This week’s Bespoke Report newsletter is now available for members.

At 1 PM ET on Thursday, the S&P 500 was trading up nicely on the day and then suddenly dropped on news headlines that President Biden’s upcoming infrastructure/tax hike proposal would include an increase in the capital gains tax on high earners from ~20% up to ~40%. It was curious that the market fell at all on this headline given that this type of tax hike was something Biden ran on during his campaign, but nevertheless, major US indices continued to fall for the remainder of the trading day to finish down roughly 1% on the day.

The worries — at least as far as the market is concerned — didn’t last long. 26 hours later at the close on Friday, the S&P 500 tracking SPY ETF closed exactly 1 cent below the level it was trading at as of 1 PM ET on Thursday!

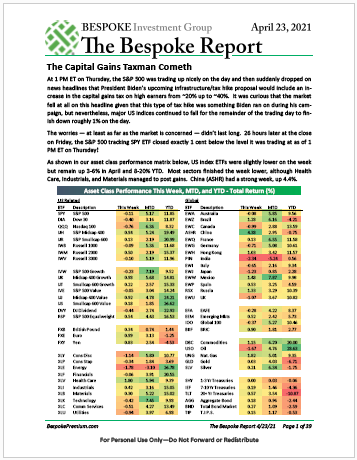

Overall, US index ETFs were slightly lower on the week but remain up 3-6% in April and 8-20% YTD. Most sectors finished the week lower, although Health Care, Industrials, and Materials managed to post gains. China (ASHR) had a strong week, up 4.4%.

As usual, this week’s Bespoke Report covers the major forces that are driving equity markets right now. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!