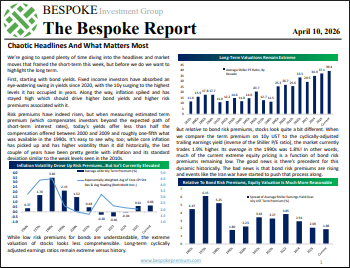

Apr 10, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. Hormuz remained closed this week but markets are working very hard to look past that fact given the huge surge in stocks and drop in energy futures. We go through the week’s chaotic headlines in detail, but keep our eye on other equity market drivers as well: economic data in the US and abroad, risk premiums (and return potential) offered by US stocks and bonds, the very strong performance of emerging markets, and the inflation outlook including the critical question of whether inflation expectations will remain anchored amidst this latest shock to consumer prices.

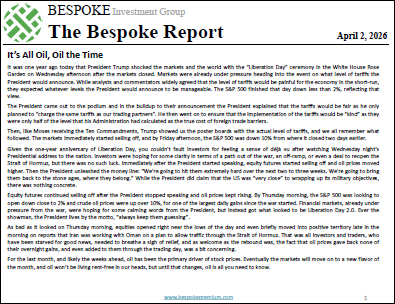

Apr 2, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week’s report comes a day early as the market is closed in observance of Good Friday. In this week’s report, we cover the market’s handcuff to oil prices, market performance during Q1, the extraordinary moves in the Energy sector, economic data since the war started, seasonality, and much more.

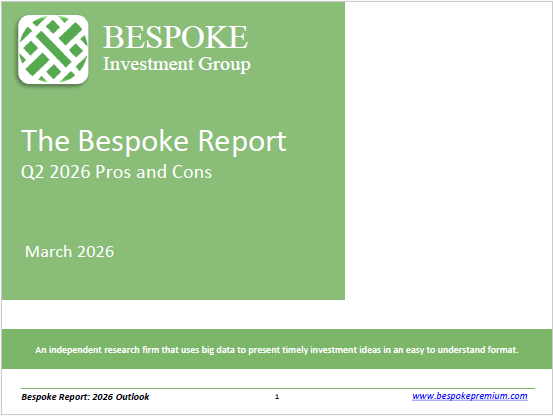

Mar 27, 2026

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q2 2026.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking.

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, start a trial to any of our three membership levels today!

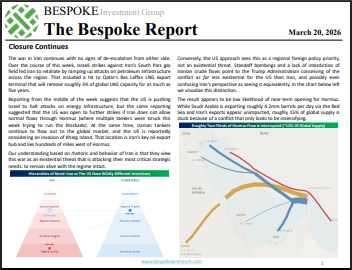

Mar 20, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we are closely focused on the three week war in Iran and its consequences for energy markets and the economy. The conflict has driven a massive surge in energy stocks around the world with US refiners especially benefitting. But broad indices have plunged into deep oversold territory as stocks reel from a sudden and extreme shift in central bank pricing. We recap a long list of central bank decisions across emerging and developed markets as well as the chaos in bonds markets that spent the week waking up to the risks for interest rates of significant global petroleum shortages. We also review economic data, which this week showed an economy with surprisingly solid labor markets, healthy balance sheets, and accelerating inflation…even before the impacts of oil price surges.

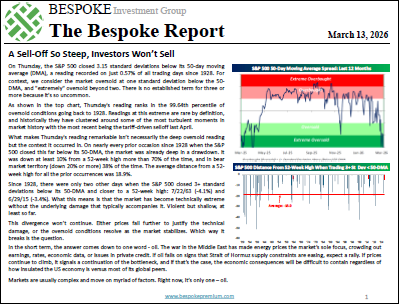

Mar 13, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. It was another eventful week in the market as we witnessed an extraordinary divergence between the S&P 500’s extreme oversold reading despite its relatively close proximity to all-time highs. This divergence won’t continue. Either prices fall further to justify the technical damage, or the oversold conditions resolve as the market stabilizes. Which way it breaks is the question. In this week’s Bespoke Report, we discuss the main factor(s) facing the market and put some of the recent moves into perspective.

Mar 6, 2026

This Week’s Bespoke Report: Oil’s Record Week, Software’s Comeback, and the Iran Fallout

It was one of the wildest weeks in recent market history. Here’s a look at what we’re covering in this week’s Bespoke Report.

Oil Just Had Its Biggest Week Ever

Crude oil surged 36% this week, the largest weekly gain since at least 1985, after US/Israeli strikes on Iran effectively shut down tanker traffic through the Strait of Hormuz. By Friday afternoon, oil was trading above $91/barrel at its most overbought level in history. In the report, we look at what has historically happened to both oil and equities after spikes like this, and how quickly the pain is likely to show up at the gas pump.

Software Bounces Back

After falling more than 22% in the first two months of 2026, the iShares Expanded Tech-Software ETF (IGV) has rallied nearly 14% in just nine trading days with remarkably steady intraday buying pressure. The Citrini essay that terrified the sector on 2/22 may have marked the clearing-out event. It’s always easier to see in hindsight, but underneath all the snow on 2/23, there was plenty of blood on the software streets. We chart the bounce and put the current streak in historical context.

A Historic Reversal in Positioning

The Iran conflict triggered what looks like a broad deleveraging across institutional portfolios. Everything that worked in January and February stopped working this week, and everything that didn’t work started working. International equities that had been trouncing the US for months got hit the hardest, while the most beaten-down US stocks rallied sharply. We break down the reversal by asset class, country, and individual stock, and we explain why the US held up better than the rest of the world.

The Three-Headed Monster Awakens

Oil, Treasury yields, and the dollar. Our “three-headed monster” indicator just surged to its highest combined level in nearly a year. Two weeks ago, the monster was still asleep. We show where current readings sit relative to 40 years of history and what it has meant for forward equity returns.

Payrolls Go Negative

Friday’s jobs report showed a loss of 92,000 nonfarm payrolls, badly missing the +55K estimate. But the headline number is misleading. A big chunk of the weakness came from a single line item that will almost certainly reverse. We walk through what’s really going on beneath the surface, including what the data says about AI’s impact on younger workers.

The S&P 500 Keeps Bouncing

The S&P 500 opened down 1% or more on three separate days this week and managed to claw back each time. That’s only happened 13 times in SPY’s history since 1993. We look at where those prior weeks fell on the chart and what happened next.

That’s just a recap of some of the topics covered in this week’s Bespoke Report, our flagship weekly newsletter. This week’s edition is 29 pages of charts, tables, and in-depth analysis. If you’d like to dive in further, you can start a Bespoke trial to read the full report and get access to all of our daily research.