To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium.

The first full week of December was modestly positive, but what really added to the good feelings was a blackout of Federal Reserve speakers.

Futures currently price a 95% chance of a 25-basis point (bps) rate cut at Wednesday’s meeting, which is essentially the exact same as in late October. Given the lack of significant official economic data during this period, the stability in expectations makes logical sense. Without fresh data, how could Federal Open Market Committee (FOMC) members really change their outlook? Sometimes, though, what experts at the Fed —or elsewhere—say doesn’t fully make sense.

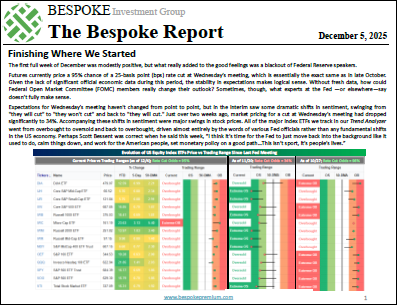

Expectations for Wednesday’s meeting haven’t changed from point to point, but the interim saw some dramatic shifts in sentiment, swinging from “they will cut” to “they won’t cut” and back to “they will cut.” Just over two weeks ago, market pricing for a cut at Wednesday’s meeting had dropped significantly to 34%. Accompanying these shifts in sentiment were major swings in stock prices. All of the major index ETFs we track in our Trend Analyzer went from overbought to oversold and back to overbought, driven almost entirely by the words of various Fed officials rather than any fundamental shifts in the US economy. Perhaps Scott Bessent was correct when he said this week, “I think it’s time for the Fed to just move back into the background like it used to do, calm things down, and work for the American people, set monetary policy on a good path…This isn’t sport, it’s people’s lives.”

This week’s Bespoke Report is packed with interesting market trends, so give the full report a read by starting a trial here.