Nov 27, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dick’s Sporting Goods’ (DKS) Q3 2025 earnings call.

Dick’s Sporting Goods (DKS) is the dominant US omnichannel sporting goods retailer, serving athletes and outdoor enthusiasts through an extensive portfolio that now includes Foot Locker. By combining experiential retail concepts like “House of Sport” with the “GameChanger” youth sports technology platform, DKS provides insight into consumer discretionary spending on health, wellness, and sneaker culture. DKS discussed a distinct bifurcation between its core business and its new Foot Locker acquisition. The legacy DKS brand was strong, delivering 5.7% comparable sales growth and raising full-year guidance despite tariff headwinds. Conversely, the integration of Foot Locker requires a “cleaning out the garage” phase. Management announced aggressive Q4 inventory cleanouts, projecting a steep 1,000–1,500 basis point margin contraction for that segment while targeting an inflection point by the 2026 Back-to-School season to make the deal accretive. DKS beat EPS and revenue estimates, and the stock finished the trading day flat on 11/25 after opening almost 3% lower and completely erasing the losses…

Continue reading our Conference Call Recap for DKSby becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Nov 26, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Symbotic’s (SYM) Q4 2025 earnings call.

Symbotic (SYM) builds automation systems that use robots, sensors, and software to move products through warehouses faster and with far fewer errors than traditional manual operations. Its bots navigate giant storage structures, retrieve items, and sequence them for shipping, helping major retailers like Walmart, wholesalers, grocers, and now healthcare distributors handle huge volumes of goods with more speed and less labor. Symbotic finished the year with $618M in quarterly revenue, up 10%, as more automated systems went live and software and service fees climbed. The biggest news was its first healthcare win with Medline, opening the door to a massive new market of 500+ US distribution centers. Its new “next-gen” storage setup is cutting installation time in half for large customers by allowing what used to be two deployments to be completed in one. GreenBox, its joint venture with SoftBank that builds and operates fully automated warehouses, allowing companies to rent space and fulfillment services powered by Symbotic’s robotics instead of constructing their own distribution centers, is preparing to open its first site in Atlanta as demand grows for faster, more local e-commerce fulfillment. SYM reported EPS of -$0.03, which missed estimates, but beat on the top line as shares surged 36% on 11/25…

Continue reading our Conference Call Recap for SYM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Nov 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Walmart’s (WMT) Q3 2026 earnings call.

Walmart (WMT) is the world’s largest retailer, serving millions of households across income levels through a massive physical footprint of supercenters, Sam’s Clubs, and expanding eCommerce. Known for its everyday low prices, Walmart provides groceries, general merchandise, health and wellness services, and an enormous third-party marketplace. Walmart delivered another strong quarter with 6% revenue growth, 27% eCommerce growth, and continued market share gains in grocery, apparel, and general merchandise. Higher-income households drove much of the momentum, while lower-income customers showed modest pressure. Delivery speeds hit records, with 35% of US digital orders arriving in under three hours, and automation now supports 50%+ of fulfillment center volume, lowering shipping costs. International strength was notable: China up 22%, and Flipkart’s Big Billion Days (BBD) generated over 700 orders per second at peak. Management was generally confident in its value proposition and growing alternative profit streams like advertising and membership, despite some discussion around tariffs. On better-than-expected results, WMT shares climbed 6.5% on 11/20…

Continue reading our Conference Call Recap for WMT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Nov 24, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers NVIDIA’s (NVDA) Q3 2026 earnings call.

NVIDIA (NVDA) designs the world’s most powerful accelerated computing hardware and software, best known for its GPUs, networking platforms, and full-stack AI systems used in data centers, autonomous vehicles, robotics, and high-performance computing. The company sits at the center of the global AI infrastructure boom, supplying hyperscalers, sovereign governments, pharmaceutical companies, automakers, and millions of developers worldwide. NVIDIA posted another blowout quarter with $57B in revenue, up 62% YoY, as demand for AI infrastructure remained well above supply, and hyperscaler CapEx expectations rose to roughly $600B for 2026. Data center revenue hit $51B (+66% YoY), driven by the GB300 Blackwell platform and explosive growth in networking (+162% YoY). The company announced 5 million GPUs’ worth of new AI factory projects, including xAI’s gigawatt-scale Colossus 2 and Lilly’s drug-discovery supercomputer. Management also highlighted soaring momentum from frontier model builders: OpenAI reaching 800M weekly users, Anthropic hitting a $7B run rate, and both expanding compute commitments. Despite geopolitical limits in China, NVIDIA expects Q4 revenue of $65B and sees multi-year leadership ahead with the Rubin architecture ramping in 2026. NVDA shares rose more than 5% after hours on 11/19 in reaction to its triple play earnings report, but fell in the tech-led market reversal to close down 3% on 11/20…

Continue reading our Conference Call Recap for NVDA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Nov 20, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 23 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

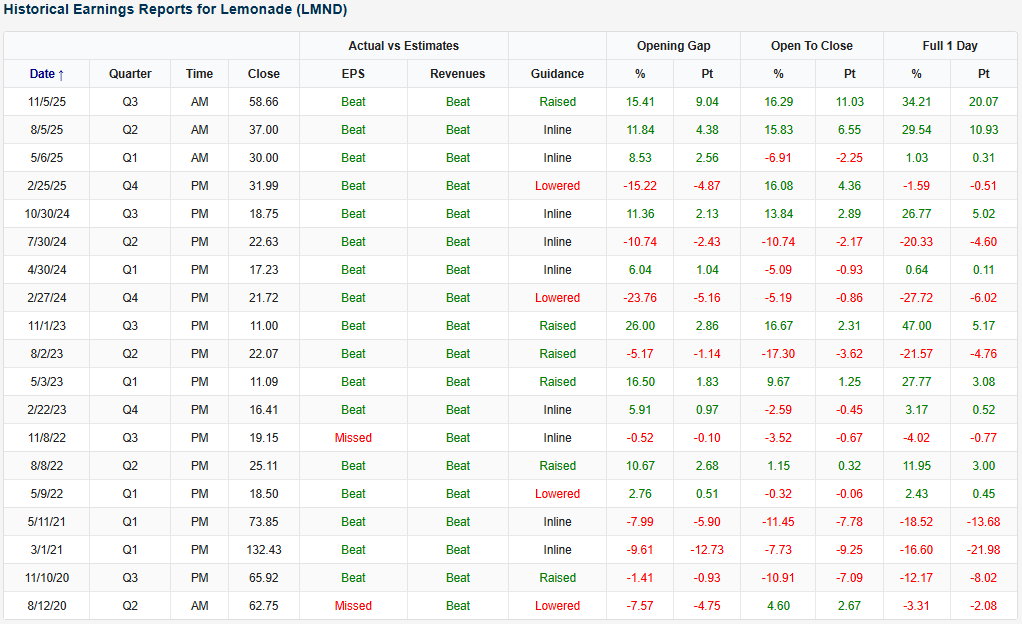

Lemonade (LMND) is an example of a company that recently reported an earnings triple play before the opening bell on 11/5. In reaction to the strong earnings results, LMND shares surged 34.2% that day. After that move, the stock hit its highest level since the summer of 2021. The stock has had a great year thus far, up 93.4% YTD.

Here’s how AI describes the company: Lemonade (LMND) is a fully digital, AI-driven insurance company that sells renters, homeowners, pet, and car policies directly through its app and website rather than through agents or legacy systems. The company’s entire model is built around automation: AI guides the majority of its marketing spend, prices policies in real time, detects risk patterns, and handles most customer support and claims without human intervention. This approach allows Lemonade to operate with a much smaller workforce than traditional insurers while providing instant quotes and often instant claim payments. Because its technology platform collects detailed customer and behavioral data, Lemonade continually updates pricing, underwriting, and fraud models, and it uses reinsurance partners to manage volatility as it grows. The long-term strategy is to use AI and automation to offer lower prices, expand into more insurance categories, and eventually compete at scale with the largest consumer insurers in the market.

Lemonade delivered one of its strongest quarters to date, with a total book of insurance that reached $1.16 billion, up 30% from last year, and revenue jumped 42% to $195 million. That faster revenue growth came partly from keeping a larger share of premiums in-house instead of passing them to reinsurance partners, which means Lemonade now earns more money on each customer it already serves. Gross profit doubled to $80 million thanks to fewer claims relative to premiums and continued efficiency gains from automation. The company added more than 176,000 customers, and car insurance remained a major growth engine, rising about 40% with over half of new car policies coming from existing Lemonade users who cost little to acquire and tend to be more profitable. Europe performed especially well, growing about 170% as Lemonade expanded renters and home insurance and adjusted prices more quickly than it could in the US. The company also highlighted meaningful cost improvements from AI, including a drop in claims-handling expense to 7%, even though overall claim volume has increased.

Diving more in-depth into car insurance, Lemonade discussed a new direct integration with Tesla that lets the insurer pull driving data straight from Tesla vehicles, with customer permission, rather than relying on a phone app or plug-in device. This gives Lemonade far more detailed information about how the car is actually being driven, including things like seatbelt use and precise trip patterns, which helps the company price car insurance more accurately and settle claims faster. Management said this level of “car-native” data becomes increasingly important as cars take over more driving functions on their own, because insurers need to distinguish between miles driven by humans and miles handled by the vehicle’s autopilot or full self-driving systems. While Lemonade did not share updates on its goal of offering very low-cost coverage for autonomous miles, the company said this integration is a crucial building block for that future, allowing it to learn directly from Tesla’s systems and design pricing that reflects how quickly autonomy is developing.

Looking at the snapshot below from our Earnings Explorer, Lemonade (LMND) has found success on earnings since it’s 2020 IPO. The company has beaten EPS and revenue estimates 89% and 100% of the time, respectively, with a running twelve straight quarters of top and bottom-line beats. Despite that consistency, the most recent report was LMND’s first triple play since a back-to-back-to-back string of them back in 2023. The moves for the stock in reaction to earnings have been somewhat of a mixed bag when looking back. After struggling in the first year after becoming a publicly traded company, the stock has seen some very positive, and very negative moves following earnings releases. The company’s last two reports, though, have been overwhelmingly positive in terms of how the stock has rallied.

You can read more about LMND and the 22 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Nov 3, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Chipotle’s (CMG) Q3 2025 earnings call.

Chipotle (CMG) operates more than 3,500 fast-casual restaurants specializing in customizable burritos, bowls, tacos, and salads. Serving a broad customer base that skews younger and urban, Chipotle offers insight into US consumer behavior and spending trends, especially among millennials and middle-income households. Chipotle’s Q3 call centered on macro pressure from lower- and middle-income consumers, who’ve reduced dining frequency as inflation, unemployment, and student loans weigh on budgets. Management noted that households under $100K account for roughly 40% of sales and are dining out less, but stressed that Chipotle isn’t losing share to competitors, only to food-at-home options. The company plans to limit 2026 price increases and absorb some cost inflation to preserve value, even as tariffs and beef costs rise mid-single digits. Digital engagement and loyalty activations like “Summer of Extras” lifted frequency, while new equipment upgrades improved throughput. Unit expansion and catering pilots remain key growth drivers heading into 2026. CMG missed on the top-line with in-line EPS as shares plummeted 18.3% on 10/30…

Continue reading our Conference Call Recap for CMG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan