Jan 30, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think in terms of next year, our constraints, I think it’s likely to be just regulatory.” – Elon Musk

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

When you see a quote like the one above from Tesla’s conference call last night, it’s understandable why Elon Musk took such an active role in last year’s Presidential election. The chart below is from our annual outlook published in December and shows the annual number of pages in the Published Code of Federal Regulations since 1950. While death and taxes are the only certainties in life, the growth of government is right up there. For nearly every year since 1950, the number of pages in the published code has increased, and for the most recent year available (2023), it hit a record high of over 190,000. As we highlighted in our outlook back in December, the potential for a halt or slowdown to what has essentially been uninterrupted growth in government over the last several decades is certainly a pro.

Jan 28, 2025

In listening to discussions over the market’s reaction to the DeepSeek sell-off yesterday, the term “shoot first, ask questions later” came up repeatedly. However, in looking at the performance of various indices and individual stocks yesterday, the market’s behavior looked more discerning than indiscriminate. At the individual stock level, most stocks in the S&P 500 finished the day higher, and the weakness was concentrated to stocks that have benefitted the most from the AI rally.

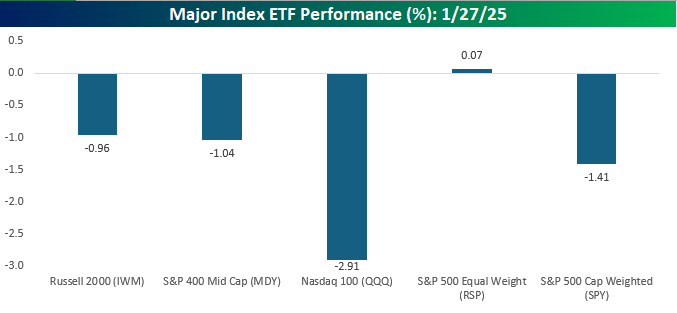

The chart below shows yesterday’s performance of major US index ETFs. As you would expect, the Nasdaq 100 with its concentration in technology was the hardest hit, falling by close to 3%. The cap-weighted S&P 500 (SPY) also declined more than 1% given its large weighting in Nvidia (NVDA) and other tech companies. The equal-weight index (RSP), however, finished the day in positive territory with a modest gain. The one index where performance was not as we expected was in small caps where the Russell 2000 (IWM) also fell nearly 1%. On a day when mega-cap tech was crushed but the majority of large-cap stocks rallied and interest rates declined, we would have expected small caps to show more strength. Given the entire Russell 2000 is smaller than NVDA, it doesn’t take much to get this area of the market to rally. Also, if DeepSeek means that the previous costs associated with adopting AI are now dramatically lower, shouldn’t that be good for small caps which presumably have smaller budgets?

Looking at the performance of these major index ETFs over the last week, outside of QQQ, they’re all still positive, even after Monday’s decline. Additionally, they’re also all trading right within the confines of their normal trading ranges (none are oversold or overbought) which is a level of homogeneity that it feels like we don’t see much these days.

The Russell 2000’s lack of a rally came within the context of a week-long period where IWM has been unsuccessfully attempting to break back above its 50-DMA. Yesterday marked the fifth straight day where it tested that level but failed to close above it.

The mid-cap ETF (MDY) finished well off its intraday high yesterday and also traded below its 50-DMA but managed to close the day just barely above that level.

The 50-DMA also acted as support for the S&P 500. After opening right at that level in the morning, the large-cap benchmark bounced throughout the session and finished at the highs of the session.

The chart of the Equal Weight S&P 500 (RSP) over the last few days looks similar to small caps with a tight range. The only difference is that, unlike IWM, RSP has closed above its 50-DMA for each of the last four trading days.

Finally, the Nasdaq 100 (QQQ) was the biggest pain point of the major indices. It started the session below its 50-DMA and made an attempt to rally back above that level intraday but came up just short by the time the closing bell rang. While QQQ failed to take out its December high in last week’s rally, it did manage a higher high, and as long as yesterday’s decline doesn’t see much in the way of follow-through, it isn’t in imminent danger of a lower low in the short-term.

Jan 27, 2025

This content is for members only

Jan 27, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The music is not in the notes, but in the silence between.” – Mozart

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 finished last week with its second straight weekly gain, and it was the first week of back-to-back 1.5%+ advances since mid-May as the S&P 500 managed to close at an all-time high last Thursday. Since the S&P 500 ETF’s (SPY) closing low on 1/10, the large-cap benchmark is up 4.73% while the Nasdaq 100 ETF (QQQ) has rallied by a similar amount (4.42%). Moving down the market cap spectrum, mid-caps (MDY) have rallied 5.64% while small caps (IWM) are up 5.47%. The leader has been micro-caps, though, as the Russell 2000 micro-cap ETF is up 5.75%.

Much of those gains from the last two weeks have been erased over the weekend as both the S&P 500 and the Nasdaq 100 are indicated to open sharply lower on concerns over DeepSeek upending the entire investment landscape for AI. News of DeepSeek first dropped around Christmas and started to pick up steam early last week as articles reported that the model has achieved comparable progress in AI to the most advanced US models for fractions of the cost. Articles published over the weekend have hit a nerve, resulting in a massive sell-off in mega cap US stocks.

If the reports of DeepSeek’s success at such low costs are true, and this is a big if as there is still a lot we don’t know in terms of how it was developed, it would pose problems for some of the biggest AI winners over the last two years. As we type this, the S&P 500 (proxied by SPY) is trading down about 2.25% which would be the largest downside gap since early August and the 60th largest downside gap in the ETF’s history dating back to 1993.

For the Nasdaq 100 (QQQ), the declines are even steeper. With the ETF poised to gap down 3.8% at the open, it would be QQQ’s largest downside gap since early August and the 20th largest downside gap since its inception in 1999. As shown in the chart below, before last August’s downside gap, the last time QQQ gapped down as much as it on pace to today was back in September 2020.

Among the mega cap stocks, this morning’s declines aren’t uniform. The chart below shows where each trillion-dollar market cap stock is trading this morning relative to Friday’s close. Leading the way to the downside, Broadcom (AVGO) and Nvidia (NVDA) are both down by double-digit percentages. These have been the biggest AI winners, so it’s no surprise that investors are selling them the fastest. Microsoft (MSFT) has also declined more than 5% given its close relationship with OpenAI. One name that has barely been impacted by the overnight sell-off is Apple (AAPL); in pre-market trading, it’s down less than 1%. Ironically, all anyone could talk about last week concerning AAPL was how it’s overvalued and missed the boat on AI. Today, that lack of investment in AI is being looked at as a plus!

Jan 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“One of the most helpful things that anybody can learn is to give up trying to catch the last eighth—or the first. These two are the most expensive eighths in the world.” – Edwin Lefèvre, Reminiscences of a Stock Operator

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Here in the US this morning, US futures are biased to the downside as markets digest what is expected to be the second week in a row of gains. Earnings season has continued on a bullish note with positive earnings from the banks and financials last week and then strong reports from Netflix (NFLX), 3M (MMM), Charles Schwab (SCHW), and P&G (PG) this week. Next week will be an even bigger test as the pace of reports will only increase and megacaps like Meta Platforms (META), Microsoft (MSFT), Apple (AAPL), and Amazon.com (AMZN) will all report.

If you’re still reading this, congratulations because that means you survived the ‘December crash’. The S&P 500 declined 4.3% from its December high to early January, which was admittedly accompanied by the weakest short-term period of market breadth since at least 1990. The rally that kicked off Monday has now fully erased the declines, and the bull market has gone on to live another day (or week, month, year, etc.). For many investors, the pullback felt especially painful even if it was modest in magnitude. As shown in the chart below, since the bull market began in October 2022, there were five other periods when the S&P 500 experienced a decline that was both larger in magnitude and longer in duration.