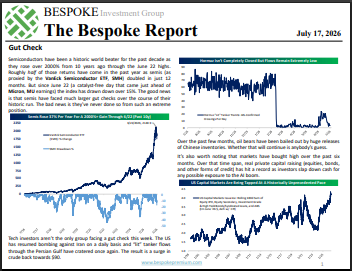

Jul 17, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report we discuss the gut check markets are facing thanks to both geopolitics and the ongoing selloff (or is it a rotation?) in the AI trade. We review charts of key single names, valuations, historical context, and the massive capital market activity that has chased price and narrative higher. We also dive into earnings, covering reports from both US and major global names this week including a gangbusters week for Wall Street’s own earnings. The Fed had a dynamic week, so we dive in to some very hawkish speeches…and the inflation data that made them a bit irrelevant. Other US data and a big slate of releases from China are discussed before we break down commodity market price action in detail.

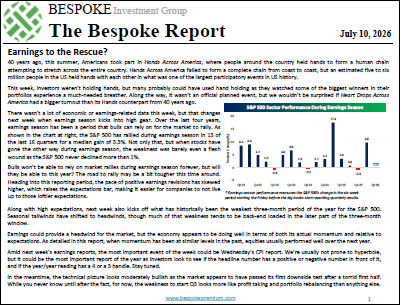

Jul 10, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report we review the market’s performance to start the quarter, and then provide a big picture look at the economy and preview earnings season. Give it a read!

Jun 26, 2026

This week’s Bespoke Report is an updated version of our “Pros and Cons” edition for Q3 2026.

With this report, you’re able to get a complete picture of the bull and bear case for US stocks right now. It’s heavy on graphics and light on text, but we let the charts and tables do the talking.

On page three of the report, you’ll see a full list of the pros and cons that we lay out. Slides for each topic are then provided on page four and beyond.

To read this report and access everything else Bespoke’s research platform has to offer, start a trial to any of our three membership levels today!

Jun 12, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report we start with a review of the successful trading debut for SpaceX (SPCX). While that event sucked up all the headlines this week, one relatively obscure US economic release was far more important and we go into detail why. We also dive into the performance of a range of stocks in our Bespoke AI Basket, review the strong year for emerging markets and which countries are driving returns, discuss Chinese economic data this week, and review the week that was in US data including inflation, housing, and labor markets. Give it a read!

Jun 5, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, choose one of our three member plans today!

This week’s report covers all you need to know about the market this week, including historic moves in major indices and an insatiable demand for equities. Give it a read!

May 29, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, choose one of our three member plans today!

This week’s report covers a market that keeps making history, a big earnings week for retailers, and a fascinating look at how private credit is financing the AI buildout. Give it a read!