Bespoke’s Morning Lineup – 7/14/25 – Letters

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Any fool can make something complicated. It takes a genius to make it simple.” – Woody Guthrie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The President’s letter-writing campaign to global trading partners continued over the weekend with notifications sent to Mexico and the EU informing them that if no trade deals are reached before August 1st, they will face tariffs of 30% on all products sold into the US. When these types of rates were first announced in April, they nearly pushed the S&P 500 into a bear market. This morning, S&P 500 futures are down just fractionally and within a couple of percentage points of all-time highs. Investors are betting that tariff rates at these levels will never go into effect, and while 30% is the unlikely long-term figure, the lack of concern today is the opposite of the panic three months ago.

Along with the weakness in US futures, European stocks are also trading down fractionally. Germany, the largest exporter in the EU, is leading the way down with a decline of 1%. Overnight, in Asia, most markets were also fractionally lower, so it’s not just US investors who are yawning at the latest batch of letters from the President.

The most action this morning is once again in the crypto pace as Bitcoin continues its march to record highs and traded well over $120K. Ether has also been getting in on the act with a 2% rally this morning and back above $3K.

Besides tariffs, the upcoming week will be an important one on the economic front with the release of June CPI (Tuesday) and PPI (Wednesday). Economists have been waiting (and waiting) for tariffs to push inflation readings higher, but those concerns have yet to manifest themselves in the official numbers.

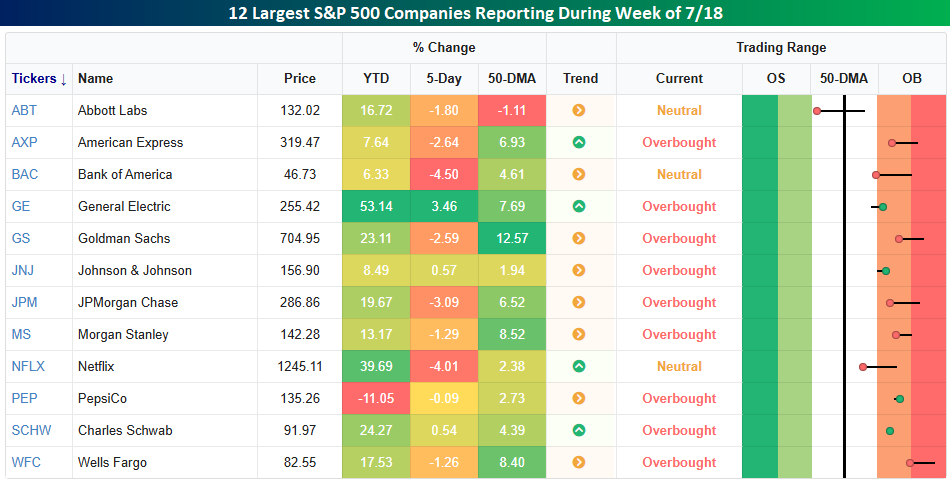

Tariffs are driving headlines this morning, but earnings (which will ultimately at least be partly impacted by tariffs) will start grabbing headlines beginning this week as Q2 earnings season gets underway. The major banks and brokers will be the main area of focus for the week. Still, other notable non-financial sector stocks reporting include Johnson & Johnson (JNJ) on Wednesday, and then Netflix (NFLX), General Electric (GE), Abbot Labs (ABT), and Pepsi (PEP) on Thursday.

The S&P 500 finished last week down by 0.3%, but of the 12 largest S&P 500 companies scheduled to report, eight of them underperformed the S&P 500 last week, indicating that some investors took profits after the strong runs they had over the last three months. That can be considered a modest positive as it suggests investors aren’t being overly complacent ahead of their respective reports. They have still mostly performed well over the last three months, though. As shown in the snapshot below, nine of the twelve stocks shown finished the week at overbought levels (1+ standard deviation above their 50-DMA), and only ABT is below its 50-DMA.

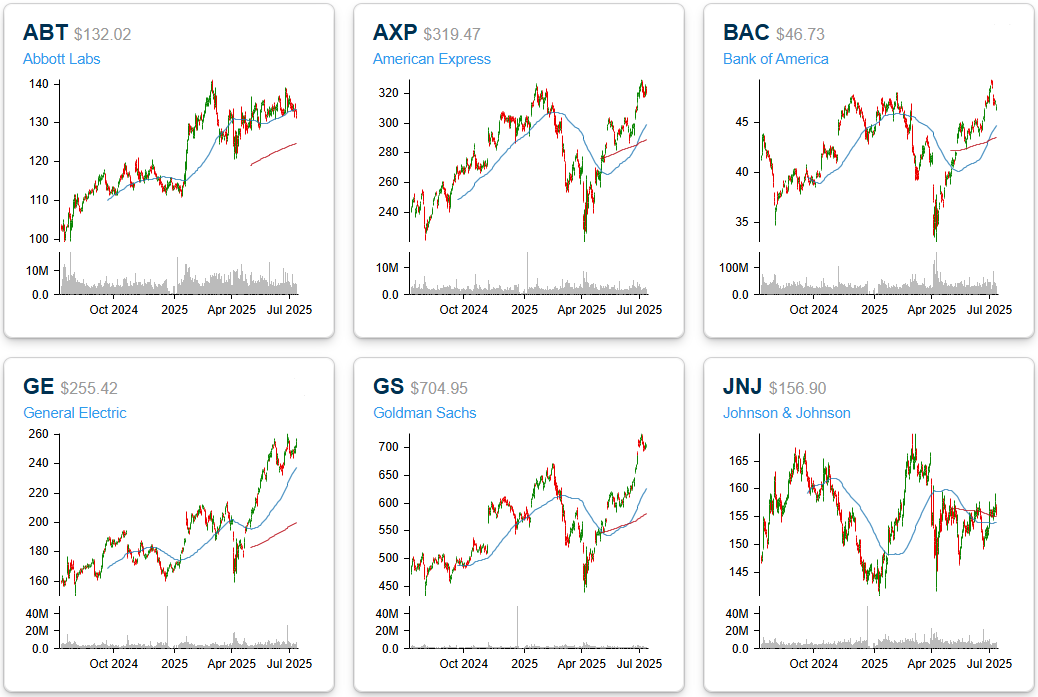

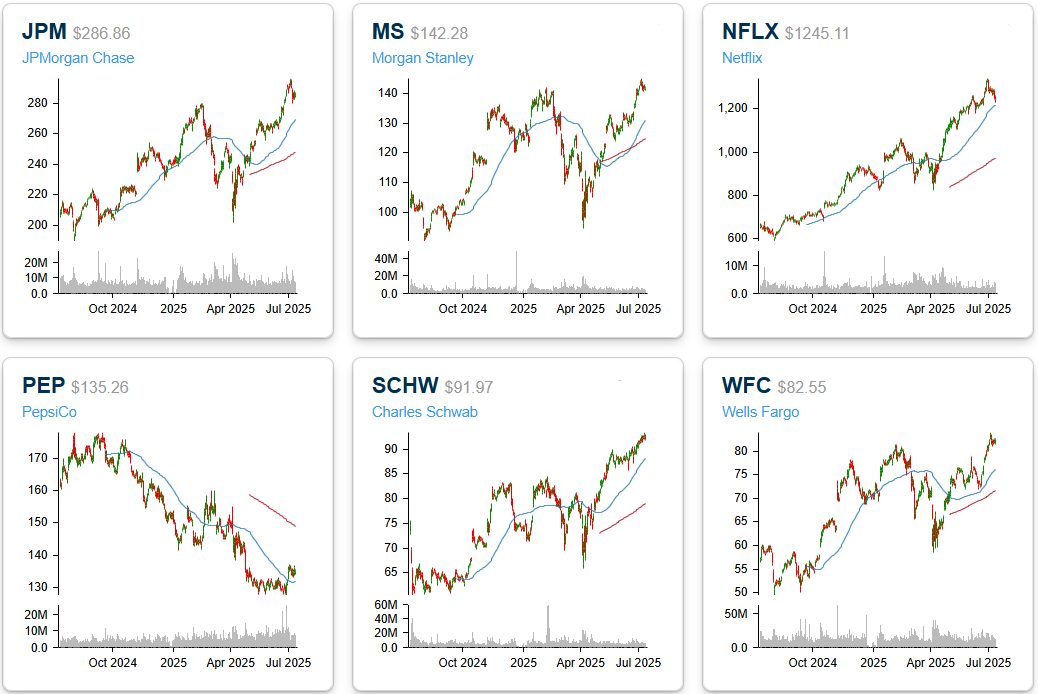

Below we show one-year charts of each of the twelve largest stocks scheduled to report earnings this week. Except for JNJ and PEP, all twelve are either at or not far from 52-week highs. Goldman Sachs (GS) is one name that has seemingly gone parabolic over the last three months. Despite trading down 2.6% last week, the stock is still up over 40% since its last earnings report in April, which ranks as the three strongest performances between earnings reports for the stock on record.

The Bespoke Report – 7/11/25 – Between Extremes

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report, we cover everything happening across financial markets as the market digests some tremendous three-month gains..

Bespoke’s Morning Lineup – 7/11/25 – Tariff Troubles

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Try and fail,but don’t fail to try.” – John Quincy Adams

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 hit another record high yesterday as certain speculative areas of the market continued to surge. This morning, though, bulls are taking a break as the latest round of tariff announcements from the President set the stage for a negative end to the week. The latest announcement causing the damage is a 35% tariff announcement on Canadian imports in what the President says is a response to the country allowing fentanyl to cross the border into our country. He then added that the 35% levy will go even higher is Canada retaliates. More broadly, President Trump also said he was planning blanket tariffs of 15% to 20% on any countries he hasn’t already sent letters to.

Futures are negative in response with the S&P 500 and Nasdaq indicated to open down 0.5% at the open. Treasury yields are also higher, but the 10-year yield remains below 4.4%. Crude oil and gold are both up 1%, but the gains in other precious metals like silver, platinum, and palladium are even larger at 3%+. The biggest moves to the upside are in the crypto space as Bitcoin is surging close to 4% at a record high of just under $118K while Ethereum is trading just under $3,000 with a gain of 6%.

Like the declines in US futures, Asian markets were mostly lower last night on concerns related to the latest Trump Tariff announcements. Those losses also overflowed into Europe as the STOXX 600 faces a decline of nearly 1% to close out the week.

In terms of what is leading the market, mega-caps remain in charge. The chart below shows the relative strength of the S&P 500 equal-weight (RSP) vs market cap weight (SPY) indices. When the line rises, it indicates outperformance of the equal-weight index, while a falling line indicates that the market-cap-weighted index is outperforming. At this time last year, RSP was in the middle of a short-term burst of massive outperformance, but the gains were fleeting, and by the end of the year, RSP had given up all of its outperformance relative to SPY. In the first quarter of this year, RSP outperformed again, but just like the fourth quarter of last year, the second quarter of this year saw RSP once again give up all of its outperformance. At one point, RSP will take the lead and keep it for a while, but for now, SPY keeps retaking the lead.

Looking ahead, depending on your time horizon, the calendar is either a good friend or an adversary. Over the last ten years, the S&P 500’s median performance in the week following the close today has been a gain of 1.32% and ranks in the 93rd percentile of all one-week periods throughout the year. Over the next three months, though, the S&P 500’s median gain of 0.64% ranks in just the 15th percentile as the months of September and October become a larger part of the three-month view.

Bespoke’s Morning Lineup – 7/10/25 – Earnings Season Starts With a Thud

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you don’t fail sometimes, you are not being ambitious enough.” – Sundar Pichai

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After several days with little in the way of economic or earnings data, this morning we’ll get reports on jobless claims, and we’ve already seen a handful of earnings reports. Of the four companies reporting earnings this morning, two reported better than expected EPS, three missed sales forecasts, and two lowered guidance. Maybe we would have been better off with no data! In response to the reports, we’ve seen some large moves. Helen of Troy (HELE), which reported a reverse triple play, is down over 20% while Conagra (CAG) and Simply Good Foods (SMPL) are both down over 4%. The only one of the four stocks trading higher in reaction to its report is Delta (DAL). That stock is flying over 13% in pre-market trading.

While these individual names have seen large reactions, overall, equity futures are up or down 0.05% or less, and treasury yields have barely budged. Crude oil is down less than 1% while gold, silver, copper, and platinum are all firmly higher.

Asian stocks were mixed, with Japan and India both down nearly 0.5% while China was up by a like amount. A former BoJ official made comments that there will likely be no more rate hikes until early 2026, while the Bank of Korea kept rates unchanged. In Europe, equities are moving higher as mining companies fuel a 0.6% rally in the STOXX 600 and a more than 1% rally in the FTSE 100.

Yesterday, we highlighted some of the massive moves in various metals like gold this year. This morning, we’ll shift our focus to Bitcoin, aka digital gold, which has also been performing very well. While Bitcoin’s performance this year looks like more of a sideways move, it’s still up a respectable 18% YTD and hit a record high yesterday. This morning’s price, right around $111K, leaves Bitcoin right near the resistance it has been dealing with since late last year. A breakout above $112K would complete a cup and handle formation, setting the stage for a new leg higher.

Just as bitcoin prices have been looking to break out from resistance, Bitcoin treasury company MicroStrategy (MSTR) has also been dealing with resistance right around $425 since late last year. Without getting into the valuation of the stock or the premium it trades at relative to its underlying crypto holdings, a move above $425 could set the stage for a new leg higher and a test of its post-Election highs from last year.

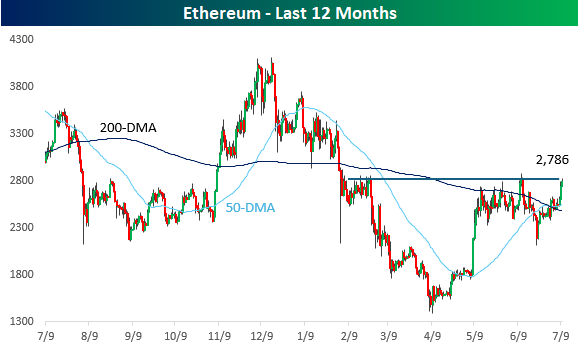

If Bitcoin is the ‘gold standard’ of the crypto space, Ethereum would be the silver standard, and price action has been much more subdued. While prices have rallied in recent weeks as digital tokens have gained in popularity, Ethereum remains more than 20% below its post-election highs. Prices are up over 7% in the last two days but remain below short-term resistance at the $2,800 level.

Throughout its history, Ethereum has been no stranger to large drawdowns. As shown in the chart below, since 2018, it has only been within 10% of a high on 6% of all days, and on average, it has traded in a drawdown of 53%! That means that the current 42% drawdown from its last record high in late 2021 is more modest than average! No one ever said the crypto space was an area of stability!