISRG’s innovation pipeline, such as its Single-Port (SP) system, force-feedback instrumentation, and AI-powered navigation, makes it a leading barometer for how technology and automation are transforming operating rooms worldwide. ISRG reported another strong quarter as worldwide procedures rose 20% and revenue climbed 23% to $2.5 billion. Adoption of the da Vinci 5 system accelerated, with 240 of 427 placements coming from the newest model. The Ion platform grew 52% in procedures, aided by new FDA-cleared AI imaging features that improved precision in lung diagnostics. SP procedures surged 91%, reflecting early success in new indications. While bariatric volumes softened amid GLP-1 drug use, benign general surgery remained robust. Internationally, growth was broad but tempered by budget pressure in Japan and China. Management highlighted AI integration, digital case insights, and refurbished systems as long-term growth drivers. On better-than-expected results, ISRG rallied 19% after-hours on 10/21…

Continue reading our Conference Call Recap for ISRG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Oct 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Capital One’s (COF) Q3 2025 earnings call.

Capital One (COF) is one of the largest diversified banks in the United States, offering credit cards, auto loans, retail and digital banking, and commercial financial services. The company has built one of the industry’s most advanced cloud-based platforms, serving over 100 million customers. It serves everyone from mass-market consumers to premium spenders and commercial clients, with its recent acquisition of Discover Financial Services expanding its reach into payment networks and debit processing. Capital One’s third quarter centered on the full-quarter impact of its Discover acquisition, which lifted revenue 23% sequentially. Management reaffirmed $2.5 billion in expected synergies. Consumer credit performance improved despite inflation, tariffs, and high rates, with charge-offs at 4.63% and strong recoveries. Auto losses were 25% lower year over year, while commercial lending remained cautious amid private credit expansion. CEO Richard Fairbank emphasized Capital One’s long-running tech transformation and AI integration, as well as continued investment in premium cards like Venture X to win higher-spending customers. COF shares opened almost 4% higher on 10/22 in reaction to stronger-than-expected results…

Continue reading our Conference Call Recap for COF by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Oct 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Illinois Tool Works’ (ITW) Q3 2025 earnings call.

Illinois Tool Works (ITW) is an industrial manufacturer operating across seven segments (Automotive OEM, Test & Measurement & Electronics, Welding, Food Equipment, Polymers & Fluids, Construction Products, and Specialty Products). Its products range from auto fasteners and welding systems to commercial food equipment and industrial fluids. Organic growth of 1% outpaced end markets that declined in the low single digits, while record operating margins of 27.4% reflected strong pricing and supply-chain management that more than offset tariff costs. The Asia-Pacific region led growth with a 7% gain, including a 10% increase in China, where ITW continues to win EV market share and increase content per vehicle. Automotive OEM margins climbed 2.4% to 21.8%, and Welding equipment sales rose 6% on new product innovation. Management described demand patterns as “choppy,” noting tariff-related CapEx pauses and seasonal construction softness. Shares fell more than 4% on 10/24 after a revenue miss…

Continue reading our Conference Call Recap for ITW by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Oct 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Norfolk Southern’s (NSC) Q3 2025 earnings call.

Norfolk Southern (NSC) is one of the largest freight railroads in North America, operating a 19,000-mile network across 22 eastern US states. The company transports a broad mix of industrial products, including automotive, chemicals, metals, construction materials, coal, and intermodal containers, linking manufacturers, utilities, and ports. NSC is a critical barometer of the US industrial and trade economy, serving major sectors like autos, energy, and agriculture. Norfolk Southern’s quarter reflected a freight economy under pressure from tariffs, oversupplied truck capacity, and weaker coal exports. Revenue grew 2% year-over-year, but volumes were flat, and management cited about $75 million in expected revenue that didn’t materialize. The pending Union Pacific merger weighed on intermodal demand as competitors reacted, especially in the Southeast, though leadership expects the effect to fade over upcoming bid cycles. Despite headwinds, NSC raised its cumulative cost-savings goal to $600 million by 2026 and highlighted advanced inspection portals that have already prevented over 40 potential derailments. NSC reported better-than-expected EPS on weaker revenue as shares fell around 1% on 10/24…

Continue reading our Conference Call Recap for NSC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan