Dec 15, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Costco’s (COST) Q4 2025 earnings call.

Costco (COST) operates a global chain of membership-only warehouses, serving over 81 million households with high-quality, low-priced items ranging from fresh food to clothing to fuel. Costco delivered strong Q1 results for the quarter that ended November 23, with $65.98 billion in net sales (+8.2%) and a 20.5% surge in digital sales, led by app enhancements and AI integration in pharmacy and logistics. Management addressed macro concerns by detailing strategies to mitigate potential tariffs, including sourcing adjustments and inventory optimization. While overall inflation remained stable, specific commodity costs like beef rose. Interestingly, a slight dip in global renewal rates to 89.7% was attributed to an influx of younger, digital-first members. The company reaffirmed plans for 30+ annual openings, including creative mixed-use sites, and highlighted record-breaking holiday demand, selling 4.5 million pies in the days leading up to Thanksgiving. Shares were flat on Friday, 12/12, despite better-than-expected results…

Continue reading our Conference Call Recap for COST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Dec 12, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Adobe’s (ADBE) Q4 2025 earnings call.

Adobe (ADBE) defines the standard for digital creativity and document productivity, serving solo artists to Fortune 500 marketers. Known for powerhouses like Photoshop and Acrobat, the company is aggressively pioneering the “agentic web” with Firefly AI and GenStudio. In ADBE’s Q4 2025 ended 11/28, the company reported record revenue of $23.77 billion, signaling a major inflection point in AI monetization. “AI-influenced” solutions now drive over one-third of their business, with generative credit consumption tripling quarter-over-quarter. Management discussed “agentic experiences,” autonomous interfaces that execute complex tasks, and the pending acquisition of Semrush to secure brand visibility in the age of AI search. With a bullish FY26 forecast targeting $2.6 billion in net new ARR, ADBE demonstrated that integrating third-party models alongside its proprietary Firefly engine is successfully converting AI hype into durable enterprise revenue. ADBE shares rose 2% on 12/11 after posting EPS and revenue beats…

Continue reading our Conference Call Recap for ADBE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Dec 11, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Vail Resorts’ (MTN) Q1 2026 earnings call.

Vail Resorts (MTN) is the world’s premier mountain resort operator, managing 42 destinations, like Vail, Whistler Blackcomb, and Park City, across three continents. It revolutionized the industry with the Epic Pass, stabilizing revenue against weather volatility by locking in skiers before the season starts. With millions of global guests, MTN provides insight into high-end leisure travel and the economic impact of climate variability on outdoor recreation. On the earnings call, management reiterated full-year guidance despite a “slow start” due to snowfall down nearly 60% in key western regions. While pass units fell 2%, revenue grew 3% thanks to pricing power and a mix shift toward premium unlimited products. CEO Rob Katz discussed aggressive lift ticket discounting, specifically a new 30% discount for 30-day advance purchases, to capture price-sensitive vacationers who missed pass deadlines. The company is also modernizing marketing by moving spend from traditional email to social and influencer channels. Finally, MTN confirmed its “Resource Efficiency Transformation” is outpacing targets, expecting over $100 million in annualized savings to offset inflation and tariffs impacting its $215–$220 million capital plan. The company missed EPS and revenue estimates, but investors overlooked that news and focused on a more optimistic outlook as the stock rallied as much as 8% on 12/11…

Continue reading our Conference Call Recap for MTN by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Dec 10, 2025

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 25 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

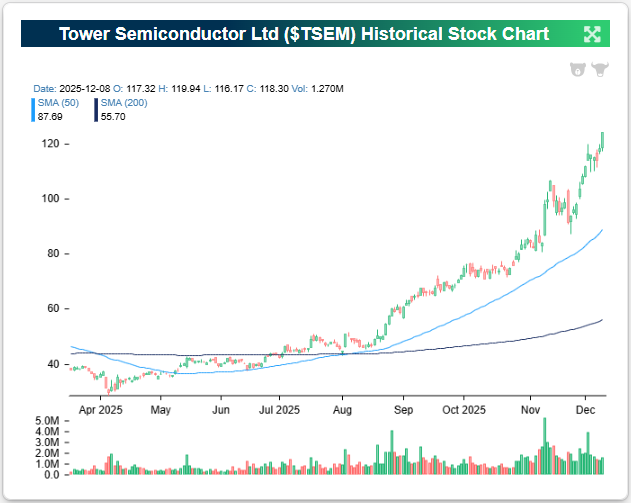

Tower Semiconductor (TSEM) is an example of a company that recently reported an earnings triple play before the opening bell on 11/10. In reaction, TSEM shares rallied 16.7% on the day. That move has helped push the stock up more than 140% YTD!

Here’s how AI describes the company: Tower Semiconductor (TSEM) is a specialized independent foundry that manufactures high-value analog integrated circuits, producing chips for customers who design hardware but do not own their own fabrication facilities. In other words, customers send TSEM blueprints, and it uses its factories to physically build those designs into finished computer chips. Instead of competing on the smallest digital processors, Tower focuses on customizing “specialty” process technologies, such as Silicon Photonics (SiPho), Silicon Germanium (SiGe), and RF-SOI, that excel at managing real-world signals like light, radio waves, and electrical power. You can think of these like the “senses” and “connectors,” rather than the main processors, “brains,” of a computer. These components are critical for optical transceivers in high-speed AI data centers, radio frequency front-ends in 5G smartphones, and power management systems in automotive and consumer electronics. Operating seven manufacturing facilities across Israel, the United States, and Japan, TSEM does not sell devices directly to consumers. Instead, it provides the essential manufacturing service and complex chemical processes needed to create these specific parts, which are then installed inside smartphones, cars, and the massive data centers powering AI.

Tower delivered a strong third quarter with revenue climbing 7% YoY to $396 million and net profit reaching $54 million, while the company raised guidance to a record $440 million for Q4 on the back of huge AI infrastructure demand. The standout performer was the Silicon Photonics segment, which creates optical interconnects for data centers, as revenue here surged 70% to $52 million and is rapidly moving toward ultra-fast 1.6 Terabit speeds that already make up nearly a third of production starts. This demand is so intense that management committed an additional $300 million investment to triple manufacturing capacity for these optical chips by late 2026. Customers are abandoning traditional lasers in favor of Tower’s silicon-based alternative because it offers better performance while requiring only half the number of lasers, making them far cheaper and more efficient.

As we touched on earlier, the stock has staged a historic run; up more than 140% YTD and roughly 325% since the April Tariff Tantrum. The stock is currently trading at its highest level in over 20 years. Wall Street has aggressively re-priced the company from a standard chip manufacturer to a critical piece of the AI supply chain. But this skyrocketing valuation creates a new challenge where expectations are now through the roof. With so much optimism already baked into the price, the company has effectively entered a zone where simply meeting estimates will likely not be enough going forward. To sustain this upward trajectory, TSEM must now likely continually deliver better-than-expected results to justify its massive run.

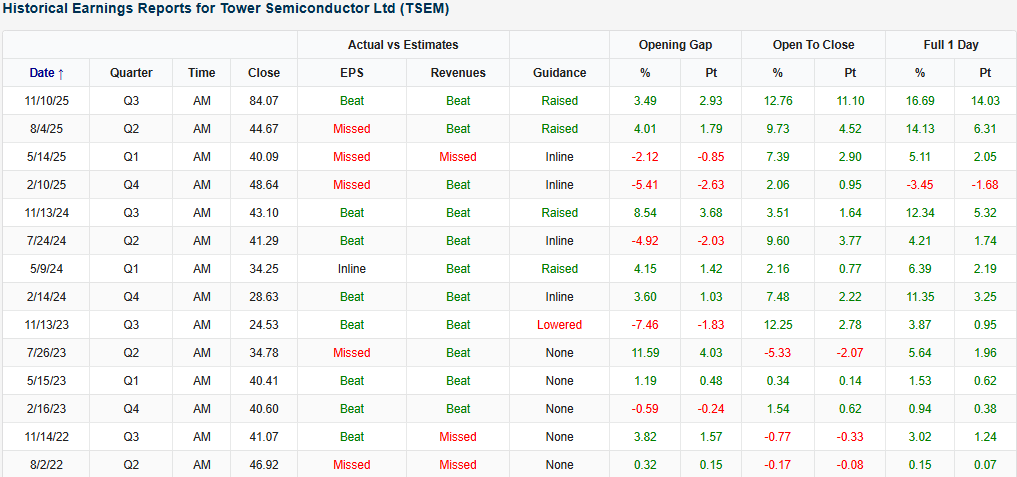

Looking at the snapshot below from our Earnings Explorer, Tower Semi (TSEM) has found a rhythm with its pace of positive reactions to earnings over the last three and a half years. The stock has risen on 13 of its 14 earnings reaction days since August 2022. EPS and revenue beat rates have been shakier, though. Although not a consistent triple play name, the company has managed a couple recently.

You can read more about TSEM and the 24 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Dec 1, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Deere’s (DE) Q4 2025 earnings call.

Deere (DE) is the world’s leading maker of agricultural, construction, and forestry machinery, serving farmers, contractors, and governments with everything from high-horsepower tractors and combines to precision sprayers, excavators, skid steers, and forestry harvesters. While farming equipment may not be traditionally associated with complex digital systems, DE is standing out with new products that incorporate automation, computer vision, satellite connectivity, and autonomy, giving investors a view into the digitization of global agriculture and infrastructure. The company’s platform, the John Deere Operations Center, now covers more than 500 million engaged acres. This quarter highlighted a tough Large Ag market, but better results elsewhere as tariffs surged to a $1.2B pretax headwind for FY26 and farm fundamentals stayed soft due to high global crop stocks and elevated input costs. Demand for biofuels was a bright spot, with US corn exports projected to hit all-time highs, and soybean crush volume set for a record year. Technology adoption grew nicely: See & Spray (Deere’s computer-vision spraying system that uses cameras and AI to detect weeds in real time and apply herbicide only where needed) covered 5M+ acres with ~50% herbicide savings, and autonomous tillage expanded toward commercial rollout. Construction markets improved with data center builds, infrastructure spending, and a 25% increase in earthmoving order books. As a result of a weaker Large Ag market, DE shares declined 5.8% on 11/26…

Continue reading our Conference Call Recap for DE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Nov 28, 2025

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Kohl’s (KSS) Q3 2025 earnings call.

Kohl’s (KSS) is a retailer serving over 60 million primarily low-to-middle-income customers through 1,100+ stores. Offering a mix of national brands and exclusive private labels like FLX, the company acts as a bellwether for middle-class discretionary spending. The partnership with Sephora has notably grown into a nearly $2 billion business. In Q3, newly appointed CEO Michael Bender reported improved momentum with comparable sales declining just 1.7%, aided by a 2.4% rise in digital sales and renewed engagement from core credit customers. Its strategy shifted back toward “opening price point” value through private labels to combat inflation fatigue. While inventory management remains strong (down 5%), KSS is anticipating a highly promotional holiday season and headwinds from potential tariffs. The company remains cautious as consumers become increasingly “choiceful” with spending. The company reported its first triple play in four years, resulting in the stock climbing 42.3% on 11/25, and another 6.5% on 11/26 before the Thanksgiving holiday! Since the April lows, the stock has almost quadrupled in value…

Continue reading our Conference Call Recap for KSS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan